Best of the Year: Top 5 Frank Talk Posts of 2017

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefitss

As we head into the New Year, I want to share with you the five most popular Frank Talk posts of 2017. One common theme you’ll see in these posts is they all center on the topic of gold. Although we specialize in educating investors about gold and managing gold funds, it’s worth noting that our gold posts garnered more interest than our bitcoin and blockchain posts in this year of cryptocurrency craze.

Cryptocurrencies hogged the spotlight in 2017, and some might say this attention drove investors away from traditional assets such as gold; however, I disagree, as I believe gold and bitcoin serve different purposes. While many might think gold underperformed in 2017, it’s actually on track to finish the year strong. The precious metal ended the year up approximately 13 percent.

2017 In Review: The Top 5 Posts

1. 5 Things You Need to Know from last Week (Look What Gold Just Did!)

The last week of May was particularly bullish for gold after a “golden cross”—the 50-day moving average climbing above the 200-day moving average—occurred for the first time in over a year. A report released that same week from the Wall Street Journal confirmed my suspicion that Wall Street is run by quantitative analysts, or quants, whereby traders and fund managers make their instincts based on oceans of data rather than gut instinct. Other highlights from the week included the U.S. bouncing back as the top wheat producer and bitcoin trading around $2,700, double that of an ounce of gold. (By the end of this year, bitcoin, of course, hit a peak of over $19,000 then lost 30 percent of its value shortly thereafter.)

click to enlarge

click to enlarge2. “Mother of All Bubbles” Keeps Gold in Focus

While many write of the potential bubble of bitcoin, I wrote earlier this year of the “mother of all bubbles”: total global debt. Global debt levels are rising each year with the U.S. alone adding $3 trillion every year to the pension deficit. People are living longer while near-zero interest rates are encouraging heavy levels of borrowing. In preparation for a possible burst, investors might consider placing some of their wealth in a hard asset such as gold.

click to enlarge

click to enlarge3. Gold Gets a Shot in the Arm from Inflation and China

In January we saw a rate hike of 0.25 percent and the gold market responded favorably after the Federal Reserve took a dovish tone regarding future rate hikes. Gold has historically been an attractive hedge against inflation. The bull market, currently in its eighth year, is facing some significant geopolitical and macroeconomic uncertainty, and we could be getting late in the economic cycle. For the 10-year period, the yellow metal has shown an inverse correlation to risk assets such as stocks and high-yield bonds.

With China and India set to become the two largest economies by 2050 and already the top two gold consuming nations, we expect to see demand rise greatly for gold. Historically, when incomes rise in China and India, demand also rises for the yellow metal.

click to enlarge

click to enlarge4. Gold Was Chemically Destined to Be Money All Along

Mid-year I brushed up on my knowledge of gold’s chemical properties. Gold is unlike any other metal, and the fact that it’s so chemically “boring” is one of the many reasons why it’s so highly valued, even today. The precious yellow metal beats out all other metals and leaves silver in second place to be the best possible candidate for a currency of any value.

click to enlarge

click to enlargeIn a time of rising global debt and currencies free-floating, I believe gold will remain a strong asset class for storing wealth and hedging against inflation. Early this year, former Fed Chairman Alan Greenspan told the World Gold Council he views gold as the primary global currency. At U.S. Global Investors, we continue our long-standing recommendation to give the metal a 10 percent weighting—5 percent in physical gold and the other 5 percent in high-quality gold stocks, mutual funds and ETFs.

5. The World is Running out of Gold Mines—here’s How Investors Can Play It

In response to lower gold prices, explorers have had to slash their exploration budgets resulting in fewer large mines being discovered. Last year marked the fourth consecutive year of falling exploration budgets and an 11-year low.

click to enlarge

click to enlargeSince all the “low hanging fruit” gold mines have likely already been discovered, explorers now have to dig deeper and venture farther into more extreme environments to find economically viable deposits. This increases the cost of exploration and ultimately production. As costs are rising, many senior gold producers are instead acquiring smaller firms with proven, profitable projects rather than exploring themselves. Investors can use this to their advantage by investing in junior gold companies that look like targets for takeover.

2017 is the eighth year of the S&P 500 Index bull-run, closing at multiple all-time highs this year alone! Test your knowledge of the index’s history or check out other interactive favorites from our Investor Library.

To all of our readers around the world, I wish you robust health, buckets of wealth and tons of happiness in the New Year!

Index Summary

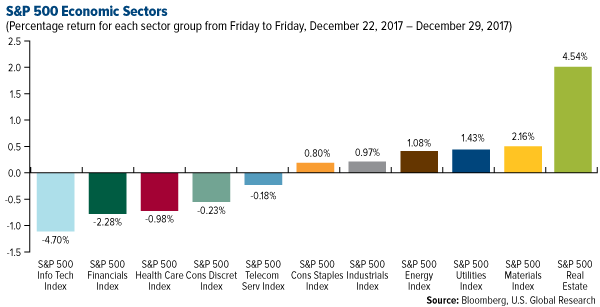

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.14 percent. The S&P 500 Stock Index fell 0.36 percent, while the Nasdaq Composite fell 0.81 percent. The Russell 2000 small capitalization index lost 0.48 percent this week.

- The Hang Seng Composite gained 1.33 percent this week; while Taiwan was up 1.00 percent and the KOSPI rose 1.10 percent.

- The 10-year Treasury bond yield fell 7.6 basis points to 2.406 percent.

Domestic Equity Market

Strengths

- For the first time ever in its nearly 90-year history, the S&P 500 Index had a “perfect” year. The index of large-cap companies ended positively every month of the year, propelled by the promise of corporate tax cuts and strong earnings growth.

- The majority of jobless rates across the world are in decline. Japan, Hong Kong, the U.S., Israel, the U.K. and Portugal, among other countries, registered 15-year lows.

- The U.S. once had the highest corporate tax rates among G7 countries, but thanks to the new tax bill, our country is now the fourth highest behind France, Italy and Japan.

Weaknesses

- The Atlantic hurricane season will most likely be one of the costliest in history with 17 storms in total. The final numbers have yet to be released, but apparently three of the storms are said to be in the top 10 most costly over the past 45 years.

- The race to finance issuance of corporate debt rose nearly five percent to $2.25 trillion, breaking records two years in a row. What’s more, the student loan market has now exceeded the size of the U.S. high-yield corporate market.

- The Fort Worth-based oil and gas operator Range Resources was the worst performer in the S&P 500 Index this year. The energy sector was mostly unloved among investors this year, and the natural gas industry in particular was least-loved. However, Seth Williams, the top trader at Tudor Pickering in Houston, recently noted that Range Resources was his top pick for the first quarter of 2018.

Opportunities

- Jeff Bezos bumped Bill Gates out of the number one spot for the world’s richest man. Could it be this greed that prompted record flow of money into startups? This year we witnessed $141.3 billion flow into what investors hope to be the “next” Amazon or Microsoft.

- The “fear index”—investors’ favored tool to measure stock market volatility and sometimes used as a leading indicator for market direction—traded at an all-time low in early November, indicating good times may linger for some time in the future.

- The green movement is upon us. Participation of global corporations within the “sustainability projects” domain increased markedly nearly doubling over the past two years.

Threats

- If the Federal Reserve continues with its anticipated rate hikes and the long end of the curve (30-year yields) fails to lift, we could see yield inversions, which would most likely become a drag on the economy.

- According to current polling numbers, the GOP could lose the House and/or the Senate in 2018. If so, increased investor uncertainty could reemerge.

- Will the North America Free Trade Agreement (NAFTA) get renegotiated or collapse altogether? The Trump administration is pushing to get talks wrapped up by the end of the first quarter, but there are still some major issues outstanding.

The Economy and Bond Market

Strengths

- U.S. home prices, as measured by the S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, appreciated 6.2 percent year-over-year in October, making it the best 12-month period since the summer of 2014. The price action was driven by low inventories and increasing sales, according to a S&P Dow Jones Indices spokesperson.

- American consumers showered retailers with some holiday cheer, with Christmas sales rising at their fastest pace since 2011. Spending was up nearly 5 percent year-over-year from November 1 through Christmas Eve, compared with a 3.7 percent gain during the same period last year, according to Mastercard data.

- Pending homes sales rose modestly in November, up 0.2 percent month-over-month from October. “The housing market is closing the year on a stronger note than earlier this summer, backed by solid job creation and an economy that has kicked into a higher gear,” commented Lawrence Yun, chief economist of the National Association of Realtors.

Weaknesses

- Consumer confidence in December slipped from its 17-year high in November. The Conference Board’s Consumer Confidence Index fell to 122.1, down 6.5 points from 128.6. Although the index remains at historically high levels, the decline was much steeper than economists had anticipated.

- Personal income in the U.S. rose only 0.3 percent month-over-month in November, somewhat below the expected 0.4 percent. The October report was also revised down to 0.2 percent from the initial 0.4 percent.

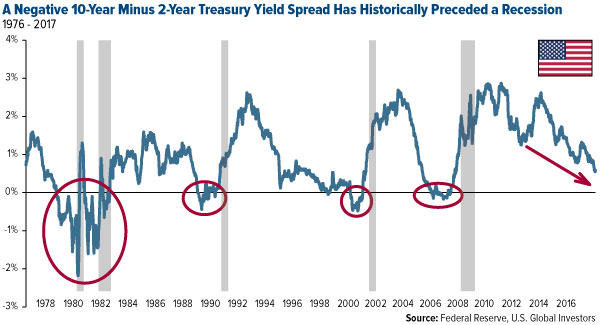

- The Treasury yield curve continued to flatten this week, with the 10-year minus 2-year Treasury yield spread falling to a slim 52 basis points on Thursday. The yield curve is often seen as a reliable predictor of U.S. recessions, as the past seven recessions were preceded by an inverse yield curve, when the shorter-term Treasury yields are more than the longer-term Treasury.

Opportunities

- The tax reform bill signed into law last week could help encourage U.S. multinational corporations to repatriate as much as $400 billion early next year, according to an estimate cited by the Wall Street Journal. The estimate is based partly on historical precedent, as President George W. Bush’s 2004 tax-repatriation holiday prompted companies to bring home $312 billion being held overseas.

- On a related note, many Wall Street economists are revising up their U.S. economic growth forecasts for 2018 and 2019 as a result of President Trump’s tax overhaul. Goldman Sachs, for one, lifted its 2018 and 2019 growth forecasts up 0.3 percentage point and 0.2 percentage point, respectively, to 2.6 percent and 1.7 percent.

- With tax reform out of the way, House Speaker Paul Ryan hopes to tackle entitlement reform next in 2018, saying he will focus on “getting people from welfare to work” and “making sure people get the skills they need to get the jobs they want.” The legislative agenda could be complicated, however, as Senate Majority Leader Mitch McConnell believes entitlement reform is a non-starter without broad bipartisan support from Democrats.

Threats

- According to an alarming new report by the American Legislative Exchange Council (ALEC), unfunded pensions and other liabilities across all 50 states now exceed $6 trillion, amounting to $18,676 per U.S. resident. California leads all other states with nearly $1 trillion in unfunded obligations, followed by Texas ($397 billion) and Illinois ($388 billion). On a per-capita basis, Alaska ranks first at $42,992. The long-term ramifications of this trend “could be far deeper and prolonged than the Great Recession,” warn the report’s authors.

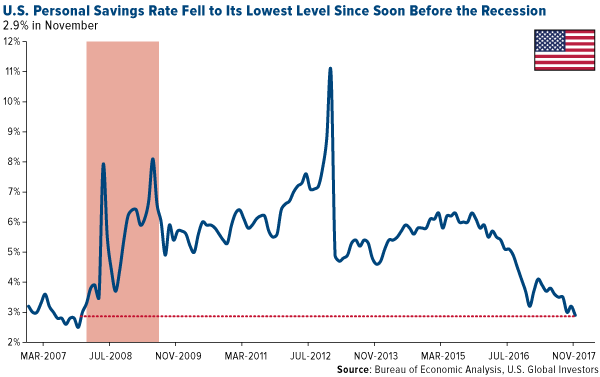

- In November, Americans’ personal savings rate fell to 2.9 percent, its lowest reading since soon before the recession. This comes as Americans rely more and more on credit cards to make transactions. According to the just-released Federal Reserve Payments Study, credit card payments grew from 103.5 billion in 2015 to 111.1 billion in 2016, with the value surging from $5.65 trillion to almost $6 trillion.

- With U.S. corporate taxes set to fall from 35 percent to 21 percent, many worry businesses will be less incentivized to put money in tax-exempt municipal bonds. As of the third quarter of 2017, banks and insurance firms held almost 30 percent of the $3.8 trillion muni bond market, according to Fed data. These large investors could potentially be less interested in seeking exemption from substantially lower business taxes and turn to higher yielding assets.

Gold Market

This week spot gold closed at $1,303.05 up $27.80 per ounce, or 2.18 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by just 1.68 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index jumped 4.99 percent. The U.S. Trade-Weighted Dollar reversed course this week and slumped 1.12 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-27 | Conf. Board Consumer Confidence | 128.0 | 122.1 | 128.6 |

| Dec-28 | Hong Kong Exports YoY | 6.0% | 7.8% | 6.7% |

| Dec-28 | Initial Jobless Claims | 240k | 245k | 245k |

| Dec-29 | Germany CPI YoY | 1.5% | 1.7% | 1.8% |

| Jan-1 | Caixin China PMI Mfg | 50.7 | -- | 50.8 |

| Jan-3 | ISM Manufacturing | 58.2 | -- | 58.2 |

| Jan-4 | ADP Employment Change | 190k | -- | 190k |

| Jan-4 | Initial Jobless Claims | 248k | -- | 245k |

| Jan-5 | Eurozone CPI Core YoY | 1.0% | -- | 0.9% |

| Jan-5 | Change in Nonfarm Payrolls | 188k | -- | 228k |

| Jan-5 | Durable Goods Orders | -- | -- | 1.3% |

Strengths

- In the final week of the year, the Bloomberg survey of analysts and traders showed the majority of respondents are bullish on the gold price for a third straight week. The yellow metal will end 2017 on a strong note closing out the year with a 13.09 percent gain for spot prices, while the U.S. dollar will see its worst year in more than a decade. Silver was the best performing metal for the week, up 3.33 percent as it typically is more volatile than gold.

- Gold is living up to its reputation as a stable and liquid asset in contrast to bitcoin, which dropped as much as 30 percent in one day. Bitcoin fell on Thursday to less than $14,000 as South Korea weighs options of shutting down some cryptocurrency exchanges amid a frenzy of speculation.

- U.S. consumer confidence fell off a 17-year high this month to 122.1 from 128.6, further than the expectation of 128.0. Consumers showed greater positivity toward present conditions and were mixed on the state of the labor market. Lower confidence could move some investors back toward gold.

Weaknesses

- The VanEck Vectors Gold Miners ETF, one of the largest such funds, saw two massive outflows of assets. On Tuesday after Christmas, investors withdrew $222.4 million from the fund, then two days later another $203.1 million was withdrawn, reducing the fund’s assets to $7.6 billion. These redemptions are likely the culprit behind the poor performance of the senior gold stocks when gold bullion was moving up strongly throughout the week. Platinum was the lagging precious metals for the week with a gain of just 1.25 percent.

- Taxpayers in high-income tax states, such as New York and New Jersey, are rushing to prepay their 2018 taxes and avoid the newly imposed cap on state and local tax deductions. Meanwhile, banks are facilitating this process by offering loans for taxpayers willing to go into debt to prepay taxes rather than miss out on the deduction.

- Centerra Gold processing operations at its Mount Milligan mine in British Columbia has been temporarily suspended due to a lack of sufficient water resources and will likely be back to full capacity by April 2018, reports Bloomberg. Consequently Royal Gold, which owns a royalty on Centerra Gold, has been downgraded from hold to buy and the target price reduced from $109 to $99.

Opportunities

- Klondex Mines announced the first open pit resource of 2.2 million ounces of Indicated and Inferred at a 1.04 gram per tonne gold equivalent grade at their Fire Creek Mine in Nevada. Klondex is following up on a series of repeating geophysical anomalies and this resource is just the first one that enough drilling data has been collected to calculate a resource. To the north of the Fire Creek land package, Newmont Mining has successfully mined similar open pit structures on its land package. While Klondex stressed it is going to remain focused on its high-grade underground operations, it would consider bringing in a partner to advance what could be a series of bulk tonnage open pits. This is extremely exciting for Klondex as gold production from the open pits would significantly extend the observable mine life of the Fire Creek Mine land package. In contrast, underground operations cannot economically drill out enough resources from underground to show a long mine life, even though historically underground mines continue mining for decades into the future with mine lives of even just three years of ore in the reserve category.

- With demand for electric cars on the rise, Argentina is looking for workers to extract lithium from its large reserves. Although Argentina currently supplies 16 percent of the lithium market, it lacks enough skilled workers to export more and supply a desired 45 percent of the market. Thus lithium markets may remain tight as China extended its tax rebate on the purchases of hybrid and electric cars into 2020 after it was supposed to expire at the end of 2017. Demand for lithium should remain strong in the near-term.

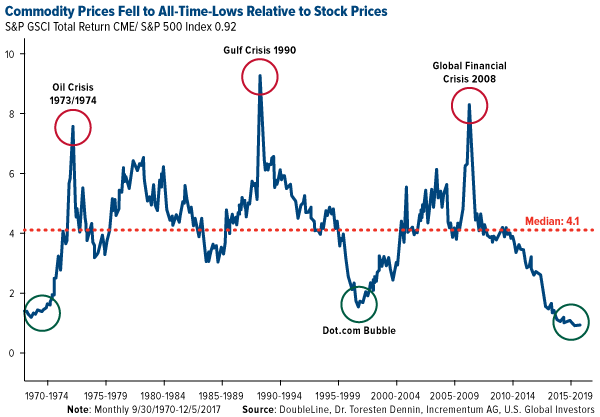

- Many believe a commodity comeback is in the works as the S&P GSCI Total Return Index is at a record-low valuation relative to the benchmark S&P 500 Index for stocks. Shawn Hackett of Hackett Financial Advisors notes that in 2008 stocks were screaming to be bought on this valuation metric, and that was proven correct. The opposite condition is now in place and commodities are the asset class screaming to be bought at the expense of stocks.

Threats

- Effective at the start of 2018, the United Arab Emirates (UAE) will impose a 5 percent value-added tax (VAT) on gold jewelry imports, potentially hurting the Indian export market. This past week Dubai as seen somewhat of a “gold rush” of buying up jewelry before the tax is imposed. There will be no import tax on 24 carat gold bars, leaving room for possibility of the UAE manufacturing its own gold jewelry.

- Personal spending was up 0.4 percent with income only up 0.3 percent as the personal savings rate fell to 2.9 percent, the lowest since 2007. This data suggests that U.S. growth is either at the expense of increased debt or reduced savings, and thereby at the expense of the balance sheet, writes Macro Strategy Partnership, hence economic conditions may not be a rosy as the consensus is trying to sell.

- Quantitative easing (QE) by the Federal Reserve is over. Now we are executing the quantitative tightening (QT) phase of reversing this policy which will accelerate in 2018, effectively reducing M2 money supply by 1.73 percent or the equivalent of a 30 basis point rate hike. Macro Strategy Partnership notes that by the second quarter of 2018, QT will be equivalent to 2.6 percent of U.S. M2 and by the third quarter 3.5 percent. With tax cuts starting to kick next year and Fed borrowing expected to climb, uncertainty over the direction of interest rates will be significant.

Energy and Natural Resources Market

Strengths

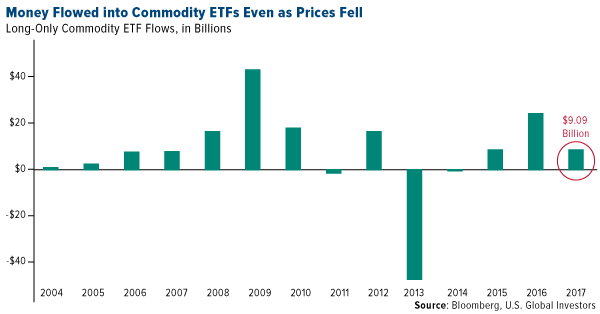

- Commodities posted a third consecutive year of inflows in 2017 as global growth accelerates. Exchange traded funds linked to raw materials attracted $9 billion dollars, capping a third straight annual inflow, the longest since 2010. Goldman Sachs analysts said the outlook is brighter over the next year, as they predict the sector will post a 7.5 percent return.

- Lumber was the best performing major commodity for the year 2017, rising 41.7 percent. The commodity rallied strongly on the back of three compounding factors. The strength of the global economy was reflected in increased softwood lumber import demand from China and Europe. Similarly, demand in the U.S. also increased as home sales rose to near records, and the country faced severe destruction from hurricanes and thunderstorms. Supply, on the other hand, was partially challenged by a U.S. trade dispute with Canada, whose production was slapped with additional import taxes that exporters passed to consumers directly, taking advantage of a tight demand and supply imbalance.

- The best performing sector the year 2017 was the FTSE 350 Mining Index. The index of diversified major metals producers rose 26.5 percent tracking a 30-plus percent rally in copper prices. The metal rose to its highest in more than three years as global inventories appeared to decline, while Chinese officials stepped up pollution-fighting efforts by forbidding certain imports and temporarily halting processing plants.

Weaknesses

- The Bloomberg Commodity Index, a measure of a basket of commodities, ended the year down 0.8 percent, dragged lower by agricultural commodities, which lagged the spike in industrial and precious metals. Corn production hit all-time highs in numerous high-production countries, resulting in increased global inventories, and depressed crop values.

- Iron ore prices dropped 25.2 percent; the most among major commodities in 2017. The metal posted a sizeable drop despite continued and synchronized global manufacturing growth. Australian exports of the raw commodity grew in 2017, resulting in sizeable growth of iron ore port inventories in China. China, on the other hand, opted to alleviate excessive pollution in its major cities, forcing the early closure of numerous polluting steel mills, resulting in weaker than expected demand for the critical steel-making raw material.

- The worst performing sector for the year 2017 was the S&P 1500 Oil & Gas Equipment and Services Index. The index dropped 15.5 percent, dragging lower the global energy complex, as negative earning’s revisions and more conservative outlook for 2018 drilling campaigns weighed heavily on the sector. The modest increases in oil prices for 2018 did not result in the anticipated expansion of drilling rigs and associated services that usually provide a boost for the sector when prices rally.

Opportunities

- A major and extended 10-year bull market run in commodity prices may in the cards, beginning in 2018, says Shawn Hackett, president of Hackett Financial Advisors. The Standard & Poor’s GSCI Total Return Index, which tracks 24 raw materials, is hovering near a record low valuation relative to the S&P 500 Index. According to Hackett, stocks were a screaming buy at the end of 2008 based on the same metric; this time the inverse is true, and the same metric is flashing a screaming buy for raw materials.

- Oil prices rose to their highest since 2015 after OPEC extended its production curbs into 2018, U.S. crude inventories continued to drop, even after the seasonal destocking period ended, and Saudi fiscal authorities revealed they expect prices to rise to $75 per barrel over the next five years.

- Precious metals prices are rallying as the U.S. dollar extends its loss. Gold is posting its best rally since October as macro-analysts suggest the U.S. may see higher than expected inflation in 2018 as a result of the enactment of the tax plan, and see the potential for a major infrastructure plan funded using fiscal stimulus.

Threats

- Hopes of a spring bounce in Chinese commodity demand are becoming less clear, reports Bloomberg. China growth and commodities bulls aren’t hearing what they want from some members of the macro-elite in Beijing, with two People’s Bank of China members and a party official talking down expectations for GDP growth. Fears of overleveraging, municipal bankruptcies, and advocating for slower growth to ease debt and environmental burdens, are the reasons cited by the aforementioned macro-elite members.

- China’s commitment to renewable energy, pollution control, and environmental policy has weakened the dependence of the world’s largest consumer of commodities from raw materials producers. At the forefront of China’s environmental push are electric vehicles. The Asian nation will extend a tax rebate on purchases of these vehicles until the end of 2020, away from the traditional internal combustion engine. Similarly, policy-makers have shunned polluting steel mills and forced early closures, while imports of lower quality raw copper have also been suspended.

- The restoring of pipeline capacity which caused supply disruptions over the past three weeks poses a challenge to the recent crude oil rally. The Forties pipeline in the U.K., is nearing full service following an unexpected shutdown. Similarly, the explosion at a Lybian pipeline earlier this week, which affected nearly 1 million barrels a day of production, is expected to be restored to full capacity in the next week.

China Region

Strengths

- The top performing region for the year is the Vietnam Stock Index, which incorporates all of the companies listed on the Ho Chi Minh City Stock Exchange. During this week alone, the index moved in a positive direction as large-cap stocks were boosted by expectations for better quarterly earnings, along with rising oil prices.

- This year, China’s domestic stocks “won a significant seal of approval from MSCI, Inc., the world’s biggest index complier,” writes Bloomberg, as the Asian nation’s stocks were added to the benchmark indices. In addition to the admission of some large caps, which will take place in 2018, this gave China a stamp of credibility and opened it up to a segment of investors that may have had little exposure to the world’s second-biggest economy, the article continues.

- China’s GDP throughout 2017 has shown strength, advancing 6.8 percent year-on-year in the third quarter, following 6.9 percent growth in the previous two periods. Despite this being the weakest pace of expansion since the fourth quarter of 2016, it still matched market consensus. According to Trading Economics, for 2017, the Chinese government expects the economy to grow by around 6.5 percent.

Weaknesses

- The worst performing region for the year is the Shanghai Stock Exchange. According to the Economic Times, Shanghai stocks suffered their biggest loss in two weeks as we approach year-end, amid signs of slowing economic growth as well as year-end liquidity tightness.

- Over the past three years, China has shut down more than 13,000 websites and nearly 10 million accounts have also been closed by websites, reports Reuters. The government has stepped up controls over the Internet since President Xi Jinping took power over five years ago. Although critics say this is an effort to restrict freedom of speech and prevent criticism of the ruling Communist Party, the articles goes on to explain that more than 90 percent of people surveyed support government efforts to manage the Internet.

- Steel mills in 28 Chinese cities have been cutting production for mid-November and mid-March as the government pledged to cut air pollution, reports Reuters, with some construction and transportation restricted as well, a move that also dented demand. Steel demand tapered off toward the end of 2017 as cold weather interrupted construction activities and steel mills are reluctant to restock raw materials as they are still curbing output, the article continues.

Opportunities

- Not only has President Xi Jinping’s push for both pollution control and reduced dependence on imported oil allowed China to become a leader in the electric vehicle market, there could be a side benefit for its automotive industry too, writes Bloomberg. “Environmental regulations and production incentives could hasten the development of a high-volume leader in electric vehicles that might finally give China a shot at a world-class auto brand,” the article reads.

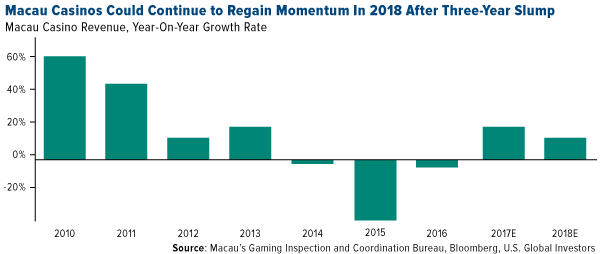

- More than two years ago Macau, the world’s largest gambling hub, saw soaring profits until a Chinese government corruption crackdown drove away wealthy high-rollers, reports Bloomberg. But now, some analysts estimate the Macau industry’s earnings could again start approaching records next year before hitting a new peak in 2019, the article continues. The biggest driver is expected to be VIP gamers.

- A report by the Centre for Economics and Business Research in London shows the growing importance of Asia’s major economies into 2018 and beyond, reports Bloomberg. According to a league table in the report, the region is shown dominating in terms of size in just over a decade, with China overtaking the U.S. economy by 2030.

Threats

- North Korea’s leader Kim Jong Un caused a stir on several occasions this year, most notably with more than a dozen missile tests throughout 2017. U.S. President Donald Trump has expressed “exasperation at the regime’s pursuit of nuclear weapons in the face of global sanctions and condemnation,” Bloomberg writes. It would be no surprise if the tension continued or intensified in 2018.

- Australia’s former Prime Minister Kevin Rudd, who is now the president of the Asia Society Policy Institute in New York, expressed his views recently on the Trump administration’s policy on North Korea. According to the South China Morning Post, Rudd said “The President of the United States is the greatest source of instability across the Asia Pacific region because no one knows which way he’s going to jump.”

- According to the National Bureau of Statistics, China’s transition to an economy driven by consumption, rather than by investment, is complete. However, according to an article from the Nikkei Asian Review, this new consumption-driven economy might not be what it seems. To understand what is happening in the Asian nation, the article explains that we must understand and note the distinction between “average” and “median” household incomes, because with that in mind, it appears only the rich are spending more, and the “investment addiction persists.”

Emerging Europe

Strengths

- Turkey was the best performing country this year, gaining 47.6 percent. After the failed coup attempt in July of 2016, the government implemented a slew of fiscal and monetary measures in order to stimulate the economy, supporting equities. Toward the end of this year, the economy started to show signs of overheating with GDP reaching 7 percent in the third quarter and headline inflation higher by about 300 basis points from 8.5 percent at the end of 2016. The lira depreciated against the U.S. dollar further by 7 percent in 2017.

- The Czech Koruna was the best performing currency this year, gaining 20.7 percent against the U.S. dollar. The Central Bank of the Czech Republic removed the cap on the koruna after more than three years, and as the first country in Europe to do so, started to increase its interest rates.

- The industrial sector was the best performer among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this year, losing 5.5 percent. After Donald Trump won the presidential election at the end of 2016, investors were hoping for a removal of sanctions imposed on Russia for the annexation of Crimea as well as an improved relationship between the two countries. However, even tougher sanctions are now expected to be announced next month for Russia meddling in the 2016 U.S. presidential elections. Russian equites usually trade in a tight range with the price of Brent crude oil, but as the chart below shows, the two were disconnected at the beginning of 2017 and toward the end on the year.

- The Turkish lira was the worst performing currency this year, losing 7 percent against the U.S. dollar. In April, Turkey approved the presidential system giving more power to the President. Throughout the year, Erdogan was pressing the government and central bank to boost economic activity overlooking the country’s depreciating currency on a worsening political relationship between the United States and the eurozone.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

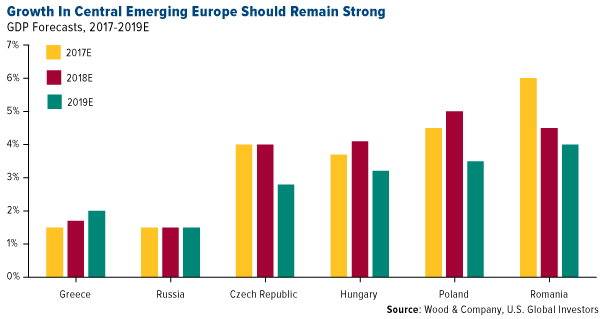

- Wood & Company expects next year’s growth in central emerging Europe to remain strong. The research group has a positive stance toward emerging market equites; however, given the strong performance of the stock market in 2017, the group prefers to be selective. Poland, Hungary and Romania are the preferred markets aimed at the strong expansion momentum and moderate valuations. Wood & Company also take a more positive stance on Greece given the ongoing economic recovery, at the same time warning that the volatility will persist. They are cautiously positive on Russia, expecting continued monetary easing via further rate cuts.

- Goldman Sachs expects the Russian oil sector’s dividends to rise 20 percent in 2018, while the other large global oil companies are expected to maintain flat dividends. Higher oil prices and lower capital spending should boost Russian oil’s free cash flow by 50 percent in 2018, allowing companies to increase their dividend payouts.

- Central emerging Europe may benefit from Brexit as companies will be relocating their businesses ahead of the UK’s departure from the eurozone. Some companies already announced plans to relocate their businesses to Poland and Hungary as Central emerging Europe has a highly educated workforce with growing wages, although still well below Western labor costs.

Threats

- After elections in Germany, France and the UK this year, Italy will hold general elections on March 4. The parliament’s current five-year term runs out in May. Recent polls and local election results suggest that Italy’s Northern League, and anti-EU and anti-immigration party, has a chance at governing in a coalition with the center-right Forza Italia party. Italy is the fourth-largest economy in Europe, and next government will have to work on reducing debt, improving banking system and breaking out of stagnation.

- Russia was the worst performing market this year, and next year could be volatile for Russian equities. Broader sanctions might be introduced on Russia in 2018 as part of the U.S. bill signed into law in August of 2017. The new sanctions could include restrictions on investment in Russia’s sovereign debt and an extension of the sanctioned individual’s list. In March, Russia will hold presidential elections. It is widely expected that Vladimir Putin, who has been actively serving the country since the end of 1999, will win again. However, investors need to wait and see what new social-economic program will be implemented for the next six-year presidential term.

- In 2017, the Czech Republic hiked its main rate twice. The first rate increase of 25 basis points took place in August and another 25 basis points hike followed in November. Next year more central emerging Europe countries may start hiking rates as inflation recovers and economic growth strengthens.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits