There has been no let-up to the economic news cycle this year. Even the approach of the holiday season has failed to offer a respite, with tax reform deliberations ongoing through the holidays.

We’ve been hesitating to send out an update to our U.S. outlook, awaiting final word from Washington. With passage of reform now likely and major details now public, we’re venturing a guess as to how the economy might react to the substantial fiscal stimulus that is being offered.

A word of caution is in order. Many details of the bill came together at the eleventh hour and are not well understood. Experts are already predicting a series of technical corrections to the new rules in the coming year to avert unintended consequences. Final amendments could certainly affect specific taxpayers, but we are assuming that they will not have a substantial influence on the broader economy.

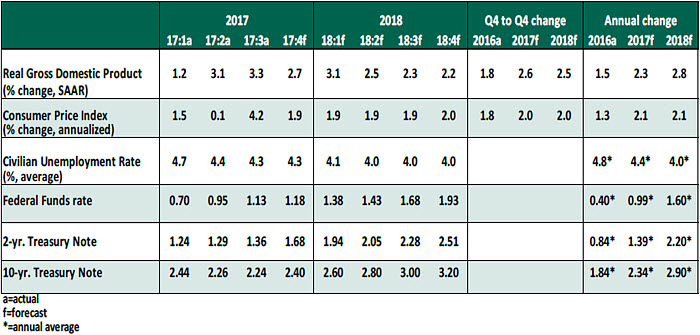

Key Economic Indicators

Influences on the Forecast

- Holiday spending has been excellent so far, with retail analysts expecting this to be the best shopping season since 2010. November retail sales exceeded expectations by a wide margin. Strong employment news and accumulating wealth effects from strong markets are buoying consumers, and should continue to do so. We’re holding our fourth quarter growth estimate at 2.7%, but there is upside potential.

- We have upgraded our projection for real gross domestic product (GDP) in 2018. Due to the tax reform proposal, we have added about 0.5% to the forecasted level of GDP growth next year.

The influence of tax reform will be seen most prominently in the following areas:

a) Many households will see a reduction in their overall tax bills, which should release funds for spending. The degree to which this benefit will be realized (or whether it will be realized at all) depends critically on individual circumstances.

b) Tax rates for large and small businesses have been substantially reduced. The additional profits can be used to increase investment, dividends or share repurchases. While each of these has somewhat different influences on GDP, all would be stimulative.

c) Firms will be immediately allowed to expense capital expenditures during the coming five years. We expect this to provide a boost to business investment, which was already progressing nicely.

The reform proposal removes the incentive of firms to hold profits overseas, and makes it much less attractive for technology companies to shift their earnings outside of the U.S. using transfer pricing. If this prompts a change in bookkeeping behavior, the U.S. trade deficit could fall by quite a bit. Coverage of this angle can be found here.

- We expect the tax reform bill to add to inflation and inflation risk. Simply stated, we are adding substantial stimulus to an economy already operating near full capacity. While firms have been resourceful in limiting prices, additional momentum may challenge that discipline.

- We have added a third Federal Reserve interest rate hike to our projections for 2018. Our anticipation is that the next move will come in June 2018, allowing time to observe the evolution of inflation. If pricing conditions evolve as expected, the Fed will be making quarterly moves from mid-year 2018 to mid-year 2019. A somewhat more hawkish group of voting members on the Federal Open Market Committee could accelerate this program.

- Long-term interest rates have been held down by substantial demand from foreign portfolios. This development has diminished the “term premium” that rewards investors for taking interest rate risk. With U.S. rates higher than those of other developed markets, we expect this appetite to be sustained, but we are expecting longer-term interest rates to drift upward over the coming year as inflation rises, the Fed tightens and the U.S. federal deficit increases.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit

© Northern Trust

Read more commentaries by Northern Trust