Gobble, Gobble: Thanksgiving Dinners Stuffed with Savings Despite Rising Fuel Costs

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

I spend a lot of time writing and talking about inflation, especially as it affects the price of gold, oil and other commodities and raw materials. The year-over-year percent change in the cost of living has been reasonably low for the past five years, averaging about 1.3 percent on a monthly basis. For commodities, the average change has been even lower at negative 0.9 percent, as measured by the producer price index (PPI). This hasn’t been too constructive for gold and oil producers, but it’s been a windfall for American consumers and manufacturers.

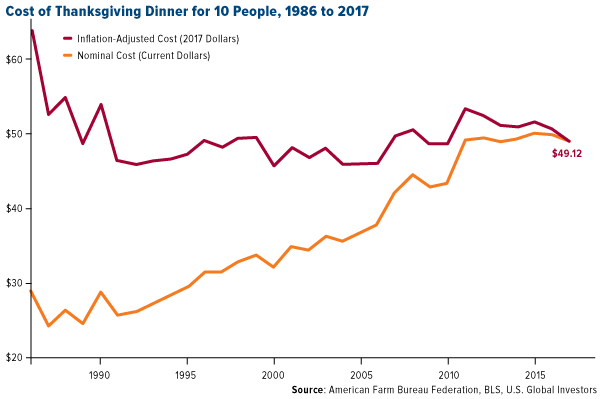

A helpful way to look at inflation is the changing cost of a typical Thanksgiving dinner for 10 people. For the second straight year, the cost actually declined from the previous year’s holiday, according to the American Farm Bureau Federation (AFBF). This year’s feast, including staples such as turkey, rolls, sweet potatoes and more, fell $0.75 to a five-year low of $49.12. On an inflation-adjusted basis, that’s down more than $10 from 30 years ago. The turkey alone cost about 1.6 percent less than last year.

Today shares of Tyson Foods, one of the top processors of the poultry, were trading above $80, up more than 30 percent year-to-date.

Again, this is good news for consumers. Also good? Multiple studies have found that Americans gain only about a pound in weight as a result of engorging themselves on Thanksgiving Day. So don’t feel so guilty about helping yourself to that extra slice of pumpkin pie.

Record Number of Americans Hit the Road and Take to the Skies

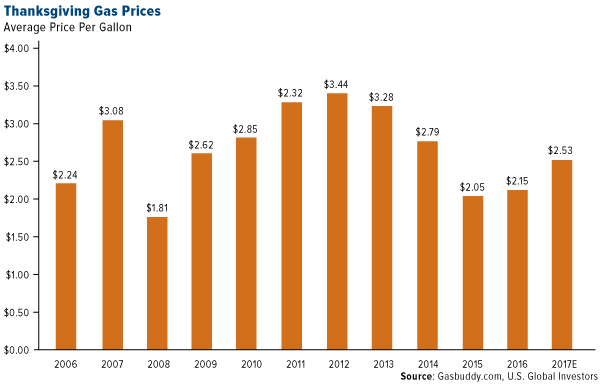

Holiday gasoline prices, however, are on the rise, with the cost per gallon rising to its highest level since 2014. A trip to the pump this Thanksgiving will cost motorists an extra 18 percent compared to last year and nearly 25 percent more compared to 2015.

As I shared with you earlier this month, oil prices climbed to two-year highs following Saudi Arabia’s purge of princes and ministers. Markets also appear to be pricing in expectations that the Organization of Petroleum Exporting Countries (OPEC) will extend production cuts to the end of 2018.

West Texas Intermediate (WTI) was trading today at a 52-week high of $59 a barrel. The next stop is $60, a level we haven’t seen since May 2015. In a strategy report this week, BCA Research recommended an overweight position in energy.

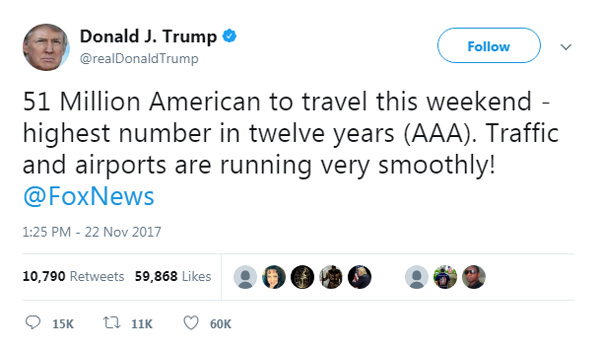

Higher fuel costs aren’t expected to discourage domestic travel, though. This Thanksgiving season, approximately 51 million Americans are projected to travel 50 miles or more from home on U.S. roads, highways, airlines, rails and waterways, according to the American Automobile Association (AAA). That’s up 3.3 percent from last year and the highest volume since 2005. President Donald Trump mentioned the impressive figure in a tweet this week, adding that “traffic and airports are running very smoothly!”

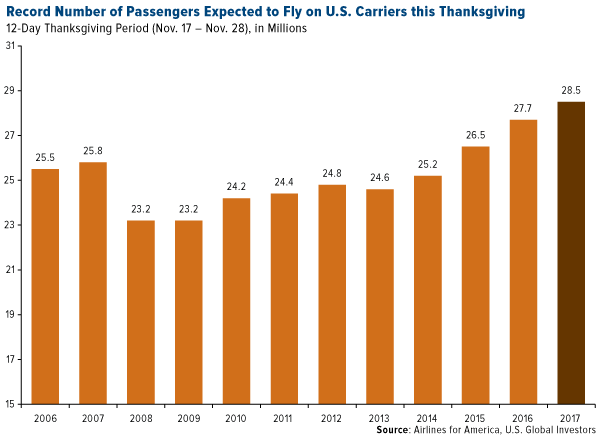

Looking at air travel alone, a record 28.5 million passengers are estimated to take to the skies this year during the 12-day Thanksgiving period, according to Airlines for America (A4A). That equates to an additional 2.38 million passengers a day.

With the economy improving, incomes on the rise and consumer confidence at multiyear highs, airline executives expressed optimism in continued flight demand growth and profitability. According to October’s Airline Business Confidence Survey, conducted by the International Air Transport Association (IATA), 80 percent of airline chief financial officers (CFOs) said profits improved in the third quarter compared to the same three-month period in 2016. An overwhelming 87 percent were confident such profitability would persist or improve over the next 12 months. Eighty-six percent of CFOs reported increased passenger demand year-over-year in the third quarter, while 71 percent expected traffic volumes to rise a year from now.

Holiday Shopping Sales Could Exceed $107 Billion

On a final note, retailers are bracing for a blowout holiday shopping season. Earlier this month, Adobe Analytics released its forecast that U.S. sales during the Thanksgiving weekend and Cyber Monday could climb above $107 billion, a year-over-year increase of 13.8 percent. Cyber Monday alone might generate as much as $6.6 billion, 16.5 percent more than last year, making it the largest online sales day in history. Among the most hotly anticipated gift items this year are Apple Air Pods, home assistants (Amazon Echo and Google Home) and Sony PlayStation virtual reality (VR) headsets.

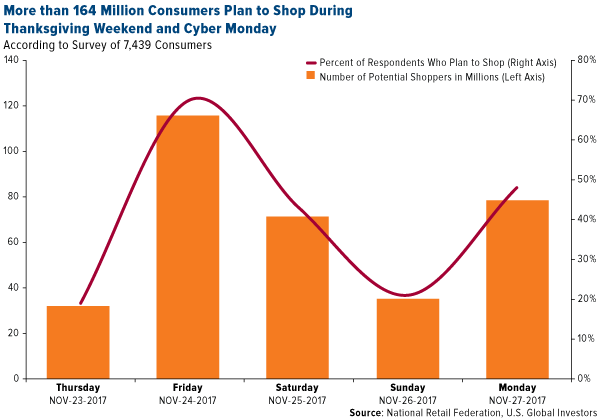

Looked at another way, more than 164 million consumers, or nearly 70 percent of all Americans, plan to shop during the Thanksgiving weekend and Cyber Monday, according to a survey conducted by the National Retail Federation (NRF). Today - Black Friday - might see the largest volume of potential shoppers at 115 million, or 70 percent of those polled, followed by 78 million on Cyber Monday.

So how could investors take advantage of these findings? According to a recent report from LPL Financial, since 2009 the S&P Retail Select Industry Index has seen the strongest gains during the months of February and March, after companies report sales for the fourth quarter. Retailers are actually down about 6 percent year-to-date, and LPL Financial adds that “it is likely that the performance of individual company stocks be more dispersed than they have been historically, which may favor active management in the sector moving forward.” I agree with this assessment, as we’ve seen quite a lot of volatility in the space.<

I want to wish everyone a blessed Thanksgiving weekend! I often say that having gratitude improves your altitude in life. It’s important that we take stock not only in our finances but also the people who matter most, from family and friends to coworkers and business associates.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.86 percent. The S&P 500 Stock Index rose 0.91 percent, while the Nasdaq Composite climbed 1.57 percent. The Russell 2000 small capitalization index gained 1.76 percent this week.

- The Hang Seng Composite gained 1.84 percent this week; while Taiwan was up 1.42 percent and the KOSPI rose 0.41 percent.

- The 10-year Treasury bond yield fell 0.3 basis points to 2.34 percent.

Domestic Equity Market

Strengths

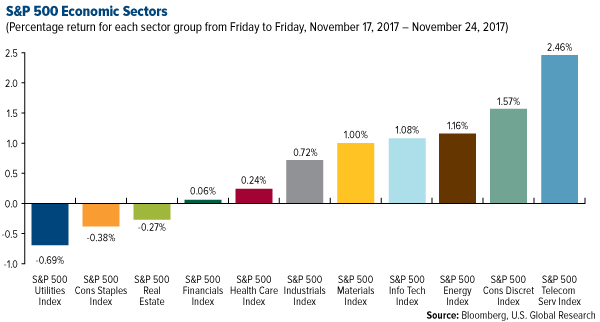

- Telecommunications was the best performing sector of the week, increasing by 2.46 percent versus an overall increase of 93 basis points for the S&P 500.

- Foot Locker was the best performing stock for the week, increasing 25.90 percent.

- Salesforce's third-quarter revenues were up 25 percent from last year. The company also reaffirmed its revenue growth plan and a timeline which includes more than doubling its annual revenues from $8.4 billion in 2017 to $20 billion by 2022.

Weaknesses

- Utilities was the worst performing sector for the week, falling 69 basis points versus an overall increase of 93 basis points for the S&P 500.

- Signet Jewelers was the worst performing stock for the week, falling 32.88 percent.

- Shares of Signet Jewelers crashed more than 25 percent after the company reported a big loss and warned on 2018. Same-store sales fell 5 percent, more than the 2.9 percent drop that Wall Street was expecting.

Opportunities

- Barron's says that IBM shares could climb 30 percent over the next year as the company is trading well below the S&P 500 on a price-to-earnings basis.

- Brian Belski of Bank of Montreal Capital Markets sees the S&P 500 finishing 2018 at 2,950, the highest forecast on Wall Street.

- According to some, there are several strategies for investors to potentially take advantage of the Amazon-induced retail apocalypse: Buy Amazon stock, buy stock in companies that support Amazon, and buy companies in "Amazon-proof" sectors.

Threats

- According to Morgan Stanley, three things could destroy the third-longest market rally of all time: extreme leverage, exuberant sentiment and excessive policy tightening.

- According to Societe Generale, the market is nearing a crucial turning point that could crush stocks. The firm said a 10-year Treasury yield above 2.5 percent could result in a U.S. equity sell off.

- Starbucks is using a financial engineering gimmick to boost its stock price. The coffee giant plans to sell $1 billion of debt and then use the proceeds to buy back its own stock, expand its business, pay cash dividends or finance acquisitions, according to a regulatory filing.

The Economy and Bond Market

Strengths

- The Leading Index rose by 1.2 percent in October, twice as much as the 0.6 percent increase expected by economists polled by Reuters. The index "suggests that solid growth in the U.S. economy will continue through the holiday season and into the new year," Conference Board research director Ataman Ozyildirim said in a statement.

- U.S. home sales increased more than expected in October as hurricane-related disruptions dissipated. The National Association of Realtors said on Tuesday that existing home sales rose 2.0 percent to a seasonally-adjusted annual rate of 5.48 million units last month.

- The University of Michigan Index for November came in at 98.5, higher than the anticipated reading of 98.0.

Weaknesses

- New orders for key U.S.-made capital goods unexpectedly fell in October after three straight months of hefty gains. Durable goods orders fell 1.2 percent last month as demand for transportation equipment tumbled 4.3 percent.

- Federal Reserve Chair Janet Yellen raised new concerns about whether or not persistently low inflation is "transitory" in a speech on Tuesday night.

- A new analysis shows the Senate GOP tax bill fails a key test that would prevent it from passing. The University of Pennsylvania's Wharton School Budget Model shows that the bill would decrease revenues and increase the federal debt outside a 10-year window, violating the "Byrd rule" that would allow Republicans to pass the bill with 50 votes in the Senate and avoid a Democratic filibuster.

Opportunities

- The U.S. economy is heading into 2018 with strong momentum that’s likely to boost wages and inflation, Goldman Sachs Group economists said in a research note. The firm raised its growth outlook for 2018 to 2.5 percent and lowered its forecast for unemployment to 3.7 percent by the end of 2018.

- Next Wednesday the second reading on U.S. GDP for the third quarter will come out. Economists are expecting a robust pace of 3.2 percent on an annualized basis.

- U.S. construction spending for October will come out next Friday and is expected to grow 0.5 percent, up from September’s 0.3 percent.

Threats

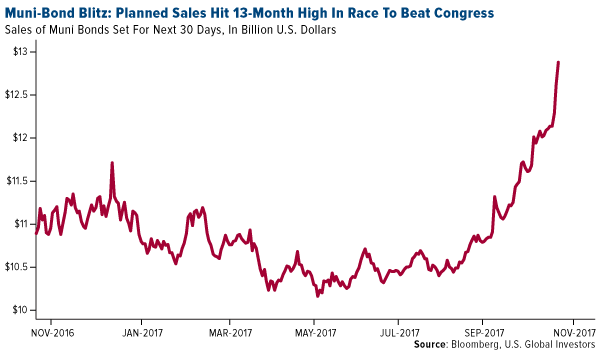

- State and local governments are rushing to borrow before Congress enacts legislation that would pull subsidies from a major swath of the municipal-bond market by curbing refinancings and preventing businesses from issuing tax-exempt debt. The amount of sales scheduled over the next month has swelled to $19.5 billion, the most since October 2016, according to Bloomberg. That’s likely to weigh on prices for the remainder of the year as investors brace for a wave of new supply to hit the market.

- The longer the trend of a flattening yield curve continues, the more likely its effects could spread to bank earnings and the real economy. In the past, the yield curve has proven a reliable indicator of impending economic slumps when it inverts, with short rates exceeding longer-term yields. BMO Capital Markets strategists Ian Lyngen and Aaron Kohli wrote in a note Tuesday that the risk of an inverted curve next year is becoming "a real possibility," as the flattening trend persists.

- U.S. credit card delinquencies are rising, which could be a red flag for consumer spending going forward.

This week spot gold closed at $1,288.59 down $5.61 per ounce, or 0.43 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.60 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index sold off 0.76 percent. The U.S. Trade-Weighted Dollar continues its three-week slide, falling 0.94 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-22 | Initial Jobless Claims | 240k | 239k | 252k |

| Nov-22 | Durable Goods Orders | 0.3% | -1.2% | 2.2% |

| Nov-27 | Hong Kong Exports YoY | -- | -- | 9.4% |

| Nov-27 | New Homes Sales | 625k | -- | 667k |

| Nov-28 | Conf. Board Consumer Confidence | 123.8 | -- | 125.9 |

| Nov-29 | Germany CPI Core YoY | 1.7% | -- | 1.6% |

| Nov-29 | GDP Annualized QoQ | 3.2% | -- | 3.0% |

| Nov-30 | Eurozone CPI Core YoY | 1.0% | -- | 0.9% |

| Nov-30 | Initial Jobless Claims | 240k | -- | 239k |

| Nov-30 | Caixin China PMI Mfg | 51.0 | -- | 51.0 |

| Dec-1 | ISM Manufacturing | 58.3 | -- | 58.7 |

Strengths

- The best performing precious metal for the week was palladium, up 0.28 percent. Trade data shows Chinese imports of palladium are up 60 percent year-over-year. The world’s leading jeweler, Chow Tai Fook Jewellery Group, saw profits increase for a second consecutive six-month period as demand for gold in China lifts sales. This mirrors China’s recovery in demand for luxury goods after a two-year slump amid a corruption crackdown in the country, reports Bloomberg. In Bloomberg’s weekly survey, gold traders see the rally in gold resuming with the dollar trading at its lowest in more than a month.

- The world’s leaders in gold imports, India and China, saw a welcome increase in gold demand for the month of October after a September slump in demand, writes Lawrie Williams.

- The Russian central bank added another 700,000 ounces of gold to its reserves last month as a part of its plan to reduce the nation’s reserve dependence on the U.S. dollar. Reported by TASS, the BRIC countries are considering forming a single, unified gold trading system.

Weaknesses

- The worst performing precious metal for the week was silver, down 1.52 percent on little news unique to the metal. According to the TD Securities outlook for 2018, precious metal gains are likely to be capped by U.S. monetary policy and the passage of tax reform.

- Western Australia’s Liberal party joins the gold industry in opposition of a proposed increase in gold royalty, saying it would cost jobs and much of its revenues would leak to the eastern states of the country.

- United Steelworkers urged the Canadian government to respond after two workers died in an incident that the union said is linked to protests at a mine project owned by Torex Gold based in Toronto, writes Bloomberg. It was later reported the men who died were not employees of Torex Gold.

Opportunities

- Mike McGlone, BI commodity strategist, writes that strong gold ETF inflows seem poised to gain momentum as investors seek diversification. He adds that gold ETF inflows are outpacing price appreciation for the longest period and at the highest velocity since the global financial crisis.

- UK-based Glint Pay announced the launch of a beta-app and credit card allowing consumers to buy portions of gold and then use the account to make purchases, reports Kitco. This is a major step forward in the re-monetization of the yellow metal.

- A UBS price forecast says gold could rebound above $1,300 per ounce toward the end of this year and into 2018. The Bank of Montreal also projects a gold price average of $1,300 per ounce in 2018. JPMorgan, however, projects precious metals will be stable through 2018, with gold averaging $1,350 per ounce by the fourth quarter.

Threats

- JPMorgan Chase & Co. is bearish on gold in the near term expecting the Federal Reserve to hike five times through December 2018, fueling a climb in real rates, reports Bloomberg. BlackRock Inc. says a tax cut and interest rate hikes would undermine gold.

- Emmerson Mnangagwa was sworn in as interim president of Zimbabwe after Robert Mugabe was removed from power. Many believe this successor and former right-hand man of Mugabe will continue to implement the violent infrastructure the nation has seen for many years while in a time of crisis with 95 percent of the population unemployed.

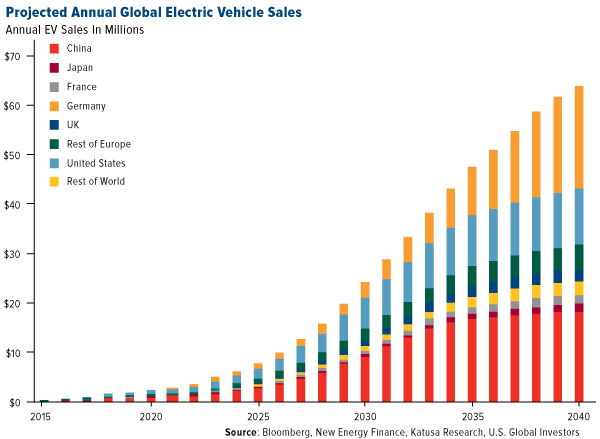

- China moves to make it more difficult for new-energy vehicle manufacturers to access subsidies and plans to phase out financial support entirely by 2020. This comes at a time when electric vehicle sales are booming in the nation with sales rising 45 percent year-over-year to 490,000 units in the first 10 months of 2017.

November 20, 2017Synchronized Global Growth May Have Arrived |

November 16, 2017Solar Energy Boom Could Heat Up the Global Energy Sector |

November 13, 2017My Conviction in Gold Royalty Companies and Bitcoin |

Strengths

- Iron ore was the best performing major commodity this week, rising 8.5 percent. The commodity has rebounded to a two-month high, with investors looking beyond China’s near-term clampdown on steelmakers to envisage a revival in demand next year.

- The best performing sector this week was metals and mining. The group rose 5.4 percent as copper prices rose for a sixth consecutive session, its longest since March. Inventories declines while strike actions in Peruvian and Chilean mines threatened the supply chain.

- Daqo New Energy Corporation, a Chinese manufacturer of parts and cells used in solar power products, was the best performing stock in the broader resource market this week. The stock rallied 23.9 percent to a fresh 52-week high after the company received positive investment recommendations from a number of retail-oriented newsletters.

Weaknesses

- Natural gas prices dropped 7.4 percent, the most among major commodities. West Texas prices have fallen as much as $0.57 per million British thermal units—or about 20 percent—below spot prices at Louisiana’s Henry Hub, the national benchmark. The problem is that natural gas is gushing out of West Texas, a byproduct of frenzied drilling for oil. That is a problem for energy producers, who are running out of places to send all of it. Pipelines running from the region’s Permian Basin are essentially full.

- The worst performing sector this week was the Alerian MLP Index. The index dropped 0.6 percent tracking natural gas price weakness, and somewhat offset by stronger crude prices and rebounding production volumes.

- The worst performing stock for the week was Fibria Celulose SA. The Brazilian producer of pulp and paper dropped 1.9 percent. A positive recommendation from Citi analysts was not enough to offset the weakness cause by a rising Brazilian real, which negatively affects the business margins.

Opportunities

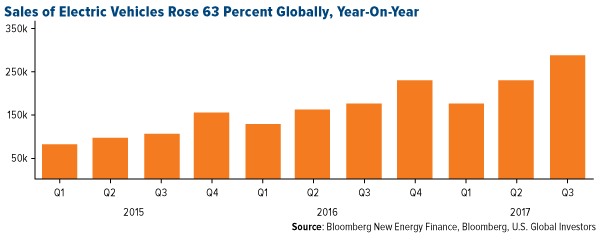

- Global sales of electric vehicles soared 63 percent in the third quarter. A total of 287,000 units were reportedly sold in the three months ended in September, leading Bloomberg New Energy Finance to expect annual total sales to exceed 1 million units for the first time. Strong demand in China was the key driver behind the record breaking numbers as the renewed crackdown on polluting industries propels renewable alternatives from power generation to consumer products.

- Crude oil advanced to a fresh two-year high as the Organization of Petroleum Exporting Countries (OPEC) and Russia were said to have crafted the outline of a deal to extend their oil production cuts to the end of 2018. After days of talks, Moscow and Riyadh now agree on the need to announce an additional period of cuts at the November 30 meeting, although both sides are still hammering out crucial details.

- Investor appetite for gold as a refuge is showing signs of life. Open interest, a tally of outstanding futures contracts, rose by the most since June, reports Bloomberg. In New York, aggregate gold open interest is headed for a third straight quarterly gain, the longest stretch since 2009, while holdings in exchange-traded funds (ETFs) are near the highest in a year.

Threats

- Travelers on this Thanksgiving Day-weekend are facing some of the highest gas prices in five years. More than 50 million people are expected to travel this weekend, according to a spokesman for the American Automobile Association (AAA). What is generally one of the highest gasoline demand periods of the year may be negatively affected by rising fuel prices. The national average price has climbed to $2.56 a gallon, which is 41 cents higher than last year.

- Crude and refined products speculative interest continues to rise to multi-year records, leading contrarian analysts to believe the crude rally may fade. The most recent data shows the total WTI net-long position was the most bullish in more than eight months. Similarly, gasoline and diesel net-long positions were the most bullish on record in data going back to June 2006.

- Rising freight rates and the increasing likelihood of an occurrence of the La Niña weather phenomenon are among the risks that farmers, investors and commodities traders face in 2018. The U.S. National Oceanic and Atmospheric Administration (NOAA) is forecasting a 65-75 percent chance of la Niña developing this year and lasting into the first quarter of 2018.

Strengths

- Hong Kong, Taiwan and Singapore all had a reasonably good week, rising 1.84 percent, 1.43 percent and 1.81 percent, respectively. Vietnam’s Ho Chi Minh Stock Index had an outstanding week, soaring 5.14 percent in part due to a recent government announcement on SOE-equitization and the easing of some regulations.

- Thailand’s third-quarter GDP reading came in at 4.3 percent, ahead of expectations for a 3.9 percent showing and up from the prior quarter’s 3.7 percent (now 3.8 revised). Singapore’s GDP came in at 5.2 percent, ahead of expectations for a 5.0 percent print and up from last quarter’s 4.6 percent number.

- China announced further import tax cuts, which may help cut into trade surplus concerns by boosting consumption.

Weaknesses

- The Shanghai Composite declined 86 basis points for the week, with Thailand’s SET Index not far behind, down 75 basis points for the week.

- Singapore’s industrial production for the October period came in lighter than expected, at 14.6 percent, behind an anticipated 16.0 percent.

- Consumer goods and conglomerates were the only two sectors of the Hang Seng Composite to decline for the week, falling 12 and 11 basis points respectively.

Opportunities

- China’s debt is on track to be more than three times the size of the economy by 2022, according to Bloomberg Economics. Although the data is startling, the Asian nation’s “drive to reduce its debt burden has shifted into a higher gear,” reports Bloomberg, particularly following the Communist Party Congress in October. Seeking to bring the market under control, regulators have set their sights on shadow banking specifically.

- The chart below highlighted by Katusa Research and originally provided by Bloomberg New Energy Finance takes a look at annual global electric vehicle (EV) sales forecast through the year 2014. As you can see, China and the U.S. will push the adoption of EVs forward, with the rest of the world following closely behind. According to the chart below, some believe that by 2040, the global EV market could get to over 60 million vehicles sold that year alone, writes Katusa Research.

- Demand for gold in China is on the rise, propping up semi-annual profit growth for the world’s top jeweler, Chow Tai Fook. The company’s profit increased for a second consecutive six-month period, reports Bloomberg, with net income rising 46 percent in the six months through September. “The results mirror the continued recovery in demand for luxury goods in China after a two-year slump amid a corruption crackdown in the country,” the article reads.

Threats

- On Tuesday, Apple Inc. announced the removal of several apps, including Skype, from its app store in China, reports Reuters. The removal came after the Asian nation’s government pointed to violations of local laws by the company. Beijing has pursued a series of laws and regulations that have raised concerns from foreign companies trying to expand their user base across the country, the article reads.

- In July, Alexandre Bompard took over Carrefour, the world’s second-largest retailer behind Wal-Mart, and according to Reuters, Bompard will unveil his “turnaround plan for the French company (which issued a profit warning in August),” on January 23. The question is now whether or not he made a decision to stay or go in China, where Carrefour has spent years trying to fix a business whose sales still fell 5.4 percent in the third quarter. “Until now, the only Western retailers to have successfully established themselves in this country have done so via partnerships with local retailers,” Bryan Garnier analysts said in a research note. The clock is ticking.

- According to Reuters, politics was in the air as the Victoria’s Secret annual fashion show hit the stage in China for the first time on Monday. Several of the “Angels” and star names who had been expected to attend were nowhere to be found, the article continues. Pop star Katy Perry and model Gigi Hadid have both drawn criticism in China, and were both absent from this week’s event.

Strengths

- Greece was the best performing country this week, gaining 1.6 percent. The Greek government submitted the 2018 draft budget to the parliament, projecting 2.4 percent GDP growth next year, up from 1.8 percent this year. According to the draft budget, unemployment is expected to fall to 19 percent in 2018, private consumption to increase 1.4 percent, and total private and public investment to rise by 12.6 percent.

- The Polish zloty was the best performing currency this week, gaining 1.8 percent against the U.S. dollar. This week a slew of positive economic data came out for Poland supporting the country’s currency. Average gross wages are growing faster than expected, unemployment keeps declining, industrial and construction output is rising and money supply is growing.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

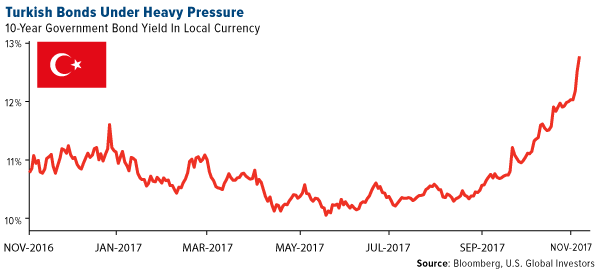

- Turkey was the worst performing country this week, losing 1.6 percent. Migros Ticaret, a supermarket and mall operator, fell 13.8 percent after BC Partners sold a 7.3 percent stake in the company below the market price.

- The Turkish lira was the worst performing currency this week, losing 1.7 percent against the U.S. dollar. The lira reached a new low as political tension continues to increase in Turkey. The central bank of Turkey increased its policy rate by 25 basis points; not enough to support its falling currency.

- The industrial sector was the worst performing sector among eastern European markets this week.

Opportunities

- IHS Markit's composite flash purchasing managers’ index (PMI) for the euro zone jumped to 57.5 this month, its highest since April 2011. Manufacturing PMI climbed to 60.00 from 58.5, the second highest reading since the index was first collected in June 1997. Services PMI also beat expectations, rising from October’s 55.0 to a six-month high of 56.2. A reading above 50 indicates growth.

- Poland’s state-owned gas company, PGNiG, signed a five-year deal to buy liquefied natural gas from the U.S. Nine shipments are scheduled from the Sabine Pass terminal in Louisiana to Poland’s gas port in Swinoujcie on the Baltic coast. This is the first such contract for regular LNG delivery for central and Eastern Europe, as the region is seeking to cut its dependence of gas delivery from Russia.

- Rosneft has agreed to supply its new partner CEFC China Energy with almost 61 million tonnes of oil over the next five years. In 2016, Russia became China’s largest oil supplier. This deal will help Russia to remain China’s top oil supplier. Sanctions imposed on Russia by the U.S. and Western Europe pushed Russia to boost oil ties with China.

Threats

- Turkish bond yields hit record highs and the lira fell to record lows against the U.S. dollar due to rising political tension. Mr. Zarrab, the Turkish-Iranian gold trader accused of doing business with Iran under sanctions, will go on trial next week in New York. His case has put more pressure on an already-strained relationship between the U.S. and Turkey. The lira may depreciate further against the dollar if the central bank doesn’t take drastic measures to support its falling currency.

- Coalition talks between Merker’s Christian Democratic Union (CDU) and its Bavarian sister party Christian Socialist Union (CSU), with pro- business Free Democratic Party (FDP) as well as the Greens, failed suddenly last weekend. Merker supports new elections over forming a minority government, but some fear that the far right nationalist Alternative for Germany party (AfD) could gain more seats in parliament if new elections are called. Germany is the largest economy in Europe and prolonged lack of government may strain some decision making processes.

- JPMorgan, in its EMEA Emerging Markets 2018 Outlook publication, recommends overweighting Russia against an underweight in Turkey. The Russian central bank will likely continue cutting rates, while the Turkish central bank is under pressure due to high inflation. However, JPMorgan also points out that relations between Russia and the U.S. remains a wild-card, and notes that the Treasury reports to Congress are due in January (on the impact of potential restrictions on sovereign debt markets). Additionally, Russia will hold presidential elections in March, which could be a source of noise.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All