Synchronized Global Growth May Have Arrived

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

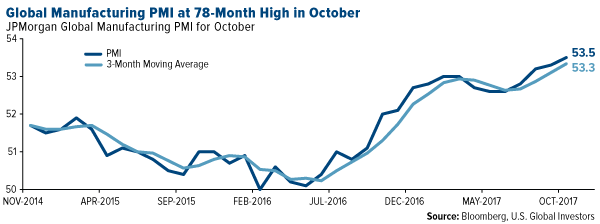

Nearly 10 years after the financial crisis brought the global economy to its knees, conditions have finally improved enough to crystallize my conviction that synchronized global growth is currently underway. Revenue and earnings growth are up year-over-year, not just in the U.S. but worldwide. Despite President Donald Trump threatening to raise tariffs and tear up trade deals, global trade is accelerating. World manufacturing activity expanded to a 78-month high of 53.5 in October, with faster rates recorded in new orders, exports, employment and input prices.

Additional trends and indicators support my bullishness. Worldwide business optimism, as recorded by October’s IHS Markit Global Business Outlook survey, climbed to its highest level in three years, with profits growth and hiring plans continuing to hit multiyear highs. Optimism among U.S. firms was at its highest since 2014, with sentiment above the global average for the second straight survey period.

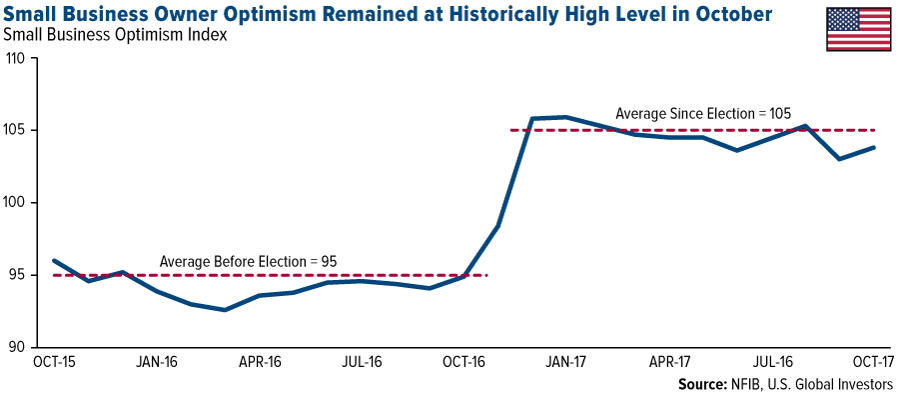

Small business owners’ optimism remained at historically high levels in October, according to the latest survey conducted by the National Federation of Independent Business (NFIB). Its Small Business Optimism Index came in at 103.8, up slightly from September and extending the trend we’ve seen since the November 2016 election.

As I told CNBC Asia anchor Bernie Lo this week, U.S., Europe and China’s economies are strong, which is igniting the rest of the world. The eurozone purchasing manager’s index (PMI), in particular—rising to 58.5 in October, an 80-month high—is very constructive for world economic growth in the next six months.

Fewest Number of Countries in Recession

Speaking on CNBC’s “Trading Nation” recently, Deutsche Bank chief international economist Torsten Slok made the case that global economic health “has never been more robust,” citing the fact that the number of countries in recession has dropped to its lowest level in decades.

“We have never seen a smaller number of countries in recession as we do at the moment,” Slok said. “And if you look ahead to the next few years… we are going to see that fall even lower.”

The Organization for Economic Cooperation and Development (OECD) backs up this claim in its quarterly economic outlook. According to the Paris-based group, synchronized global growth is finally within sight, with no major economy in contraction mode for the first time since 2008. World GDP is expected to advance 3.5 percent in 2017—its best year since 2011—and 3.7 percent in 2018.

Taken together, this should help boost exports and global trade even further as more countries have the capital and demand to make purchases on the world market.

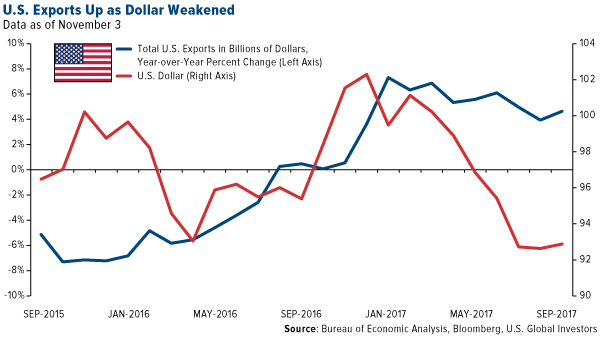

Bolstered by a weaker U.S. dollar, exports by American firms hit a three-year high in August, the Commerce Department reported this month. Exports rose to nearly $200 billion, the highest level since December 2014.

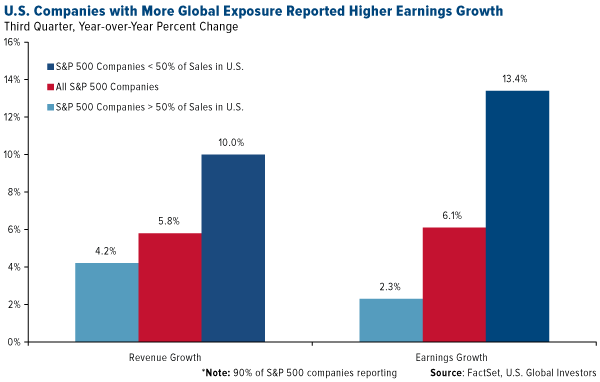

As further proof that the global economy is humming along, S&P 500 Index companies with greater exposure to foreign markets, especially Europe, saw higher revenue and earnings growth in the third quarter than those companies whose business is more focused domestically.

According to FacSet data, revenue grew 10 percent year-over-year for firms that generated 50 percent or more of their sales outside the U.S., compared to only 4.2 percent for firms whose sales were conducted mostly within the U.S. The difference was even greater for earnings growth—13.4 percent for S&P 500 companies with strong foreign exposure, 2.3 percent for companies with less exposure.

We saw similarly impressive results with Dow Jones Industrial Average (DJIA) companies. According to FactSet’s November 17 Earnings Insight :

Overall, 11 of the 30 companies in the DJIA provided revenue growth numbers for Europe for the third quarter. Of these 11 companies, nine reported year-over-year growth in revenues. This number was the highest number of Dow 30 companies… to report revenue growth in Europe on a quarter basis since Q2 2014. Of these nine companies, five reported double-digit revenue growth in Europe for the third quarter.

FactSet adds that Nike reported its seventh straight quarter of year-over-year revenue growth in European markets, Apple its fifth straight quarter.

As of today, 95 percent of S&P 500 companies have reported earnings for the third quarter, and of those, nearly three quarters have logged earnings per share (EPS) that are above the five-year average.

The U.S. isn’t the only economy that’s had a standout quarter. According to Thomson Reuters data, 65 percent of companies in the MSCI Europe Index have beaten third-quarter expectations, with overall year-over-year earnings growth standing at nearly 10 percent.

Enthusiasm Over Corporate Tax Cuts Drive Stock Prices Higher

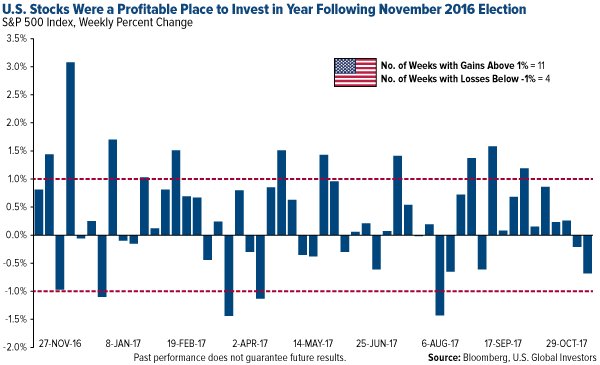

As you’re likely aware, it’s been one year since the U.S. election, and since then the market has surged more than 21 percent on improved global growth, higher corporate earnings and hopes that President Trump’s pro-growth agenda of tax reform and deregulation will improve business conditions in the U.S. In the past 12 months, there have been nearly three times as many weeks posting market gains above 1 percent than those with losses below negative 1 percent. This makes it one of the most profitable markets to have invested in for many years.

So where does the Trump rally rank? Looking at the 12 months following every November presidential election since 1950, LPL Research found that the bull run we’ve seen under Trump ranks fifth place, following Presidents Bush Sr. in 1988; Obama in 2012; Kennedy in 1960 and, in first place, Clinton in 1996, with gains climbing to nearly 32 percent.

|

Where Does the Trump Rally Rank? |

||||

| Election Date | Winning President | S&P 500 Return One Year Later | Rank | |

| 11/05/1996 | Clinton | 31.7% | 1 | |

| 11/08/1960 | Kennedy | 28.4% | 2 | |

| 11/06/1912 | Obama | 23.9% | 3 | |

| 11/08/1988 | Bush Sr. | 21.7% | 4 | |

| 11/08/2016 | Trump | 21.1% | 5 | |

| Past performance does not guarantee future results. Source: LPL Research, FactSet, U.S. Global Investors |

||||

Before year’s end, we could see prices appreciate even more as investors act on enthusiasm over tax reform. This week the House approved $1.5 trillion in tax cuts that, if signed into law, would slash corporate taxes down from 35 percent to a much more competitive 20 percent. The bill is now in the Senate’s court where hopefully it doesn’t suffer the same fate as the failed Obamacare repeal-and-replace efforts. Goldman Sachs analysts place the chances of tax reform being completed by early 2018 at 80 percent—encouraging for sure, but there are some tough challenges ahead. A handful of Republican Senators, including Jeff Flake (AZ) and Ron Johnson (WI), have already said they will not vote for the Senate bill as it’s currently written.

Despite the bill’s uncertain future, markets responded very favorably to the House news. The S&P 500 Index closed up 0.82 percent on Thursday, its best one-day move since June, with gains led by retailers such as Foot Locker, Ross Stores and Gap.

Next week I’ll have more to add on consumer spending forecasts for the upcoming holiday shopping season. This Black Friday is expected to be the largest-ever for online shopping. In the meantime, explore investment opportunities in domestic companies with exposure to foreign markets by clicking here!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.27 percent. The S&P 500 Stock Index fell 0.14 percent, while the Nasdaq Composite climbed 0.47 percent. The Russell 2000 small capitalization index gained 1.18 percent this week.

- The Hang Seng Composite lost 0.20 percent this week; while Taiwan was down 0.29 percent and the KOSPI fell 0.35 percent.

- The 10-year Treasury bond yield fell 5.5 basis points to 2.34 percent.

Domestic Equity Market

Strengths

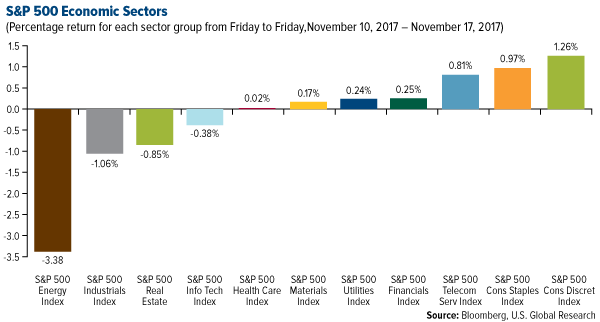

- Consumer discretionary was the best performing sector of the week, increasing by 1.26 percent versus an overall decrease of 0.13 percent for the S&P 500.

- Foot Locker was the best performing stock for the week, increasing 34.54 percent.

- Walmart beat and raised guidance as online growth explodes. The company said U.S. comparable-store sales rose by 2.7 percent versus a year ago, making for the thirteenth straight quarter with positive results.

Weaknesses

- Energy was the worst performing sector for the week, falling 3.38 percent versus an overall decrease of 0.13 percent for the S&P 500.

- General Electric was the worst performing stock for the week, falling 11.13 percent.

- The rough year for General Electric shareholders has yet to end as GE shares had their worst day since 2009 on Monday, falling 7 percent after the company reduced its dividend and unveiled a restructuring plan during its investor day. RBC Capital Markets lowered its rating to sector perform from outperform saying the company did not present a credible plan to fix its businesses.

Opportunities

- Amazon won the UK rights to broadcast the ATP World Tour and will stream 37 men's games to British Prime subscribers. The company won the rights from Sky, amid signs the firm will step up its sports content.

- Cisco beat analysts' expectations and climbed out of an 8-quarter revenue decline streak. The company posted $12.136 billion in revenue for the first quarter of 2018, compared to the previous quarter when it saw $12.133 billion come in.

- Elon Musk unveiled Tesla's first electric truck on Thursday evening, promising greater safety and efficiency than a diesel vehicle. The company says the semi-truck will have a range of up to 500 miles a charge and can charge up to 400 miles in just 30 minutes when using a newly released high-speed Megacharger. The company also announced a surprise new model of its Roadster sportscar at a base cost of $200,000. The roadster will be able to do 0 to 60 miles per hour in 1.9 seconds.

Threats

- According to investment manager John Hussman, stocks are flashing an ominous signal not seen since the financial crisis. He points out that stock market dispersion is widening, while two technical indicators known as the Hindenburg Omen and Titanic Syndrome flashed sell signals.

- According to Bank of America Merrill Lynch, “irrational exuberance” could spell disaster for markets. The company is sounding the alarm on what they perceive to be investor overconfidence, as valuations sit near record highs and cash levels dwindle.

- Norway's trillion-dollar sovereign wealth fund is proposing to drop oil and gas companies from its benchmark index, which would mean cutting its investments in those companies, the deputy central bank chief supervising the fund told Reuters, sending energy stocks lower.

The Economy and Bond Market

Strengths

- U.S. homebuilding jumped to a one-year high in October as disruptions from recent hurricanes faded and communities in the region started replacing homes damaged by flooding. Housing starts surged 13.7 percent to a seasonally-adjusted annual rate of 1.29 million units. That was the highest level since October 2016 and also the second-best reading in 10 years. September’s sales pace was revised up to 1.135 million units from the previously reported 1.127 million units.

- U.S. industrial output accelerated in October as a result of manufacturing production bouncing back after hurricane-related disruptions. Industrial production rose to a seasonally-adjusted 0.9 percent in October from the prior month. Economists surveyed by The Wall Street Journal had expected a 0.6 percent gain for September.

- U.S. producer prices rose more than expected in October, driven by a surge in the cost of services, leading to the biggest annual increase in wholesale inflation in more than five-and-a-half years.

Weaknesses

- Various pieces of economic data from China posted weaker-than-expected readings. Industrial output, retail sales and fixed-asset investment all missed to the downside in October, according to data released by China's National Bureau of Statistics.

- Japan's economy lost momentum as it grew at a 0.3 percent quarter-over-quarter pace in the September quarter, decelerating sharply from the previous quarter's 0.6 percent growth.

- Euro-area inflation slowed to an annual rate of 1.4 percent in October as telecommunication, garments and social protection had the biggest downward impacts, Eurostat data showed.

Opportunities

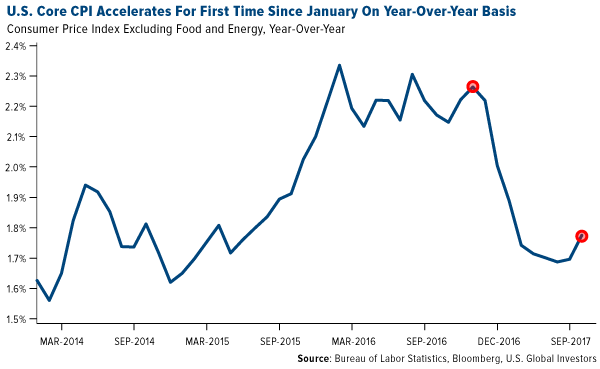

- U.S. inflation excluding food and fuel accelerated on an annual basis for the first time since January, climbing 1.8 percent from October 2016, according to the Labor Department. The pickup should be welcomed by Federal Reserve officials debating the pace of interest-rate increases and may help reinforce investors’ expectations that the central bank will raise rates in December for the third time this year.

- The FCC is set for a final vote next week to reverse net neutrality rules in the U.S., paving the way for Internet providers to block or throttle websites. FCC chair Ajit Pai claims the existing regulation harms jobs and investment.

- Tax reform passed in the House by a vote of 227-205, mostly along party lines.

Threats

- Abolishing advance refundings would imperil Connecticut's plan to rescue Hartford. The state offered to lend its backing to help refinance some of Hartford’s $620 million debt. “It would be catastrophic if that bill passed as it was written in the House," said Hartford Treasurer Adam Cloud. “We do have bonds as part of our restructure that we would look to advance refund. To do that on a taxable basis would be costly."

- Other municipalities could feel the pain from tax reform, too. Nearly all the major proposals of the Republican tax plan will have a "direct, negative link to credit quality" for municipal issuers, S&P said Thursday. Demand from banks, insurers and other companies could decrease because of lower corporate tax rates. That "would result in an increased cost of borrowing for municipal issuers and decreased market access for some."

- People are underrating the odds of a government shutdown in December. According to Business Insider's Josh Barro, while President Donald Trump and congressional leaders prevented one fairly easily in September, it will be different in December.

This week spot gold closed at $1,293.77, up $18.30 per ounce, or 1.43 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.82 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index came in up just 0.29 percent. The U.S. Trade-Weighted Dollar fell this week 0.77 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-13 | China Retail Sales YoY | 10.5% | 10.0% | 10.3% |

| Nov-14 | Germany CPI YoY | 1.6% | 1.6% | 1.6% |

| Nov-14 | Germany ZEW Survey Current Situation | 88.0 | 88.8 | 87.0 |

| Nov-14 | Germany ZEW Survey Expectations | 19.5 | 18.7 | 17.6 |

| Nov-14 | PPI Final Deman YoY | 2.4% | 2.8% | 2.6% |

| Nov-15 | CPI YoY | 2.0% | 2.0% | 2.2.% |

| Nov-16 | Eurozone CPI Core YoY | 0.9% | 0.9% | 0.9% |

| Nov-16 | Initial Jobless Claims | 235k | 249k | 239k |

| Nov-17 | Housing Starts | 1190k | 1290k | 1135k |

| Nov-22 | Initial Jobless claims | 240k | -- | 249k |

| Nov-22 | Durable Goods Orders | 0.3% | -- | 2.0% |

Strengths

- The best performing precious metal for the week was silver, up 2.53 percent. It has lagged behind the other precious metals this year and speculators have raised their net long position this week. Gold bounced back positively after several attempts to knock down the price. Last Friday, over 4 million ounces of gold changed hands within minutes. Then, this past Tuesday, more than 2 million ounces changed hands, spurring a price drop. Bullish investors responded two hours later with a surge in buying to help boost prices.

- Lawrie Williams writes that the attempt to lower gold prices mentioned above reflects positively for those who consider gold to still be in a bull market.

- Ray Dalio of Bridgewater went on a gold-buying spree to increase his holdings by 575 percent and enter the gold ETF space. Perhaps buyers following Dalio’s lead are using these sell-offs to pick their entry spots.

Weaknesses

- The worst performing precious metal for the week was palladium, up just 0.05 percent for the week. “Palladium prices could plunge 90 percent by 2040 as cars become electric,” reported ABN Amro. According to Reuters India, gold prices flipped to discount as wedding demand for the yellow metal were lower than expected. Additionally, the Federal funds futures show a possible rate increase in December at 92 percent.

- BMI cut the average price forecast for gold next year to $1,300 per ounce from $1,350 previously. As a result, UBS strategist Joni Teves reversed her position on gold from bullish to neutral, believing there is no catalyst to justify a strong rally in gold prices or one to cause a substantial fall in prices.

- Operations at one of Banro’s mines in the Democratic Republic of Congo have been suspended since September. This week, the company announced doubt at continuing the project as they are unable to raise enough capital.

Opportunities

- Marlin Gold announced a plan to spin off a subsidiary, Sailfish Royalty, to enhance respective business operations and provide shareholders with additional investment choices and flexibility. Investors will receive one Sailfish Royalty share for every five common shares of Marlin Gold. Typically, such spin-out opportunities have resulted in enhanced values for shareholders.

- This week, Zimbabwe’s military seized power from the only leader they’ve ever known, President Robert Mugabe. Zimbabwe is a nation rich in minerals and the change in power could be an opening for economic growth to be reestablished. Caledonia Mining Corp. (TSX: CAL) is one of the few listed gold mining companies operating within Zimbabwe.

- Klondex Mines’ Fire Creek exploration results demonstrate the potential for resource expansions with senior vice president of exploration Brian Morris saying, “the surface drill results are extremely exciting” at 8.25 ounces per ton of gold over 1.7 feet. In addition to rising stock price, analysts raised consensus earnings estimates for quarter four to 6.6 cents per share from 5.6 cents per share, according to Bloomberg. Klondex Mines also saw insider buying of company stock which signals optimism of future growth.

Threats

- Uncertainty arises as Federal Reserve officials push for a radical revamp of the playbook for guiding U.S. monetary policy as growth and productivity have been tepid under the current 2 percent inflation target. Measures may allow for flexible play book as a new Fed Chairperson takes the reins.

- Economists at Goldman Sachs and JP Morgan are forecasting that the Federal Open Market Committee next year will likely tighten four times, rather than three times as implied in policy maker projections, according to Bloomberg. Economists stress that inverted yield curves prove a reliable indicator of an impending recession and that when the spread between short- and long-term debt shrinks, it hurts bank earnings and the real economy. The yield curve is at its flattest level in a decade, not leaving the Fed much room to maneuver.

- The Federal Reserve is shrinking its balance sheet and raising interest rates, which leads some to believe that it’s unlikely gold will thrive in that environment, according to Ranjeetha Pakiam at Bloomberg. Matthew Turner from Macquarie Group says that it’s cheaper to hold a non-interest bearing asset such as gold when rates are low because higher rates are thought to be negative for prices. He continued to say that gold was strong in the last cycle and flat in the other cycles with a historical analysis of gold in a tightening cycle showing no safe conclusion.

Energy and Natural Resources Market

Strengths

- Gold was the best performing major commodity this week rising 1.5 percent. The yellow metal rallied amid uncertainty about the passage of U.S. tax cuts and renewed concerns over the investigation into Russia’s meddling in last year’s election.

- The best performing sector this week was the S&P 1500 Paper and Forest Products Index. The index rose 1.2 percent tracking lumber prices, which traded at an all-time high on Wednesday as Canadian producers pass double-digit import duties directly to U.S. consumers as the building materials market fears a lumber shortage.

- Daqo New Energy Corporation, a Chinese manufacturer of parts and cells used in solar power products, was the best performing stock in the broader resource market this week. The stock rallied 8.2 percent to a 52-week high after the company reported strong revenue and earnings’ growth in the third quarter as pricing for its products continues to rise.

Weaknesses

- Brent crude prices dropped 1.3 percent; the most among major commodities. Prices dropped after the International Energy Agency increased its supply growth forecasts. According to the Agency, growth in U.S. oil output until 2025 will be the strongest seen by any country in the history of crude markets, making it the “undisputed” leader among global producers.

- The worst performing sector this week was the S&P/TSX Oil & Gas Exploration and Production Index. The index dropped 7 percent after crude prices softened throughout the week.

- The worst performing stock for the week was Nine Dragons Paper Holdings. The Hong Kong-based producer of containerboard products dropped 10 percent after Deutsche Bank reported China paper prices have crashed 19 percent in the last two weeks, while lumber and other input prices have continued their upward trajectory.

Opportunities

- Renewables, led by wind and solar, will capture two-thirds of global investment in power plants as they become, for many countries, the cheapest source of new generating capacity, the International Energy Agency said. The FT reported that solar will become the biggest source of “green” power by 2040, by which time the share of all renewables in global power generation will reach 40 percent, led by China and India.

- Crude prices rose on Friday, nearly offsetting the week’s drops after Saudi Arabia’s energy minister reiterated the nation remains committed to negotiate for an extension of OPEC’s oil-output cuts agreed in November last year.

- Vitol’s Seaways Laura Lynn, a supertanker as long as the Empire State building is high, has finally offloaded its crude in a sign that the market has truly turned a corner, according to oil traders cited by the FT. Laura Lynn sat laden with oil off the coast of Oman for more than two years, carrying a cargo of more than 3 million barrels of crude. This week the trading house has suddenly unloaded the majority of its oil on to smaller tankers for delivery to hungry refineries.

Threats

- Crude prices dropped as the International Energy Agency increased its supply growth forecasts. According to the Agency, growth in U.S. oil output until 2025 will be the strongest seen by any country in the history of crude markets, making it the “undisputed” leader among global producers.

- Chinese growth in factory output, fixed-asset investment and retail sales all slowed in October, as Beijing imposed tighter pollution controls and continued restrictions on home purchases. M2 money supply was lower than expected at 8.8 percent in October, the weakest increase on record. Weaker fixed-asset investments and property purchases translate into softer demand for raw commodities, while lower money supply growth has negative implications for credit availability.

- Wheat prices at the Chicago Board of Trade hit $4.19 a bushel this week, down almost 25 percent since Russia began a record wheat harvest in July. Russian farmers are forecast to have reaped a bumper harvest this season, aided by large investments and a weaker ruble, and ratcheted up the pressure on U.S. farmers, who sowed fewer acres of wheat in 2017 than ever before.

Strengths

- Thailand, Vietnam and Indonesia came in positive for the week, rising 1.19, 2.61 and 0.50 percent.

- Malaysia’s third quarter GDP reading came in up 6.2 percent year-over-year, surpassing analysts’ expectations for a gain of only 5.7 percent.

- Philippines’ third quarter GDP reading came in at 6.9 percent year-over-year, beating expectations for a 6.6 percent reading and constituting the ninth straight quarter of more than 6 percent growth.

Weaknesses

- The Shanghai Composite dropped 1.45 percent for the week, barely nudging out the Philippines Composite Index, which declined 1.42 percent for the week.

- Both New Yuan and Aggregate Financing came in weaker than expected in China. New Yuan loans came in at 663.2 billion, shy of expectations for 783.0 billion, and Aggregate came in at 1040.0 billion, short of expectations for a print of 1100.0 billion.

- Retail Sales came in weaker than expected in China for the October period, at only 10.0 percent year over year versus expectations for a 10.5 percent gain.

Opportunities

- The number of Hong-Kong-bound tourists rose 1.8 percent annually in the third quarter, Bloomberg News reports, making it the first quarter of growth three years marking the end of a three-year contraction.

- Late last week it was announced Country Garden and Sunny Optical Technologies will join Hong Kong’s blue chip Hang Seng Index, effective December 4. The two names are to be added at the expense of Cathay Pacific and Kunlun Energy, which will be dropped accordingly from the index. Guangzhou Auto will be added to the Hang Seng China Enterprises Index, with China Longyuan to be removed.

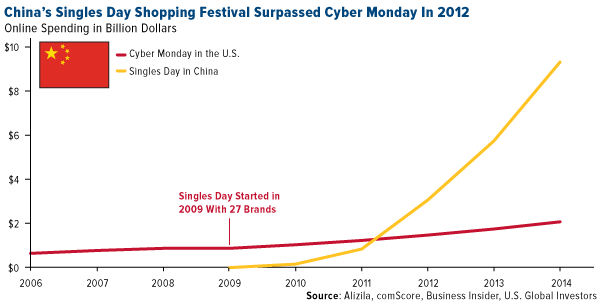

- The Chinese commercial phenomenon known as “Singles’ Day” smashed additional sales records this year, ringing up more than USD $25 billion worth of cyber sales in 24 hours, far surpassing the combined sales of U.S. retailers between last year’s “Black Friday” through “Cyber Monday.”

Threats

- Officials at last weekend’s ASEAN summit in Manila expressed doubt about finalizing anything with respect to the China-backed Regional Comprehensive Economic Partnership (RCEP) by the end of 2017, Bloomberg reports.

- The dramatic defection of a North Korean soldier this week calls fresh attention to the state of basic needs (like nutritious and untainted food) in a rogue East Asian nation that turns out soldiers filled with intestinal parasites. China also dispatched a special envoy to Pyongyang following U.S. President Donald Trump’s visit to Asia this week.

- Mainland-listed liquor producer Kweichow Moutai tumbled on Friday after a warning from the state, delivered through Xinhua News Agency, on the steep rise in the shares. The company subsequently issued its own warning to investors, Bloomberg News reports, in which Kweichow Moutai suggested that investors will be cautious and discriminating with respect to its “overly high” price.

- Lately several prominent members of the Trump administration (including the president himself as well as Rex Tillerson, U.S. Secretary of State) have made a point to emphasize and (re-)introduce the terminology of “Indo-Pacific” into geopolitical parlance, stressing a broader strategic role for India in the region (or at least in official statements), perhaps at China’s expense, perhaps to its annoyance, or perhaps both.

Strengths

- Romania was the best performing country this week, gaining 1 basis point. Romania reported very strong third quarter gross domestic product. Prime Minister Midai Tudose said that the 8.8 percent growth is sustainable. The budget gap will stay below the 3 percent of GDP level this year as economic growth helps to boost the country’s revenue.

- The Romanian leu was the best performing currency this week, gaining 1.3 percent against the dollar. Romania is growing at the fastest pace since 2008, inflation is accelerating and central bank may start tightening policy. Under normal economic conditions rate hikes will reduce inflation and increase the appreciation of the currency.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 3 percent. Greek banks were the biggest losers on the Athens stock exchange. The EU’s European Court of Auditors published a report criticizing the first and second Greek bailouts, launched in 2010 and 2012. They were not properly planned and failed to anticipate the recessionary effect of austerity measures, the report said. Creditors initially estimated that Greece would return to growth in 2012, but the country returned to growth this year.

- The Turkish lira was the worst performing currency this week, losing 30 basis points against the U.S. dollar. The country’s president criticized Turkey’s central bank for staying on the wrong path. Mr. Erdogan wants the central bank to cut rates, while a strong rate hike is needed to stop the currency deprecation.

- The industrial sector was the worst performing sector among eastern European markets this week.

Opportunities

- Third quarter flash GDP data was released this week and growth surprised to the upside. Central emerging Europe, Hungary, Poland and the Czech Republic reported better-than-expected growth supported by increasing household consumption and continued growth in investment expenditure. Romania’s GDP skyrocketed to 8.8 percent year-over-year, up from 6.1 percent in the second quarter. The growth of the biggest economy in Europe, Germany, surprised to the upside as well, driven mostly by investments and exports.

- Russian president Vladimir Putin met Turkish president Recap Taya Erdogan in Sochi this week. It was the sixth meeting the two leaders held together this year, discussing their next steps in Syria. Despite differing views on the Syrian President Bashar Assad, they managed to work together on Syria, helping both countries to restore bilateral trade. Putin said that relations between Moscow and Ankara have been “restored practically in full.”

- Next week, flash November purchasing managers’ index (PMI) data for the eurozone will be released. In October, the eurozone PMI rose to 58.5, expanding in each month since July 2013 and driven by an increase in output, new orders and employment. The eurozone’s economy is on track for a strong finish to 2017.

Threats

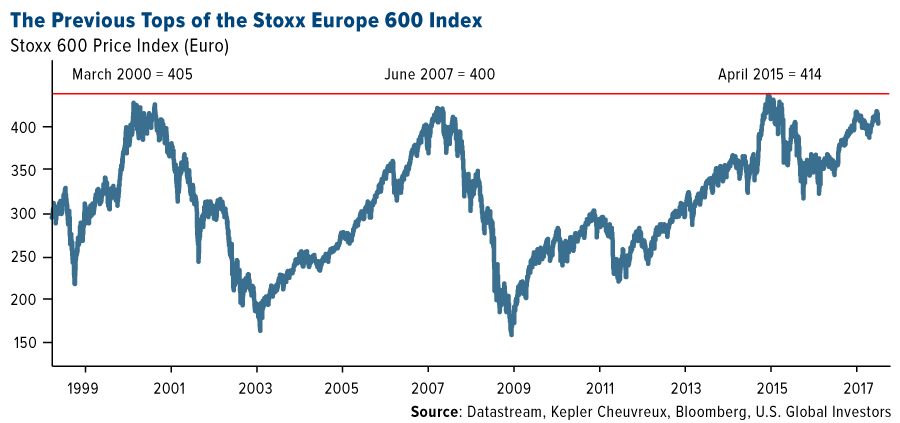

- Kepler Cheuvreuex in the “Sell When You Can Report,” wrote that “the recent phase of international outperformance by European equity is exhausted. The growth without inflation in Europe will not survive the end of this year.” The group thinks that investors have about three months until a significant equity market correction takes place. The chart below shows price performance of the STOXX 600 index, comprised of large, mid and small companies across 18 countries of the European region, as it is approaching Kepler’s price target of 400-415 for this year.

- The eurozone’s final inflation reading confirmed that consumer price index (CPI) data slipped from 1.5 percent in September to 1.4 percent in October, year-over-year. The final core inflation, excluding volatile food and energy prices, dropped to 0.9 percent from 1.1 percent in the prior month, although in line with the flash reading. According to Eurostat, the European Union's statistics office, inflation slowed last month on falling prices for telecommunications, clothes and social protection.

- Russia’s economy grew by 1.8 percent year-over-year in the third quarter, down from 2.5 percent growth in the second quarter of 2017. The slowdown was due to weaker growth in industrial production, which dipped to 1.2 percent in the latest quarter from 3.8 percent in the prior quarter.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits