Puerto Rico: Left On An Island

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMofongo, the national dish of Puerto Rico, is not for those on a diet. Fried plantains are mashed with a little bit of pork fat and then formed into a cup that serves as a vessel for shrimp, vegetables or (preferably for me) more pork. A few chicharrones on top, and I am in heaven.

What many don’t realize is that mofongo is regional American cuisine. Puerto Ricans are U.S. citizens, they vote in presidential primaries, and thousands of them have served honorably in the American army. The island’s legal status is complicated; it is neither a state nor a sovereign. But the ties that bind Puerto Rico and the United States are deep and longstanding.

This background is important as Congress considers granting aid to Puerto Rico in the wake of Hurricane Maria. This isn’t just a matter of moral calculus, though. Given the potential financial and economic costs of inaction, providing generous support to the island would be a wise investment.

The current situation in Puerto Rico cannot be fully understood without a bit of a history lesson. The United States gained control of the island in 1898, and immediately saw its value as a bulwark against Latin incursion. (Later, the association was seen as a check against the spread of communism in the Western Hemisphere.) Puerto Ricans were granted citizenship exactly 100 years ago, just in time for the World War I draft.

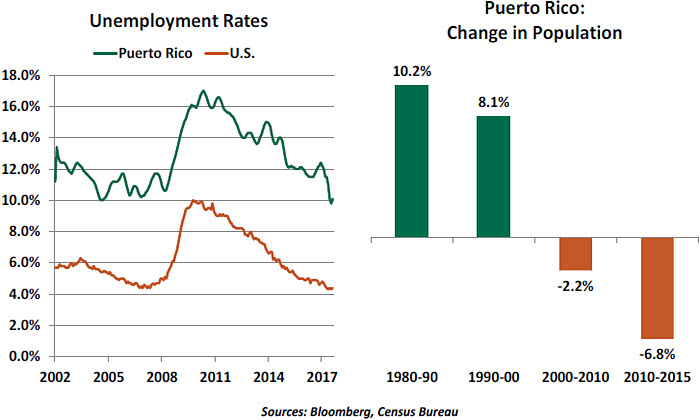

Historically, the island has received a lot of economic support from Washington. For many years, U.S. firms were provided an exemption from taxes on profits earned in Puerto Rico. This led to significant amounts of industrial investment, with drug companies in the forefront. Congress voted to phase out this favorable treatment over a ten-year period beginning in 1996. This had a predictable impact on investment and employment in Puerto Rico. Debt grew, taxes rose and citizens left, a vicious cycle that eventually led to insolvency.

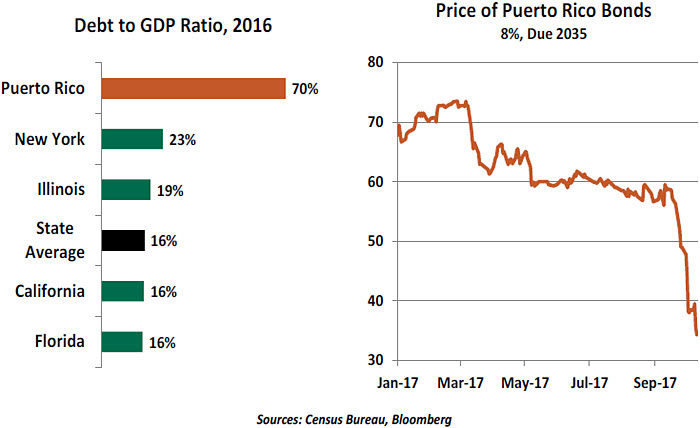

Puerto Rico is an “overseas territory” of the United States. This falls short of statehood, which creates an important financial distinction: the island cannot access the debt resolution process available to U.S. states. Puerto Rico defaulted on its bond obligations in 2016; last May, the governor filed to restructure $74 billion in public debt.

Last year, the Puerto Rico Oversight, Management and Economic Stability Act (PROMESA) established an oversight board to sort out the government’s finances. One of Puerto Rico’s biggest obligors is the Puerto Rican electric utility, which is $9 billion in debt. This burden has limited its ability to maintain capacity (let alone modernize it). Austerity programs curbed infrastructure spending further.

And then the rains came. Hurricane Irma hit Puerto Rico with a glancing blow and Hurricane Maria scored a direct hit. After years of deferred maintenance and under-investment, the island’s infrastructure was ill-prepared to withstand the wrath of nature. The power grid has been decimated, telecommunications remain spotty and poor roads have hindered transportation of relief supplies.

For residents of Texas and Florida, the damage done by Harvey and Irma is likely to total about $3,000 per resident. For Puerto Rico, Maria’s damage is projected to amount to $10,000 per resident. And Puerto Rico’s per capita income is about half that of the continental U.S.

With recovery likely to be prolonged and economic prospects uncertain, there is ample temptation for Puerto Ricans to migrate to the continental United States. (Barely half of all Americans understand that passports and visas are not needed for this transition.) Several hundred thousand people could choose to move north; assimilating these migrants will not be easy for the communities in which they settle.

Those who choose to depart are likely to be among the younger and better educated, accelerating a skewing of the Puerto Rican population that would further hinder efforts to rebuild the local economy. The public pension shortfall, already at $50 billion, would get worse. If the island is unable to generate sufficient commerce, the bill for aid would be greater, putting bondholders at risk for larger losses.

The case of Puerto Rico demonstrates what happens when fiscal problems and out-migration become intertwined. As we have seen elsewhere (in places like Greece), severe austerity is not the solution. We may see this situation repeated on the U.S. mainland before long, given the sorry financial state of some U.S. states. So the magnitude and design of support for Puerto Rico may establish a framework for future assistance programs.

Some in Washington blame the territory for failing to develop new industries that could compensate for the sunset of tax preferences a decade ago, and criticize Puerto Rico’s legislature for poor fiscal management. They fear offering support will be seen as a bailout, and that monies offered will be poorly spent.

Others, though, see aid to Puerto Rico as an investment in the island’s economy that could slow, or eventually reverse, its decay. Renewed prosperity could lure talent back home and restore financial stability. In essence, the cost of rebuilding Puerto Rico could be lower than the cost of leaving the island to fend for itself.

Late this week, the House passed a broad hurricane relief plan that included loans to Puerto Rico. The amounts are very modest, though, and represent a small down payment at best. Ultimately, Congress will need to wake up and smell the mofongo.

Breaking Up Is Hard To Do

My daughter studied abroad in Barcelona. Perhaps I should qualify that somewhat: she was in Barcelona for four months, and she was registered for classes there. And I suppose she did study, although photos from that era suggest that the subjects she was most immersed in weren’t always the most academic.

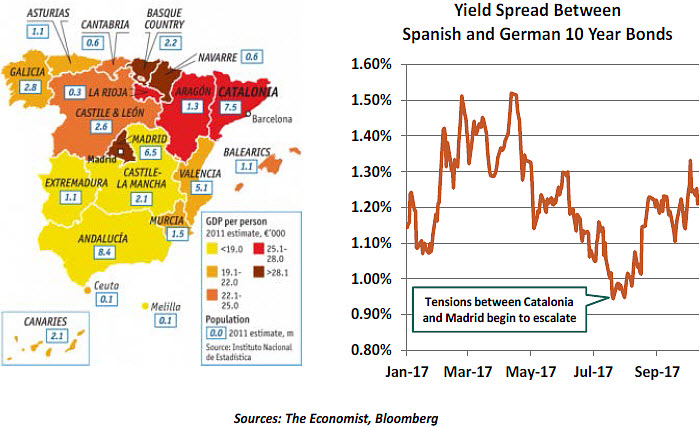

But the cultural education she got was a rich one. Catalonia, the region where Barcelona is located, was an independent nation until captured by the king of Spain a little over 300 years ago. Ever since, it has retained its unique culture and language. A portion of Catalonia briefly separated from Spain prior to World War II, only to be reconsolidated by force.

Even after Spanish regions were given more autonomy forty years ago, Catalonia has had an uneasy relationship with the central government in Madrid. The roots of recent antipathy are not cultural, but economic. The region is arguably the most prosperous in the country, and therefore finds itself paying a large portion of national taxes. Catalans resent sending resources to Madrid, which it sees as misusing the funds and mismanaging the Spanish economy.

In the past year, however, Spain has been performing solidly, as we discussed here. Economic reforms are taking root; real growth is running near 3% per year; and unemployment has been declining. The premium of Spanish interest rates over other European sovereigns has been shrinking, and the main Spanish stock index is 18% higher than it was a year ago.

Catalonia’s independence referendum, and the hard line reaction it provoked from Madrid, has introduced unwanted uncertainty. Spanish markets have been in retreat ever since, and several regional banks have announced plans to move their headquarters out of the province.

Disentangling one member from an economic cooperative is a very difficult exercise. Catalonia is deeply indebted, and more than 70% of that debt is held by the central Spanish government. An independent region would have to find outside buyers for its bonds. Catalonians rely on the federal government for defense, infrastructure and other social benefits. These would not be easily recreated.

The European Union (EU) would not look kindly on separation, and it is unlikely that Catalonia would be granted membership. (A more beneficent response might provide temptation for other breakaways in the years ahead.) This would place the region in a poor position with regard to international trade. Catalonia would also have to create its own currency and its own central bank, which would bring another set of potential perils. Residents would lose their right to work elsewhere in the EU without permits and could be required to obtain visas to travel elsewhere in Europe.

These sorts of issues were a deterrent for Scots as they approached their own independence referendum in 2014. The current confusion surrounding the Brexit negotiations serves as an additional warning to those who think they can go it alone. Given the new nationalism present in so many places, this is certainly not an opportune time to be seeking new trade agreements.

As of this writing, the government of Catalonia has opted to seek negotiations with Madrid instead of declaring outright independence. That is probably the best outcome for all stakeholders, but there may be twists and turns ahead before things truly settle.

For a long while, the display of the Catalan flag was forbidden by Madrid. It appeared clandestinely, though, in the crest of FC Barcelona. History adds extra weight to the El Clásico matches between Barça and Real Madrid; here’s hoping that Spain’s provincial battles remain confined to the pitch.

Ain’t Misbehaving

When I saw the movie “The Big Short,” I proved (once again) that I am a nerd. In a scene that attempted to explain pre-crisis finance, the pop singer Selena Gomez was seated at a blackjack table next to an economist, Richard Thaler. Ms. Gomez has 53 million followers on Twitter; Thaler has about 100,000. Nonetheless, I yelled across the theater: “Hey! That’s Richard Thaler!”

Thaler has probably picked up a few followers since last Monday, when he was awarded the 2017 Nobel Prize in Economics. (By coincidence, we published a long essay on his work just two weeks ago: “Misbehavior Complicates Economic Outcomes.”) Thaler is the third behavioral economist to earn a Nobel Prize; Daniel Kahneman and Robert Shiller preceded him. The recognition is a clear sign that economic models predicated on the assumption that people behave sensibly and efficiently are in need of review.

Psychologists who began questioning economic dogma were initially scorned. By some accounts, Thaler had a difficult integration into the faculty at the University of Chicago, the bastion of neoclassical economic thought. But he won over doubters with rigorous research that supported his conclusions.

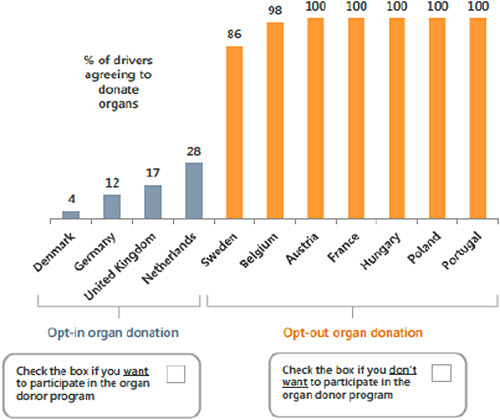

Thaler has worked to apply his learnings to public policy. He has been a vocal advocate of automatic enrollment into retirement and organ donation systems, a shift that has increased participation significantly. The transition from “opt-in” to “opt-out” regimes has proven beneficial to both individuals and to society.

Thaler has inspired scores of acolytes. He helped to found the U.K. Behavioral Insights Team (known as the “Nudge unit,” after the title of one of Thaler’s books), which continues its efforts to this day. Similar groups have been chartered in other countries, seeking ways to steer behavior in subtle but effective ways.

Thaler has taken pains to say that classic economic models should not be thrown away. Incentives still matter, and the interaction of supply and demand curves is still critical to the achievement of equilibrium. But behavioral factors have a huge impact on how and where the two curves intersect. Taking better account of these imperfections is a challenge for those of us working in the field.

When asked how he would spend the approximately $1.1 million that comes with the award, Thaler fittingly responded: “as irrationally as possible.” He has certainly earned the right to be reckless.

© 2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures. Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All