5 Agents of Change Investors Need to Know About Now

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

The world is changing fast right now in ways that many investors might not easily recognize or want to admit. This could end up being a costly mistake. If you’re not paying attention, you could be letting opportunities pass you by without even realizing it.

With that in mind, I’ve put together a list of five agents of change that I think investors need to be aware of and possibly factor into their decision-making process.

1. Xi Jinping

|

|

At China’s 19th National Party Congress last week, Xi Jinping’s political thought was enshrined into the country’s constitution, an honor that, before now, had been reserved only for Mao Zedong, founder of the People’s Republic of China, and Deng Xiaoping. It was Deng, if you recall, who in 1980 established special economic zones (SEZs) that helped turn China into the economic powerhouse it is today.

But back to Xi. His elevation to Chairman Mao-status last week not only cements his place in the annals of Chinese history but also makes him peerless among other world leaders in terms of political and militaristic might, with the obvious exception of U.S. President Donald J. Trump.

But whereas Trump has been criticized by some for setting the U.S. on a more isolationist path—shrinking the size of the State Department, just to name one example—Xi sees China emerging as the de facto global leader by 2050. To get there, his country is spending billions on the “Belt and Road Initiative” and other massive infrastructure projects, opening its doors to foreign investors, reforming state-run enterprises, weeding out corruption, investing heavily in clean energy and public transportation and expanding its middle class. And let’s not forget that the Chinese yuan, also known as the renminbi, was included in the International Monetary Fund’s (IMF) basket of reserve currencies in 2015, placing it in the same league as the U.S. dollar, British pound, Japanese yen and euro.

During his three-hour speech before the congress, Xi made reference to the “Chinese dream,” adding that the “Chinese people will enjoy greater happiness and well-being, and the Chinese nation will stand taller and firmer in the world.”

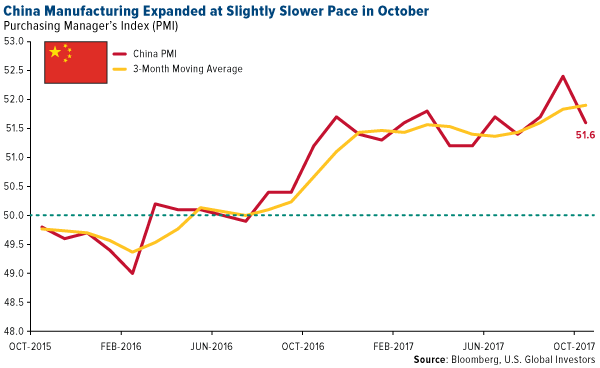

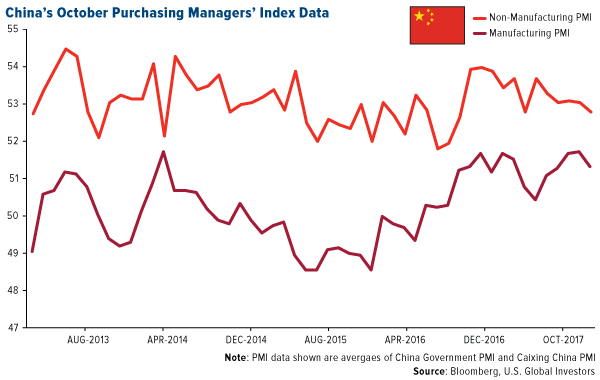

Xi has his own detractors, of course, who see China’s rise as a threat to established world order. But if his vision is to be realized, it might be prudent to recognize and prepare for it now. China’s economy grew a healthy 6.8 percent in the third quarter year-over-year, helping it get closer to meeting economists’ target of 6.5 percent for 2017. And although manufacturing expansion slowed in October, falling from 52.4 in September to 51.6, it was still well above the 50 threshold.

Citing these indicators as well as strong medium and long-term bank lending to nonfinancial corporations, research firm BCA recommended that investors overweight Chinese stocks relative to the emerging market aggregate.

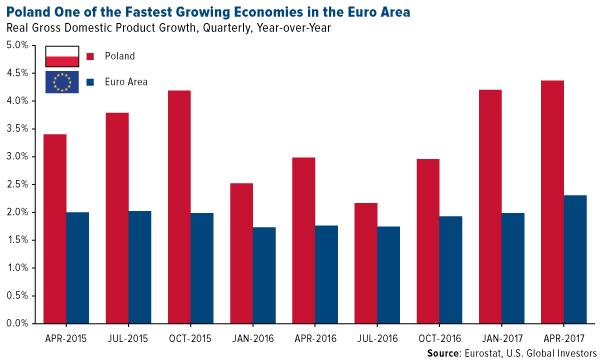

2. Poland

Besides China, another region I’m keeping my eye on is Poland. Already one of the fastest growing economies in Europe, the country was just upgraded from the “advanced emerging” category to “developed” by FTSE Russell, effective September 2018. This will place Poland in the same company as, among others, the U.S., U.K., Japan, Germany, Singapore and South Korea, the last country to have joined the club of top-ranking economies. Poland is the first Central and Eastern European (CEE) country to receive “developed” status.

