Gold Looks Like a Bargain Just in Time for Christmas

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

One of the most compelling and engaging presenters at the Precious Metals Summit in London last month was Ronald-Peter Stöferle, a managing partner at Liechtenstein-based asset management company Incrementum. Incrementum, as you may know, is responsible for publishing the annually-updated, widely-read “In Gold We Trust” report, which I’ve cited a number of times before.

During his presentation, Stöferle shared the fact that his wife prefers to do her Christmas decoration shopping in January. When he asked her why she did this—Christmas should be the last thing on anyone’s mind in January—she explained that everything is half-off. A bargain’s a bargain, after all.

This is very smart. Here we are several days before Christmas, and demand for ornaments, lights and other decorations is red-hot, so be prepared to pay premium prices if you’re doing your shopping now. But mere hours after the Christmas presents have been unwrapped and Uncle Hank has fallen asleep on the couch with a glass of boozy eggnog, stores will begin slashing prices to get rid of inventory.

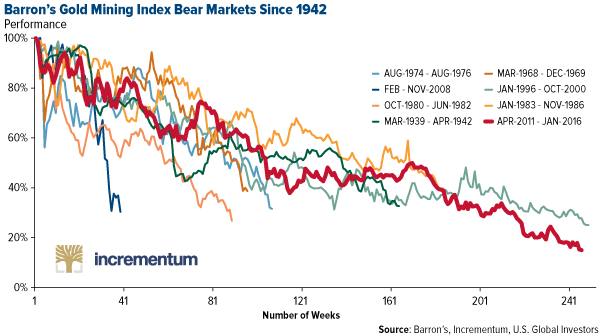

Gold bullion and mining stocks are currently in the “January” phase, so to speak, according to Stöferle. The Barron’s Gold Mining Index, which goes all the way back to 1938, recently underwent its longest bear market ever, between April 2011 and January 2016. And as I already shared with you, the World Gold Council (WGC) reported last month that gold demand fell to an eight-year low in the third quarter.

“Most people get interested in stocks when everyone else is,” Warren Buffett famously said. “The time to get interested is when no one else is.”

The same logic applies to Christmas decorations, gold and mining stocks.

As of my writing this, gold is trading around $1,280, up 11 percent in 2017. That’s off 5 percent from its 52-week high of $1,351 set in September. If it stays at its present level until the end of the year, the metal will end up logging its best year since 2010, when it returned 30 percent.

|

Gold traded up on Friday as the U.S. dollar weakened following news that former National Security Advisor Mike Flynn pleaded guilty to lying to the FBI about conversations he had with Russian officials last December during the presidential transition. It’s possible that the details Flynn might provide as part of a plea bargain could help special prosecutor Robert Mueller advance his investigation into Russia’s meddling in the 2016 election.

For whatever it’s worth, ABC News is reporting that Flynn is expected to testify against President Donald Trump for “directing” him to make contact with the Russians.

But back to gold. Considering it’s faced a number of strong headwinds this year—a phenomenal equities bull run that’s drawn investors’ attention away from “safe haven” assets, lukewarm inflation and anticipation of additional rate hikes, among others—I would describe its performance in 2017 as highly respectable.

And yet if you listen to the mainstream financial news media, gold is “boring” and “flat.” Speaking to CNBC this week, Vertical Research partner Michael Dudas called the gold market “eerily quiet.”

|

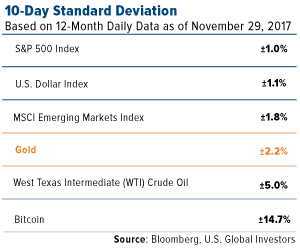

Dudas was specifically describing gold’s volatility, but even here the facts tell a slightly different story. In the table to the right, you can see the 10-day standard deviation for a variety of assets, using data from the past 12 months. Gold traded with higher volatility than domestic equities, the U.S. dollar and global emerging markets. Of those measured, only oil and bitcoin showed higher volatility.

Based on volatility alone, it’s stocks that look pretty “boring” and “quiet” this year, but you’re not likely to hear a pundit or analyst describe them that way.

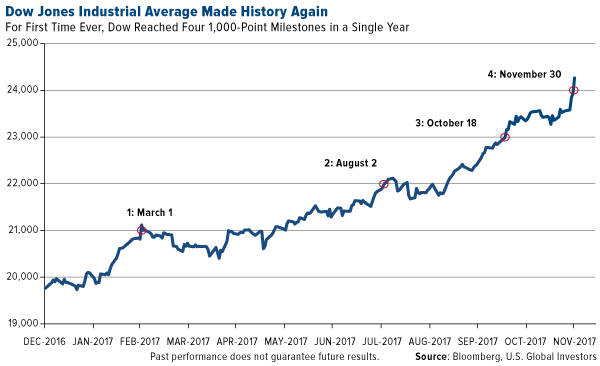

And with good reason. The S&P 500 hasn’t fallen more than 3 percent from a previous high for more than 388 days now, the longest stretch ever for the index. And for the first time in its 120-year history, the Dow Jones Industrial Average has reached four 1,000-point milestones in a single year—with a whole month left to go. It’s possible that excitement over the Senate’s tax bill will be enough to push the Dow above 25,000 sometime before the ball drops in Times Square. The drama involving Flynn, however, threatens to derail those chances.

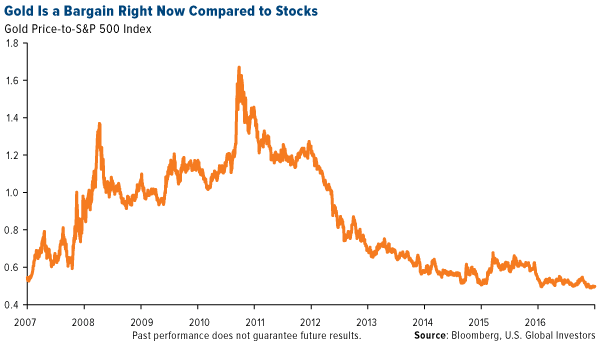

What this means is that, compared to domestic equities, gold is highly undervalued right now. The gold-to-S&P 500 ratio, a time-tested trading indicator, is near 50-year lows. I see this as a strong buy signal, especially now as we await the Federal Reserve’s decision to lift rates this month. If you recall, gold broke out strongly following the December rate hikes in 2015 and 2016.

In his December outlook on precious metals, Bloomberg Intelligence commodity strategist Mike McGlone writes that “gold is ripe to escape its cage soon,” adding that “prices just don’t get as compressed as they did for gold in November, indicating a breakout soon.”

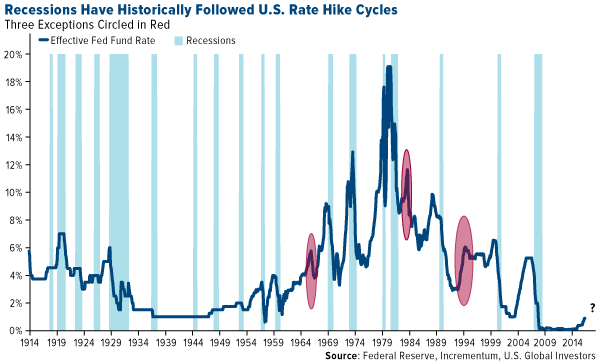

So what are the catalysts that could trigger a breakout? Stöferle mentions two: a possible recession and stronger inflation.

“I think the odds are pretty high that a recession might be upon us sooner or later because we’re in this rate hike cycle, and as always the central banks are way behind the curve,” he said.

What Stöferle is referring to is the strong historical correlation between new U.S. rate hike cycles and recessions. Going back more than 100 years, 15 of the last 18 recessions were directly preceded by monetary tightening.

click to enlarge

click to enlargeThe Federal Reserve isn’t just raising rates, remember. It’s also begun to unwind its $4.5 trillion balance sheet, which was built in the years following the financial crisis. This carries historical risk. The central bank has embarked on similar reductions six times in the past—in 1921-1922, 1928-1930, 1937, 1941, 1948-1950 and 2000—and all but one episode ended in recession.

“Quantitative tightening will fail,” Stöferle predicted.

Obviously, there’s no guarantee that this particular round will have the same outcome as past cycles, but if you agree with Stöferle, it might be prudent to have as much as 10 percent of your wealth in gold bullion and gold stocks.

Inflation is a trickier thing to forecast. A lot of people, myself included, had expected the cost of living to show signs of life this year in response to some of President Trump’s more protectionist and policies. But nearly 10 months into his term, no major legislation has been passed or signed.

That might be about to change with the highly anticipated tax reform bill, which reportedly has enough votes in the Senate. If the bill reaches Trump’s desk, it will be the first time in a generation that the U.S. has amended its tax code.

But will the $1.5 trillion bill, as it’s currently written, lead to stronger economic growth and pay for itself, as its most vehement supports insist? My hope is that it will. As I’ve been saying for a while now, it’s time we begin relying more on fiscal policies to drive growth, especially now that the Fed is beginning to tighten policy.

In the spirit of staying balanced, though, there are troubling signs and forecasts that the bill could actually end up being a disappointment. After reviewing the bill, the Joint Committee on Taxation (JCT) estimates that its enactment could lead to a whopping $1.4 trillion increase in the deficit between now and 2027. Even if we factor in economic growth that might come as a result of reforms, the JCT says, we’d still be looking at a $1 trillion shortfall.

Many economists are also skeptical. A recent University of Chicago Booth School of Business survey of economists from Yale, MIT, Princeton, Harvard and other Ivy League schools found that over half did not believe the current tax bill will “substantially” grow GDP. Only 2 percent thought it would, and more than a third were uncertain. Additionally, nearly 90 percent believed that if the bill is enacted, the U.S. debt-to-GDP ratio will be “substantially” higher a decade from now.

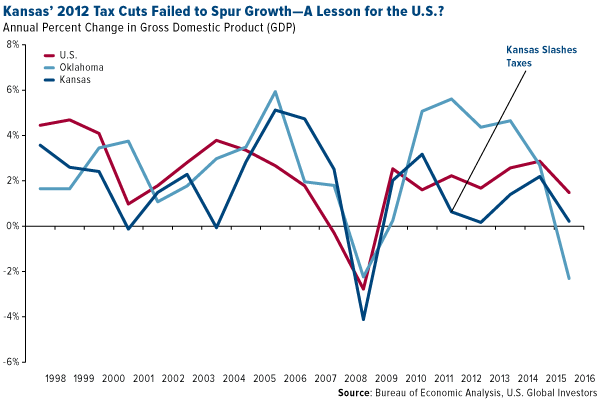

And then there’s the Kansas experiment from five years ago. In May 2012, Governor Sam Brownback signed a sweeping state tax reform bill that in many ways resembles the Senate’s current tax bill. It slashed personal and business income taxes, consolidated the state’s three tax brackets into two and eliminated a number of credits and exemptions. Hopes were high that the reforms would kickstart economic expansion, help taxpayers and attract new business to the state.

Instead, none of that happened. Following the bill’s enactment, Kansas GDP growth remained stagnant, trailing the national growth rate as well as that of neighboring states and even its own rate from years past. This year, the nonprofit financial watchdog group Truth in Accounting gave Kansas a failing financial grade of D, citing its inability to pay its debts or balance its budget.

click to enlarge

click to enlargeIn June of this year, Kansas’ Republican-controlled state legislature voted to raise taxes for the first time since reforms were enacted and eventually had to override Governor Brownback’s veto. Many of those state legislators who initially supported the Kansas tax cuts are now warning federal lawmakers that similar outcomes could occur on a nationwide scale.

I’m not sharing this to discredit tax reform—in fact, I’m strongly in favor of it. However, I believe it’s important to highlight the fact that nothing in life is guaranteed. Hope for the best, prepare for the worst. What steps can you take now in the event the tax reform bill doesn’t accomplish what it’s designed to do—or worse? This type of uncertainly has historically made gold shine the brightest.

At conferences I’ve attended and spoken at recently—the Silver & Gold Summit in San Francisco and Mines and Money in London among them—the suggestion has been made by a few big-name investors and money managers that bitcoin’s meteoric rise is to blame for the market’s apparent disregard for gold and gold stocks right now. With bitcoin up more than 980 percent since the beginning of the year, even after a 21 percent dip on Wednesday, many market-watchers might simply be too star-struck by the newness of bitcoin to be bothered by the “barbarous relic.”

I happen to think this is a mistake. As much as I believe in the value of bitcoin, gold and gold stocks still play a crucial role in the modern portfolio.

As I told Kitco News’ Daniela Cambone at the Silver & Gold Summit, bitcoin isn’t responsible for dismantling gold. Although both assets are currencies, I don’t see them at odds because they serve very different functions. For one, gold is more than money—it’s worn as jewelry, widely used in dentistry and can be found in art and even some high-end foods. It’s been traded around the world for millennia and, unlike bitcoin, does not require electricity. Indeed, it conducts electricity, which is why you can find it in your iPhone and GoPro camera’s circuitry.

|

Bitcoin is more than money as well. It’s the most influential spokesperson, if you will, of blockchain technology, upon which the currency is built. Speaking with SmallCapPower’s Angela Harmantas at the Mines and Money conference in London, I made the comparison that bitcoin is to email as blockchain is to the internet. In the earliest days of the internet, few people truly understood what it was or could predict the implications of this new technology—but email they understood. It’s what woke people up to the idea of using the internet. Bitcoin is doing just that for blockchain.

But blockchain’s utility goes far beyond finance. As a decentralized, highly encrypted ledger, it has untold potential to change the way we run our lives, businesses and governments. Among other tasks, the technology can help manage digital rights to intellectual property, bring transparency to supply chains and reliably track the spending of public funds. It can even be used as a tamper-proof voting system, whether you’re voting for a new chairman of the board or president of the United States. One day soon, we might all be e-voting from our smartphones and tablets, reassured that our vote cannot be compromised.

For more on my outlook on bitcoin and blockchain, and to get my thoughts on why I think HIVE Blockchain Technology is well-positioned to be an industry leader, watch my full interview with Angela Harmantas.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 2.86 percent. The S&P 500 Stock Index rose 1.53 percent, while the Nasdaq Composite fell 0.60 percent. The Russell 2000 small capitalization index gained 1.17 percent this week.

- The Hang Seng Composite lost 2.56 percent this week; while Taiwan was down 2.34 percent and the KOSPI fell 2.71 percent.

- The 10-year Treasury bond yield rose 2.1 basis points to 2.364 percent.

Domestic Equity Market

Strengths

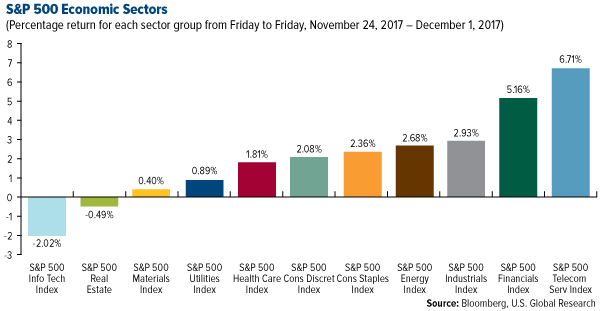

- Telecom was the best performing sector of the week, increasing by 6.71 percent versus an overall increase of 1.53 percent for the S&P 500.

- L Brands was the best performing stock for the week, increasing 15.49 percent.

- The Dow Jones industrial average soared 331.67 points on Thursday, topping the 24,000 level for the first time.

Weaknesses

- Information technology was the worst performing sector for the week, falling 2.02 percent versus an overall increase of 1.53 percent for the S&P 500.

- Autodesk was the worst performing stock for the week, falling 17.33 percent.

- Sears continued its streak of declining sales in the third quarter, reporting a double-digit drop in comparable sales at its Sears and Kmart chains. Sales at Sears stores open for more than a year fell 17 percent, while comparable sales at Kmart fell 13 percent.

Opportunities

- CVS and Aetna are reportedly nearing a $66 billion deal. According to reports from The Wall Street Journal, CVS is closing in on a deal that would pay $200 to $205 per Aetna share.

- Microsoft is launching a mobile version of its browser, Edge, on both Android and iOS. The release is part of a larger effort to make Microsoft software and services available on all platforms.

- Apple and Stanford University have partnered to launch a new Apple Watch app, Apple Heart Study. The app aims to collect data on abnormal heart rhythms and is part of a larger heart research study between the two.

Threats

- Qualcomm is asking U.S. courts to ban iPhone X models that don't use its chips. It’s seeking a ban of Apple's smartphones that use modems from its main competitor, Intel, which would result in AT&T and T-Mobile not being able to sell the phone in the U.S. anymore. Additionally, Apple is countersuing Qualcomm, claiming that a number of its Snapdragon chips infringe some of Apple's patents.

- Chipotle founder and CEO Steve Ells said on Wednesday he would step down and the company would look for a new CEO. This is the second time in less than a year that Chipotle has announced a CEO change.

- "It has seldom been the case that equities, bonds and credit have been similarly expensive at the same time, only in the Roaring 20s and the Golden 50s," wrote a group of Goldman strategists led by Christian Mueller-Glissmann in a client note. "While in the near term, growth might stay strong and valuations could pick up further, they should become a speed limit for returns."

November 27, 2017Bitcoin & Gold: What Competition? |

November 27, 2017Frank Holmes Discusses Digital Currency Demand |

November 14, 2017World Economy Continuing on Bull Run |

Strengths

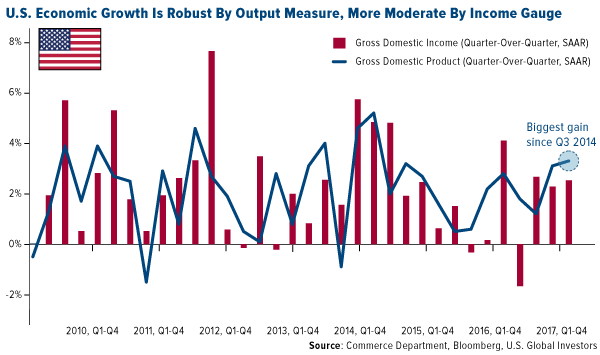

- U.S. GDP climbed at a 3.3 percent annualized rate in the third quarter, the fastest in three years, according to Commerce Department data on Wednesday. Gross domestic income (GDI), another measure of the economy that combines all forms of earnings, was less robust, though still solid. It rose at a 2.5 percent following a downward revision to the second quarter on softer wage gains. While GDI and GDP often diverge over the short term, they tend to track each other over longer periods.

- The Conference Board's measure of consumer confidence rose to 129.5, the highest mark since November 2000. Economists anticipated a decline to 124, after October marked 126.2. "Consumer confidence increased for a fifth consecutive month and remains at a 17-year high," Lynn Franco, Director of Economic Indicators at The Conference Board, said in a statement.

- U.S. construction spending increased 1.4 percent in October, the best gain in five months, with all major categories of building posting gains. The October spending increase was the third monthly gain after advances of 0.3 percent in September and 0.5 percent in August, the Commerce Department said Friday.

Weaknesses

- U.S. government bond prices slipped through the week amid fresh economic data, a poorly received bond auction and concerns about progress on the budget.

- The ISM Manufacturing index for November came in at 58.2, slightly lower than expectations of 58.3 and last month’s 58.7.

- Personal spending in October slowed down to 0.3 percent from the prior month’s 1 percent growth.

Opportunities

- The U.S. employment report is due next Friday. The September and October data was distorted by the hurricanes. As such, next week's November report could give a better read on the labor market. Firm employment growth and accelerating wage gains should cement the case for the Fed to hike rates again in mid-December.

- The only other notable U.S. economic release will be the nonmanufacturing ISM survey on Tuesday. Given the strength in manufacturing reports this week, a confirmation from the service side of the economy would be reassuring.

- Aside from economic data, investors will need to keep a close eye on U.S. fiscal developments regarding the ongoing effort by the GOP-led Congress to agree and pass tax reform.

Threats

- Martin Sullivan, the chief economist at the nonprofit research firm Tax Analysts, says he is normally reserved about policy. Formerly a staff economist at both the US Treasury and the nonpartisan Joint Committee on Taxation, he has a reputation for his research on taxes. Kevin Hassett, now the head of President Donald Trump's Council of Economic Advisers, said in 2013 that Sullivan "goes wherever the facts and the economics lead him." "I'm usually pretty calm about policy — I tend to try and avoid using words like 'crazy' or 'stupid' because I'm a pretty even-keeled guy, but those words apply here," Sullivan told Business Insider on Wednesday. He said the rushed process Republicans are using to try to pass the bill is wasteful and could hurt the legislation in the long run. He also said the bill is unlikely to produce substantial economic gains.

- As the Federal Reserve and the European Central Bank stop their own bond buying, the credit market will be more vulnerable, Societe Generale strategists forecast.

- The federal government will run out of funding on December 8. Unless legislation is passed to extend the funding, non-essential government agencies will have to shut down.

This week spot gold closed at $1,280.30, down $8.50 per ounce, or -0.66 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.92 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index came in off -0.63 percent. The U.S. Trade-Weighted Dollar gave up most of its intraweek gains and closed up just 0.13 percent

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-27 | Hong Kong Exports YoY | 10.1% | 6.7% | 9.4% |

| Nov-27 | New Home Sales | 628k | 685k | 645k |

| Nov-28 | Conf. Board of Consumer Confidence | 124.0 | 129.5 | 126.2 |

| Nov-29 | Germany CPI YoY | 1.7% | 1.8% | 1.6% |

| Nov-29 | GDP Annualized QoQ | 3.2% | 3.3% | 3.0% |

| Nov-30 | Eurozone CPI Core YoY | 1.0% | 0.9% | 0.9% |

| Nov-30 | Initial Jobless Claims | 240k | 238k | 240k |

| Nov-30 | Caixin China PMI Mfg | 50.9 | 50.8 | 51.0 |

| Dec-1 | ISM Manufacturing | 58.3 | 58.2 | 58.7 |

| Dec-4 | Durable Goods Order | -1.0% | -- | -1.2% |

| Dec-6 | ADP Employment Change | 188k | -- | 235k |

| Dec-7 | Initial Jobless Claims | 240k | -- | 238k |

| Dec-8 | Change in Nonfarm Payrolls | 200k | -- | 261k |

Strengths

- The best performing precious metal for the week was palladium, up 2.43 percent on hedge funds, boosting their net bullish position this past week. Gold surged on Friday as the dollar and equities dropped after former national security advisor Michael Flynn prepared to testify that President Donald Trump directed him to contact Russia, reports Bloomberg. In Bloomberg’s weekly poll, almost half of respondents were neutral on gold’s outlook as of Thursday afternoon.

- The World Gold Council announced a resurgence of gold demand in China driven by millennials and online sales. China was also the biggest contributor to global gold demand during the past quarter, according to China Daily. The yellow metal is also becoming popular in Germany as gold trading stores are now in every major city. There are over 100 in the nation, up from just a handful ten years ago. The BCA Research continues its recommendation to keep gold exposure limited to 5 percent in portfolios.

- Early in the week, gold futures briefly climbed above $1,300 an ounce for the first time in six weeks, writes Susanne Barton of Bloomberg. The weakness of the dollar has been a positive driver of gold.

Weaknesses

- The worst performing precious metal for the week was silver, down 3.71 percent. Silver is now trading the cheapest relative to gold since April 2016. This month, gold traded in its tightest monthly range and narrowest volatility in 12 years despite recent pullback in the yellow metal, which could lead to trading elsewhere with a lack of volatility and into the highly volatile digital currency space. CME Group Inc. and CBOE Global Markets Inc. are poised to offer bitcoin futures contracts, which would make it easier for investors to bet on digital currencies. This could potentially take away interest from gold.

- U.S. GDP rose to a three-year high and the Federal Reserve Chair Janet Yellen described a brightening picture for the economy. Uncertainty arises around investing in gold amid speculation that economic growth will lead to the Federal Reserve raising interest rates has kept generalist away from gold.

- Trouble continues for Barrick Gold as they were downgraded to sell from buy by Citi this week. As reported on IKN, an investigation into their Argentinian mine waste spillage incident appears to show Argentine officials deliberately prevented the area surrounding the mine from being included in a national consensus in 2010 to protect glaciers. It is unclear whether the issue would lead to the Barrick having to shutter the mine.

Opportunities

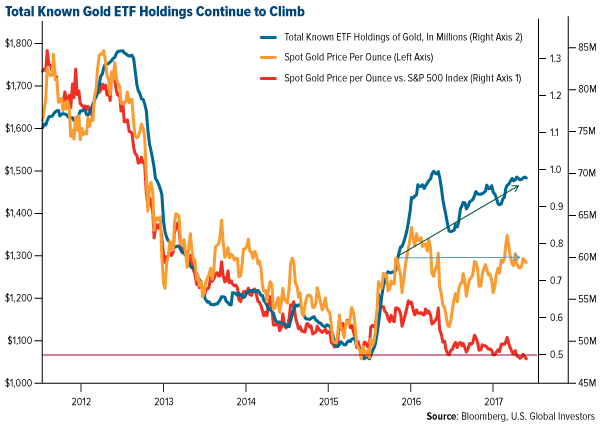

- Gold open interest, a tally of outstanding futures contracts, dropped to its lowest since August as risk assets prevail. This is an interesting contrast to the fact that total gold holdings ETFs have racked up their third straight quarterly rise in assets, its longest stretch since 2009, showing that bulls haven’t given up on gold yet.

- INK Research on gold stock sentiment closed this week at a two-year high of 361 percent despite the growing popularity of bitcoin and digital currencies. The research shows insiders of gold mining companies are buying the gold stock dip, betting that gold can compete with cryptocurrencies as a form of insurance against unforeseen, negative market-moving events. Insiders buying stock in their own company generally is seen as a good sign to investors to also buy the stock.

- Total known gold-ETF holdings continue to rise up to 17 percent this year. Ironically, the pace of accumulation is exceeding the rise in the gold price which is up 11 percent. In addition, the ratio of the S&P 500 relative to gold shows that gold is trading at a ratio of 0.50 on this price to value ratio. According to Bloomberg the implication is that stocks, with record valuation levels, are expensive relative to gold and that already investors seem to be quietly moving money out of stocks and into gold, hedging a market correction.

Threats

- Goldman Sachs warns of an eventual bear market as the current prolonged bull market has left a measure of average valuation at the highest since 1900, reports Christopher Anstey of Bloomberg. Goldman Sachs International strategists wrote “all good things must come to an end” and that the average valuation across equity, bonds and credit in the U.S. is currently at an all-time high of 90 percent.

- Bitcoin faced major hurdles this week as hedge-fund platforms Brooklands Fund Management, Mirabella Advisers and Privium Fund Management all said they turned down requests to take on bitcoin based investors as a client, citing concerns over its place as a legitimate asset. Additionally bitcoin prices plummeted nearly 20 percent in less than 90 minutes after being interrupted by a market outage on Thursday before recovering about half the slippage from the FOMO crowd (“Fear Of Missing Out”).

- The latest update from the New York trial of a Turkish banker accused of laundering Iranian oil money is that a Turkish-Iranian testified that he paid tens of millions of dollars in bribes to the head of a Turkish bank to evade the U.S. sanctions against Iran. Turkish Prime Minister Binali Yildirim responded saying he hopes that the gold trader will “turn back from his mistake” in cooperating with U.S. prosecutors, furthering Binali’s stance that the trial is politically motivated, according to Reuters.

Energy and Natural Resources Market

Strengths

- Natural gas was the best performing major commodity this week rising 8.85 percent. The commodity has rebounded strongly after two consecutive weekly drops as cold weather nears. Futures prices for the commodity rallied this week as forecasts for frigid weather are likely to drive up demand for the heating fuel.

- The best performing sector this week was oil and gas equipment and services. The group rose 4.22 percent, tracking a rally in crude late in the week after the Organization of Petroleum Exporting Countries (OPEC) announced the extension of the 2016 production cuts that have helped rebalance the global oil market. The equipment and services subsector is seen as one of the most levered operationally to benefit from rising oil prices.

- Nippon Steel & Sumitomo Mining, a Japanese integrated steel maker, was the best performing stock in the broader resource market this week. The stock rallied 10.32 percent after SMBC Nikko Securities analysts raised their outlook for the steel market in 2018, and Daiwa Securities analysts raised their price target for the company’s shares.

Weaknesses

- Copper prices dropped 3.11 percent, the most among major commodities. The metal posted a sizeable drop despite a large drawdown in inventories and continued growth in China’s manufacturing sector. Commerzbank analysts said that comments by copper miner Antofagasta expecting lower Chinese demand growth indicate that sentiment in the private sector is not as good as the state sectors.

- The worst performing sector this week was the FTSE 350 Mining Index. The index of diversified major metals producers dropped 5.26 percent, tracking copper price weakness. In addition, analysts at Goldman Sachs showed concerns over the new record volumes of iron ore port inventories in China, and warned the commodity may drop again to $50 a tonne.

- The worst performing stock for the week was Lundin Mining. The Canadian base metals producer dropped 24.24 percent. The company announced production at its flagship Candelaria operation in Chile will be 20 percent lower than expected as the operators contend with a recent rock slide that resulted in pit wall instability issues.

Opportunities

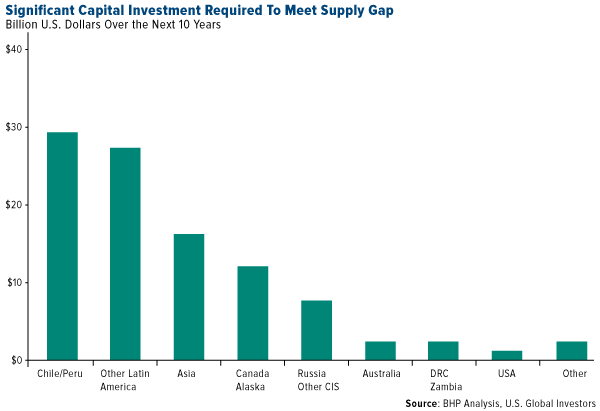

- Buy Copper! That’s the call to action from Global Mining Research (GMR) analysts. The thesis is a result of speaking to various BHP personnel who made it was clear that copper is firmly commodity number one for the diversified metals producer. The positive view is not only as a result of the incoming China ban on scrap imports, but also because the fundamental level of investment needed to meet demand is just not being met. Both GMR and BHP currently forecast a sizeable cumulative market deficit by 2020. In addition, the longer-term picture is also quite positive as it depends heavily on new projects coming on-line as expected, and as BHP illustrated in their recent presentation (chart below), that growth will require a lot of capital.

- China’s manufacturing purchasing manager’s index (PMI) picked up in November, as robust global demand for Chinese exports rose more strongly than expected. The manufacturing index rose to 51.8 in November from 51.6 in October, beating analyst median expectations of 51.5. Orders for exports showed improvement in November, according to subindexes that bode well for China’s trade figures, and similarly provide a strong tailwind for commodity demand, and stronger prices.

- The energy sector is ready for a new wave of mergers and acquisitions which may propel equity prices higher, according to Goldman Sachs’ analysts. The drivers of this new wave will be technological advancements in shale, and the financial underperforming of equity prices relative to the commodity performance. These two current conditions should be very appealing to potential consolidators, conclude the analysts.

Threats

- Jay Powell, President Donald Trump’s nominee to take over the chairmanship of the Federal Reserve, is expected to set the stage for further increases in interest rates. Mr. Powell has vowed to support the economy’s progress toward full recovery, leading experts to conclude that interest rates will rise further and the size of the balance sheet to continue to decrease. Powell’s policy is expected to shoulder the U.S. dollar, a move that may lead to stronger “greenback” levels, and weaker commodity prices.

- The Norwegian Sovereign Wealth Fund, the world’s largest of its kind, has proposed a multi-billion dollar divestment from the oil and gas sector. The approximately $1 trillion fund proposed earlier in November to remove the oil and gas sector from its index, a move that would result in the portfolio being required to sell its current holdings in that space. Considering the size of the fund, a potential divestment, no matter how organized, may lead to an oversupply of energy sector equities, and price weakness. For the time being, the fund is not actively divesting its position, as it requires approval for Norwegian authorities before proceeding.

- Crude prices declined after OPEC members agreed to extend the 2016 cuts and limit oil output through the end of 2018. While the 12-month extension was a positive surprise, longer than the six to nine months expected, OPEC members expect the pact to be enacted only when they receive support from non-OPEC members led by Russia. The Russia “veto” power was not expected, and it appears the market is questioning whether OPEC can incentivize Russia to join the cuts.

Strengths

- Thailand’s SET Index returned 24 basis points for the week, with Singapore’s Straits Times Total Return Index not far behind at 21 basis points. Vietnam’s Ho Chi Minh Stock Index rose 2.66 percent.

- China put up stronger-than-expected official purchasing manager’s index (PMI) numbers. Manufacturing PMI posted a 51.8, beating expectations for 51.4 and coming in higher than October’s 51.6 reading. Non-Manufacturing PMI came in at 54.8, up from the prior month’s 54.3.

- Macau’s casino revenue for the month of November beat analysts’ expectations, as gross gaming receipts came in at a growth rate of more than 22 percent, ahead of estimates for a 19 percent showing.

Weaknesses

- It was not the best of weeks for the region. The Korean Composite Stock Price Indexes (KOSPI) declined 2.71 percent, while the Philippines’ PCOMP, Hong Kong’s Hang Seng Index and Taiwan’s Capitalization Weighted Stock Index (TCWSI) also declined more than 2 percent apiece, falling 2.64, 2.56 and 2.34 percent respectively.

- The Caixin China Manufacturing PMI came in ever-so-slightly below expectations with a 50.8 print, just shy of an anticipated 50.9 and down from last month’s 51.0.

- Information technology declined heavily in the Hang Seng Composite this week, falling 6.97 percent over the last five trading days, far worse than the second-worst-performing sector, Industrials, which declined only 2.96 percent.

Opportunities

- Geely Automobile Holdings launched its first Lynk & Co model 01 this week. The brand will compete with Great Wall’s WEY brand in the Chinese domestic market. Reuters also reported this week that Geely is considering the possibility of Lynk & Co production facilities in South Carolina and/or Belgium.

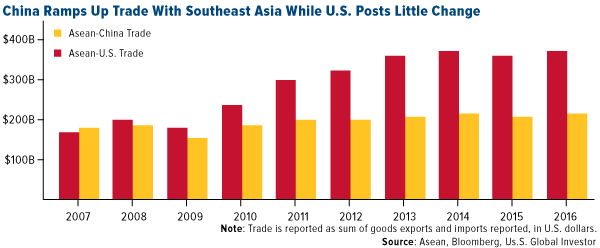

- China continues to expand its clout in Southeast Asia, a recent Bloomberg News story reports. Xi’s hallmark “Belt and Road” initiative and China’s push for trade agreements in the region have continued to boost soft power. Infrastructural buildouts remain central: a China-to-Myanmar crude pipeline is now operational, for example, and construction of a China-to-Laos railway is in the works. China has also widened its lead over the U.S. in trade with Southeast Asia over the last several years. About a decade ago, the tally was almost equal, the authors of the article point out.

- Even as regulators in the United States approved bitcoin futures, South Korea’s heavyweight Shinhan Bank announced it is in the process of creating and testing a bitcoin vault and wallet service for its customers, with service likely expected by mid-2018, according to media reports.

Threats

- North Korea once again launched an intercontinental ballistic missile into the Sea of Japan, continuing its present trajectory to nuclear power and defying international calls to cease its weapons development program. President Trump spoke with Chinese President Xi Jinping on the topic. Trump subsequently tweeted: “Additional major sanctions will be imposed” upon North Korea, following its “provocative actions.” Kim Jong Un declared the nuclear cause now complete, claiming the ability to strike anywhere in mainland United States.

- Hong Kong-listed tech juggernaut Tencent Holdings had its largest weekly loss since the 2015 selloff. The stock’s weighting in Hong Kong’s blue chip Hang Seng Index was slashed from 11.7 to 10 percent, while some investors also fretted over recent notes of caution from Chinese officials on valuations in Hong Kong and amid broader questions about possible rotations heading into the end of the year.

- Bloomberg reports that the Monetary Authority of Singapore (MAS) suggested this week that among banks in Asia’s biggest economies, “those in Hong Kong, South Korea and Singapore stand to lose the most in the face of competition from financial technology companies.”

Strengths

- Greece was the best performing country this week, gaining 3.5 percent. Banks rebounded, gaining 18 percent. Alpha Bank and Piraeus Banks reported third quarter results in line with consensus. Additionally, the Greek notary strike ended and banks started selling the foreclosed properties through e-auctions. Greek banks aim to auction around 700 to 800 properties per month.

- The Turkish lira was the best performing currency this week, gaining 1.1 percent against the dollar. Last week, the lira reached a new record low against the dollar due to growing political tension. It rebounded during the past five days. Some investors are betting that Turkey will have to raise rates soon.

- The industrial sector was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 3.8 percent. MOL Hungarian Oil & Gas Company declined 6.5 percent after the Organization of the Petroleum Exporting Countries (OPEC) announced oil production cuts will be extended until the end of the next year.

- The Hungarian forint was the worst performing currency this week, losing 90 basis points against the dollar. Dovish central bank policies are pushing the currency lower against the dollar. November Manufacturing purchasing manager’s index (PMI) rose to 58.6 from 58.3, less than the estimated 59.5.

- The material sector was the worst performing sector among eastern European markets this week.

Opportunities

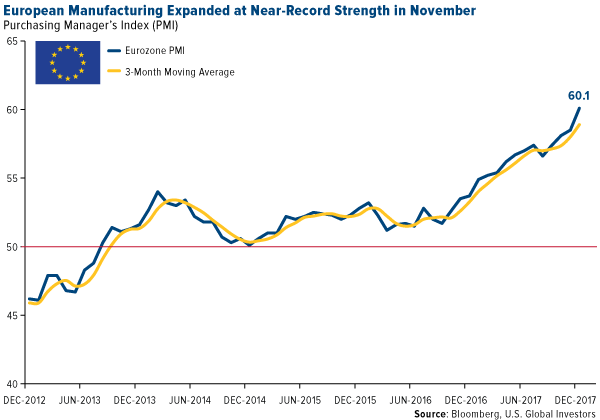

- PMIs readings improved for all countries in November, resulting in the best performance for euro zone manufacturing in over 17 years. IHS Markit’s final manufacturing PMI for the bloc climbed to 60.1 last month from October’s 58.5. PMIs readings in central emerging Europe moved higher. Hungary reported PMI reading of 58.6, Czech Republic 58.7, Poland 54.2, Turkey 52.9, Greece 52.2 and Russia 51.5. 2017 is expected to be the best year for euro zone economic growth in a decade.

- OPEC, including Russia, agreed to extend oil-production cuts to the end of 2018. The Russian economy depends on oil stability as most of the country’s revenue comes from the sale of oil and gas. Higher oil prices could help economy to stabilize and growth at a faster rate. In 2017, the growth is expected to reach 1.7 percent.

- Russian government will spend $8.6 billion over three years on measures to support families with more than once child. The welfare program will boost child payments and subsidize family mortgages. According to the finance minister, the money will come from government reserves and won’t require change in the budget. A similar plan was introduced in Poland, after the Law & Justice Party came to power. The additional money boosted consumer confidence and stimulated gross domestic product growth.

Threats

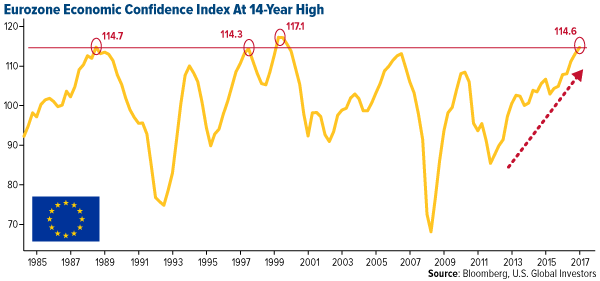

- The Eurozone Economic Sentiment Indicator, which tracks overall sentiment in the economy, improved again in November, supported mostly by strong consumer confidence and the construction sector. Confidence in the European Union (EU) has surged in the past couple years, despite some political obstacles like Brexit, the Catalonia push for independence and the failure of German coalition talks. As seen in the chart below, the latest reading of 114.6 is a 17 year high. The prior highest index readings in 1998 and 2000 were not too far from it, suggesting possible reversal.

- The Bundesbank, the central bank of Germany, released a financial stability report which said that low interest rates and the strong economic conditions in Germany might cause market participants to underestimate risks. Valuations for many investments are very high. The number of low-interest investments on the balance sheets of banks and insurers has risen quickly. The report added that an abrupt rise in interest rates or a continued period of low interest rates could hit the financial system hard.

- Jerome Powell, the next Federal Reserve Chairman, is expected to keep rising rates and trimming the U.S. balance sheet. Rising rates usually lead to a stronger dollar, which could adversely affect emerging Europe currencies. The lira is the most vulnerable to a strong dollar. Janet Yellen’s four-year term as Chair of the Board of Governors of the Federal Reserve System will end in February 2018.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits