It’s Time for the Fear Trade to Move Gold Prices

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

The price of gold and gold mining stocks were very competitive in 2017. The yellow metal ended the year up a little more than 13 percent—its best year since 2010—while gold stocks, as measured by the NYSE Arca Gold Miners Index, gained more than 11 percent. All of this occurred even as large-cap stocks regularly closed at all-time highs and cryptocurrencies invited massive speculation.

We can thank the Fear Trade for much of gold’s performance last year. The Fear Trade, of course, is driven by low to negative real interest rates—when inflation erodes away at government bond yields—deficit spending, a weaker U.S. dollar and geopolitical uncertainty.

I believe these forces will only intensify in 2018. With inflation finally showing green shoots and President Donald Trump’s $1.5 trillion tax reform law expected to increase deficit spending, this year could provide the right conditions to spur gold prices higher.

The risks inherent in the Federal Reserve’s monetary policy tightening is a good place to start.

Beware the Rate Hike Cycle?

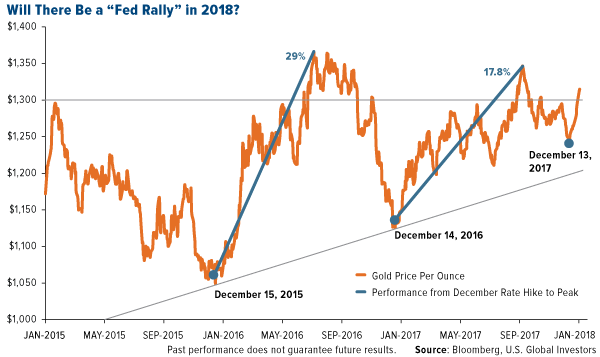

Since the Fed lifted rates last month, gold has behaved just as it did following the last two December rate hikes—that is, it’s begun to appreciate. On the final trading day of 2017, gold broke above $1,300 an ounce, a psychologically important level, and has since climbed an additional 1 percent. This is the first year since 2013, in fact, that gold has started the year above $1,300.

We’ve seen this movie before. In July 2016, the yellow metal peaked close to $1,370 an ounce, a 29 percent surge since the December 2015 rate hike. (If you remember, this represented gold’s best first half of the year since 1974.) And in September 2017, it topped out around $1,360, up close to 18 percent since the December 2016 rate hike.

So will we see a “Fed rally” in 2018 as well? Obviously nothing is guaranteed, but let’s say gold were to follow a similar trajectory this year as it did in 2016 and 2017. That would put gold somewhere between $1,460 and $1,600 an ounce by summer. These are prices we haven’t seen in four years.

I think it’s also worth pointing out in the chart above that support looks good for gold. For the past couple of years, it’s steadily posted higher lows.

But wait—shouldn’t rate hikes put a damper on gold prices? Gold, as I’ve discussed many times before, has typically thrived in a low-rate environment since it’s a non-yielding asset. What’s really happening here?

I’ll let Jim Rickards, editor of Strategic Intelligence, field this question. In a recent Daily Reckoning article titled “The Next Great Bull Market in Gold Has Begun,” Jim explains that the market is looking beyond the rate hike and “asking what comes next.”

After all, the December rate hikes in 2015, 2016 and 2017 were all advertised well in advance by the Fed and were fully discounted by the market. This means that the rate hike was a nonevent, because gold was already priced for it.

Yet the rate hike itself and the Fed’s commentary suggest both a headwind for economic growth and possible Fed ease in the form of future inaction and forward guidance relative to expectations.

Gold markets, in other words, could be forecasting slower economic growth as a result of higher borrowing costs. You might not agree with Jim here, and I’m not asking you to. After all, the U.S. economy is humming right now. Consumer spending is up, optimism is high and we have a robust labor market with unemployment at a 17-year low of 4.1 percent. Many people expect the Trump tax cuts to prompt multinational corporations to bring home cash that’s been held overseas, lift wages and boost capex spending.

At the same time, we can’t ignore the historical implications of past rate hike cycles. I shared with you last month that in the past 100 years, only three such cycles out of at least 18 didn’t end in a recession.The current cycle could turn out to be just as benign, but that would make it a huge exception, not the norm.

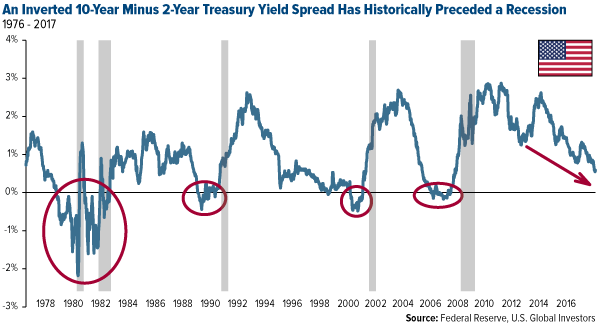

U.S. Yield Curve Flattens to Level Not Seen Since 2007

Then there’s the flattening yield curve. The yield curve is said to “flatten” when the difference between the two-year Treasury yield and 10-year Treasury yield starts to tighten. As of today, that spread drew up to around 0.496 percentage points, its flattest level since October 2007.

This measure is worth watching because it’s often seen as one of the most reliable “canary in the coal mine” predictors of recession. The past seven U.S. recessions were directly preceded by an inverted yield curve—that is, when short-term yields rose above long-term yields.

To be clear, we still have a way to go before the yield spread inverts. But if this observation concerns you—if you believe the business cycle is in fact getting a little long in the tooth—it might make sense to ensure you have a 10 percent weighting in gold bullion and high-quality gold mutual funds and ETFs.

Inflation Could Be a Lot Hotter Than We Realize

Another factor that’s driven gold prices in the past is inflation. When the cost of living has eaten away at government bond yields, investors have tended to seek more attractive stores of value, including gold. This is at the heart of gold’s Fear Trade.

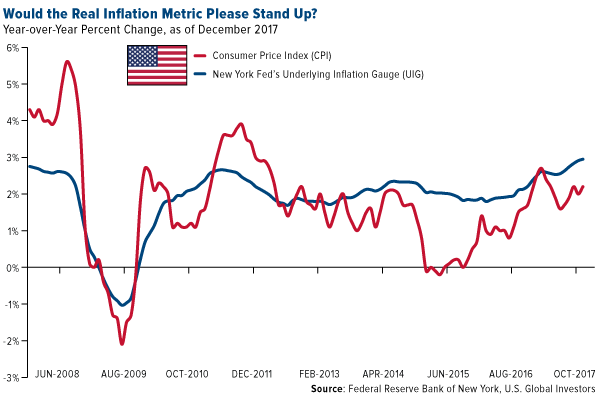

The problem is that inflation has been sluggish lately—if we’re using the official consumer price index (CPI). In 2017, the CPI just barely met the Fed’s 2 percent target rate. Many economists had expected prices to start creeping up last year in response to President Trump’s nationalist “America first” agenda, complete with new tariffs, strong crackdown on illegal immigration, cancellation of U.S. participation in the Trans-Pacific Partnership (TPP) and a renegotiation of the North American Free Trade Agreement (NAFTA). So far these policies haven’t had much effect on inflation.

But what’s the “real” inflation? Which gauge should we be looking at? Again, the CPI doesn’t show much movement.

The underlying inflation gauge (UIG), however, tells a different story.

The UIG, introduced only last year by the New York Fed, is a much broader measure of inflation than the CPI. It includes not just consumer prices but also producer prices, commodity prices and financial asset prices.

When we use this dataset, we find that—surprise!—inflation is not as subdued as we initially thought. Whereas the November CPI came in at 2.2 percent, the UIG heated up to 3 percent, its highest reading since August 2006.

The implications here are huge. Three percent is higher than the five-year Treasury yield, currently around 2.3 percent, and the 10-year yield, about 2.5 percent. It’s even higher than the 30-year Treasury yield at 2.8 percent!

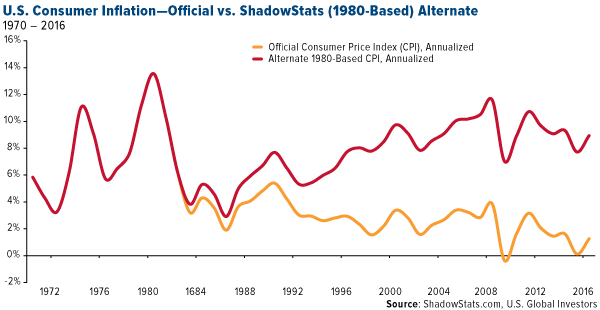

But there are even more ways to measure inflation, and some show it being higher than the UIG. Economist John Williams runs a website called Shadow Government Statistics, where you can find, among other “alternate” datasets, current inflation rates as is they were calculated the way the U.S. government did pre-1980. Note the huge bifurcation between the official CPI and alternate 1980-based CPI. According to the alternate gauge, consumer prices in November rose close to 10 percent year-over-year, or 7.75 percentage points more than the CPI.

