10 Charts That Show Why Gold Is Undervalued Right Now

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

With the year quickly coming to a close, it might be time to start thinking about rebalancing the gold holdings in your portfolio. That includes bullion, jewelry, gold stocks and well-managed gold funds—all of which I recommend giving a collective 10 percent weighting. Because it’s been such a strong year for stocks—they’ve advanced more than 20 percent as of today—it’s likely that most investors will need to add to their gold exposure to meet that 10 percent weighting as we head into 2018.

Some investors might wonder why they need gold in their portfolios right now. The stock market is still chugging along, and the just-passed tax reform bill is likely to help ratchet up share prices even more. Cryptocurrencies have been hogging the spotlight lately, especially after bitcoin tumbled nearly 30 percent on Friday morning.

While I’m on the subject, inflows into cryptocurrencies have totaled more than $500 billion this year alone. To put that in perspective, the total sum of global equity mutual fund and ETF inflows were around $411 billion as of November 29. What’s more, cryptocurrencies are now doing as much daily trading as the New York Stock Exchange (NYSE), according to Business Insider.

Just think on that. Something is happening here that cannot be ignored or dismissed.

But back to gold. It’s important to remember that the precious metal has historically shared a low-to-negative correlation with many traditional assets such as cash, Treasuries and stocks, both domestic and international. This makes it, I believe, an appealing diversifier in the event of a correction in the capital and forex markets.

Need more reasons to add to your gold holdings? Below are 10 charts that show why the yellow metal is undervalued right now:

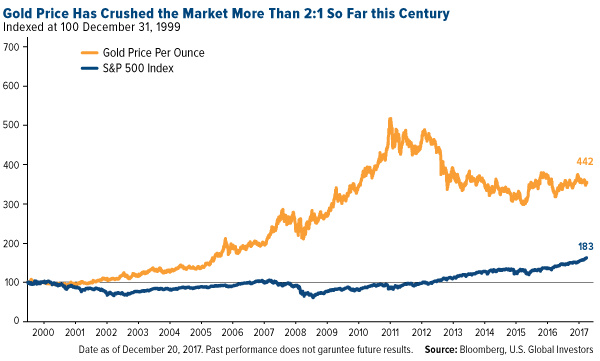

1. The gold price has crushed the market so far this century.

click to enlarge

click to enlargeInvestors are invariably surprised to see this chart whenever I show it at conferences. Believe it or not, since 2000, the gold price has beaten the S&P 500 Index, which has undergone two 40 percent corrections so far this century.

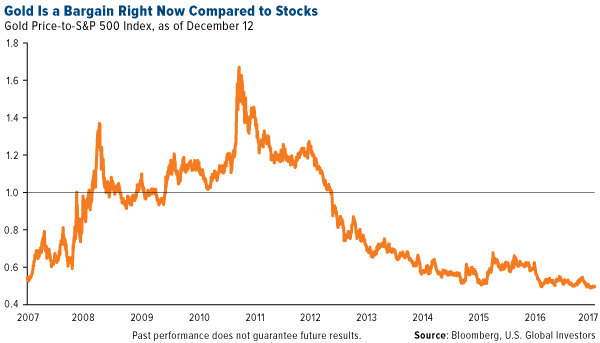

2. Compared to stocks, gold looks like a bargain.

click to enlarge

click to enlargeAs of this month, the gold-to-S&P 500 ratio is at its lowest point in 10 years. For mean reversion to occur, either the gold price needs to appreciate or share prices need to fall. Either way, consider this a once-in-a-decade opportunity.

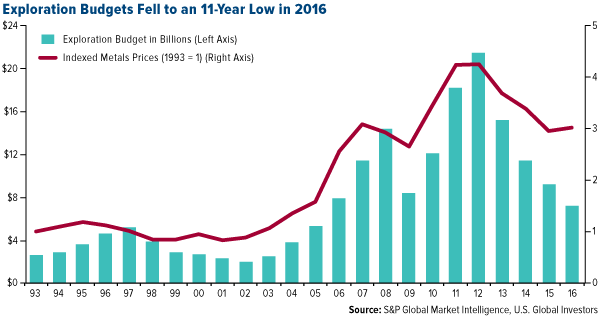

3. Exploration budgets keep getting slashed.

click to enlarge

click to enlargeOne of the reasons why gold is so highly valued is for its scarcity. There’s a possibility it could get even scarcer as explorers continue to trim exploration budgets and uncover fewer and fewer large deposits. The time between initial discovery and day one of production is also expanding. This has led many experts in the field to wonder if we’ve finally reached “peak gold.”

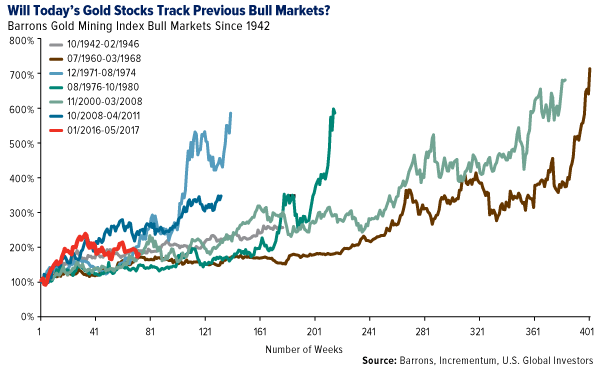

4. Gold stocks could be just getting started.

click to enlarge

click to enlargeLast year marked a turnaround in gold prices and gold stocks, and according to analysts at Incrementum Capital Partners, a Swiss financial management firm, they’re just getting warmed up. When charted against past gold bull markets, the present one looks as if it still has a lot of room to run.

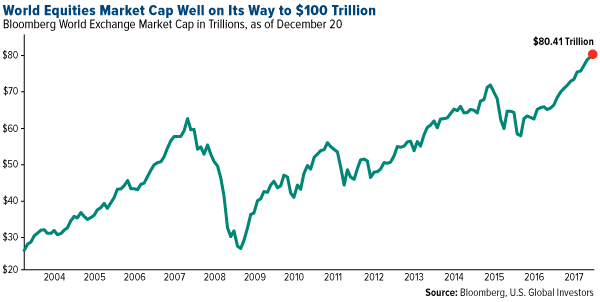

5. Is too much money going into equities?

click to enlarge

click to enlargeMore than $80 trillion sits in global equities right now, a monumental sum that’s likely to surge even more as we venture further into the bull market. Some worry this is a ticking time bomb just waiting to go off. Another correction similar to the one 10 years ago would wipe out trillions of dollars around the world, and it’s then that the investment case for gold would become strongest.

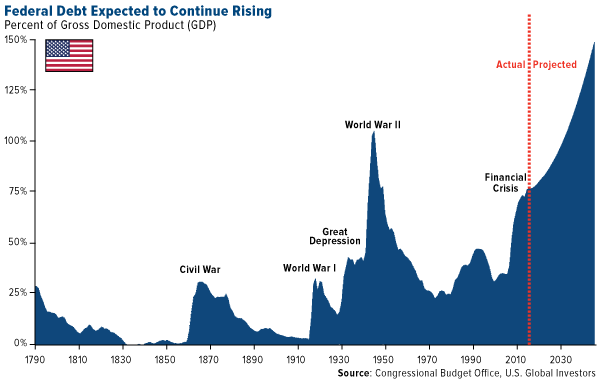

6. Higher debt could mean higher gold prices.

click to enlarge

click to enlargeThe yellow metal has historically tracked global debt, which stood at $217 trillion as of the first quarter of this year. Looking just at the U.S., debt is expected to continue on an upward trend, driven not just by new, and largely unfunded, spending but also underlying interest. By most estimates, President Donald Trump’s historic tax cuts, although welcome, will contribute to even higher debt as a percent of gross domestic product (GDP).

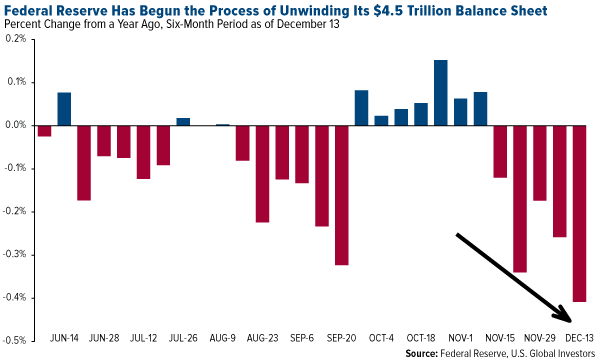

7. The Fed’s about to take away the punch bowl.

click to enlarge

click to enlarge“My opinion is that business cycles don’t just end accidentally. They end by the Fed. If the Fed tightens enough to induce a recession, that’s the end of the business cycle.” That’s according to MKM Partners’ chief economist Mike Darda, who was referring to the Federal Reserve’s efforts to unwind its $4.5 trillion balance sheet after it bought vast quantities of government bonds and mortgage-backed securities to mitigate the effects of the Great Recession. There’s definitely a huge amount of risk here: Five of the previous six times the Fed has similarly reduced its balance sheet, between 1921 and 2000, ended in recession.

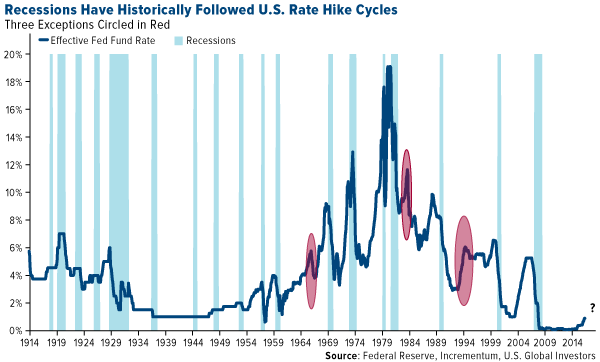

8. Rate hike cycles have rarely ended well.

click to enlarge

click to enlargeRate hike cycles also have a mixed record. According to Incrementum research, only three such cycles in the past 100 years have not ended in a recession. Obviously there’s no guarantee that this particular round of tightening will have the same outcome, but if you recognize the risk here, it might be prudent to have as much as 10 percent of your wealth in gold bullion and gold stocks.

9. Trillions of dollars of global bonds are guaranteed to lose money right now.

click to enlarge

click to enlargeAs of May of this year, nearly $10 trillion of bonds around the world were guaranteed to cost investors money, as more and more central banks instituted negative interest rate policies (NIRPs) to spur consumer spending. Instead, it encouraged many savers to yank their cash out of banks and convert it into gold. That’s precisely what households in Germany did, and by 2016, the European country became the world’s biggest investor in the yellow metal.

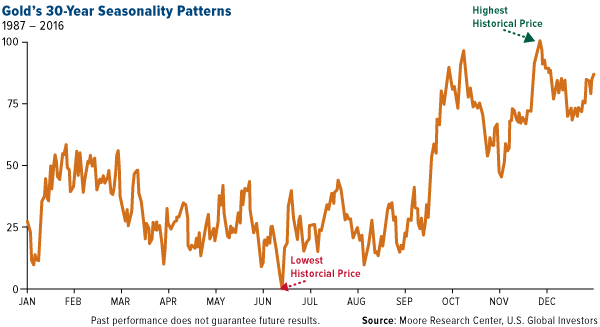

10. The Love Trade is still driving gold demand.

click to enlarge

click to enlargeThe chart above, based on data provided by Moore Research, shows gold’s 30-year seasonal trading pattern. Although it’s changed over the past few years, the pattern reflects the Love Trade in practice. According to the data, the gold price rallies early in the year as we approach the Chinese New Year, then dips in the summer. After that it surges on massive gold-buying in India during Diwali, in late October and early November. Finally, it ends the year at its highest point during the Indian wedding season, when demand is high. The pattern isn’t always observed exactly how I described, but it happens frequently enough for us to make educated, informed decisions on when to trade the precious metal.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.42 percent. The S&P 500 Stock Index rose 0.29 percent, while the Nasdaq Composite climbed 0.34 percent. The Russell 2000 small capitalization index gained 0.83 percent this week.

- The Hang Seng Composite gained 2.64 percent this week; while Taiwan was up 0.44 percent and the KOSPI fell 1.67 percent.

- The 10-year Treasury bond yield rose 12 basis points to 2.48 percent.

Domestic Equity Market

Strengths

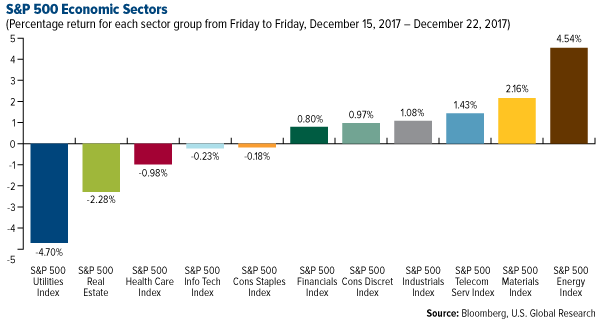

- Energy was the best performing sector of the week, increasing by 4.54 percent versus an overall increase of 0.28 percent for the S&P 500.

- Discovery Communications was the best performing stock for the week, increasing 13.77 percent.

- Global IPO activity has hit a post-financial crisis high. Ernst and Young's Global IPO Report found that 1,624 companies have gone public worldwide in 2017, making for a 49 percent increase versus the prior year and the highest total since 2007.

Weaknesses

- Utilities was the worst performing sector for the week, falling 0.65 percent versus an overall increase of 0.28 percent for the S&P 500.

- PG&E Corp was the worst performing stock for the week, falling 15.98 percent.

- Chipotle's latest health scare caught traders off-guard. The stock dropped Wednesday amid reports that another one of its stores could be tied to an illness outbreak, leaving traders unprepared as downside hedges sat at their lowest level in a decade.

Opportunities

- The tax reform bill is largely expected to provide a boost to stocks as a result of lower corporate tax rates and a tax repatriation holiday. Companies are rushing to announce special bonuses and pay hikes. AT&T, Boeing, Wells Fargo, and Comcast are among the companies that have announced plans to pay employees a special bonus, increase their minimum wage, or announce capital expenditures following the passage of the Tax Cuts and Jobs Act.

- According to Goldman Sachs, the companies that stand to benefit the most from the tax reform act are General Electric, Foot Locker, Citrix Systems, Western Digital, Waters Corp, Ralph Lauren, Microsoft, Oracle, Amgen, Apple, Qualcomm, NetApp and Cisco Systems.

- FedEx boosted its guidance. The company beat on both the top and bottom lines and raised its full-year fiscal 2018 earnings forecast to a range of $12.70 to $13.30 a share.

Threats

- Traders are increasing their bets that the stock market will encounter more turmoil. Investors are increasingly wagering on stock market volatility, according to a measure of options trading.

- Corporate borrowing drove global debt issuance to a record $6.8 trillion in 2017 and made up 55 percent of global debt issuance for the year.

- An analyst from Nomura downgraded Apple stock because of "historical patterns." According to the analyst, the company's stock has historically taken a hit following the launch of "tick" iPhone models, like the iPhone 5 and iPhone 6.

December 20, 2017Coming Housing Boom Could Mean It's Time to Add Raw Materials |

December 18, 20175 Big Questions for 2018 |

December 14, 2017Coinbase and the IRS: A Win for Both |

The Economy and Bond Market

Strengths

- Sales of new U.S. single-family homes unexpectedly rose in November, hitting their highest level in more than 10 years, driven by robust demand across the country. The Commerce Department reported new home sales jumped 17.5 percent to a seasonally adjusted annual rate of 733,000 units last month. That was the highest level since July 2007. Sales surged 26.6 percent from a year ago.

- U.S. consumer spending accelerated in November. The Commerce Department reported consumer spending, which accounts for more than two-thirds of U.S. economic activity, rose 0.6 percent last month after a downwardly revised 0.2 percent increase in October.

- Overall orders for durable goods rebounded 1.3 percent last month as demand for transportation equipment surged 4.2 percent. Durable goods orders had fallen 0.4 percent in October.

Weaknesses

- U.S. gross domestic product (GDP) was revised slightly lower on weaker consumer spending. GDP increased by 3.2 percent, down from the prior 3.3 percent estimate, as the growth of consumer spending was found to be weaker than initially reported.

- U.S. Treasuries extended a sell-off this week alongside major bond markets in Europe and Asia. Some investors are speculating that tax cuts could stoke economic growth and alter how the Federal Reserve approaches interest-rate increases. Furthermore, there’s concern that the Fed's reduction of its bond purchases would increase the market's supply. The 10-year yield has climbed to its highest level in nine months.

- The University of Michigan Sentiment Index fell to 95.9 from the previous print of 96.8 and disappointed expectations of an increase to 97.2.

Opportunities

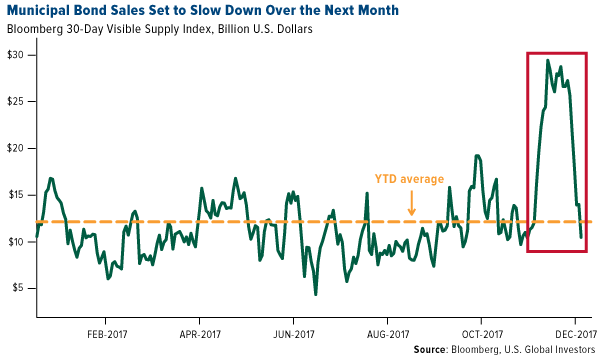

- The flood of new municipal-bond sales is receding after state and local governments raced to borrow before Congress could roll back subsidies. While $49 billion of securities have been sold so far this month, putting it on pace to potentially exceed the record of $54.7 billion set in December 1985, the volume of sales planned over the next 30 days slid to about $10.5 billion with Republicans’ tax-overhaul legislation locked up. Tighter supply could firm up the market.

- The largest tax overhaul since 1986 was signed into law today by President Donald J. Trump. The Tax Cuts and Jobs Act, which cleared both chambers of Congress on Wednesday, reduces the corporate tax rate to 21 percent from 35 percent and lowers the tax bill of most Americans.

- Municipal bond sales are expected to decline by about 20 percent in 2018, according to a survey by the Securities Industry and Financial Markets Association. Curtailed supply could help buoy prices amid a rising rate environment.

Threats

- Rich homeowners in blue states are among the biggest losers in the GOP tax bill as certain provisions are set to disproportionately affect homeowners in affluent parts of the U.S. The main changes affect the mortgage interest deduction and the SALT deduction.

- A Fed official who has been voting against rate hikes thinks he knows why wages aren't rising faster. Minneapolis Fed President Neel Kashkari worries the central bank's interest-rate hikes are actively contributing to a decline in U.S. inflation expectations that could make the Fed’s job harder in the next downturn. He also believes the job market is not as tight as the 4.1 percent unemployment rate suggests.

- A U.S. financial watchdog is warning investors about crypto “pump and dump” schemes. FINRA, the U.S. financial regulator, put out an alert on Thursday to warn investors.

Gold Market

This week spot gold closed at $1,274.55, up $19.10 per ounce, or 1.52 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 4.61 percent. The S&P/TSX Venture Index came in up 0.95 percent. The U.S. Trade-Weighted Dollar reversed course this week and fell 0.66 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-18 | Eurozone CPI Core YoY | 0.9% | 0.9% | 0.9% |

| Dec-19 | Housing Starts | 1250k | 1297k | 1256k |

| Dec-21 | GDP Annualized QoQ | 3.3% | 3.2% | 3.3% |

| Dec-21 | Initial Jobless Claims | 233k | 245k | 225k |

| Dec-22 | Durable Goods Orders | 2.0% | 1.3% | -0.8% |

| Dec-22 | New Homes Sales | 650k | 733k | 685k |

| Dec-27 | Conf. Board Consumer Confidence | 128.0 | -- | 129.5 |

| Dec-28 | Hong Kong Exports YoY | -- | -- | 6.7% |

| Dec-28 | Initial Jobless Claims | 240k | -- | 245k |

| Dec-29 | Germany CPI YoY | 1.5% | -- | 1.8% |

Strengths

- The best performing precious metal for the week was platinum, up 2.64 percent. For the second week in a row gold traders are bullish as the year comes to a close, according to Bloomberg’s survey of traders and analysts. Additionally, the yellow metal saw a second weekly advance as bond yields climb with slower trading around the holiday period. Prices are up 10 percent for the year in comparison to 8.1 percent in 2016.

- UBS strategist Joni Teves reports that gold is showing considerable resilience to the recent rise in U.S. real rates and more players view gold as a valid asset for diversification and a hedge against risk.

- Tibet Summit Resources and partner NextView Capital are set to purchase lithium producer Lithium X Energy for a premium price of $C265. This deal is one of many as Chinese companies are looking to secure raw materials for electric car batteries.

Weaknesses

- The worst performing precious metal for the week was gold, although up 1.52 percent. Gold is trading low compared to oil as expanding global economic growth increases fuel demand, reports Bloomberg. The world’s largest ETF backed by gold, SPDR Gold Shares, is seeing a fall in investors as it dropped to its lowest in three months with holders pulling around $1.14 billion in assets since the end of September.

- Platinum shorts reached an all-time high this week, further raising short-covering risks with net longs declining by 684.90koz, the largest weekly outflow on record. Both gold and silver positioning fell as well, reports UBS. Hedge funds are moving away from gold and into other equities as gold gains are far from the excitement of record-breaking U.S. equity indexes and cryptocurrencies. Joe Foster, who manages the VanEck International Investors Gold Fund says, “Nobody cares about gold right now.”

- Torex Gold faces labor issues as they suspended their Mexican employment contracts as competing labor unions fight for control of the employees of Torex. In response their target price was lowered to C$14 from C$25 by Coremark, reports Bloomberg.

Opportunities

- Bad news for bitcoin this week after its price plunged almost 30 percent today, down from its record high of $19k. Adding to the frenzy, digital currency exchange Coinbase had temporarily suspended all buying and selling for several hours. Lastly, the newly passed tax overhaul removed the tax break for investors in virtual currencies. New limits in the bill bar cryptocurrency owners from deferring capital gain taxes when trading one type of virtual currency to another, reports Bloomberg. This closes a grey area in the tax code on digital currencies.

- Two Federal Reserve governors expressed their doubts on the tax cuts actually spurring new investments and hiring. While president Trump has said that the fiscal overhaul will lead to higher growth, Minneapolis Fed President Neel Kashkari, among others, does not believe this will happen and said, “Very few CEOs that I’ve talked to in my district say that the tax package is going to lead to some dramatic change in their behavior.” The Peterson Institute believes that the new post-tax cost of research and development of large corporations reduces the incentive to develop new products relative to spending money on other activities as research and development will have to be amortized versus expensed, lowering the incentive for research.

- Measuring inflation has its critics. Typically, policymakers have to rely on monthly data releases of the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE). To try and measure core or underlying inflation, often times the most volatile components of inflation, like food and energy, are stripped from the data. New research published by the New York Fed Staff on their construction of an Underlying Inflation Gauge (UIG) is now getting some attention. Historically, inflation measures only relied on price measures. The UIG measure includes a wide range of nominal, real and financial variables in addition to prices, and focuses on the persistent common component of monthly inflation. The Fed Staff concluded that the UIG proved especially useful in detecting turning points in trend inflation and has shown higher forecast accuracy compared with core inflation measures. What is particularly interesting is that the Fed compiles two data series, UIG using just price data and UIG using the Full Data Set (FDS) they have researched. In the graph below we chart both series over the last five years and the results are eye popping. The UIG Index using just price data has compounded at an average annual rate of inflation of just 1.13 percent while the UIG Index using the Full Data Set has compounded at an average annual rate of inflation of 10.51 percent over the last five years. This could be a game changer as the UIG FDS has turned sharply up in recent years indicating a change in direction for inflation, and the government just added a stimulus package with meaningful shifts in the tax base.

Threats

- South Africa’s ruling party ANC adopted a resolution calling for land expropriation without compensation and its more hardline members have voiced support for mines and banks to be state-owned. While state ownership of the mines is unlikely, such policies are a disincentive for foreign capital to invest in the country.

- Private equities firms might have trouble exiting the subprime auto lending space as delinquencies are soaring toward crisis levels, writes Bloomberg. Buyout firms pushed billions into auto finance after the mortgage crisis to capitalize on the profits associated with high-interest loans.

- Jared Dillian, investment strategist at Mauldin Economics, writes that the South will rise again as the tax cut plan moves forward. States with an already high income tax that will no longer be able to write it off on their federal taxes, such as New York and California, and we will likely see residents and businesses moving to cheaper states such as Texas and Florida. Dillian predicts that over time New York City will lose its status as the intellectual and cultural capital of America and that the real estate market in California will suffer greatly.

Energy and Natural Resources Market

Strengths

- Lumber was the best performing major commodity this week rising 4.33 percent. The commodity rallied after U.S. housing data showed new home sales surged to the highest level since 2007. November new home sales rose 17.5 percent, well above expectations.

- The best performing sector this week was the S&P 1500 Oil & Gas Exploration and Production Index. The index rose 8.74 percent as WTI crude prices rose for the first week in four, and substantial bets were made by market participants purchasing long options of the sector.

- Daqo New Energy Corporation, a Chinese manufacturer of parts and cells used in solar power products, was the best performing stock in the broader resource market this week. The stock rallied 13.84 percent after Citic Securities analysts initiated coverage of the stock and suggested prices may rally 50 percent next year.

Weaknesses

- Steel prices dropped 1.22 percent; the most among major commodities. Finished long steel prices in Europe weakened in line with the seasonal fall in end-user demand in December, according to market participants.

- The worst performing sector this week was the Alerian MLP Index. The index was essentially flat for the week, significantly underperforming other energy related sectors as the passing of the Tax Plan means the tax-advantageous nature of MLP structures is less advantageous than it once was.

- The worst performing stock for the week was Weyerhaeuser Co. The integrated forest products company dropped 1.76 percent. The company is structured as a Real Estate Investment Trust that has advantageous tax rates, which are less advantageous after the passing of the Tax Plan.

Opportunities

- Oil headed for the first weekly advance in a month as U.S. crude stockpiles fell to the lowest level in more than two years and the pace of production gains slowed, Bloomberg reports. Crude stockpiles in the U.S. slid last week to 436.5 million barrels, the lowest level since October 2015, suggesting the market has begun a long-awaited rebalancing.

- Iron ore staged a Christmas rally as China mills appear to be buying volumes before the output curbs end. The metal’s futures rallied to the highest in three months, helping shares of BHP, the world’s largest mining company jump to a 2015 high, as steelmakers in China replenish stockpiles to prepare for a rebound in demand after a winter clampdown on output eases.

- Mining companies in Australia rose near a four-year high on Thursday, buoyed by an improving near-term outlook for commodity prices. Westpac, the Australian financial services corporation raised its near-term forecasts for prices across iron ore, metallurgical and thermal coal and oil this past week. “There is more to this picture than stronger than expected Chinese industrial activity. While important, another significant factor has been the overall strength in the global economy and, in particular, a surprising strong recovery in global trade,” Westpac analysts said.

Threats

- Copper snapped a seven-day rally in London as BNP Paribas says prices are set for a short-term decline. “The appreciation pace might have been too fast,” BNP Paribas analysts, including Gabriel Gersztein, said as bank shorts copper with an initial target of $6,300/ton, a 10 percent drop from current levels. BNP still expects an upward trend in the coming months and describes the short position as “tactical.”

- November durable goods new orders rose 1.3 percent, well below the 2.3 percent expected, as a transportation surge was offset by declines elsewhere. Outside of transport, there were declines for fabricated metals and machinery, which does not bode well for raw commodity demand.

- China’s Central Economic Work Conference triggered expectations of tighter monetary policy and cuts to risky lending in financial markets and the economy. The comments suggest the government is determined to deleverage financial markets and the economy, to cut down on risky lending behavior despite leading to a slowdown in economic growth, and points to further tightening of monetary policy, analysts said.

China Region

Strengths

- Hong Kong’s Hang Seng Composite Index climbed 2.64 percent for the week. Indonesia’s Jakarta Stock Exchange Composite Index and Thailand’s SET Index also performed reasonably well, with the Jakarta Composite rising 1.66 percent and the SET climbing 1.42 percent.

- Media reports this week stated that Chinese ride-hailing company Didi Chuxing raised more than $4 billion in its latest financing round, placing the firm’s valuation somewhere in the neighborhood of $56 billion.

- Fitch raised Indonesia’s credit rating one level to BBB, with a stable outlook, Bloomberg reports, putting the country on par with Portugal and the Philippines.

Weaknesses

- There has been no change to the pace for reviews of initial public offerings (IPOs) applications in China, according to the Asian nation’s securities regulator, reports Reuters. During the first 10 months of the year, the China Securities Regulatory Commission (CSRC) exceeded a record of approvals set in 2010. However, approvals have slowed significantly in recent weeks, with officials reiterating that capital markets should support the country’s strategic interests.

- Korea’s KOSPI Index declined 1.67 percent for the week. The bulk of the decline came Thursday as tech and index heavyweight Samsung fell following analysts’ revisions.

- The Chinese government has reportedly “softened” its focus on cutting debt as it seeks faster growth, according to the Wall Street Journal. One government official is quoted as saying that “it’s not realistic to reduce leverage when the whole economy relies on banks for financing.” Financial institutions, from the International Monetary Fund (IMF) to the World Bank, have urged Beijing to reduce its reliance on debt.

Opportunities

- In keeping with the tone of the recent Party Congress and the formal incorporation of “Xi Jinping Thought” into the CCP’s doctrine, Chinese authorities this week announced new criteria to measure the economy. Bloomberg cited People’s Daily as mentioning innovation, new momentum in economic growth, efficiency, product quality and utilization of social resources. The idea, in keeping with Xi Jinping Thought and the recent roadmap to 2050, is a shift toward higher quality production and the increasing modernization of China’s economy.

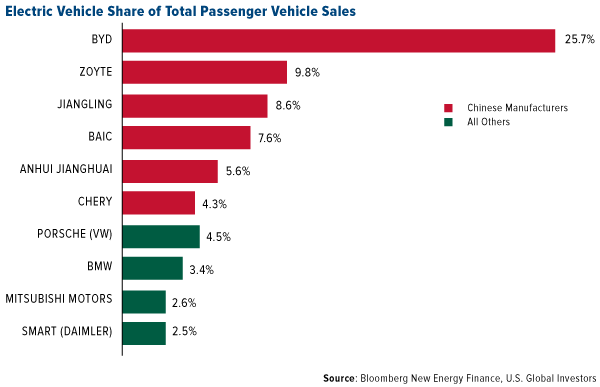

- Chinese carmakers still lead in terms of the percentage of electric vehicles they sell, though the Europeans and Japanese are catching up, Bloomberg New Energy Finance data show. The gap should begin to close in 2019/20 as China allows more foreign competition and global brands boost the number of EV models they offer.

- U.S. coal exporters may stand to benefit from China’s fuel shortage this year, Bloomberg reports. Chinese authorities have eased limits on overseas purchases to ensure it has enough supply for heating homes and businesses this winter. The article notes that Australian and Indonesian coal exporters may similarly stand to benefit.

Threats

- The European Union introduced new rules to guard against excessively cheap imports, specifically singling out China as a distorted, state-run economy, reports Reuters. On Thursday, China’s foreign ministry criticized what it called the “thoughtless remarks” about the country’s economic development, and said the EU had “fabricated excuses” and was hypocritical in its report.

- Breaking with recent U.S. convention, President Donald Trump is now portraying China as a rival that wants to undermine American prosperity. On Monday, the White House lumped China with Russia as powers seeking to “challenge American power, influence, and interests,” reports Bloomberg.

- As part of a government campaign to slow the pace of overseas takeovers, which set a record in 2016 and led to a surge in capital outflows, local Chinese regulators have stepped up scrutiny of the country’s most prolific dealmakers, reports Bloomberg Businessweek. One of these dealmakers is HNA Group, once a little-known airline operator that has now taken on billions of dollars in debt as it made more than $40 billion of acquisitions over six continents since the start of 2016, the article continues.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 4.7 percent. Optimism for the successful conclusion of the ongoing third review of the bailout program is pushing Greek equities higher. Banks are leading gains on the Athens Stock Exchange.

- The Hungarian forint was the best performing currency this week, gaining 1.7 percent against the U.S. dollar. Economic sentiment and business confidence spiked to new record-high levels this week. The National Bank of Hungary revised up next year’s economic expansion to 3.9 percent from 3.7 percent.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 1.9 percent. Real wages are growing at 5.4 percent year-over-year, but the faster-than-expected growth in real wages is not improving disposable income growth, and the gap between the two is widening. Retail sales and industrial production surprised on the downside in November as well. Russian equites usually follow the price of Brent crude oil, but oil gained 3 percent in the past five days while stocks trading on the Moscow Stock Exchange lost 1.9 percent.

- The Czech koruna was the worst relative performing currency this week, gaining 65 basis points against the U.S. dollar. Central Bank of the Czech Republic left its key rate unchanged at 50 basis points after inflation slowed. More hikes are expected next year.

- The utility sector was the worst performing sector among eastern European markets this week.

Opportunities

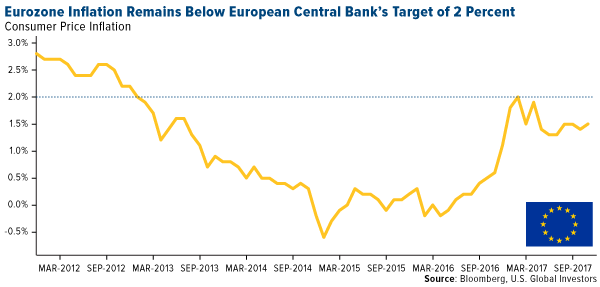

- Annual eurozone inflation edged up to 1.5 percent last month, up slightly from October’s figure of 1.4 percent. Inflation remains below the European Central Bank’s (ECB’s) target level of 2 percent, and once again, this week the ECB restated its prior announcement that the bank will keep buying assets until inflation shows sustainable pick-up. A longer bond-buying program will keep rates low and stimulate further growth in the euro area.

- Russian companies are set to reach $2.8 billion in initial public offerings in Moscow and London this year, the most since 2011. Despite the U.S. toughening sanctions against Russia, an oil recovery, monetary easing and a rally in emerging markets, this year set the stage for new equity placements. Considering the relatively stable oil price and absence of new geopolitical shock, the trend will likely continue next year, according to Vladimir Vedeneev, chief investment officer at Raiffeisen Capital Asset Management in Moscow.

- Greece retuned to the bond market in the summer and yields on 10-year government bonds continue to decline, boosting investors’ confidence. Standard & Poor’s Rating Agency may upgrade Greece by two notches to B+ from B- on January 19, while Fitch may follow with an upgrade to B+ on February 16, according to Wood & Company.

Threats

- On Wednesday, the European Union said that the Polish government poses a threat to rule of law and recommended triggering Article 7 against Poland that could lead to sanctions, including stripping Poland of voting rights. The probability of sanctions is low, as all members need to vote in favorite of it, and Hungary declared its support for Poland. Therefore, triggering Article 7 against Poland likely won’t lead to sanctions, but it will sour the country’s relationship with Brussels.

- Austria’s new coalition government was sworn in by the President this week. The conservative, center-right People’s Party led by Sebastian Kurz, will govern with the anti-immigration, far-right Freedom Party. Austria is now the only western European country with a far-right party in government. The new Austrian government program includes pledges to stop illegal immigration and to cut taxes. It also opposes further EU political and economic integration.

- In Catalonia, separatist parties retained their majority in the regional parliament, which was a setback for Spain’s efforts to contain the push for independence. The results of the new elections open a new chapter in the conflict between leaders of Catalonia’s independence movement and Spain. Catalonia is an important state of Spain, contributing around one-fifth of the country’s economic output.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits