My good friend Pierre Lassonde, cofounder and chairman of Franco-Nevada, doesn’t know how we’ll replace the massive gold deposits of the past 130 years or so. Speaking with the German financial newspaper Finanz und Wirtschaft this month, Pierre says we’re seeing a significant slowdown in the number of large deposits being discovered. Legendary goldfields such as South Africa’s Witwatersrand Basin, Nevada’s Carlin Trend and Australia’s Super Pit—all nearing the end of their lifecycles—could very well be a thing of the past.

Over the medium and long-term, this could lead to a supply-demand imbalance and ultimately put strong upward pressure on the price of gold.

According to Pierre:

If you look back to the 70s, 80s and 90s, in every one of those decades, the industry found at least one 50+ million ounce gold deposit, at least ten 30+ million ounce deposits and countless 5 to 10 million ounce deposits. But if you look at the last 15 years, we found no 50 million ounce deposit, no 30 million ounce deposit and only very few 15 million ounce deposits.

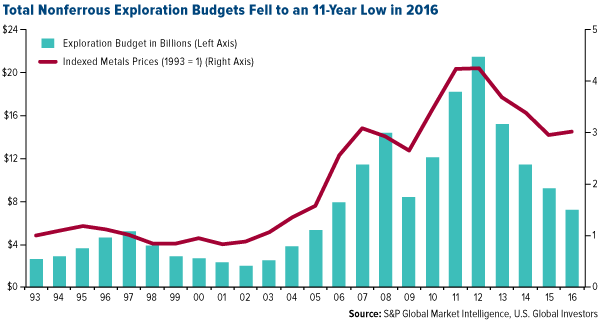

So few new large mines are being discovered today, Pierre says, mostly because companies have had to slash exploration budgets in response to lower gold prices. Earlier this year, S&P Global Market Intelligence reported that total exploration budgets for companies involved in mining nonferrous metals fell for the fourth straight year in 2016. Budgets dropped to $6.9 billion, the lowest point in 11 years. Although we’ve seen an increase in spending so far this year, it still dramatically trails the 2012 heyday.

click to enlarge

And because it takes seven years on average for a new mine to begin producing—thanks to feasibility studies, project approvals and other impediments—output could recede even more rapidly in the years to come.

“It doesn’t really matter what the gold price will do in the next few years,” Pierre says. “Production is coming off, and that means the upward pressure on the gold price could be very intense.”

Have We Reached Peak Gold?

What Pierre is talking about, of course, is the idea of “peak gold.” I wrote about this last year and suggested another factor that could be curtailing new discoveries—namely, the low-hanging fruit has likely already been picked. Gold is both scarce and finite—one of the main reasons why it’s so highly valued—and explorers are now having to dig deeper and venture farther into more extreme environments to find economically viable deposits.

Other factors contributing to the decline include tougher regulations and higher production costs. And unlike with the oil industry, no “fracking” method has been invented yet to extract gold from hard-to-reach areas, though Barrick—the world’s largest producer by output—has been experimenting with sensors at its Cortez project in Nevada.

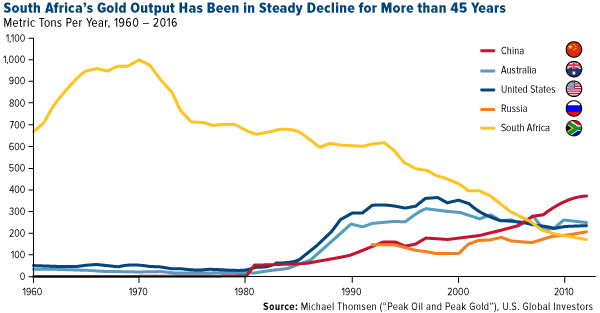

Take a look at how drastically annual output has fallen in South Africa, once the world’s top gold-producing country by far. In the 1880s, it was the discovery of gold in South Africa’s prolific Witwatersrand Basin—responsible for more than 40 percent of all gold ever mined in human history, if you can believe it—that helped transform Johannesburg into one of the world’s largest and most populous cities. Today, South Africa’s economy is the most advanced and stable in Sub-Saharan Africa, all thanks to the yellow metal.

In 1970, miners dug up more than 1,000 metric tons—an unfathomably large amount. Since then, production has steadily dropped. No longer in the top spot, South Africa produced only 167.1 tons in 2016, an 83 percent plunge from the 1970 peak. Meanwhile, miners in the notorious Mponeng mine—already the world’s deepest at 2.5 miles—continue to follow veins even deeper into the earth at greater and greater expense.

click to enlarge

Australia could soon be seeing a similar downturn over the next four decades. A first-of-its-kind study conducted by MinEx Consulting and released this month, shows that Australia’s gold production is expected to see a significant drop between now and 2057. By then, all but four of the 71 currently operating mines in the country will be exhausted. Most of these will close in the next couple of decades. Any additional production will be dependent on new exploration success, which will become increasingly difficult if companies don’t invest in exploration and if the Australian government doesn’t relax rules in the mining space.

MinEx estimates that “for the Australian gold industry to maintain production at current levels in the longer term, it will either need to double the amount spent on exploration or double its discovery performance.”

To be fair, large discoveries haven’t disappeared entirely. Back in March it was reported that Shandong Gold Group, China’s second-largest producer, uncovered a deposit in eastern China containing between 380 and 550 metric tons of the yellow metal. If true, this would make it the country’s largest ever by amount. The mine has an estimated lifespan of 40 years once operations begin.

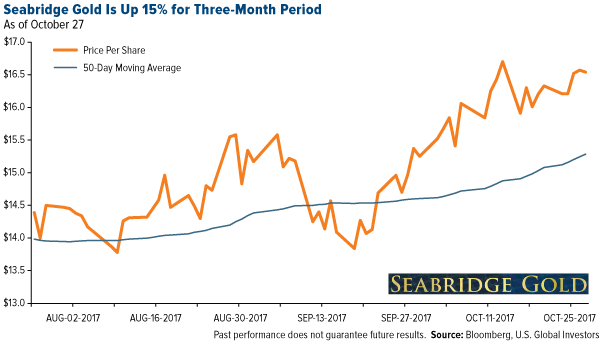

In addition, Kitco reports this month that Toronto-based Seabridge Gold recently stumbled upon a significant goldfield in northern British Columbia. The find appeared, coincidentally, after a glacier retreated. It’s estimated to contain a whopping 780 metric tons.

“There’s no question that as glaciers retreat, more ground will become available for exploration and more discoveries could be made in that part of the world,” Seabridge CEO Rudi Fronk told Kitco.

The company already has the permits to begin mining.

click to enlarge

Exploration Budgets Jumped

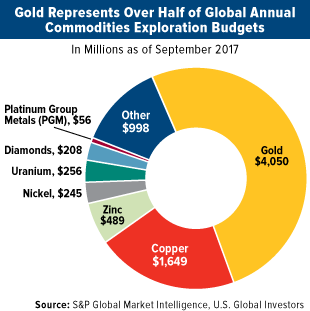

As I said earlier, we just saw an encouraging spike in the amount spent on exploration. According to S&P Global Market Intelligence, exploration budgets increased in the 12-month period as of September for the first time since 2012. Budgets jumped 14 percent year-over-year to $7.95 billion, with gold explorers leading the way. During this period, gold companies spent around $4 billion on exploration, which is roughly half the value of all nonferrous metals mining budgets.

But because exploration is getting more expensive for reasons addressed earlier, senior producers might very well decide instead to acquire smaller firms with proven, profitable projects.

This could create a lot of value for investors, so I would keep my eyes on juniors that look like targets for takeover. Dealmaking in the Australian mining industry, for example, is showing some growth this year compared to last, according to a September report by accounting firm BDO. Last year, Goldcorp finalized its deal to acquire Vancouver-based junior Kaminak Gold, and in May of this year, El Dorado announced it was taking over Integra Gold for C$590 million. I expect to see even more deals in the coming months.

In the meantime, I agree with my friend Pierre’s “absolute rule” that investors should hold between 5 and 10 percent gold in your portfolio. I would also add gold stocks to the mix, especially overlooked and undervalued names, and rebalance once and twice a year.

U.S. Global Investors Recognized for Best Retail Communication

On a final note, I’m very pleased to share with you that U.S. Global Investors was recognized this week at the Mutual Fund Education Alliance’s (MFEA) STAR Awards in Chicago. Our firm walked away with three awards, one for best newsletter for advisors, one for our Gold’s Love Trade whitepaper and one for best overall retail communications.

This is truly a great honor, and I would like to thank the MFEA and its judges for recognizing the long hours, hard work and innovation that our crack investments and marketing teams put into making our market commentary among the very best on the internet.

You can see the full list of winners by clicking here. Congratulations to all!

Gold Market

This week spot gold closed at $1,272.99, down $7.51 per ounce, or 0.59 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.13 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index came in off just 0.27 percent. The U.S. Trade-Weighted Dollar reversed course this week and surged 1.22 percent.

| Date |

Event |

Survey |

Actual |

Prior |

| Oct-25 |

Durable Goods Orders |

1.0% |

2.2% |

2.0% |

| Oct-25 |

New Home Sales |

554k |

667k |

561k |

| Oct-26 |

Hong Kong Exports YoY |

5.9% |

9.4% |

7.4% |

| Oct-26 |

ECB Main Refinancing Rates |

0.000% |

0.000% |

0.000% |

| Oct-26 |

Initial jobless Claims |

235k |

233k |

223k |

| Oct-27 |

GDP Annualized QoQ |

2.6% |

3.0% |

3.1% |

| Oct-30 |

Germany CPI YoY |

1.7% |

-- |

1.8% |

| Oct-31 |

Eurozone CPI Core YoY |

1.1% |

-- |

1.1% |

| Oct-31 |

Conf. Board Consumer Confidence |

121.0 |

-- |

119.0 |

| Oct-31 |

Caixin China PMI Mfg |

51.0 |

-- |

51.0 |

| Nov-1 |

ADP Employment Change |

190k |

-- |

135k |

| Nov-1 |

ISM Manufacturing |

59.3 |

-- |

60.8 |

| Nov-1 |

FOMC Rate Decision (Upper Bound) |

1.25% |

-- |

1.25% |

| Nov-2 |

Initial Jobless Claims |

235k |

-- |

233k |

| Nov-3 |

Change in Nonfarm Payrolls |

310k |

-- |

-33k |

| Nov-3 |

Durable Goods Orders |

-- |

-- |

2.2% |

Strengths

- The best performing precious metal for the week was palladium, down slightly by 0.42 percent. Germany’s BASF noted that the automotive industry appears to be responding to the price surge in palladium this year and are slowing down purchases. According to Bloomberg, gold traders and analysts are bearish for the first time in four weeks as the dollar strengthens. The passing of the U.S. budget by the Senate lifted hopes by boosting risk sentiment and pushing yields higher. Joni Teves of UBS says a large fiscal package is a key downside risk for gold as it would result in a higher policy rate path.

- Even though there has been a pullback in gold prices, large buy orders came into the market two times this week and spiked prices higher. On Monday, 18,1792 gold contracts were traded in a span of five minutes and on Wednesday another 21,129 contracts were traded. Tai Wong, head of base and precious metals trading at BMO Capital Markets, bets the dollar is going to retrace and it will be good for gold.

- Paul Wright, former CEO of Eldorado Gold Corp., will resign from his board position after 20 years at the company and just months after resigning as CEO. Although stock value tripled during his tenure, Wright’s late career was marked by a high-profile dispute with the Greek government after investing over $2 billion in the country. Following the results of the European Central Bank meeting, gold is seeing some selling pressure and trade surging after the dollar index rallied.

Weaknesses

- The worst performing precious metal for the week was silver, down 1.05 percent. Gold declined for the sixth week out of seven to trade near the lowest close in more than two months, writes Ranjeetha Pakiam. In addition, China’s purchases of gold from Hong Kong dropped to an eight-month low in September as wholesalers have ample stocks and imports will likely remain weak.

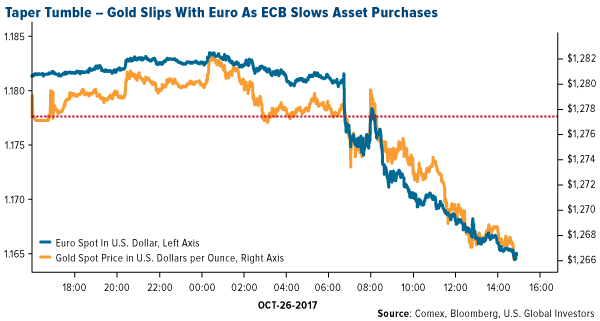

- European Central Bank President Mario Draghi outlined plans to cut monthly bond purchases in half beginning in January and indicated that zero percent interest rates could remain at current levels. The euro slid down in value taking gold with it as the dollar seems to be the only currency in the near-term to potentially see an interest rate hike.

click to enlarge

- Eldorado Gold plunged more than 28 percent after cutting its annual production forecasts for its flagship mine in Kisladag Turkey for the second time this year after struggling with low gold recoveries. Production guidance is down to 170,000-180,000 ounces from 230,000-245,000 ounces, citing lower-than-expected recovery, writes Aoyon Ashraf. Turkey contributed about 91 percent of Eldorado’s 2016 revenue.

Opportunities

- The U.S. posted its largest budget deficit since 2013 in the fiscal year that just ended and the Senate also approved a budget resolution that would fast-track up to $1.5 trillion in tax cuts. These measures would worsen the deficit situation, writes Saleha Mohsin. Despite this threat of higher interest rates, rising budget deficits have historically been associated with higher gold prices.

- Ray Dalio, founder of Bridgewater Associates, shared that the top 0.1 percent of households now holds about the same amount of wealth as the bottom 90 percent – similar to the wealth gap from 1935 to 1940 in the “era of populists” much like we are seeing today. Dalio continued to say that the Federal Reserve should more closely monitor the economic struggles of the bottom 60 percent of the economy and look beyond average statistics.

- Gold may climb back above $1,300 per ounce this year prompting investors to buy or increase their holdings as insurance, according to Gold Fields Mineral Services. Construction of Fruta del Norte, Ecuador’s first large gold mine, owned by Lundin Gold Inc. is underway while other companies continue to rush to the country after the government lifted a moratorium on exploration concessions last year. Additionally in South America, Mirasol Resources announced that one of its Argentine subsidiaries signed an exploration agreement for a gold-silver project.

Threats

- Chinese millennials are demonstrating a different taste toward gold from their elders as they pull away from traditional 24K gold in favor of exclusivity and individuality in their jewelry, writes Ruonan Zheng of the Jing Daily. Gold jewelry sales fell 3.6 percent in the first half of 2017 compared to the same period in 2016. Millennials are buying low caret value gold where more uniquely designed jewelry can be fabricated for younger taste versus a simple pure gold chain.

- With few deals completed and negative investor relations, the total value of mining deals involving North American companies is $3.7 billion, down 40 percent from the same time in 2016. Nate Trela writes that possible explanations are displeasure with results of transactions in recent years and traders taking advantage of arbitrage opportunities.

- Barrick Gold settled a dispute between its Acacia Mining unit and the Tanzanian government by agreeing to hand 50 percent of the economic benefits over to the country. This grew criticism from mining investors saying Barrick may have set a baseline for what nations may demand from mining companies.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 1.3 percent. OTB Bank, which is the largest holding of the Budapest stock exchange, accounting for about one third of the index, gained 2 percent in the past five days. The bank will release its latest quarter results on November 10, and analysts expect solid performance to continue.

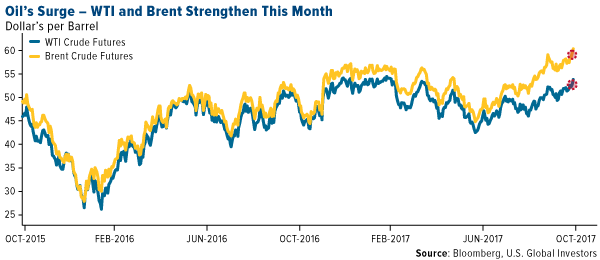

- The Russian ruble was the best relative performing currency this week, losing 90 basis points against the U.S. dollar. The ruble is highly correlated with the price of crude oil, but this week the currency and crude oil moved in opposite directions. Brent crude oil climbed to $60 per barrel for the first time since July 2015. Saudi Arabia and Russia backed the extension of OPEC oil cuts beyond March 2018.

- The health care sector was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 1.3 percent. The Greek banking index declined by 6.5 percent. The central bank chief Mr. Stournaras urged the banking sector to act faster to tackle its bad debt problem. Three of Greece’s largest lenders plan to sell up to 5.5 billion euros ($6.5 billion) in bad loans by early next year. Greek banks hold 103 billion euros in bad loans, equal to almost 60 percent of the economy.

- The Turkish lira was the worst performing currency this week, losing 3.5 percent against the U.S. dollar. Germany announced funding cuts to Turkey over an escalating political dispute between the two counties. Turkey relies on access to foreign funding to finance its current account deficit, and German banks are the second-largest providers of lending to the Turkish private sector as of August. Despite increasing political tension, the central bank of Turkey once again refused to support its currency, leaving the country’s main rates unchanged on Thursday.

- The real estate sector was the worst performing sector among eastern European markets this week.

Opportunities

- The European Central Bank (ECB) delivered what the market expected in terms of the size and duration of asset purchases. The ECB’s key rates were kept at the same level and will remain at the present level for an extended period of time. In January, the monthly bond purchases will be reduced from 60 billion euros to 30 billion for an initial nine-month period. The size and duration of the bond buying program could be extended, if needed. A dovish ECB tone pushed the euro lower against the U.S. dollar, but its decision should be growth supportive.

- Strong economic data continues to be released. French, German and eurozone manufacturing PMIs were reported above market expectations. Germany business confidence rose to a record high in October, supported by construction and manufacturing activities. Germany’s Ifo measure of sentiment reached 116.7 from a upwardly revised 115.3 last month. The record-high reading came after two consecutive monthly falls.

- The Central Bank of Russia cut its main policy rate by 25 basis points to 8.25 percent, as expected. The next central bank meeting is scheduled for December, and most analysts predict that the key rate will be cut again either by 25 or 50 basis points.

Threats

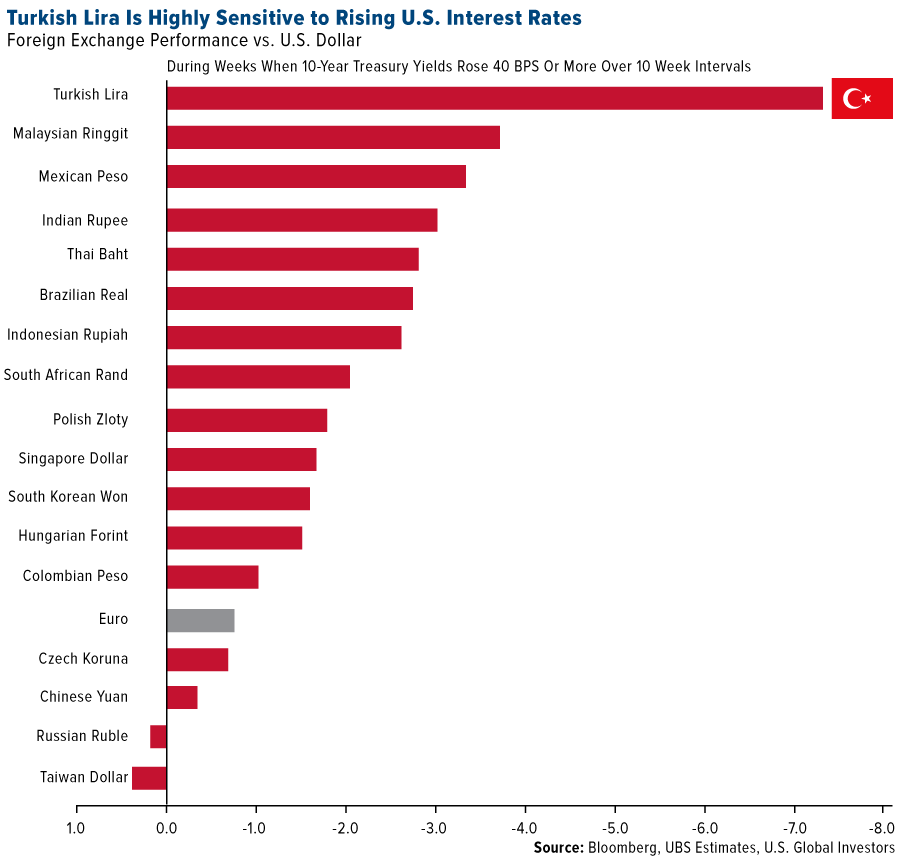

- UBS in its Global Macro Strategy publication from October 19 wrote that the Turkish lira (TRY), Malaysian ringgit (MYR) and Mexican peso (MXN) are the most sensitive currencies to periods of rising U.S. yields. The chart below shows currency performance versus the U.S. dollar during weeks when 10-year U.S. Treasury yields have risen 40 basis points or more over 12-week intervals. Rising rates in the U.S. could push the lira even lower against the U.S. dollar.

click to enlarge

- S&P analyst Frank Gill said that Poland is close to its economic peak. Poland’s economy is reaping the benefits from “almost full employment, capital expenditures increasing in the public sector, and the EU investment cycle picking up again.” However, despite the strong economic growth in the private sectors, there is no policy in place to increase public savings, Frank said. He believes that public debt will grow as fast as the economy in the coming years.

- We see rising political noise in Europe currently. Catalonia’s vote for independence has created political tension between Madrid and Barcelona. Germany, the Czech Republic and Austria are in the process of forming new governments. Sebastian Kurz, leader of Austria’s conservative People’s Party, opened talks with the far-right Freedom Party. In Turkey, a new party was launched, led by former interior minister Meral Aksener, who unsuccessfully opposed Erdogan’s drive for great presidential powers in a referendum last year. In Russia, Alexei Navalny, the biggest opponent of Putin, was barred from running in next year’s presidential election. Ksenia Sobchak, a 35-year-old television host, announced her willingness to run against Putin. The election in Russia will be held in March 2018.

© US Global Investors

www.usfunds.com

© U.S. Global Investors

Read more commentaries by U.S. Global Investors