Recently, Ryan Vlastelica penned a column suggesting investors should simply be “apathetic” when it comes to their money.

“Apathy doesn’t sound like a sensible investment philosophy, but it may be one of the most successful approaches a person can employ to grow wealth.”

Listen. I get it.

You can’t beat the market, so just “buy and hold.”

Over a long enough period, I agree, you will make money.

But, simply making money is not the point of investing.

We invest to ensure our current “hard earned savings” adjust over time to provide the same purchasing power parity in the future. If we “lose” capital along the way, we extend the time horizon required to reach our goals.

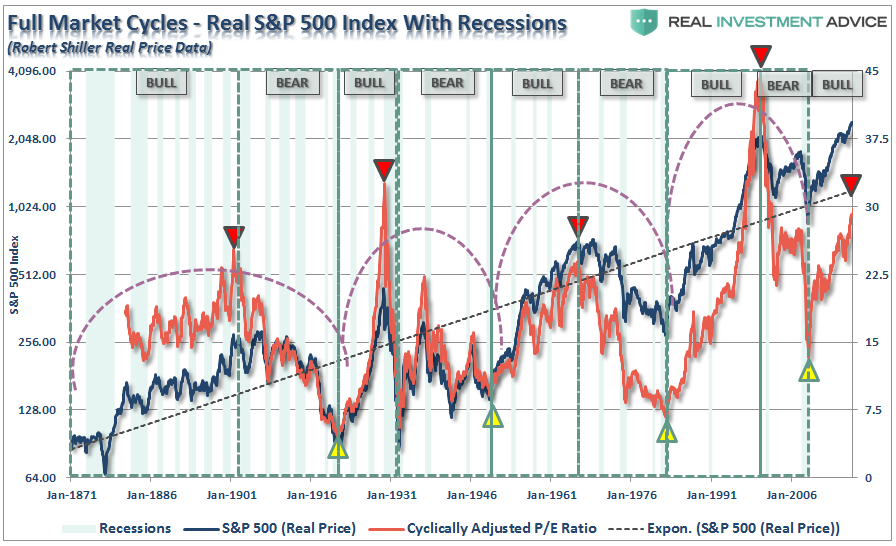

Crashes Matter A Lot

Ryan makes his case for “apathy” by quoting Barry Ritholtz who stated:

“If you don’t want to invest in equities because you fear a market crash, then you should never be in equities, because equities always crash.”

While Barry is absolutely correct in his statement, investing is never an “all or none” proposition. Being an investor is about understanding the “risk to reward” relationship of placing capital into the financial markets.

There is no “great investor” in history, not even Warren Buffett, who is apathetic about investing. It is also why every great investor has one simple rule in common:

“Buy low, Sell high.”

Why? Because it is the ONLY manner in which you truly create wealth. As Ryan notes:

“Ritholtz stressed that investors should diversify, in part to mitigate their concerns about portfolio volatility, but added that the best buying opportunities were when things looked the worst.”

The problem with being “apathetic” should be obvious. If you never sold high, then where will the capital come from to “buy low?”

Think about your personal situation.

- If you have a big cash pile at the moment, then you aren’t investing and are “missing out,” according to Ryan.

- If you don’t have a big cash pile, then where would you come up with the cash to buy “when things looked their worst?”

Yes, that’s the problem with “buy and hold” and “dollar cost averaging” which will become much more apparent momentarily.

Crashes matter, and they matter a lot.

Let’s set up a quick example to prove the point.

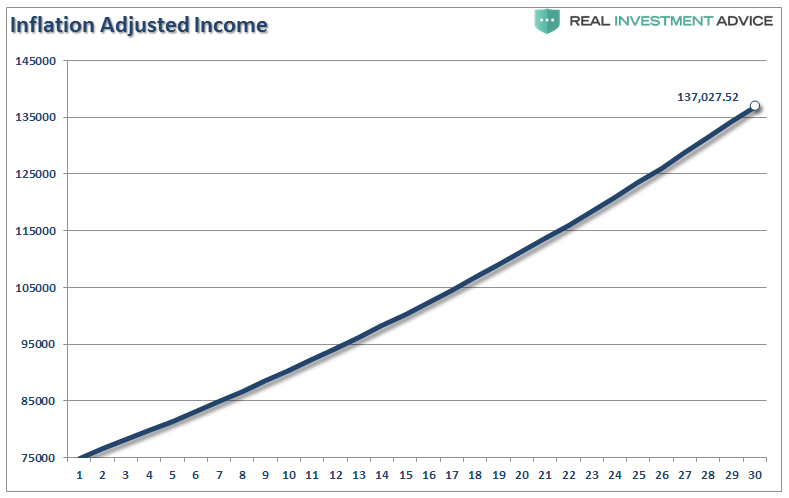

Bob is 35-years old, earns $75,000 a year, saves 10% of his gross salary each year and wants to have the same income in retirement that he currently has today. In our forecast, we will assume the market returns 7% each year and we will use 2.1% for inflation (long-term median) for planning purposes.

In 30 years, Bob’s equivalent income requirement will roughly be $137,000 annually.

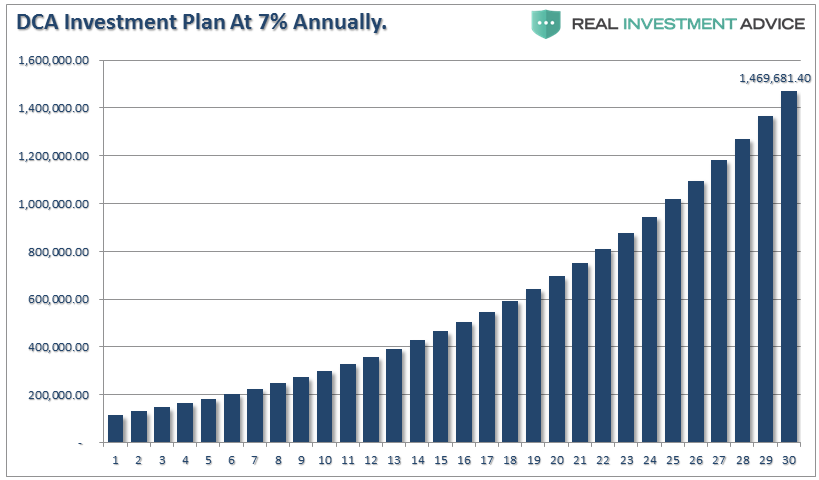

So, starting with a $100,000 investment, he gets committed to saving $7500 each year into his index fund and sits back to watch it grow into a whopping $1.46 million nest egg at retirement.

See, absolutely nothing to worry about. Right?

Not so fast.

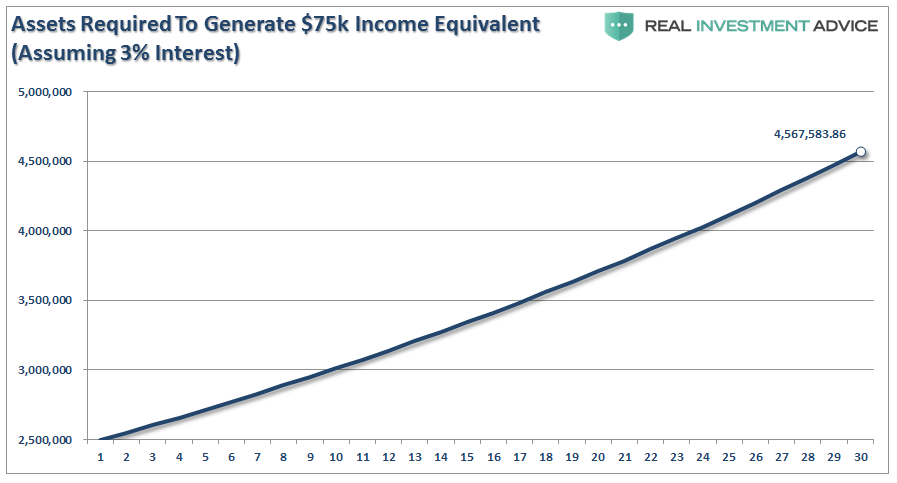

This is where problem number one arises for the vast majority of Americans. Given the economic drag of the 3-D’s (Debt, Demographics & Deflation) currently in progress, which will span the next 30-years, long-term interest rates will remain low. Therefore, if we assume that a portfolio can deliver an income of 3% annually, the assets required by Bob to fulfill his retirement needs will be roughly $4.6 Million.

(Yes, I have excluded social security, pensions, etc. – this is for illustrative purposes only.)

The roughly $3-million shortfall will force Bob to reconsider his income requirements for retirement.

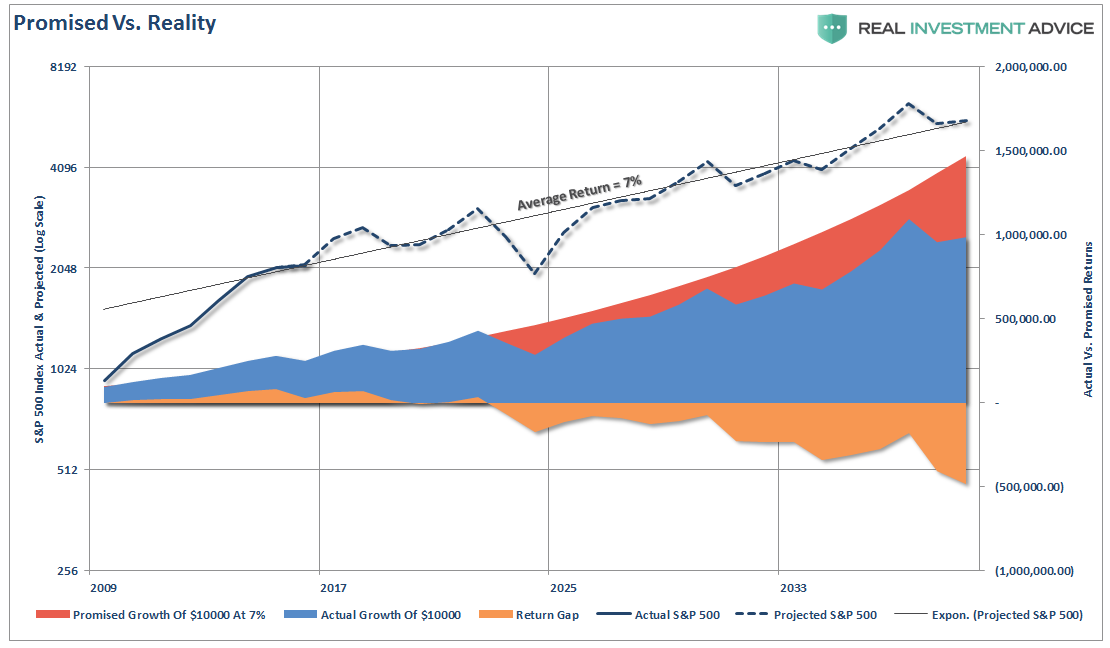

The second problem is that “crashes” matter and they matter a lot. The chart below is a $100,000 investment plus $7500 per year compounding at 7% annually versus actual market returns. I have taken historical returns from 2009 to present (giving Bob the benefit of front-loaded returns at the start of his journey) and then projected forward using a normal standard deviation for market returns.

The important point is to denote the shortfall between what is “promised to happen” versus what “really happens” to your money when crashes occur. The “sequence of returns” is critical to the long-term success of your investment outcomes.

Bob’s $1.5 million projected retirement goal comes up short by $500k. This only compounds the shortfall between what is actually required to create an inflation adjusted income stream at retirement.

This is specifically why there are more “baby boomers” in the workforce today than ever before in history.

“So, stop blaming “baby boomers” for not retiring – they simply can’t afford to.”

Yes, Valuations Matter Also

As I noted last week in “The Rule Of 20”

“Importantly, it is not just the length of the market and economic expansion that is important to consider. As I explained just recently, the ‘full market cycle’ will complete itself in due time to the detriment of those who fail to heed history, valuations, and psychology.

There are two halves of every market cycle. “

While valuations should NEVER be used as a means to manage a portfolio in the “short-term,” valuations haveeverything to do with how you invest long-term.

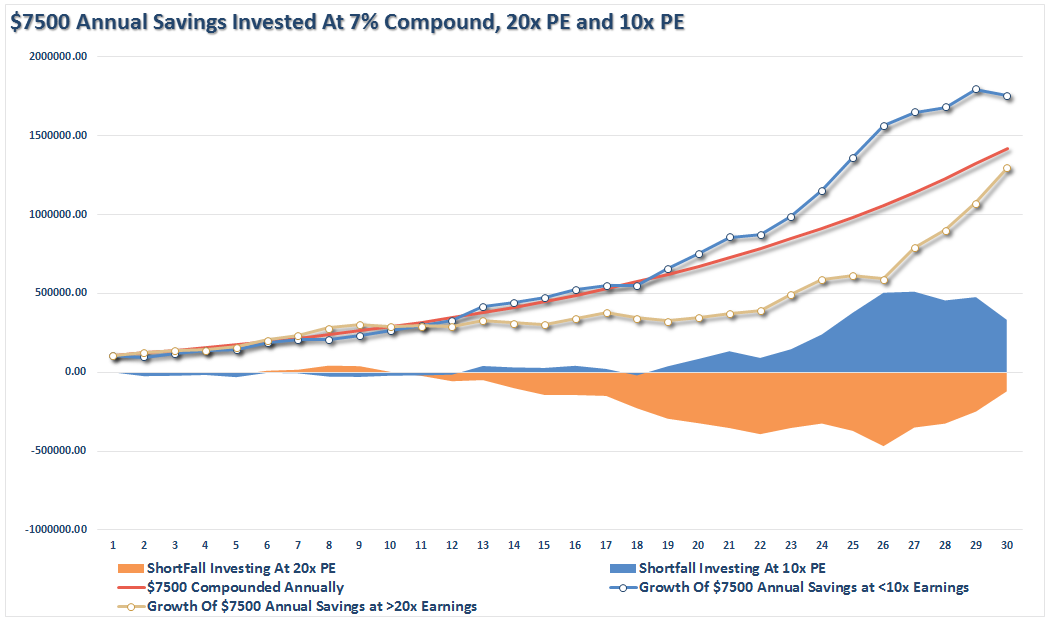

As I have shown many times previously (most recently here), the level of valuations at the start of the investing period are determinant of future returns. The chart below makes this extremely simple to understand. The chart shows the composite of total real compound returns over the subsequent 30-year period when valuations were either less than 10x earnings, or greater than 20x. I have then used those composites for Bob’s potential outcomes given valuations are currently greater than 20x on a trailing reported basis.

(Starting investment of $100,000 with $7500 annual savings)

Again, the outcome for Bob’s financial future comes up meaningfully short.

A Fix For Bob’s Financial Insecurity

Ryan quoted Barry again:

“It isn’t the market crashes that get investors, it’s the high blood pressure. They trade excessively and their investment philosophies are all over the place. They do things they shouldn’t, then stick with it when they shouldn’t. They flip from one style to the other. They’re overconfident. They make emotional decisions.”

Ryan, Barry and I can all agree on that point.

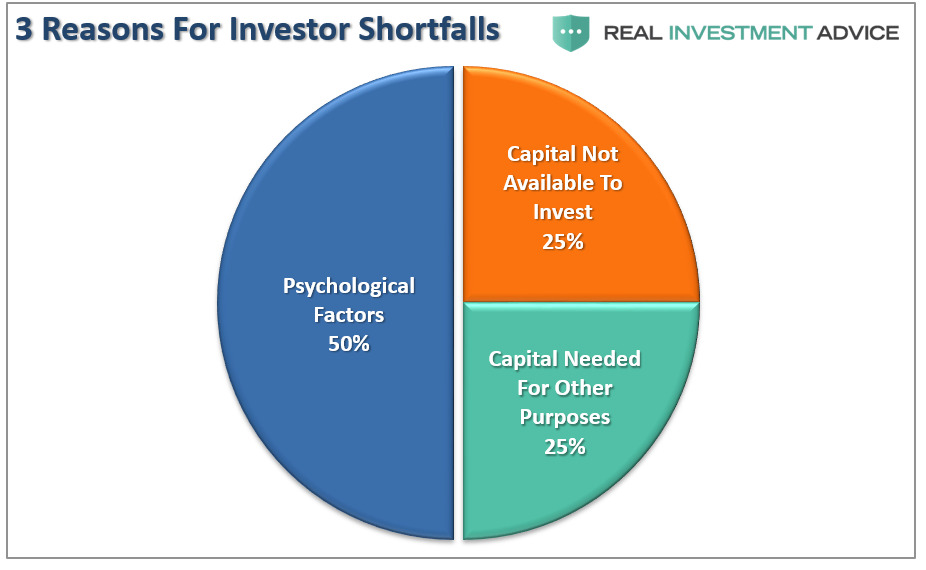

Psychology makes up fully 50% of the reason investors underperform over time. But notice, the other 50% relates to lack of capital to invest. (See this) Again, where is that capital going to come from to “buy low?”

These biases come in all shapes, forms, and varieties from herding, to loss aversion, to recency bias. They are all the biggest contributors to investing mistakes over time.

These biases are specifically why the greatest investors in history have all had a very specific set of rules they followed to invest capital and, most importantly, manage the risk of loss. (Here’s a list)

Here’s what you won’t find on that list. “Be apathetic.”

So, what’s Bob to do?

There is NO argument Bob needs to save and invest in order to reach his retirement goal and sustain his income in retirement.

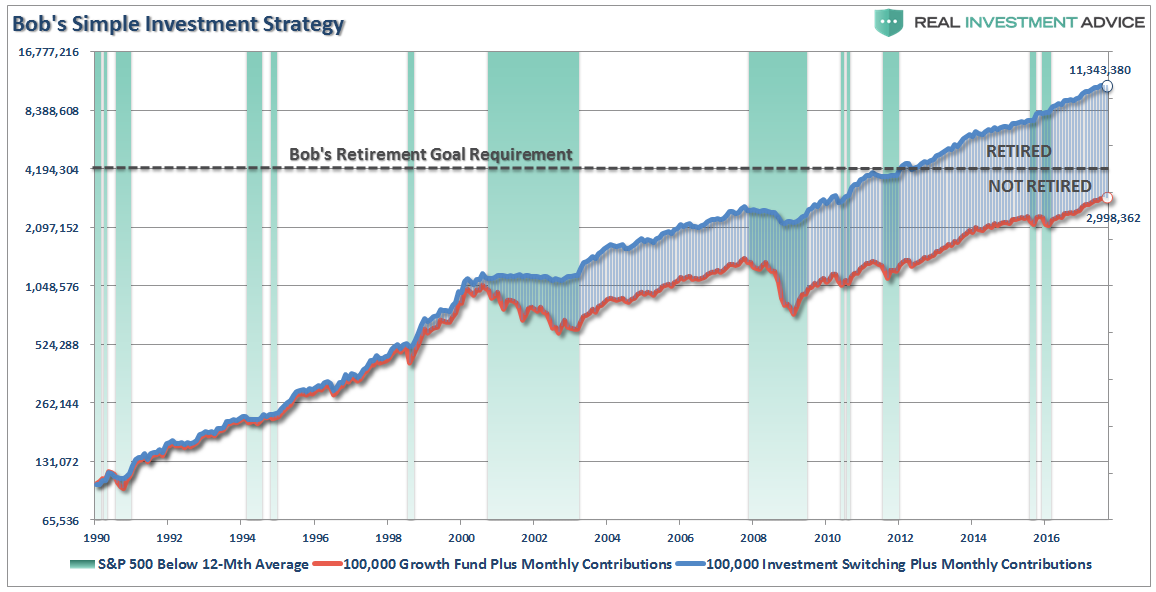

A simple solution can be designed using a well-known growth stock mutual fund and intermediate bond fund. The management method is simple. When the S&P index is above the 12-month moving average, you are 100% invested in the growth mutual fund. When the S&P index is below the 12-month moving average you are 100% invested in the bond mutual fund. I have compared the outcome to just “buy and holding” and “dollar cost averaging” into JUST the growth stock mutual fund.

For Bob, the difference is between meeting his retirement goals or not.

Over the next 10-years, given where current valuation levels reside, forward returns are going to be substantially lower than they have been over the last 10-years. This doesn’t mean there won’t be some “rippin'” bull markets during that time, there will also be some corrections along the way.

Just remember:

“Getting Back To Even Does Not Equal Making Money.”

Planning To Win

With valuations elevated, the economic cycle very long in the tooth, and the 3-D’s applying downward pressure to future economic growth rates, investors, along with Bob, need to consider the following carefully.

- Expectations for future returns and withdrawal rates should be downwardly adjusted.

- The potential for front-loaded returns going forward is unlikely.

- The impact of taxation must be considered in the planned withdrawal rate.

- Future inflation expectations must be carefully considered.

- Drawdowns from portfolios during declining market environments accelerate the principal bleed. Plans should be made during rising market years to harbor capital for reduced portfolio withdrawals during adverse market conditions.

- The yield chase over the last 8-years, and low interest rate environment, has created an extremely risky environment for retirement income planning. Caution is advised.

- Expectations for compounded annual rates of returns should be dismissed in lieu of plans for variable rates of future returns.

Chasing an arbitrary index that is 100% invested in the equity market requires you to take on far more risk that you most likely want. Two massive bear markets over the last decade have left many individuals further away from retirement than they ever imagined. Furthermore, all investors lost something far more valuable than money – the TIME that was needed to reach their retirement goals.

Investing for retirement, no matter what age you are, should be done conservatively and cautiously with the goal of outpacing inflation over time. This doesn’t mean that you should never invest in the stock market, it just means that your portfolio should be constructed to deliver a rate of return sufficient to meet your long-term goals with as little risk as possible.

Don’t be apathetic about your money.

There should be no one more concerned about YOUR money than you, and if you aren’t taking an active interest in your money – why should anyone else?

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter and Linked-In

© Real Investment Advice

© Real Investment Advice

Read more commentaries by Real Investment Advice