Among the decisive factors behind the upgrade were the country’s advanced infrastructure, secure trading and a high gross national income (GNI) per capita. The World Bank expects Poland’s economic growth in 2017 to reach 4 percent, up significantly from 2.7 percent in 2016, on the back of a strong labor market, improved consumption and the child benefit program Family 500+.

Economists aren’t the only ones noticing the improvement. Young Polish expats who had formerly sought work in the U.K. and elsewhere are now returning home in large numbers to participate in the booming economy, according to the Financial Times. Banks and other companies, including JPMorgan Chase and Goldman Sachs, are similarly considering opening branches in Poland and hiring local talent.

This represents quite an about-face for a country that, as recently as 1990, was languishing under communist rule.

One of U.S. Global’s analysts, Joanna Sawicka, has seen the dramatic transformation firsthand. A native of Białystok, Poland, Joanna has vivid memories of waiting in line for hours just to buy food and school supplies. After returning to the U.S. from a visit to her hometown in 2015, though, she was singing its praises:

“I saw big changes. There’s now a small business on every street corner. A lot of my old friends own businesses now. Poland is the largest beneficiary of European Union funds, and people are clearly taking advantage of having more money and better opportunities.”

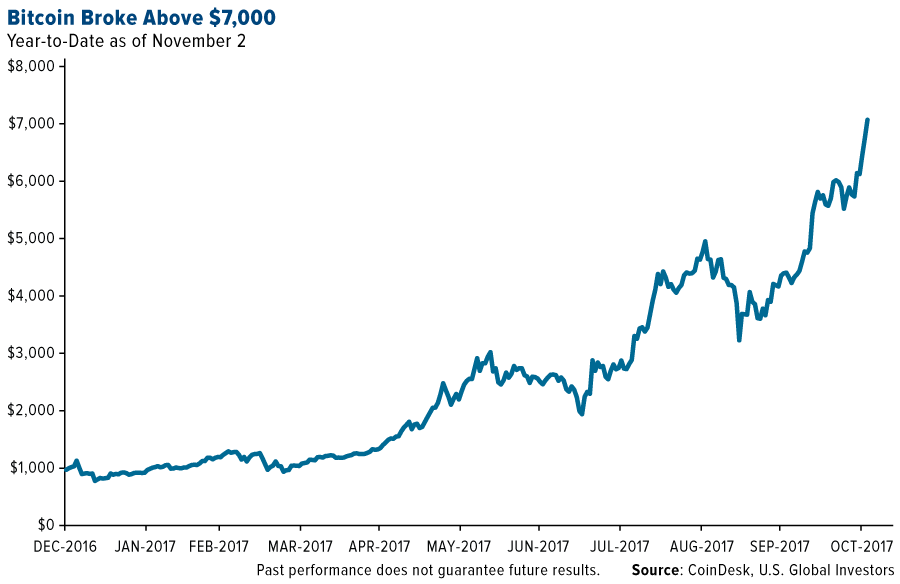

3. Bitcoin

One of the most influential agents of change right now is bitcoin, and indeed the entire digital currency market. Cryptocurrencies are challenging underlying notions of the global monetary framework, upending the way many companies raise funds and disrupting the investment world.

All this from an asset class nobody even knew about 10 years ago.

For the first time this week, bitcoin traded above $7,000 a coin, bringing its 2017 gains to around 650 percent. Some are calling this a bubble, but I recently shared with you a chart that shows that, when placed on a logarithmic scale, bitcoin doesn’t appear to have found its peak yet.

Bitcoin can no longer be called a curiosity or niche investment. Large brokerage firms and financial institutions, including Fidelity and USAA, now allow clients to use their websites to check their holdings of bitcoin and other digital currencies alongside their more traditional assets. And just this week, the Chicago Mercantile Exchange (CME) announced it will be offering a bitcoin futures contract by the end of the year, giving investors an easier way to trade cryptos.

Following the announcement, Coinbase, a leading digital currency broker, saw a record number of people opening new accounts on its platform. Within a single 24-hour period, as many as 100,000 new users opened accounts, helping to double the number of Coinbase clients since the beginning of the year.

This explosion in interest hasn’t come without consequences in other markets, however. The U.S. Mint reported that this year’s sales of American Eagles, the popular gold coins, have fallen to their lowest level since 2007, presumably as investors who otherwise would have bought bullion have instead put money in bitcoin as a store of value.

4. U.S. Tax Reform

It’s been a generation at least since the U.S. has had meaningful tax reform. That might be about to change, though, as Congress and the president this week unveiled their plans to overhaul the tax code and deliver the “biggest tax cut in U.S. history,” according to Trump.

If passed and signed, the plan would consolidate the number of income brackets, currently at seven, down to only four, while also eliminating a number of tax credits and exemptions, including the alternative minimum tax (AMT). The fourth bracket, with a rate of 39.6 percent for the nation’s top earners, was added at the last minute to address concerns the new code would blow up the deficit. Many savers are no doubt relieved to learn that 401(k)s will be left alone, ending rumors that annual contribution caps would be lowered.

As for corporate taxes, the plan is to slash them from 35 percent—the highest among any country in the Organization for Economic Cooperation and Development (OECD)—to a much more competitive 20 percent. This change would be both immediate and permanent.

Right now, as much as $2.5 trillion or more in cash is estimated to be held overseas by multinational corporations to avoid having to pay the steep rate. Lowering it would allow these firms to bring profits home and reinvest them in workers, new equipment and more. It would also encourage American companies to relocate operations back to the U.S., as we saw this week with semiconductor manufacturer Broadcom.

After failing to repeal and replace Obamacare, both Congress and the president need this win if they expect voters to give them another term.

5. Jerome Powell

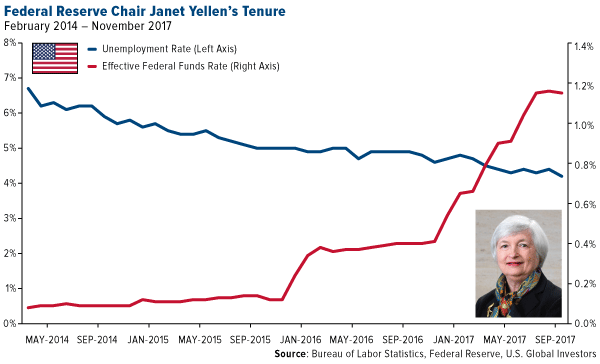

For the final agent of change, I’m picking someone whom some readers might not agree reflects real change. Jerome “Jay” Powell, the person Trump has tapped to replace Federal Reserve Chair Janet Yellen—assuming he gets Senate confirmation—is being described as someone who’ll mostly hold to the status quo established by his two immediate predecessors, Yellen and Ben Bernanke. Powell appears to be dovish and supportive of the cautious interest rate hikes we’ve seen during Yellen’s tenure, which will come to an end in February 2018.

There’s one huge difference, however—one that likely convinced Trump a change was needed, despite his previous acclaim for Yellen’s handling of the job. Whereas Yellen has expressed support for the raft of financial regulations that were introduced in the wake of the financial crisis, Powell generally seems to be in favor of deregulation, in line with Trump’s own agenda. On numerous occasions I’ve written that our industry needs more streamlined rules and laws, so I see this as very constructive. Although Powell, as head of the Fed, won’t have any policymaking authority to alter or reverse such rules, at least he’ll serve as an ideological ally of Trump’s.

On top of all this, Powell’s appointment will set new precedent. He’ll be the first Fed chair in decades not to hold an advanced degree in economics—he’s a former investment banker with the Carlyle Group—and he’ll also be the first in nearly as many years to replace someone before the end of their full 14 years.

In any case, I speak for everyone at U.S. Global by wishing Powell the best, once confirmed, and hope his policies can help the U.S. economy continue moving in the right direction.

Like what you read? Sign up for my award-winning CEO blog Frank Talk and never miss a post!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.45 percent. The S&P 500 Stock Index rose 0.26 percent, while the Nasdaq Composite climbed 0.94 percent. The Russell 2000 small capitalization index lost 0.89 percent this week.

- The Hang Seng Composite gained 0.64 percent this week; while Taiwan was up 0.86 percent and the KOSPI rose 2.46 percent.

- The 10-year Treasury bond yield fell 8 basis points to 2.33 percent.

Domestic Equity Market

Strengths

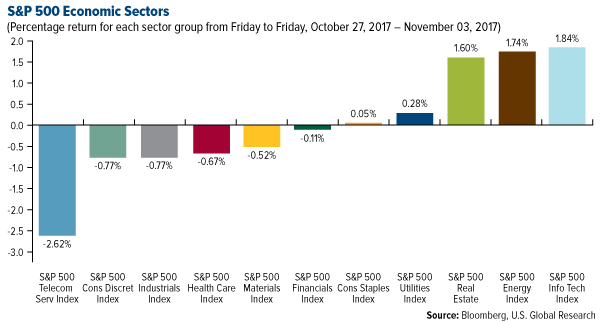

- Information technology was the best performing sector of the week, increasing by 1.84 percent versus an overall increase of 0.23 percent for the S&P 500.

- Qualcomm was the best performing stock for the week, increasing 13.27 percent.

- Apple had spectacular earnings and beat its own expectations. The company reported profit and revenue that exceeded Wall Street analyst targets and grew sales for all three of its major product lines — iPhone, iPad and iMac.

Weaknesses

- Telecommunications was the worst performing sector for the week, falling 2.62 percent versus an overall increase of 0.23 percent for the S&P 500.

- Envision Healthcare was the worst performing stock for the week, falling 37.70 percent.

- Under Armour’s stock fell roughly 23 percent after posting mixed third-quarter earnings and slashing guidance for the rest of the year. The company disclosed that it suddenly has a huge Gen Z problem. During its third-quarter conference call, the company listed its youth business, which has historically been a strength, as one of its weakest categories.

Opportunities

- The companies most likely to benefit from the tax plan rose on the plan’s proposed details. These companies can be broken into two main groups: those who pay the most taxes and would benefit most from a cut, and those with the most cash stashed overseas that would see a huge windfall from a proposed one-time repatriation tax holiday.

- Sprint and T-Mobile are reportedly working to save their merger after talks broke down. The wireless carriers could announce a deal within weeks.

- Nintendo almost doubled its profit forecast due to massive sales of the Switch. The company raised its full-year operating profit forecast too as supply shortages on its new games console finally began to abate.

Threats

- A lawsuit alleging price-fixing of generic drugs is about to be expanded to include nearly every state in the country, and Mylan is at the center of it. Forty-six state attorney generals are alleging price fixing of generic drugs by 18 companies. The states are focusing on Rajiv Malik, Mylan's president and executive director, along with Satish Mehta, CEO at Emcure Pharmaceuticals. Mylan's shares were down more than 8 percent on the news.

- Tesla posted a big loss and cut Model X and Model S production to catch up on Model 3. The company reported the largest quarterly loss in its history and said it would produce "about 10 percent fewer" units of those two models.

- Facebook crushed third-quarter earnings but warned that future profit will slow. The company fell in after-market trading after it cautioned that future profitability would be affected by increased investments around its efforts to fight fake news.

The Economy and Bond Market

Strengths

- Personal spending in the U.S. bounced back to 1 percent growth from the previous month’s 0.1 percent growth. This beat expectations of 0.9 percent.

- The ISM Non-Manufacturing Composite Index for October increased to 60.1 from the prior month’s reading of 59.8. It beat forecasts of a decline to 58.5.

- The Markit U.S. Manufacturing purchasing managers’ index (PMI) for October held strongly at 54.6, slightly higher than the previous month’s 54.5.

Weaknesses

- The U.S. economy added 261,000 jobs in October as hiring bounced back following the storm-weakened month of September. However, the jobs creation number was considerably below Wall Street expectations of 310,000.

- The Markit U.S. Composite PMI for October fell slightly to 55.2 from the previous month’s 55.7.

- Canada's GDP unexpectedly went negative, falling by 0.1 percent month-over-month in August following the prior month's flat reading of 0.0 percent. Economists were expecting GDP to tick up by 0.1 percent.

Opportunities

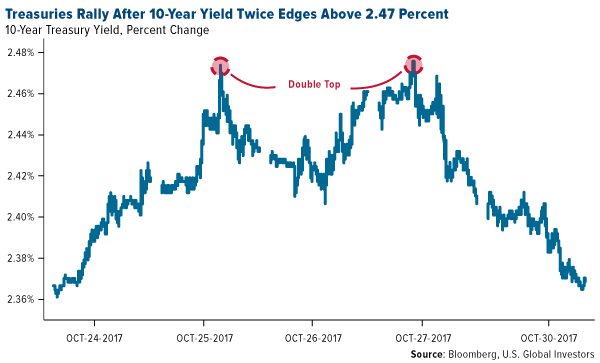

- The benchmark 10-year Treasury yields twice climbed above 2.47 percent last week, only to retreat. BMO Capital Markets strategists see it as a “double top” technical pattern, indicating a reversal. Indeed, yields have continued to fall to about 2.34 percent this week and that might be only the beginning. “We’re open to a retest of the 200-day moving average at 2.31 percent,” according to BMO’s strategists.

- President Trump chose Jerome Powell to replace Janet Yellen as Federal Reserve Chairman this week. Powell is seen as a relatively safe, Wall Street-friendly choice at a crucial time for the central bank. The Fed has begun the process of raising interest rates from post-recession lows and is unwinding its massive balance sheet.

- In the U.S., the fourth-quarter senior loan officer survey will be released on Monday. In the eurozone, final PMIs are also due on Monday.

Threats

- The third quarter of 2017 broke a 13-consecutive-quarter streak where Fitch municipal public finance upgrades outnumbered downgrades. This quarter saw 35 upgrades and 35 downgrades, compared to 94 upgrades and 34 downgrades in the second quarter. The downgrades were driven by the health care and public power sectors, Fitch said.

- The proposed tax plan has the real estate industry in a panic. The plan would cap the mortgage-interest deduction on new homes at $500,000. This could dampen the benefit of the deduction outside of the most expensive housing markets and may lower home values. "We're worried about a national housing recession," Jerry Howard, the CEO of the National Association of Home Builders, a lobbying group based in DC, told Business Insider.

- Puerto Rico’s federal oversight board has given the island about seven weeks to revise its financial recovery plan to account for damage suffered from Hurricane Maria, raising the possibility the territory will need to impose deeper losses on bondholders. The devastation has made revenue collections "almost impossible,” said Natalie Jaresko, the panel’s executive director.

This week, spot gold closed at $1,270.42, down $3.46 per ounce, or 0.27 percent. Gold stocks, measured by the NYSE Arca Gold Miners Index, ended lower by 0.12 percent. Junior-tiered stocks outperformed seniors, with the S&P/TSX Venture Index closing up 0.58 percent. The U.S. Trade-Weighted Dollar was essentially unchanged by the end of the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-30 | Germany CPI YoY | 1.7% | 1.6% | 1.8% |

| Oct-31 | Eurozone CPI Core YoY | 1.1% | 0.9% | 1.1% |

| Oct-31 | Conf. Board Consumer Confidence | 121.5 | 125.9 | 120.6 |

| Oct-31 | Caixin China PMI Mfg | 51.0 | 51.0 | 51.0 |

| Nov-1 | ADP Employent Change | 200k | 235k | 110k |

| Nov-1 | ISM Manufacturing | 59.5 | 58.7 | 60.8 |

| Nov-1 | FOMC Rate Decision (Upper Bound) | 1.25% | 1.25% | 1.25% |

| Nov-2 | Initial Jobless Claims | 235k | 229k | 234k |

| Nov-3 | Change in Nonfarm Payrolls | 313k | 261k | 18k |

| Nov-3 | Durable Goods Orders | 2.0% | 2.0% | 2.2% |

| Nov-2 | Initial Jobless Claims | 230k | -- | 229k |

Strengths

- The best performing precious metal for the week was palladium, up 2.92 percent as traders pointed to Ford’s surprise increase in auto sales. As gold bar sales surge in China, demand for gold rose to 815.89 tons in the first nine months from a year ago, according to Bloomberg. Perth Mint released figures saying gold coin and minted bar sales were 44,618 ounces in October, down from 46,415 ounces in September. However, silver sales spiked up 43 percent to 999,425 ounces from 697,849 last month.

- Hong Kong introduced a new program linking the city to Shenzhen for trading and facilitating the international role of the renminbi. Hong Kong provides the trading platform while Shenzhen will provide physical asset clearing, writes Ranjeetha Pakiam.

- Turkey added 3.6 million ounces of gold, worth almost five billion dollars, to their reserves this year. This ranks them among the top two or three buyers in 2017. The central bank said changes in official reserves are part of a diversification strategy.

Weaknesses

- The worst performing precious metal for the week was gold. Gold recorded its second monthly decline, off 0.71 percent, as the dollar strengthens and investors weigh the outlook for U.S. tax changes and interest rates, Bloomberg reports. In addition, gold traders and analysts surveyed by Bloomberg are divided on outlook as President Donald Trump named Jerome Powell to lead the Federal Reserve.

- Bitcoin is now more than five and a half times the price of gold, as it grew to over $7,000 this week. Harvard economist Ken Rogoff warns that cryptocurrencies are “fool’s gold,” since their futures depend on government regulation. Initial Coin Offerings (ICOs) of electronic coins are likely pulling some demand away from the physical bullion coin market.

- As Acacia Mining continues to resolve its $190 billion tax bill from the Tanzanian government, its chief executive officer and chief financial officer are stepping down from their positions at the end of the year. The Moody’s Investors Services downgraded Eldorado Gold Corporation’s outlook rating to negative from stable due to continued production challenges at its main operating mine in Turkey and execution risks in key projects in Greece.

Opportunities

- Gold stocks outperformed relative to bullion in 2016 and are now trading at late-2008 levels when the price of gold was around $730 per ounce. Christopher Wood, CLSA, writes that a long-term bullish view is maintained on gold bullion, with the ultimate price target remaining at $4,200 per ounce due to central banks being unable to exit from unconventional monetary policy in a benign manner.

- Copper could test record highs of $10,000 per ton as the supply and demand balance shifts to deficits in 2018, according to top copper producer Codelco. Copper prices climbed above $7,000 per ton earlier this month for the first time since 2014, reports Bloomberg.

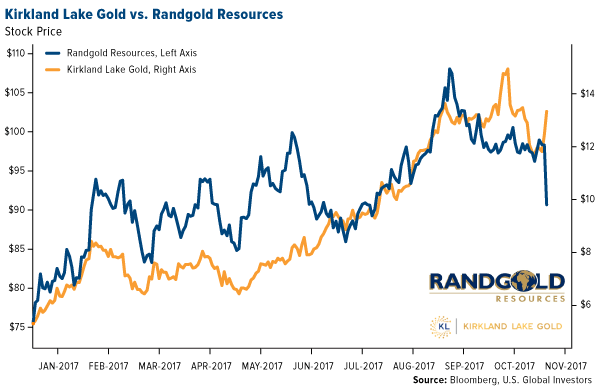

- Market leadership and contrasting earnings results drove a big spread between Kirkland Lake Gold and Randgold Resources on Thursday. Kirkland Lake missed earnings on higher-than-expected deferred taxes and exploration expense; however, it guided production higher for the second time this year, lifting the share price by 6.4 percent. Randgold had third-quarter production come in lower than the prior quarter but reiterated it would meet full year guidance. Its stock was sold down 7.8 percent. Wesdome Gold Mines Ltd. reported results from drilling in the Eagle River Mine in Ontario with assays containing over one ounce of gold per ton of rock. Wesdome’s share price closed almost 15 percent higher in response to the positive news.

- Renowned economist Harry Dent warns that gold has to fall significantly and get back to its bubble origin before it will boom again. He says the next commodity peak will happen around the year 2030 and gold will likely hit $5,000 per ounce.

- Investors have ignored tightening supplies of silver, which have lagged in price performance as other metals are seeing a pick-up in demand and price. As a result, an ounce of gold buys 76 ounces of silver, compared with the average of 63 ounces over the past decade, said Suki Cooper, an analyst at Standard Chartered Pic.

- One current and three former female lawmakers told the Associated Press that over the years they had been harassed or subjected to hostile sexual comments by fellow members of Congress. These allegations revealed that Congress has few training or reporting requirements in place to deal with sexual harassment. There is no Human Resources department or designated person to turn to when these incidences occur.

Energy and Natural Resources Market

Strengths

- Natural gas was the best performing major commodity this week rising 8.9 percent. The commodity rallied after weekly weather models showed stronger “cold chances” for the midwest, east and south. This should result in increased use of gas-powered heating.

- The best performing sector this week was the S&P 500 Oil Producers and Explorers Index. The index of oil and gas producers rose 5.1 percent, tracking the weekly advance of crude prices, which rose 3.3 percent.

- CVR Refining LP, an independent limited partnership with refining and logistics assets, was the best performing stock in the broader resource market this week. The stock rallied 15.8 percent to a 52-week high after the company announced expenses related to the purchase of Renewable Identification Numbers (RIN) that were significantly below market expectations.

Weaknesses

- Steel was the worst performing major commodity this week, dropping 0.6 percent. The commodity dropped as Chinese purchasing managers’ indexes (PMIs) disappointed for the month of October. This was likely a result of weaker demand, resulting from a week-long holiday early in the month and a government directive to cut metal output ahead of the Party Congress.

- The worst performing sector this week was the S&P 1500 Steel Index. The index dropped 3.0 percent after index heavyweight AK Steel Corporation announced disappointing third quarter earnings results. The announcement resulted in a 30 percent weekly drop in the stock price.

- The worst performing stock for the week was Centerra Gold Inc. The Canadian gold and copper producer dropped 8.3 percent after announcing disappointing earnings results and slashing its gold production guidance for the full year 2017.

Opportunities

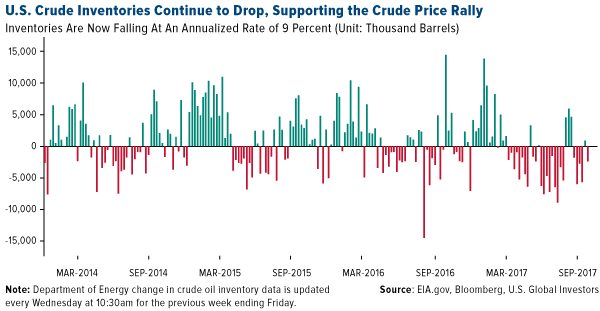

- U.S. crude oil inventories fell 2.4 million barrels last week, a much better than expected withdrawal. In addition, the 52-week moving average for U.S. crude inventory levels has dipped into withdrawal territory for the first time since early 2014. At the going rate, numbers suggest the U.S. could see as much as a 25-million-barrel inventory drop over the next 12 months. This would necessarily facilitate the global crude oil rebalancing, and may result in crude prices spiking well above their current price levels.

- In addition to inventory depletions, U.S. crude production continues to fall as August crude production was reported at 9.21 million barrels per day, compared to 9.23 in July. Simultaneously, the EIA has reported U.S. gasoline demand rose to a record 9.77 million barrels in August. The data suggests the U.S. is simultaneously seeing a drop in supply and a rise in demand which has resulted in better-than-expected inventory draws over the fall and a quicker-than-expected rebalancing of global crude markets.

- Nickel rallied this week, despite its global inventories still elevated. Global inventories are being driven by nickel briquettes that largely go into stainless steel. However, nickel for the electronic vehicle (EV) market know the necessary nickel plate cathode, as opposed to briquette’s, have inventories are approaching all time lows. As a result, stainless steel producers, which have been demanding cathode, will start to deplete the supply of nickel briquettes and kick-start demand.

Threats

- Chinese economic activity showed evidence of softness in October. The official manufacturing purchasing managers index, a gauge of China’s factory activity, fell to 51.6 in October from 52.4 in September - slightly below the median forecast of 51.8 by economists. Officials attributed the slowdown to the Golden Week holiday, which disrupted production and curbed orders. However, economists say rising borrowing costs and waning effects of government support for economic growth may have started to weigh on businesses.

- The Venezuela crude production collapse that may lead to a major supply disruption and a spike in global prices may never materialize. Venezuela is too important for China and Russia to let it fail. Venezuela is among the top 10 suppliers of crude to China, according to China customs information. In addition, those expecting a major default should know that the South American nation still has numerous oil assets it can pledge to China and Russia before it will allow a default.

- Money managers have cut their bullish gold bets to the least bullish in 12 weeks. Hedge fund managers and others have reduced their long positions by 6,508 contracts to 166,535, according to weekly data. The net-long position was reduced to coincide with the announcement of Jay Powell as next Fed Chairman, which suggests a more hawkish Federal Reserve rate hiking path and a stronger U.S. dollar.

Strengths

- South Korea’s KOSPI Index climbed 2.46 percent for the week. It climbed to new record highs with the help of technology, including heavyweight Samsung.

- Casinos and gaming stock Landing International Development Ltd. (582 HK) rose 33.70 percent for the week, making it the top performer in the Hang Seng Composite Index.

- A preliminary year-over-year third quarter gross domestic product (GDP) reading for Taiwan came in at 3.11 percent, well ahead of analysts’ expectations for a 2.20 percent showing.

Weaknesses

- The Shanghai Composite fell 1.32 percent for the week, taking a breather after the conclusion of the 19th Party Congress last week.

- Building sub-contractor Hong Kong International Construction Investment Management Group Co. fell 15.58 percent for the week, making it the weakest performer in the HSCI.

- The official measurement of China’s Manufacturing purchasing managers’ index (PMI) came in slightly below expectations, coming in at a 51.6 print, shy of an anticipated 52.0 and below last month’s 52.4. Notably, however, last month’s gains beat, and this month appears more in line with where the previous range had been. Non-manufacturing PMI came in at 54.3, down from last month’s 55.4, and the Caixin China Manufacturing and Services PMIs came in at 51.0 (inline) and 51.2 respectively.

Opportunities

- In a big week of headlines for cryptocurrencies, the CME Group announced the upcoming launch of a bitcoin futures contract later this year or early next year, even as the Monetary Authority of Singapore (MAS) announced late last week that it will not seek to regulate cryptocurrencies.

- According to Banny Lam, head of research at CEB International Investment Corp, Chinese bonds and stocks might be benefiting from President Trump’s visit to Beijing next week. Lam believes that Trump could unveil deals and initiatives that bolster the links between Chinese and American business, reports Bloomberg.

- On its NASDAQ debut Friday, China’s fifth biggest peer-to-peer (P2P) lender, Hexindai, surged more than 60 percent, reports the South China Morning Post. Since last year, China’s watchdogs have ramped up efforts to contain risk in the P2P sector, but this news seems to shrug off any looming concerns about tighter scrutiny.

Threats

- The backlash against Chinese products in India is ramping up, according to Bloomberg. An economic policy group linked to the ruling Bharatiya Janata Party drew more than 100,000 people onto the streets of New Delhi on October 29 to rally against the dominance of Chinese products. “This flood of Chinese imports fits in very uncomfortably with the priority of the Modi government to expand India’s manufacturing base,” said Harsh Pant, professor at King’s College in London.

- Toyota Motor Corporation, Japan’s biggest automaker by volume, is feeling pressure from its Japanese automobile rivals in China, reports Reuters. Due to lack of presence in a key segment, Toyota has fallen to the number three spot, behind Honda Motor Company and Nissan Motor Company. “Toyota’s relative weakness lies in the lack of smallish crossover sport-utility vehicles that others have leveraged to accelerate growth,” the article concludes.

- Two U.S. strategic bombers conducted drills over South Korea this week, reports Reuters, raising tensions with North Korea just a few days before President Trump is set to visit the region. According to North Korean state news agency KCNA, “[t]he reality clearly shows that the gangster-like U.S. imperialists are the very one who is aggravating the situation of the Korean peninsula and seeking to ignite a nuclear war.”

Strengths

- Greece was the best performing country this week, gaining 3.2 percent. The Greek banking index appreciated almost 8 percent. The country is working on its third review and analysts predict that Greece will exit the bailout program next year. The Greek government plans to create an ample cash buffer of EUR 12-15 billion before the completion of the program, giving Greece the opportunity for a “clean” exit, according to Wood & Company analyst Alex Boulougouris.

- The Polish zloty was the best relative performing currency this week, losing 5 basis points against the U.S. dollar. A strong economy is supporting the country’s currency. According to a Bloomberg Barclays local-currency government bond index, Poland’s local currency bonds have returned 19 percent so far this year. The zloty is the second-best performing currency this year against the U.S. dollar.

- The industrial sector was the best performing sector among eastern European markets this week.

Weaknesses

- The Czech Republic was the worst performing country this week, losing 1 percent. The central bank hiked its main rate by 25 basis points this week. This is the second rate hike this year and further increases are expected.

- The Turkish lira was the worst performing currency this week, losing 2.6 percent against the U.S. dollar. Increasing political tension between the U.S. and Turkey, along with rising inflation, are souring investors’ sentiment. Turkey’s inflation accelerated to 11.9 percent year-over-year in October, the highest since 2008 and ahead of the 11.5 percent estimate.

- The consumer staples sector was the worst performing sector among eastern European markets this week.

Opportunities

- The Wall Street Journal said that the European Central Bank’s caution on ending bond purchases looks like the right call after stronger GDP and weaker inflation data was released. The publication added that the ECB’s decision to extend bond purchases until at least September 2018 has brought time and flexibility. The quantitative easing (QE) program and low inflation will stimulate further growth and should be positive for European equities.

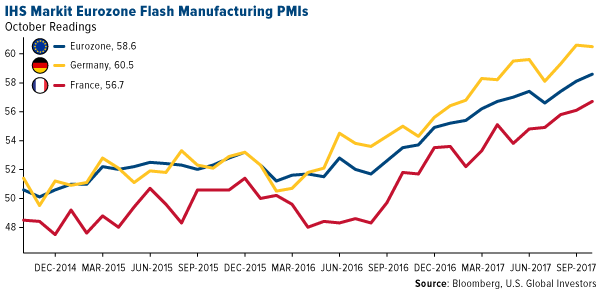

- Euro-area manufacturing is expanding at one of the fastest rates since the start of the millennium. The eurozone factory purchasing managers’ index (PMI) rose to 58.5 in October, the highest since February 2011 and the second highest in over 17 years. Strong Euro-area PMIs are supported by robust readings coming out of Germany and France, the two largest European economies. In central Emerging Europe, the Czech Republic had the strongest PMI reading in October of 58.5, and Russia had the weakest at 51.1. Both are above the 50 level that separates growth from contraction.

- Russia moved up to 35th place in the World Bank’s annual index which ranks countries based on the ease of doing business, pushing it ahead of some EU states including Italy and Belgium. In 2012 Russia ranked 120, the year when Vladimir Putin set a goal for Russia to reach a top 20 position by 2018.

Threats

- A former Trump campaign chief, his associate and an ex-foreign policy adviser were arrested on Monday and charged with crimes including money laundering, lying to the FBI and conspiracy, as a result of the ongoing federal investigation into whether President Trump’s campaign colluded with Russia. Paul Manafort has been targeted for months in the Mueller investigation; he left Trump’s campaign in 2016 after information surfaced about his work in Ukraine for a pro-Russian party.

- According to Kepler Cheuvreux research, the momentum of the euro’s recovery has been broken, and the revival of the dollar is now apparent to all. The research group’s target for pan-European equity benchmarks appear to be in reach in November. The world has become more aware of the investment risk associated with the crisis in Spain. The Spanish market was downgraded from Neutral to Underweight. The UK-EU negotiations have entered a critical phase and it seems as if the perception of political risk has returned to Europe.

- Despite the fact that crude oil continues to perform well, Deutsche Bank is not positive that fourth-quarter financial results in the Russian oil sector will be better quarter-over-quarter. The third quarter set a particularly strong base, and there is a seasonal pick up in operating expenses in the final quarter of the year. Pavel Kushnir, Deutsche Bank analyst, expects export duties on crude oil to increase in the fourth quarter, negatively affecting company earnings.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits