5 Big Questions for 2018

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Today marks the fourth day of Hanukkah, and in only 10 days, many families across the world will be celebrating Christmas. Not only is it the season of giving, but it’s also time to reflect back on the past 12 months and look ahead to 2018.

Below are five questions to help guide your thinking when making investment decisions in the new year.

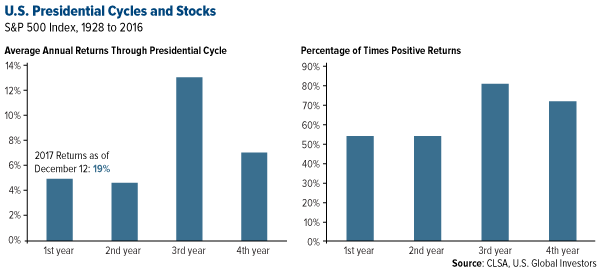

1. Will stocks follow the historical presidential cycle?

click to enlarge

click to enlargeNext month marks President Donald Trump’s first year in office and the beginning of his second. How have markets responded to his pro-growth policies, including pledges to lower taxes and slash regulations?

The answer: Overwhelmingly. As of my writing this, the S&P 500 Index is up 19 percent year-to-date, far outperforming the historical returns we’ve seen in the first year of a president’s four-year term.

In the second year, returns have traditionally been lower than the first. From 1928 to 2016, such years produced average market gains of just above 4 percent, making it the weakest year.

The reason for lower returns in the first two years, according to CLSA analysts this week, could be that “an administration looks to put as much bad news and painful actions into the first two years to form a good bias for getting reelected or paving the way for the predecessor of its own party.” Recall that President Bill Clinton didn’t hesitate to hike taxes after getting elected—he signed the Omnibus Budget Reconciliation Act just eight months into his first term.

But Trump has taken a different strategy. As CLSA puts it, “all the good news is being front loaded in the first half of this presidential cycle.” Right out of the gate, Trump placed major executive and legislative agenda items on the docket, from an Obamacare repeal to deregulation to sweeping tax cuts.

Not all of these efforts have borne fruit, of course. Even this week, his tax overhaul appeared to be imperiled after serious concerns were raised by moderate Republican senators such as Marco Rubio, Bob Corker and Jeff Flake.

I remain optimistic, though, and I see no reason at the moment to think that 2018 won’t be an encore of 2017. We’re nine years into the current equities bull market, the second-longest in U.S. history, but there could still be plenty of “gas in the tank,” according to a Bank of America Merrill Lynch report this week.

So with only a month remaining to Trump’s first term, it’s important to remember the words of Warren Buffett a day before the president was sworn in. Even though Buffett backed Hillary Clinton in the election, he said that “America works and I think it’ll work fine under Donald Trump.”

2. Will S&P 500 Index companies continue to post record-level earnings per share (EPS) in 2018?

Earnings per share (EPS) growth is one of the most reliable and closely monitored indicators of market health. It’s one of the key metrics we use to find the most growth-driven and profitable companies.

As my good friend Alex Green said in an interview back in August, “if you look back through history, you’d be hard-pressed to find a single example of a company that increased its earnings, quarter over quarter, year after year, and not see its stock tag along.”

Except for a slight dip from 2014 to 2015, when EPS for the S&P 500 Index fell from $119.70 to $117.55, earnings have been rising steadily since 2009.

As of today, EPS for 2017 stands at $133.73, a new record and up nearly 13 percent from last year.

Next year we could see them climb even higher, if estimates prove to be accurate. In a report this week, FactSet analysts predict EPS by year-end in 2018 to reach $143.17, 7 percent higher than 2017.

In other words, the American stock market is poised to continue its record-setting bull run in 2018.

3. Can small and mid-size businesses get any more pumped than they are now?

The short answer here is: Yes, they can—but not by much before a new all-time record is reached.

For the past 44 years, the National Federation of Independent Business (NFIB) has taken a monthly survey to measure the optimism of small-business owners, and in November, the index climbed to a skyscraping 107.5. That’s the second-highest reading ever, after the index hit 108.0 way back in July 1983 on the hopes of additional Reagan tax cuts.

If we drill down into the various index components, we find that owners are most optimistic about the next three months, with 27 percent saying it will be a “good time to expand,” up from only 11 percent one year ago. They’re ready to unleash capital, buy new equipment and increase labor.

In their monthly commentary, NFIB economists William Dunkelberg and Holly Wade wrote: “There is still much uncertainty about health care and taxes, but it appears that [small-business] owners believe that whatever Congress finally comes up with will be an improvement and so they remain positive.”

That positivity is shared by small-cap stock investors, who’ve driven up the Russell 2000 Index more than 12 percent since the beginning of the year.

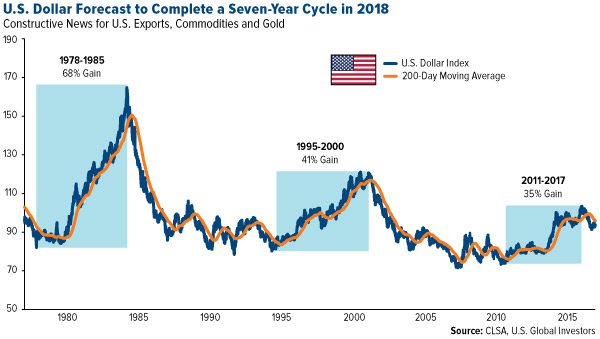

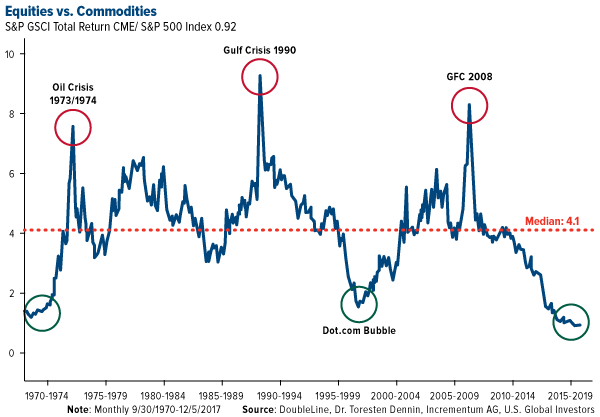

4. What will drive gold prices higher?

click to enlarge

click to enlargeAs of today, gold is up more than 9 percent for the year. If it stays at its current price level, gold will log its best year since 2011, when it returned 10 percent.

The yellow metal has faced a number of significant headwinds in 2017, including surging equity markets around the world and rate hikes by the Federal Reserve. Under the circumstances, I would describe its performance as highly respectable.

Potential tailwinds in 2018 could help the yellow metal crack the $1,300 level and head higher.

That includes a weaker U.S. dollar. CLSA analysts this week noted that the dollar has traditionally risen in seven-year cycles. Between 1978 and 1985, it gained 68 percent; between 1995 and 2000, 41 percent. The current bull market so far has seen the dollar rise 35 percent, which has been a challenge for gold, commodities and U.S. exports.

That might be set to change in 2018, when we could see a completion of the seven-year cycle. As CLSA writes, “our tactics through 2018 would be to sell U.S. dollar strength in anticipation of break below 91-92 support.”

Other possible tailwinds include geopolitical risks, negative real interest rates across the globe, continually expanding global debt and overvalued equities.

Just today, the North Atlantic Treaty Organization (NATO) raised concerns that Russia has developed a ground-launched cruise missile system that might violate a 1987 Cold War pact banning such weapons. It’s believed the missile system would be able to strike Europe on very short notice. Meanwhile, the U.S. State Department is working around the clock to encourage North Korea to abandon its nuclear weapons program. As a store of value, gold has historically performed well in such times.

Meanwhile, two-year government bond yields in a number of European countries—the Netherlands, Germany, Austria, Belgium, France, Spain and more—are below zero. As I’ve explained many times before, negative real rates have traditionally been constructive for gold in that particular country’s currency.

Finally, there’s some concern that too much money is flowing into equities right now. According to Bloomberg, the total market cap for world equities is now just a “whisker” away from hitting $100 trillion—a monumental sum, to be sure. Should there be a correction, the investment case for gold and precious metals will become stronger than ever.

5. Can anything stop bitcoin?

Bitcoin made some people a whole lot of money this year. One year ago today, the cryptocurrency was trading in the $770 to $780 range. Today, it briefly broke above $18,000. That’s a phenomenal return of 2,200 percent. The total market cap of all cryptocurrencies has already crossed above $500 billion and is well on its way to $1 trillion.

So is there anything that could stop its progress?

The most obvious answer might be regulations, but remember, bitcoin made these unexpected gains even as several countries clamped down on the digital currency. Venezuela, which will introduce its own government-sanctioned cryptocurrency, is scheduled to begin regulating bitcoin, but as the bolivar loses more and more of its value, residents have had to rely on bitcoin to survive.

It’s not surprising at all to see that bitcoin has undergone the greatest surge in peer-to-peer trading in countries that have imposed some of the most stringent regulations on cryptocurrencies. This is a currency, after all, that does not require any third-party involvement to trade. It’s able to bypass governments, central banks and borders with ease.

As I said last week, this is precisely why bitcoin is appealing to many investors. And according to Metcalfe’s law, more investors could mean higher ask prices.

Bitcoin might be very appealing right now, but it’s important to keep in mind that this has been a very volatile market. If I didn’t readily have the money to buy bitcoin, I wouldn’t go into debt and certainly wouldn’t mortgage my house to get my hands on it, as some people are reportedly doing.

December 14, 2017The Secret to Driving on Both Sides of the Road According to Frank Holmes |

December 13, 2017Inflation Expected to Rise with Higher Wages and Oil Prices |

December 13, 2017U.S. Global Investors Taps Into Virtual Currency Market |

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.33 percent. The S&P 500 Stock Index rose 0.92 percent, while the Nasdaq Composite climbed 1.41 percent. The Russell 2000 small capitalization index gained 0.57 percent this week.

- The Hang Seng Composite gained 0.55 percent this week; while Taiwan was up 0.89 percent and the KOSPI rose 0.73 percent.

- The 10-year Treasury bond yield fell 2.5 basis points to 2.35 percent.

Domestic Equity Market

Strengths

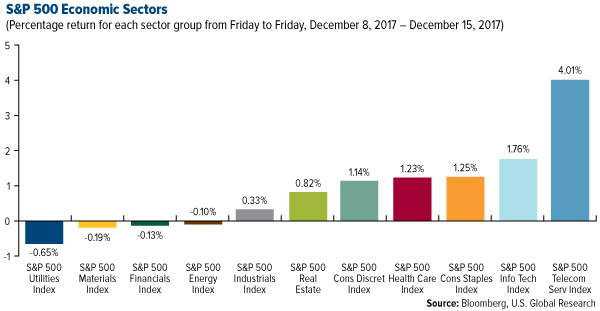

- Telecommunications was the best performing sector of the week, increasing by 4.01 percent versus an overall increase of 0.92 percent for the S&P 500.

- Centurylink was the best performing stock for the week, increasing 15.81%.

- Shares of Under Armour were up as much as 11.9 percent on Friday. The big jump was primarily caused by a note released by Stifel analyst Jim Duffy, who upgraded his rating on Under Armour from "hold" to "buy." Duffy also increased his price target to $17, $5 higher than the prior $12 target.

Weaknesses

- Utilities was the worst performing sector for the week, falling 0.65 percent versus an overall increase of 0.92 percent for the S&P 500.

- Centene was the worst performing stock for the week, falling 6.39 percent.

- CSX stock nosedived Friday following news that President and CEO Hunter Harrison is on unplanned medical leave. The stock dropped nearly 10 percent in pre-market trading.

Opportunities

- Bank of America says the bull market has plenty of “gas in the tank.” The bank's technical team says that the chart for 2018 looks a lot like that of 2014 and that the S&P 500 could hit 3,000 by the end of next year.

- Disney will acquire Fox TV's film and TV assets for $52.4 billion, obtaining brands like "The Simpsons,” "X-Men" and the film "Avatar." Fox shareholders will receive 0.2745 Disney shares for each unit of Fox stock they own. Disney also announced that it would buy back $10 billion of stock to offset the share dilution from the deal.

- Samsung is planning to release its first smart speakers integrated with its digital assistant Bixby in the first half of 2018, according to Bloomberg. Its speakers will reportedly cost around $200 and compete against Apple's HomePod speaker, Amazon's Echo devices, and Google Home.

Threats

- Morgan Stanley laid out three things that could slow the sizzling FAANG stocks in 2018: a heavy concentration of broader market gains in those stocks, a reversal of growth stocks beating value stocks, and a historical tendency for outperformers in a given year to underperform the following year. While the firm isn't bearish on the group heading into next year, it does say that its massive outperformance could slow.

- Geopolitical risk is the biggest fear in markets right now, according to a Barclays survey of over 700 institutional clients. The firm says the concerns are a combination of developments on the Korean peninsula, tensions with Russia, political turmoil in Saudi Arabia, Brexit and less predictability in U.S. foreign policy.

- According to InvestorPlace, the five stocks that are at the most risk from the net neutrality vote are Facebook, Netflix, Twitter, Alphabet and Amazon.

The Economy and Bond Market

Strengths

- The NFIB Small Business Optimism Index soared to 107.5 in November, hitting its highest level since 1983, according to Bloomberg.

- Eurozone flash December manufacturing PMI hit a record high of 62.0 versus consensus 59.7 and prior 60.1, following the best factory output and order book gains since 2000. Services sector PMI registered the highest level since early 2011 at 56.5 versus consensus 56.0 and prior 56.2 (and has also underpinned the notion of a broad-based expansion in euro area output). The survey showed job creation running at its highest level in 2017.

- Americans are spending more as the holiday season continues. November retail sales were up 0.8 percent from the prior month versus the 0.3 percent increase expected by economists.

Weaknesses

- Americans’ paychecks aren’t stretching quite as far lately. Even though inflation is only gradually picking up, it’s outpacing wages, according to Labor Department figures. Adjusted for inflation, average hourly earnings dropped 0.2 percent in November from the previous month, the fourth straight decline and the longest such period since the second half of 2009 when the economy was clawing its way back from the Great Recession.

- For November, the Industrial Production report came in at 0.2 percent, lower than the 0.3 percent forecast. The Empire Manufacturing report also disappointed, coming in at 18.0 versus expectations of 18.7.

- While the core consumer price inflation (CPI) measure met expectations of 0.4 percent, the PCI ex food and energy was lower than expected at 0.1 percent versus 0.2 percent.

Opportunities

- Given the strength seen in this week's retail sales, household consumption is likely to be strong in the PCE report next Friday. Investors and the Federal Reserve will also be looking closely at the core PCE deflator to determine if inflation is making any progress toward the 2 percent target.

- Next Friday’s durable goods orders report should confirm that capex investment is reviving.

- In Europe, the German Ifo survey on Tuesday will be the highlight of the week. It should mirror the strength seen in this week's PMIs and confirm that economic growth is quite robust.

Threats

- The Fed raised rates 25 bps to 1.5 percent, but left its outlook unchanged. It judged the tax cuts to boost the economy next year, but with no lasting benefit, and its estimate of long-run growth stalled at 1.8 percent.

- In the view of Wells Fargo, this year’s resurgence in Chinese buying of treasuries is likely to peter out as the yuan stabilizes after a steep gain in 2017. Most analysts see little change in the yuan through 2018, from its current level of around 6.62 per dollar. A steady exchange rate suggests limited pressure on Chinese authorities to increase their Treasury holdings as part of intervening in currency markets. For the U.S., the specter of cooler Chinese demand comes at an inopportune time, with the Federal Reserve tapering its portfolio of treasuries and Congress debating a tax-overhaul plan that could increase the federal deficit by $1 trillion over the next decade. The U.S. debt burden was already forecast to swell by $10 trillion in that period even before any tax changes. U.S. borrowing costs could rise as a result.

- The Shanghai Containerized Freight Index slipped to 763.14, its lowest level in a year. The world Index (WCIDCOMP) is also the lowest since September last year, and down 21 percent from the 52-week moving average. Given how instrumental trade has been to the global economy, any further weakening would be of concern.

Gold Market

This week spot gold closed at $1,255.45, up $6.95 per ounce, or 0.56 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.79 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index came in up 1.04 percent. The U.S. Trade-Weighted Dollar finished the week essentially flat.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-12 | ZEW Survey Current Situation | 88.7 | 89.3 | 88.8 |

| Dec-12 | ZEW Survey Expectations | 18.0 | 17.4 | 18.7 |

| Dec-12 | PPI Final Demand YoY | 2.9% | 3.1% | 2.8% |

| Dec-13 | Germany CPI YoY | 1.8% | 1.8% | 1.8% |

| Dec-13 | CPI YoY | 2.2% | 2.2% | 2.0% |

| Dec-13 | FOMC Rate Decision (Upper Bound) | 1.50% | 1.50% | 1.25% |

| Dec-14 | China Retail Sales YoY | 10.3% | 10.2% | 10.0% |

| Dec-14 | ECB Main Refinancing Rate | 0.0% | 0.0% | 0.0% |

| Dec-14 | Initial Jobless Claims | 236k | 225k | 236k |

| Dec-18 | Eurozone CPI Core YoY | 0.9% | -- | 0.9% |

| Dec-19 | Housing Starts | 1245k | -- | 1290k |

| Dec-21 | GDP Annualized QoQ | 3.3% | -- | 3.3% |

| Dec-21 | Initial Jobless Claims | 235k | -- | 225k |

| Dec-22 | Durable Goods Orders | 2.0% | -- | -0.8% |

| Dec-22 | New Home Sales | 650k | -- | 685k |

Strengths

- The best performing precious metal for the week was palladium, up 1.71 percent. Automobile replacement was up due to water damaged cars post hurricane season. Catalytic converters containing palladium will enter the recycling phase. A Bloomberg survey of gold traders shows most are bullish on the yellow metal after the Federal Reserve raised rates earlier in the week. This is in part due to gold advancing for the first time in four weeks as the Fed stuck to its projection of three hikes in 2018, writes Ranjeetha Pakiam of Bloomberg.

- The European Central Bank left its policy rate unchanged, leading Bloomberg Intelligence analyst Mike McGlone to suggest that relative value and mean reversion might lead to gold outperforming bitcoin and the U.S. dollar. Gold counter-intuitively rallied the last five times the Fed raised interest rates, leading some to believe gold has no reason not to rally again.

- Pure Gold Mining Inc. announced the addition of mineral resources to two of its mines in Ontario. The estimate includes an additional 96,000 ounces of indicated resources and 118,000 ounces of inferred resources. CEO and President of the company, Darin Labrenz, said the addition has “strong potential to positively impact project economics."

Weaknesses

- The worst performing precious metal for the week was platinum, up just 0.57 percent post the rate hike but not out of favor completely as Sibanye Gold made an all-share takeout offer for Lonmin which has been on the ropes for several years now. The Democratic Republic of Congo changed its mining code again with details still emerging. The last time the nation changed its code it resulted in increased royalties, tax rates, minimum unpaid share of new mining projects and now, for large projects, 10 percent of a mine’s shares must be owned by a Congolese investor.

- Bloomberg reports that economists are telling investors to prepare for the largest tightening of monetary policy in more than 10 years as forecasts predict average interest rates to rise at least 1 percent next year, the biggest increase since 2006.

- Two of Gold Fields Ghana mines will now use contractors for operations. A contractor will take over the Tarkwa operations early next year after terminating 1,500 staff while the Damang mine has been run by contractors since 2016. Perhaps Gold Fields is winding down its focus on operating these two mines to instead have increased future focus on the Namdini project in Ghana owned by Cardinal Resources of which Gold Fields has an interest in.

Opportunities

- Over the past thirty years gold and silver metal equities have demonstrated seasonal trading patterns, which means now is the time to buy the precious metals when they are at a bargain. The seasonal rally has occurred from December to February four of the past five years, reports CIBC World Markets Corp. The history of rate hikes also favors gold faring better than expected while in the aftermath of previous rate hikes bitcoin declined 20 percent dipping below its 60-day mean.

- John Reade, chief market strategist of the World Gold Council, believes gold will continue its upward trajectory in 2018. Reade said, “Investor attention may have been focused on U.S. equity markets, technology stocks and cryptocurrencies this year, but gold still had a decent 2017, delivering double-digit growth in the first eleven months alone.”

- UBS Global Macro Strategy analyzed the repatriation component of the upcoming tax bill and found that it may not ignite capital inflows back to the U.S. They report that nearly three quarters of foreign retained earnings are already in U.S. dollars and that a large share of non-U.S. dollar cash held abroad is hedged or used for offshore operations. During the last tax holiday of 2005-2006 to bring dollars back to the U.S., the dollar ended flat. Lananh Nguyen of Bloomberg writes that the U.S. dollar will continue to worsen into 2018 as the greenback is currently down more than 7 percent versus the world’s major currencies this year, and he expects the euro and other emerging markets to do well in 2018.

Threats

- Libor, the interest rate basis for trillions of dollars in loans, is surging after the Federal Reserve’s latest interest-rate increase, reports Bloomberg. Three-month dollar Libor hit 1.6 percent after the rate increase, the highest level since December 2008 during the global financial crisis.

- For cross-currency basis swap, the interest rate differential between the dollar and euro is making dollar-funding much more expensive with Libor surging. Macro Strategy Partnership suggests that the extra cost to borrow U.S. dollars in Europe is equivalent to a 150 basis point rate hike for the offshore U.S. dollar economy and suggests investors should avoid commodities and miners.

- Dominic Schnider, head of commodities at UBS Wealth Management said in a Bloomberg TV interview that gold is likely to trade around $1,200 in early 2018 due to slower physical demand but expects that demand to rebuild closer to the end of 2018.

December 14, 2017Coinbase and the IRS: A Win for Both |

December 13, 2017Visit the Top Blockchain and Cryptocurrency Power Hubs of the World |

December 11, 2017This Week in Bitcoin: IRS Targets Coinbase, Venezuela Launches Own Cryptocurrency |

Energy and Natural Resources Market

Strengths

- Gold was the best performing major commodity this week, with prices advancing 0.7 percent. Gold futures posted its first weekly gain in a month after the Federal Reserve eased concerns over the pace of interest rate increases, which led the U.S. dollar for a weekly loss.

- "I think investors should add commodities to their portfolios," Jeffrey Gundlach tells investors. Gundlach, founder of DoubleLine Capital, said commodities are just as cheap relative to stocks as they were at historical turning points. While the macroeconomic backdrop also supports the case for commodities, Gundlach believes 2018 may prove a turning point for the sector.

- Freeport-McMoran Inc. was the best performing stock in the global resource market this week, rising 4.9 percent. Indonesia and Freeport may sign a new agreement as soon as this weekend that will lay out a roadmap for the transfer of majority ownership of the giant Grasberg mine to a local firm.

Weaknesses

- Platinum was the worst performing commodity this week, dropping 1.4 percent. Money managers flipped to bearish from bullish on the precious metals with short positions outnumbering long positions.

- The oil rig count in North America fell by four this week to 747, the first week in as many as six to see a decline. Although the move is likely an effort to moderate capacity growth, it could also been seen as a sign that some producers are concerned expansion cannot be supported by current oil prices.

- Painted Pony Energy, a Canadian crude producer, was the worst performing stock in the resource market this week. The company announced a subdued 2018 capital budget which will result in average production down to 62 million barrels of oil equivalent a day (mboe/d), compared to prior forecast Of 70 mboe/d.

Opportunities

- Copper is heading for its best year since 2010, racking up gains of about 24 percent, more than twice gold’s advance. The price ratio of copper to bullion is near a three-year high as better-than-expected economic growth boosts investor optimism over base-metals use.

- Axiom analysts upgraded US Steel stock in positive views on the sector. Analysts argue that protectionism from the Trump administration, as well as positive seasonality in the steel market, could result in a more optimistic tone for the sector.

- Metals Focus analysts estimate that silver demand in India, one of the world’s top importers of the white metal, could rise again in 2018. Imports surged this year to 5,500 tonnes, compared to 3,000 in 2016, and could climb as high as 6,000 tonnes by the end of next year.

Threats

- The World Bank has announced it will end financial support for oil and gas extraction projects globally. The Bank announced in Paris it “will no longer finance upstream oil and gas” after 2019 in response to threat posed by climate change.

- Crude’s rally fizzled out for a third week, with prices stalled near $57 a barrel. Concerns over excess supplies next year tempered enthusiasm for the Organization of Petroleum Exporting Countries’ (OPEC) extended production curbs. Both OPEC and the International Energy Agency (IEA) warned that current oil prices are conducive to production growth out of the shale basins in the US.

- China producer price inflation slowed to a four-month low in November as factory activity softened due to government’s ongoing efforts to curb pollution, thus cooling demand from factories and raw materials.

China Region

Strengths

- Malaysia’s FTSE Bursa Malaysia Kuala Lumpur Composite Index (KLCI) climbed 1.89 percent for the week. Indonesia’s Jakarta Composite also put in a strong showing, finishing up 1.49 percent for the week.

- Consumer services constituted the top-performing sector in the Hang Seng Composite Index (HSCI) this week, rising 3.18 percent.

- Both imports and exports beat expectations in Indonesia this month, though down from last month’s numbers. Year-over-year imports rose 19.62 percent, ahead of expectations for a gain of 13.00 percent, while exports were up 13.18 percent, ahead of an anticipated 12.63 percent pace.

Weaknesses

- Most of the region had a mildly positive week, but China’s Shanghai Composite Index, Vietnam’s Ho Chi Minh Stock Index, and Singapore’s Straits Times Total Return Index all declined for the week, falling 73, 53, and 22 basis points, respectively.

- Information technology was the weakest sector in the Hang Seng Composite Index this week, declining 1.32 percent.

- Year-over-year exports from the Philippines missed expectations this week, coming in at a growth rate of 6.6 percent, below an anticipated reading of a 6.9 percent rate.

Opportunities

- American tech giant Google seeks to deepen its push into China and bolster its investment and research in artificial intelligence. The tech giant this week said that its Alphabet Inc. unit will open a new Beijing research facility, The Google AI China Center, according to Bloomberg News.

- While several Chinese data came in more or less in line this week (retail sales, fixed asset investment, intellectual property), new yuan loans and aggregate financing came in ahead of expectations. But of particular note is the big jump in foreign direct investment (FDI), which clocked in at a growth rate of 90.7 percent for November (significantly higher than last month’s 5.0 percent reading).

- It seems that massive technology companies just can’t stay away from grocery stores these days. While the U.S. has seen its share of high profile investments recently, Bloomberg News reports that Tencent Holdings announced an agreement to take a 5 percent stake in China’s Yonghui Superstores for about $639 million this week. Alibaba recently purchased a 36 percent stake in Chinese hypermarket operator Sun Art.

Threats

- North Korea remains relevant as a regional risk, though U.S. Secretary of State Rex Tillerson announced this week that the United States is prepared to negotiate with Pyongyang without preconditions, indicating preconditions are likely, at this point, unrealistic and impractical.

- Hong Kong’s Securities and Futures Commission stressed the potential risks associated with cryptocurrency futures and related investment products earlier this week, Bloomberg reports. In a separate story from Bloomberg but also of note: according to a recent study, China is home to more than half of the major computer pools generating digital currency

- According to Reuters, smog warnings across northern China forced authorities to “order factories to reduce output, construction sites to slow work, and the enforcement of limits on the use of diesel-fueled vehicles” on Thursday. The highest pollution reading came from the city of Taiyuan in Shanxi province, the article continues, at 344 micrograms per cubic meter of hazardous particles. The World Health Organization (WHO) recommends concentrations of no more than 10 micrograms per cubic meter.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 3.65 percent. Gains on the Athens stock exchange were led by banks. Greek banks have been cleaning up their balance sheets, and many analysts are optimistic for the stress test results and the overall asset quality. Banks trade at a 70 percent discount to European Union peers, or 0.3 times price-to-book value on 2018 estimates, according to Auerbach Grayson research.

- The Russian ruble was the best performing currency this week, gaining 48 basis points against the U.S. dollar. Despite larger-than-expected rate cuts by the Bank of Russia, the ruble strengthened over the past five day. Russia has one of the highest real yields among emerging markets, and its currency is supported by prospects of higher oil prices.

- The telecommunication service sector was the best performing sector among eastern European markets this week.

Weaknesses

- Romania was the worst performing country this week, losing 1.17 percent. Weak trade balance and current account data released this week point to the deteriorating macro view. Romania’s current account deficit for 2017 will exceed 3 percent of GDP, the largest deficit among the European Union’s emerging economies.

- The Turkish lira was the worst performing currency this week, losing 82 basis points against the U.S. dollar. The Central Bank of Turkey raised its late liquidity lending rate by 50 basis points; a 100 basis points hike was expected.

- Health care was the worst performing sector among eastern European markets this week.

Opportunities

- Global central banks started to hike rates, but the European Central Bank (ECB) left its monetary policy unchanged this week, as expected. The ECB also reiterated that official rates will remain at the present level well past the end of the asset purchase program. The Bank also raised its GDP forecast to 2.4 percent from 2.2 percent for this year, and next year’s growth was revised up from 1.8 percent to 2.3 percent.

- October industrial production growth in the eurozone came in at 0.2 percent month-over- month, which was better than expected. Year-over-year growth was 3.7 percent. Preliminary December Manufacturing purchasing managers’ index (PMI) data reached a new high level of 60.6, above expectations of 59.7, and the prior reading of 60.1. Manufacturing businesses are expanding, pushing production, new orders and exports higher, and pointing to stronger euro area growth in the last quarter of the year.

- The Central Bank of Russia surprised the market with a 50 basis points cut while the market watcher expected a 25 basis points cut. The key rate stands at 7.75 percent, and more cuts are expected next year. The bank raised its 2018 oil price forecast to $55 per barrel from $44. Given the better outlook for oil, the Bank of Russia revised its 2018 GPD forecast to 2.2 percent from 1.7 percent.

Threats

- Stronger third-quarter GDP growth in Turkey of 11.1 percent year-over-year allowed the central bank to deliver a 50 basis point hike on Thursday. The 10-year Turkish government bond yields have been around 12.5 percent, but high inflation is eating away at this yield. According to JP Morgan research, inflation should fall to 10 percent over the next four months. As inflation declines, real rates should attract carry trades and support the country’s currency.

- After elections in Germany, France and the UK this year, now Italy will hold general elections on March 4, 2018. Recent polls and local election results suggest that Italy’s Northern League, and anti-EU and anti-immigration party, has a chance at governing in a coalition with the center-right Forza Italia party. Italy is the fourth-largest economy in Europe, and the next government will have to work on reducing debt, improving the banking system and breaking out of stagnation.

- Russia’s central bank is stepping in to bailout another systematically important financial institution. Promosvyazbank was Russia’s ninth biggest bank as of December 1, with assets of 1.3 trillion rubles, according to the central bank. Two other large banks, Otkritie and B&N, were placed under the central bank’s administration recently. This is the third rescue of a major lender since August.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits