On Friday, I touched on the proposed “tax cut/reform” bill introduced by the House Ways and Means committee which is chaired by Congressman Kevin Brady. Some of the key highlights of the “House plan” are as follows (courtesy of Zacks Research):

- No change to 401(k) contribution caps

- Repeal the Alternative Minimum Tax (AMT)

- Corporate tax rate at 20% (aims to be a permanent cut)

- Top individual tax rate 39.6% threshold at $1 million

-

Cut the current 7 individual tax brackets down to 4:

- 12% for $45,000 ($90,000 married) and lower

- 25% for $45,001 – $200,000 ($90,000 – $260,000 married)

- 35% for $200,000 – $500,000 ($260,000 – $1,000,000 married)

- 39.6% for $500,000+ ($1,000,000+)

- Estate tax threshold doubles and gets repealed starting in 2024

- Deductions limited to $10,000 on property tax and 500,000 on “new mortgages”.

-

Pass-throughs

- Passive owners of pass-through get 25% rate

- Active owners have different standard

- Presumes 70% of pass-through income is attributable to labor and would be taxable at higher individual income tax rates

- For professional service firms default rate would be 100% of labor – no benefit from 25% rate

- Repeals itemized deduction for medical expenses

- Repeals credit for adoption

- Child tax credit at $1600 and creates $300 credit for each parent – $300 credits expire after 2022

- Repeals deduction for student loan interest

- No expansion of charitable giving limits

- For corporations, 10% tax on US companies’ high profit foreign subsidiaries calculated on global basis

- Foreign companies operating in US face up to 20% tax on payments made abroad from US operations to prevent deduction load-up

- Tax rate could be lowered by companies agreeing to increase US operations

- Interest deductions capped at 30% of EBITDA – exemption for real estate firms and small businesses

While on the surface this tax proposal looks promising, when you dig into the details the outcome looks less robust.

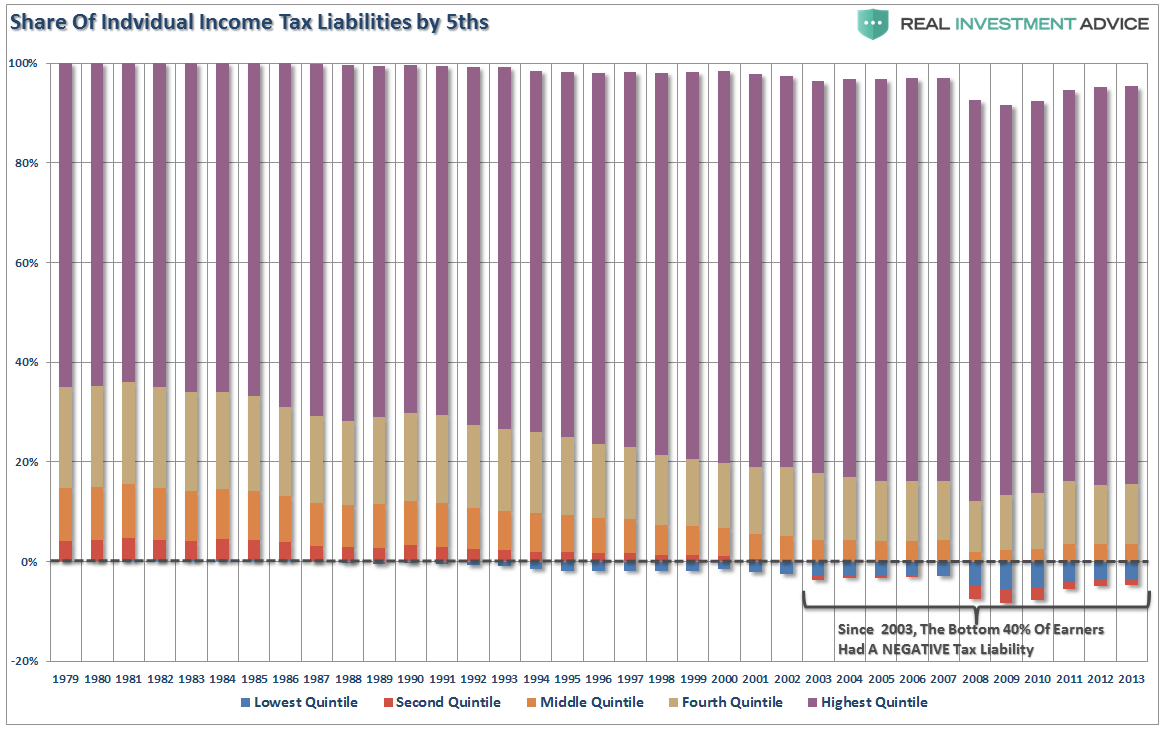

Many of the proposed changes may sit wrong with the public as some of today’s more popular deductions will be reduced or repealed. Furthermore, when lumping individuals into fewer income brackets, combined with deduction eliminations, the result may actually create a “tax increase” on the bottom 40% of earners. As I noted on Friday the bottom 80% of tax payers currently pay only about 18% of the total individual tax liability with top 20% paying the rest. But the bottom 40% currently have a NEGATIVE tax liability and the elimination, or reduction, of many of the deductions could increase taxes for many.

Importantly, notice the trend of those in the bottom 80% of taxpaying Americans. Ever since Reagan passed “tax reform,” the trend of Americans that do not pay taxes has trended steadily higher.

While Republican’s rush to promote the “tax bill” as the biggest tax cut for Americans ever, they also have to find ways to offset the initial reduction in tax collections so as to NOT expand the deficit by more than the estimated $1.5 Trillion dollars. By doing so Senate republicans can pass tax reform with only a 51-vote majority through the“reconciliation” process, otherwise it would require 60-votes which would be impossible for the current Senate to obtain.

Therefore, if order to “score” the bill to fit within that $1.5 trillion window, Republicans, are relying on several “myths”about how tax cuts will “pay for themselves” in the future as:

- Tax cuts will lead to stronger economic growth

- Tax cuts will increase wages for American workers

- Tax cuts will reduce Federal debt and deficit levels.

Let’s look at each one.

The Myths Of Tax Cuts

Myth #1: Tax Cuts Will Create An Economic Revival

As the Committee for a Responsible Federal Budget stated last week:

“Tax cuts do not pay for themselves; they can create growth, but in the amount of tenths of percentage points, not whole percentage points. And they certainly cannot fill in trillions in lost revenue. Relying on growth projections that no independent forecaster says will happen isn’t the way to do tax reform.”

That is absolutely correct and as I pointed out on Friday:

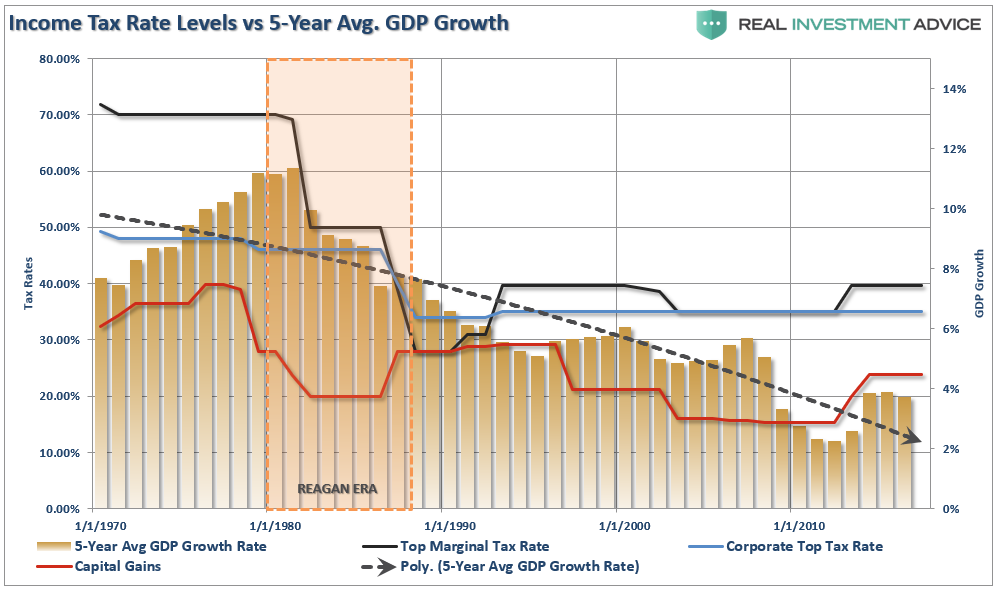

“As the chart below shows there is ZERO evidence that tax cuts lead to stronger sustained rates of economic growth. The chart compares the highest tax rate levels to 5-year average GDP growth. Since Reagan passed tax reform, average economic growth rates have only gone in one direction.”

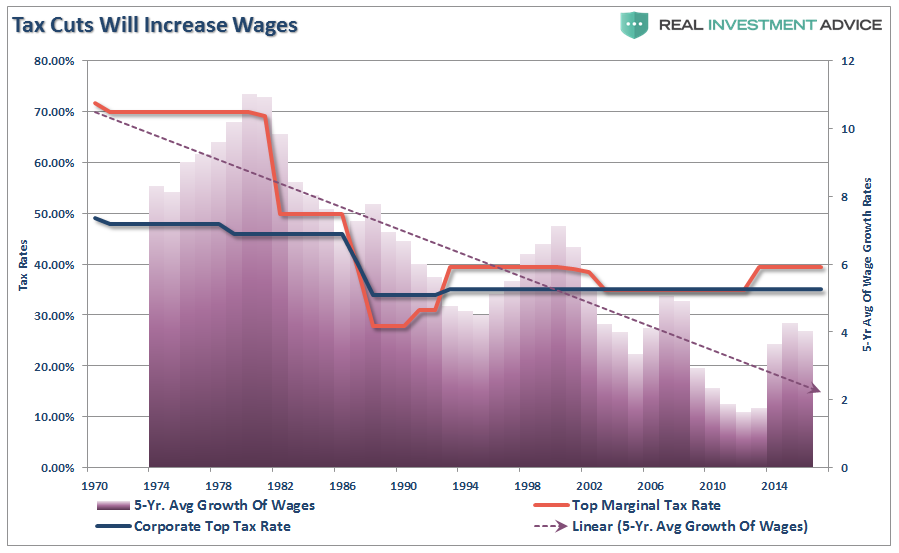

Myth #2: Tax Cuts Will Lead To A Rise In Wages

The same is true for the myth that tax cuts lead to higher wages. Again, as with economic growth, there is no evidence that cutting taxes increases wage growth for average Americans.

In fact, as I discussed previously:

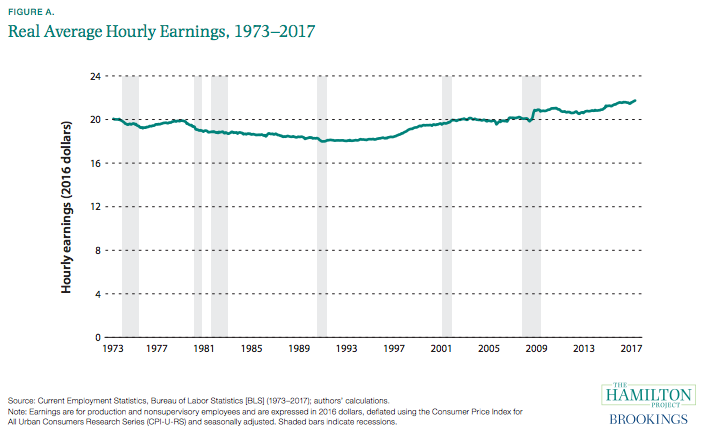

“An expansion that began, believe it or not, more than seven years ago has extended a longer-run trend of wage stagnation for the average US worker, despite a sharp drop in the official unemployment rate to 4.4% from an October 2009 peak of 10%.

After adjusting for inflation, wages are just 10% higher in 2017 than they were in 1973, amounting to real annual wage growth of just below 0.2% a year, the report says. That’s basically nothing, as the chart below indicates.”

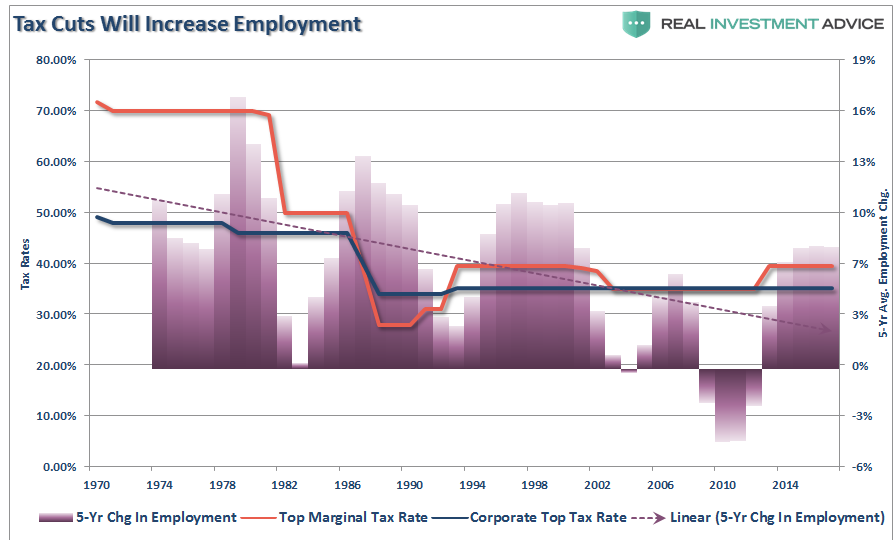

Furthermore, the idea that companies will begin to increase employment is likely overestimated as well. With the long-run trend of employment growth declining, not to mention we are very late in the current economic cycle, tax cuts are unlikely to sharply increase employment rates.

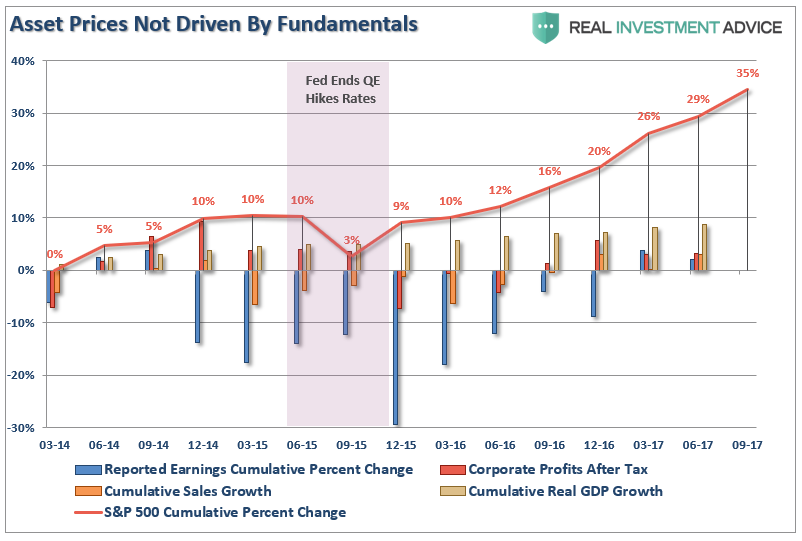

This is particularly the case currently as companies are sourcing every accounting gimmick, share repurchase or productivity increasing enhancement possible to increase profit growth. While asset prices have surged higher, the underlying fundamental growth story remains weak.

“The chart below expands that analysis to include four measures combined: Economic growth, Top-line Sales Growth, Reported Earnings, and Corporate Profits After Tax. While quarterly data is not yet available for the 3rd quarter, officially, what is shown is the market has grown substantially faster than all other measures. Since 2014, the economy has only grown by a little less than 9%, top-line revenues by just 3%along with corporate profits after tax, and reported earnings by just 2%. All of that while asset prices have grown by 29% through Q2.”

Myth #3: Tax Cuts Will Pay For Themselves

While the GOP has, for the last 8-years, continued to wield “fiscal conservatism” as a badge of honor, they have completely abandoned those principals in recent months in a full-blown effort to achieve “tax reforms.”

We are told, by these same Republican Congressman and Senators who just recently passed a fiscally irresponsible 2018 budget of more than $4.1 trillion, that tax cuts will “pay for themselves” over the next decade as higher rates of economic growth will lead to more tax collections.

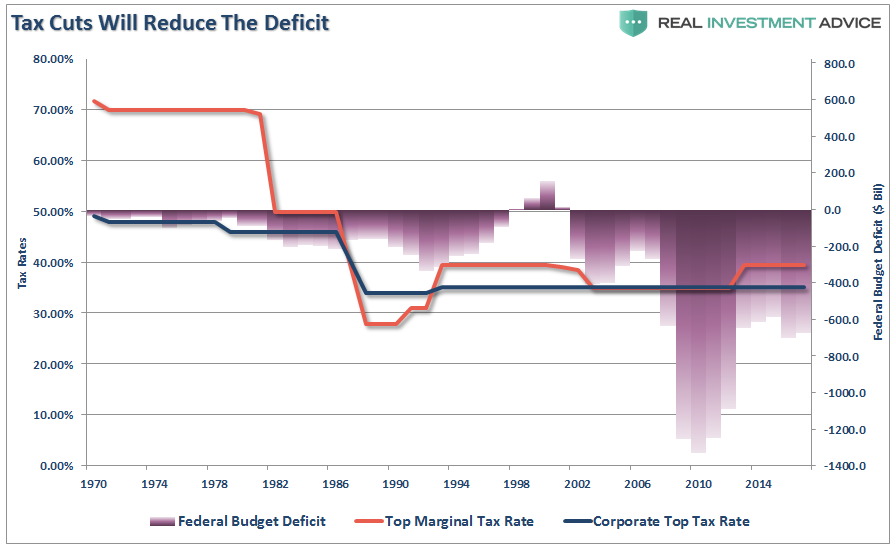

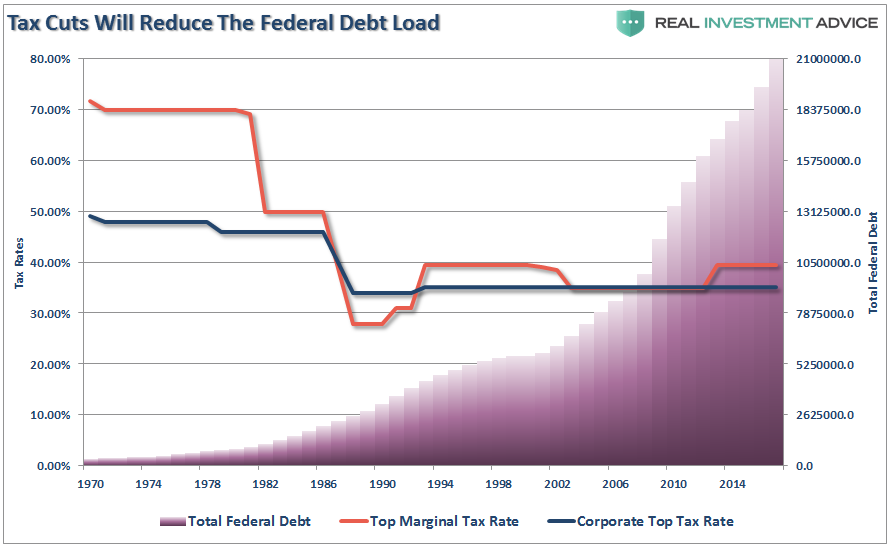

However, once again, we see that over the “long-term” this is simply not the case as the deficit has continued to grow during every administration since Ronald Reagan. Furthermore, the widening deficit has led to a massive surge in Federal debt which is currently pushing $21 trillion and growing much faster than economic activity, or the nations ability to pay if off.

Effective Outcome

The effective outcome of tax cuts at this juncture will result in:

- Only provide a minimal impact to economic growth, if any at all.

- An expansion of the debt of between $2-5 Trillion depending on the severity of the next recessionary drag.

- A ballooning of the budget deficit as entitlements rise with the expansion of child tax credits.

- A further divide in the “wealth gap” between those in the top 10% and the bottom 90%.

The data suggests the myth that income tax cuts raise growth has been repeated so often it is now believed to be true. However, theory, evidence, and historical studies tell a different and more complicated story.

I am not stating that tax cuts don’t offer any potential to raise economic growth by improving incentives to work, save, and invest. However, tax cuts also create income effects that reduce the need to engage in productive economic activity, and they may subsidize old capital, which provides windfall gains to asset holders that undermine incentives for new activity.

In addition, Republicans are engaged in trying to use tax cuts as a stand-alone policy, rather than tying them to spending cuts, which will raise the federal budget deficit. It is important to consider that an increase in the deficit diverts income from productive investment as the underlying debt swells and must be serviced.

With the economic dynamics not supportive (debt, demographics, productivity and deflation) of further fiscal deficits, tax cuts, without spending cuts, are not self-supporting. Given today’s record-high and rapidly growing levels of national debt, the country cannot afford a deficit-financed tax cut. Tax reform that adds to the debt is likely to slow, rather than improve, long-term economic growth.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter and Linked-In

© Real Investment Advice

© Real Investment Advice

Read more commentaries by Real Investment Advice