“In general terms,” Williams writes, “methodological shifts in government reporting have depressed reported inflation, moving the concept of the CPI away from being a measure of the cost of living needed to maintain a constant standard of living.”

So which metric do you believe? The official CPI? The 1980-based CPI? The broader UIG? If it’s one of the last two, you have to ask yourself why you would lock your money up for five years, 10 years or even 30 years in a government bond that fails to keep up with real inflation. The investment case for gold suddenly becomes very attractive.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.33 percent. The S&P 500 Stock Index rose 2.60 percent, while the Nasdaq Composite climbed 3.38 percent. The Russell 2000 small capitalization index gained 1.60 percent this week.

- The Hang Seng Composite gained 3.33 percent this week; while Taiwan was up 2.23 percent and the KOSPI rose 1.22 percent.

- The 10-year Treasury bond yield rose 6 basis points to 2.48 percent.

Domestic Equity Market

Strengths

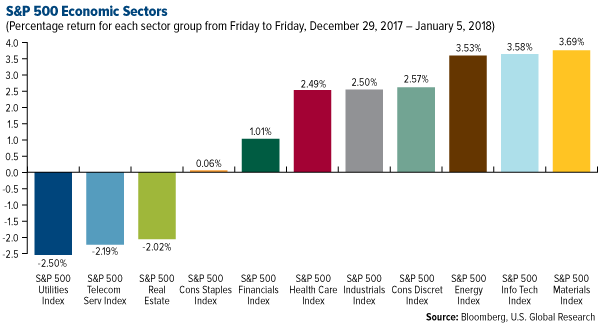

- The best performing sector for the week was information technology, closing up 4.5 percent.

- The best performing stock for the week was Advanced Micro Devices, closing up over 15 percent.

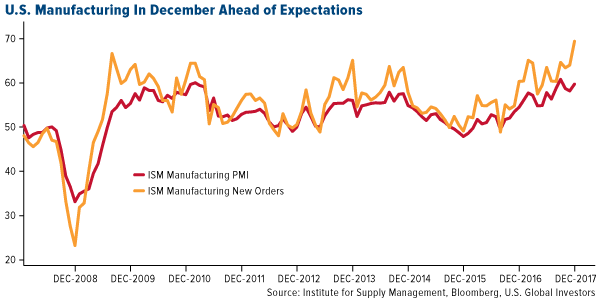

- Markit’s U.S. manufacturing report for December came in at 55.1, up 1.2 points from the November reading. Highlighting the results are acceleration in new orders and a two-year best for backlogs, reports Bloomberg.

Weaknesses

- The worst performing sector for the week was utilities, down 2.48 percent.

- The worst performing stock for the week was Leading Brands, down 16.09 percent.

- A snow storm pummeled the U.S. Northeast this week, reports Bloomberg, knocking out power for thousands of residents. Along the East Coast, 21,000 customers lost power and on Friday around 1,427 flights were cancelled.

Opportunities

- Amazon will debut the first augmented-reality glasses with the company’s Alexa voice assistant next week at CES in Las Vegas, reports Bloomberg. “The strategy is designed to put Amazon’s service, which generates revenue for the company, in as many places as possible to sell more products,” the article reads.

- Investors will get additional information about the last month’s employment situation next week when the Labor Department’s JOLTS report is released on Tuesday.

- The number of scripted television shows released in the U.S. reached a new high in 2017, more than doubling in seven years, reports Bloomberg. Of the 487 shows released last year, 117 were accounted for by streaming services. This news reflects the “growing efforts of Netflix, Amazon and YouTube to steal viewers and advertisers from traditional networks,” the article reads.

Threats

- Charles Schwab’s client account cash balances as a percentage of total assets are at record low levels, levels below the lows prior to the Technology crash in 2000. This, combined with the longest bull market in history, nine years running, is seemingly starting to worry some market participants.

- During the “dot com” era we witnessed companies adding “.com” to their names. In doing so, stocks rocketed higher as if they found the cure for previously incurable disease. Unfortunately, in the recent past we started witnessing similar behaviors except “.com” was replaced with “crypto.” For example, Long Island Iced Tea recently changed its name to “Long Blockchain Corp” and the stock price rallied 180 percent. When we see these situations, it might be time to invest with additional caution.

- The spread between the 2-year yield and 10-year yield is at multi-year lows. If the Federal Reserve continues to tighten rates and the 10-year yield stays at current levels, the spread will be close to inverting, thus slowing the flow of money and possibly hindering future growth.

The Economy and Bond Market

Strengths

- The headline JPMorgan Manufacturing purchasing managers’ index (PMI), hit 54.5 in December, the highest since February 2011. This data indicates that manufacturing has now gained growth momentum for six successive months, with output, employment and new orders rising at increased rates toward the end of 2017.

- American consumers last year were more up beat on average than at any time since 2001, reflecting more favorable views of the economy, personal finances and the buying climate, according to the Bloomberg Consumer Comfort Index released Thursday. The index came in at 50.0 for 2017, up from 43.6 a year earlier and the best reading since 51.8 in 2001. Sentiment in 2017 got a boost from the combination of a solid labor market that’s pushed unemployment to an almost 17-year low, limited inflation and record stock prices.

- The Atlanta Fed’s GDP Nowcast model now sees U.S. fourth-quarter GDP at 3.15 percent compared to 2.7 percent forecast earlier. The latest releases affecting the model were ISM manufacturing and construction spending. The PCE contribution was estimated at 2.24 percent.

Weaknesses

- The U.S. M2 monetary growth, already the slowest since 2011 at 4.7 percent, should slow further to 2.1 percent in the second quarter due to quantitative tightening, all other things being equal.

- Home builders and building materials in the U.S. fell Thursday after Wednesday’s Federal Reserve minutes release firmed up expectations of monetary tightening and rising rates, which makes home buying more unfavorable. Mortgage REITs were among the largest decliners in both the U.S. and Canada Wednesday. Credit Suisse analyst Douglas Harter wrote in a report that residential mortgage REITs will likely generate a 4.9 percent return this year versus the 14.3 percent return in 2017.

- Employers added 148,000 workers, compared with the 190,000 median estimates of economists surveyed by Bloomberg, held back by a drop in retail positions, a Labor Department report showed Friday. The unemployment rate holds at 4.1 percent, the lowest level since 2000.

Opportunities

- The ISM manufacturing index rose 1.5 percentage points from a month earlier to a reading of 59.7 in December, the second-highest level since early 2011, the Institute for Supply Management said Wednesday. A sub index of new orders, a measure of sales at factories, rose more than 5 points to 69.4, the highest since early 2004. Details hinted at further growth in coming months. While sales picked up, inventories at both factories and customer count fell. That combination suggests factories will have to boost production further in the first quarter of 2018 to satisfy demand.

- According to Bloomberg, the top three high duration and high beta securities attracted $200 million each during the first session of 2018. After a year that saw investors swap credit risk for duration risk whenever risk aversion arose, it is clear that reaching for yield is alive and well in 2018.

- According to the Wall Street Journal, workers in metro areas with the lowest unemployment are experiencing among the strongest wage growth in the country. The labor market in places like Minneapolis, Denver and Fort Myers, Fla., where unemployment rates stand near or even below 3 percent, has now tightened to a point where businesses are raising pay to attract employees, often from competitors. Wage growth is finally moving higher and could point to improved incomes nationally in 2018.

Threats

- The WSJ reports that although sales suffered an annual decline, the number of units sold actually surpassed the 17M mark for three consecutive years. However, executives remain concerned that the decline may be more than a blip. U.S. production is reduced in anticipation of weaker demand, rising interest rates and potential decline in value of used cars. The Federal Reserve forecasts three rate hikes this year, crimping the free-flowing credit that’s helped fuel a record streak of demand growth that’s come to an end.

- The strongest manufacturing activity since the aftermath of the global financial crisis is slowly draining commodities surpluses, sending prices to a 3-year high as investors pour money into everything from oil to copper. For the global economy, the pickup in commodities poses a conundrum. It could show how years of ultra-lax monetary policies have finally boosted activity and may even be enough to revive long-dormant inflationary pressures. The risk is inflation reemerging faster than central banks expect, forcing them to raise interest rates more aggressively than they now plan or investors anticipate.

- Ray Dalio of Bridgewater sees Americans’ debt as a coming drag on growth and markets. He said not only will this drag on growth and markets, it will leave the economy acutely vulnerable to higher interest rates. The problem is that with interest rates and risk premia near all-time lows and debt and asset values near all-time highs, there’s little fuel to repeat the process. Just as the Fed can’t cut rates much, it can’t raise them much either, or debt servicing would swamp cash flow and asset prices would sink. Thus Mr. Dalio sees years of low interest rates, and while he thinks stocks are fairly valued, returns to a typical stock-bond portfolio over the next decade will be around zero after inflation and taxes.

Gold Market

This week spot gold closed at $1,320.24 up $17.19 per ounce, or 1.32 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.65 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index closed up 5.29 percent. The U.S. Trade-Weighted Dollar was flattish this week losing just 0.11 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-1 | Caixin China PMI Mfg | 50.7 | 51.5 | 50.8 |

| Jan-3 | ISM Manufacturing | 58.2 | 59.7 | 58.2 |

| Jan-4 | ADP Employment Change | 190k | 250k | 185k |

| Jan-4 | Initial Jobless Claims | 240k | 250k | 245k |

| Jan-5 | Eurozone CPI Core YoY | 1.0% | 0.9% | 0.9% |

| Jan-5 | Change in Nonfarm Payrolls | 190k | 148k | 252k |

| Jan-5 | Durable Good Orders | -- | 1.3% | 1.3% |

| Jan-3 | PPI Final Demand YoY | 3.0% | -- | 3.1% |

| Jan-4 | Initial Jobless Claims | 248k | -- | 250k |

| Jan-5 | CPI YoY | 2.1% | -- | 2.2% |

Strengths

- The best performing metal this week was platinum, up 4.3 percent as speculators cut their net bearish platinum positions. After being bullish for the previous three weeks, gold traders and analysts are neutral this week, according to a Bloomberg survey. However, the number of new investors for BullionVault hit the highest level since November 2016, according to the online gold vaulting firm.

- Even as equities were record-high in 2017, investors still turned to gold as a hedge against uncertainty, pushing the Comex futures volume to an all-time high, according to Bloomberg.

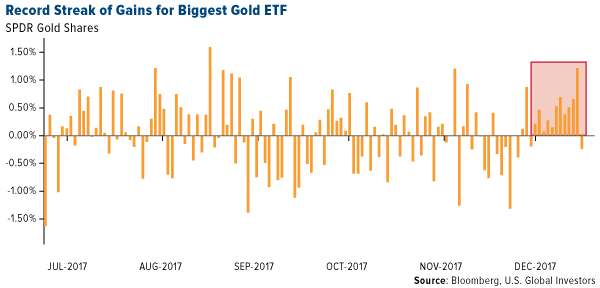

- The largest gold ETF, SPDR Gold shares, kicked off 2018 strong by continuing its record streak of gains. The gold price continues to increase due to a weaker U.S. dollar.

Weaknesses

- The worst performing metal this week was gold, still up 1.3 percent. Although gold has started 2018 strong, some think warning signs have flashed the gain may be overdone. Bullion’s 14-day relative strength index hit 74, which is above the level of 70 that suggest a pullback is imminent, according to Bloomberg. Gold fell after the Federal Reserve meeting minutes showed most officials support higher interest rates.

- Gold futures were set for the longest rally since 1975 after a report showed a slower-than expected hiring rate. The U.S. dollar dropped at the initial reaction of the news, and then bargain hunters stepped in raising the price of the dollar and pushing the gold price down.

- Home resales dropped in Manhattan, New York down 11 percent to 2,127 homes. More than 88 percent of homes sold in the fourth quarter of 2017 were below the asking price with the median resale price of $916,425. Many see this as a reaction to impending tax reform taking effect.

Opportunities

- India’s December 2017 gold imports rose 37 percent year-over-year from 56.9 tons to 77.7 tons. This is very positive news given that India has the second highest gold demand behind only China, and might signal the return of a gold bull market. India’s gold market has struggled the last year with demonetization and tax reform but Fitch recently ranked India number one of the top 10 emerging markets for GDP growth with the largest working-age population in the next five years. A stronger Indian economy has historically been good for gold prices.

- Gold mining companies are on the rise due to record high commodity prices and years of self-help measures that have strengthened balance sheets, according to Bloomberg. “Miners look to be in the healthiest position that we have seen for years,” says Paul Gait, analyst at Sanford C. Bernstein, but noted that the big M&A deals of the past were value destructive. “There is nothing wrong with being a cash cow,” Gait wrote in the report.

- The yellow metal was off to a strong start this month and might rally for the remainder of the month, if not the entire year. David Lennox, resource analyst at Australian brokerage Fat Prophets said, “Higher inflation coupled with weakness in the dollar will push the price upwards.” Other evidence to support a bullish view is that gold remained strong in 2017 despite the U.S. stock market surging to record highs and interest rates rising three times.

Threats

- According to Morgan Stanley, it might be too late in the market cycle to bet on high-yield bonds. The money management firm cut its junk bond allocation, citing excesses from the tax cuts might lead to a recession after growth in the short-term.

- The U.S. trade deficit hit its highest level in almost six years with an increase in imports exceeding a gain in shipments. This could keep the gross domestic product from advancing at least 3 percent, according to Bloomberg’s Andrew Mayeda. Automakers saw their first annual U.S. sales decline since 2009 and projections for 2018 are down due to expectations of interest rate hikes.

- In a Bloomberg interview this week, Former U.S. Treasury Secretary Jacob J. Lew said the recently passed tax reform is a ticking time bomb for debt that could leave the U.S. broke. Lew said the administration is “spending trillions of dollars you don’t have at a time that the economy is doing well.” Lew believes the tax cuts will lead to certain proposals cut or reduced such as medical insurance for the poor and Social Security and Medicare.

Energy and Natural Resources Market

Strengths

- Lumber was the best performing major commodity this week rising 3.2 percent. The commodity rallied on the back of another reading showing synchronized global purchasing manufacturers index (PMI) advances. Lumber prices have one of the highest correlations to rising PMIs, which have lifted lumber prices to near all-time highs.

- The best performing sector this week was the S&P 1500 Oil & Gas Exploration and Production Index. The index rose 7.9 percent propelled higher by rising crude oil prices, to which they offer greater beta than other energy related sectors.

- Fortescue Metals Group, a major Australian producer of iron ore, was the best performing stock in the broader resource market this week. The stock rallied 10.3 percent after M&G Investments out of London revealed it had initiated a position in the stock, while simultaneously decreasing its holding in BHP.

Weaknesses

- Natural gas prices dropped 4.0 percent; the most among major commodities. The commodity dropped in spite of the abnormally cold weather experienced by most Americans this week, as natural gas bulls are heading for the exits on signs that the polar chill won’t last, with Accuweather Inc. expecting warmer than seasonal temperatures reaching the East Coast next week.

- The worst performing sector this week was the FTSE 350 Mining Index. The index actually advanced 0.9 percent but trailed other resources sectors as advances in industrial metals were offset by declining copper prices.

- The worst performing stock for the week was Hochschild Mining PLC. The precious metals miner dropped 5.4 percent after RBC cut its rating on the stock to sector perform from outperform on valuation grounds.

Opportunities

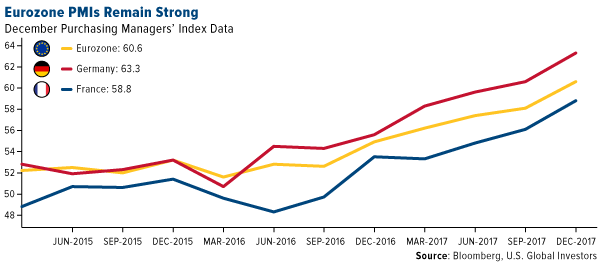

- Global PMIs continued their synchronized expansion in December, suggesting the commodity rally could continue. China’s manufacturing sector expanded at its fastest rate in four months in December. The Caixin-Markit manufacturing purchasing managers’ index rose to 51.5 in December. Eurozone manufacturers report strongest month on record - The manufacturing purchasing managers’ index for the eurozone as a whole came in at 60.6 in December, its strongest level since the survey began in mid-1997. Similarly, India’s manufacturing sector expanded at its fastest pace in five years in December on sharp increases in output and new orders.

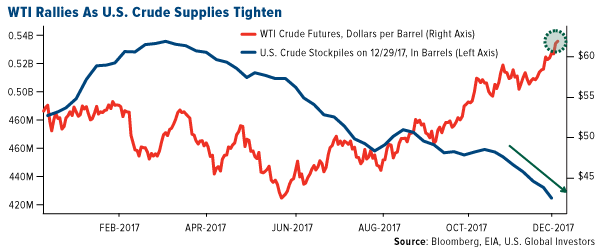

- Oil prices jumped as U.S. crude stockpiles shrink the most since August. American crude inventories slipped by 7.42 million barrels last week as refiners boosted operating rates to the highest level in more than a decade, signaling strong demand, the Energy Information Administration said on Thursday.

- India’s gold imports surged 67 percent in 2017. Increased demand in the South Asian nation drove a rise in imports to 855 tonnes in 2017 as jewelers replenished inventory amid a rebound in retail demand.

Threats

- Oil retreated from a 3-year high as expanding inventories of gasoline and diesel in the world’s biggest economy tempered enthusiasm about shrinking crude supplies. Gasoline stored in U.S. terminals and tanks swelled for an eighth straight week, a phenomenon not seen since the winter of late 2015 and early 2016. Ample stockpiles of gasoline and other fuels may signal an imminent fall-off in refiners’ demand for crude that helped support the recent price rally.

- Iron ore stockpiles amassed in ports across China have burst above 150 million metric tons, notching another record in the world’s largest importer. Unprecedented state-mandated curbs on steelmakers’ output over the winter months’ have blunted demand while seaborne supplies increase. The record port stockpiles are among signs global supply remains plentiful as miners BHP Billiton Ltd., Rio Tinto Group and Vale SA press on with production.

- Clouds have drifted over the U.S. solar industry according to the Financial Times. Tax reform, electricity regulation and potential new duties on imported panels are looming over the industry, threatening to disrupt the conditions that have made success possible. Already, installations have slowed for the first time in more than a decade, dropping about 22 percent to 11.8GW last year. President Trump is scheduled to deliver a decision on new duties on imports by January 26, and if he chooses to impose the tariffs sought by U.S. manufacturers, the price of panels in the US could double.

China Region

Strengths

- Hong Kong’s Hang Seng Composite Index closed out the first calendar week of 2018 with a 3.33 percent gain. Much of the rest of the region also had a strong week, with indices like the Shanghai Composite, the SET Index, TWSE Index, the PCOMP Index, the Ho Chi Minh Stock Index and Singapore’s FTSE Straits Times Total Return Index all returning between 2-3 percent for the week.

- Energy, along with properties & construction, finished out the week as the top two sectors in the Hang Seng Composite so far in 2018, rising 7.17 and 6.84 percent, respectively.

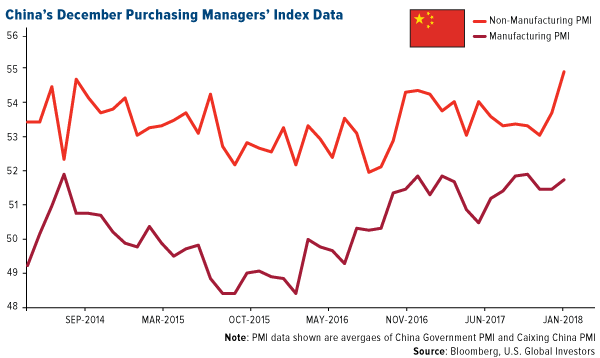

- China’s purchasing managers’ index (PMI) came in strong for the December period. Official Manufacturing and Non-manufacturing PMI clocked in at 51.6 (in line) and 55.0 (beat), while the Caixin China Manufacturing PMI came in at 51.5 (ahead of expectations for 50.7 and up from last month’s 50.8), while the Caixin Services finished at 53.9, ahead of expectations for a 51.8 print.

Weaknesses

- Indonesia was the laggard for the week, as the Jakarta Composite actually declined by 3 basis points.

- The services and telecommunication sectors were the worst in the Hang Seng Composite this week, declining mildly by 73 and 70 basis points, respectively.

- The Nikkei Indonesia PMI for the December period declined to contractionary territory with a reading of 49.3, down from the prior month’s 50.3 print.

Opportunities

- China will reportedly maintain the same official economic growth expectations as 2017, with a 6.5 percent GDP growth rate target.

- Bloomberg News reported this week that Chinese authorities’ plans to introduce a property tax are likely set to be enacted later than initially expected, and probably not until 2020, at this point. While the introduction of a tax is a net negative for properties, it appeared that property & construction names liked the news of a delay this week.

- After some overtures earlier in the week, South Korea and North Korea have now agreed to a formal dialogue starting next week, one that hopefully bears fruit.

Threats

- Despite some of the positives in the North Korea situation this week, the issue of rhetorical skirmishes between Pyongyang and Washington continued in the odd form of a my-nuclear-button-is-bigger-and-more-powerful-than-your-nuclear-button tweet, delivered in response to a Kim Jong Un speech. Indeed, while the odds of serious escalation continue to appear relatively low, there remains a certain wildcard factor to North Korea—and in potential responses to it.

- At the close of 2017, Chinese authorities announced per-individual caps on domestically-issued bank card annual withdrawals, a change from the previous policy of per-account caps on withdrawals.

- China is planning to limit access to power supplies for some Bitcoin miners, Bloomberg reported this week, highlighting plans supposedly outlined in a closed-door meeting of the People’s Bank of China (PBOC). China remains home to many of the world’s largest Bitcoin miners.

Emerging Europe

Strengths

- Russia was the best performing country this week, gaining 4.6 percent. This week the country was on a New Year Holiday Break. The Moscow Stock Exchange was only open a few days, and as most people were on vacation break, trading was light. Mail.Ru and X5 Retail Group were the best performing stocks, gaining more than 12 percent each. Brent crude oil traded above $68 per barrel, a level last seen on May 13, 2015.

- The Turkish lira was the best performing currency this week, gaining 1.6 percent against the U.S. dollar. Foreign capital is flowing into Turkish stocks and bonds. According to Bloomberg’s note, foreign investors bought around $9 billion of Turkish securities in 2017, the most in five years.

- The material sector was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst relative performing country this week, gaining 1.1 percent. Jurors in a New York court found the Turkish banker, Hakan Atilla, guilty of helping Iran evade U.S. financial sanctions. The judge will announce his sentence in April, and a potential fine against Halkbank might be announced soon.

- The euro was the worst relative performing currency this week, gaining 30 basis points against the U.S. dollar. A stronger dollar and weaker inflation put pressure on the currency.

- Real estate was the worst performing sector among eastern European markets this week.

Opportunities

- Germany and the eurozone’s final manufacturing PMIs for December were unrevised and stayed at record highs. France’s PMI was revised lower, but still is at the highest reading since September 2000. New orders are rising as firms prepare for higher production in 2018.

- Russian gas output jumped by 7.9 percent last year to a record high, supported by higher sales to Europe and rising domestic demand. With new pipeline projects in the works, Russia still has more room for growth. Higher gas and oil exports will help the country to generate more revenue.

- Hungary’s government bond yields fell below 2 percent for the first time. Policy makers will start interest-rate swap tenders on January 18 in order to lower long-term borrowing costs in the economy. The central bank is expected to continue its dovish strategy, which should lead to further outperformance for Hungarian government bonds compared with Poland, according to Guillaume Tresca, Credit Agricole SA strategist.

Threats

- The mainstream media is telling the world that 2018 should be another favorable year for investors in risk assets, but Kepler Cheuvreux research team does not agree with the mainstream media view. The group says that the correction in Europe already began in November and the most persuasive signal for a correction in European equities will be given when the DAX index falls below the 12780-12800 treshold. The research team anticipates a selloff in European equites.

- At the end of January, the United States may announce additional sanctions on Russia. The list of people and companies under sanctions might be extended, and sanctions could be imposed on countries and/or individuals who continue to do business with Russia. Turkey is a member of NATO, but recently purchased a weapon system from Russia, making itself a target for some kind of sanctions.

- Eurozone inflation weakened despite good growth in the euro area. Consumer prices rose 1.4 percent in the year to December, down from the previous month’s 1.5 percent rate. The core inflation, which strips out potentially volatile items such as energy and food, remained even lower at 0.9 percent. The inflation is moving further away from the European Central Bank’s target of 2 percent.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits