Recipe Calls for a Broad Commodities Rally in 2018

Membership required

Membership is now required to use this feature. To learn more:

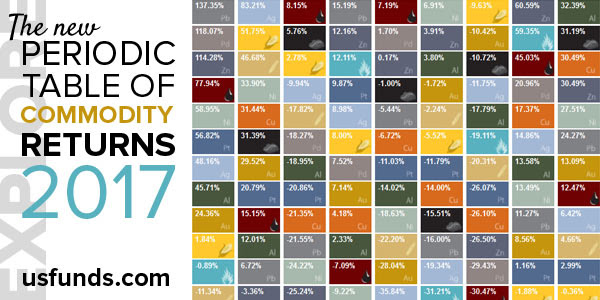

View Membership BenefitsAt the beginning of every year, we update what’s typically one of our most popular pages, the Periodic Table of Commodity Returns. I encourage you to explore 10 years’ worth of data on basic materials such as aluminum, zinc and everything in between. A word of warning, though—the interactive feature makes the table highly addictive. Please feel free to share it with friends and family!

It was a photo finish for commodities in 2017. The group, as measured by the Bloomberg Commodity Index, barely eked out a win for the second straight year, edging up 0.7 percent. Spurred by a weaker U.S. dollar and strengthening materials demand from factories, the index headed higher thanks to a breathtaking rally late in the year that lasted a record 14 consecutive days.

The annual return might not look too impressive, but I believe the economic conditions are ripe for a broad commodities rally in 2018. I’m not alone in predicting they’ll be among the best performing asset classes by year end, perhaps even beating domestic equities as quantitative tightening threatens to put a damper on the nine-year bull run.

Analysts at Goldman Sachs, for instance, are overly bullish on commodities, recommending an overweight position for the next 12 months. Bank of America Merrill Lynch is calling for a $7,700-a-tonne copper price target by mid-2018, up from $7,140 today. In today’s technical market outlook, Bloomberg Intelligence commodity strategist Mike McGlone writes that the “technical setup for metals is similar to the early days of the 2002-08 bull market.” Hedge fund managers are currently building never-before-seen long positions in heating oil and Brent crude oil, which broke above $70 a barrel in intraday trading Thursday for the first time since December 2014. It’s now up close to 160 percent since its recent low of $27 a barrel at the beginning of 2016.

Few have taken such a bullish position, though, as billionaire founder of DoubleLine Capital Jeffrey Gundlach, whose thoughts are always worth considering.

Commodities Ready for Mean Reversion?

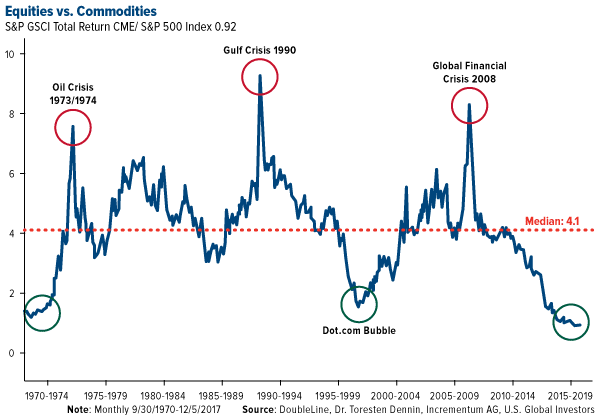

Last month I shared with you a chart, courtesy of DoubleLine, that makes the case we could be entering an attractive entry point for commodities, based on previous booms and busts. The S&P GSCI Total Return Index-to-S&P 500 Index ratio is now at its lowest point since the dotcom bubble, meaning commodities and mining companies are highly undervalued relative to large-cap stocks. We could see mean reversion begin to happen as soon as this year, triggering a commodities super-cycle the likes of which we haven’t seen since the 2000s.

Gundlach has more to say on this subject. During his annual “Just Markets” webcast this week, he told investors that “commodities will outperform in 2018” because they “always rally sharply—much more sharply than they have so far—late in the business cycle as we head into a recession.”

Speaking to CNBC, he added that the S&P 500 “may go up 15 percent in the first part of the year, but I believe, when it falls, it will wipe out the entire gain of the first part of the year with a negative sign in front of it.”

Gundlach might be in the minority here, but it’s hard to ignore the tell-tale signs that we’re approaching the end of the business cycle, as I’ve pointed out before. We’ve begun a new interest rate hike cycle, both here in the U.S. and the United Kingdom. The Federal Reserve has started to unwind its massive balance sheet. The Treasury yield curve continues to flatten. And the S&P 500 just had its least volatile year on record.

All of these indicators, among others, have historically preceded a substantial market correction.

In his 2018 outlook, David Rosenberg, chief economist and strategist at Canadian wealth management firm Gluskin Sheff, makes similar observations, writing that “it is safe to say that we are pretty late in the game.”

How late? After looking at a number of market and macro variables, Rosenberg and his team concluded that we’re about “90 percent through, which means we are somewhere past the seventh inning stretch in baseball parlance but not yet at the bottom of the ninth.”

Look for mean reversion this year, Rosenberg adds, “which would be a good thing in terms of opening up some buying opportunities.”

Resource stocks, I believe, could be an attractive place to look, as they’ve traditionally outperformed in the last phase of an economic cycle.

Manufacturing and Construction Booms Underway

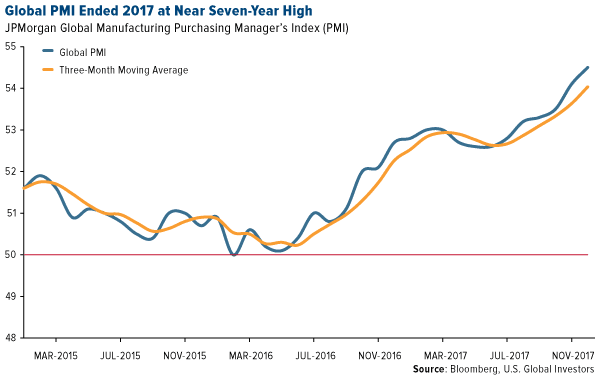

You don’t have to bet on a recession to be bullish on commodities. The dollar appears to have peaked, making materials less expensive for overseas markets, and the Global Manufacturing Purchasing Manager’s Index (PMI) ended 2017 at 54.5, close to a seven-year high. The sector has been in expansion mode now for the past 22 months, with the eurozone signaling its fastest growth in the series’ two-decade history.

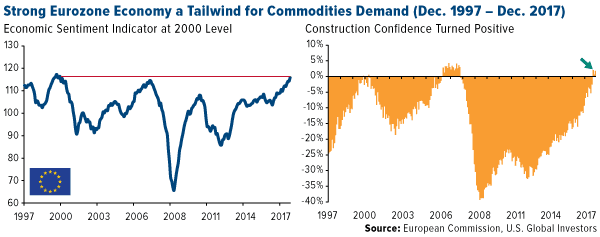

That’s not the only constructive news out of Europe. The European Commission’s headline economic sentiment indicator jumped more than economists had anticipated in December, ending the year at a 17-year high. Construction confidence in the eurozone also looks as if it’s fully recovered and is trending in positive territory for the first time since the financial crisis.

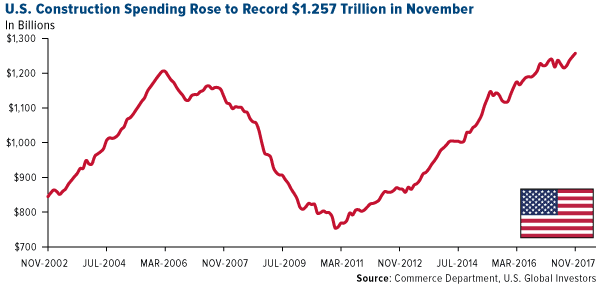

Strong manufacturing and construction expansion here in the U.S. is likewise supportive of commodity prices. December’s ISM Manufacturing PMI clocked in at a historically high 59.7. New orders grew 5.4 percent from the precious month to 59.4, its highest reading since January 2004. What’s more, U.S. construction spending in November rose to an all-time high of $1.257 trillion, according to this month’s report from the Census Bureau.

Which Commodities Are Set to Rally the Most?

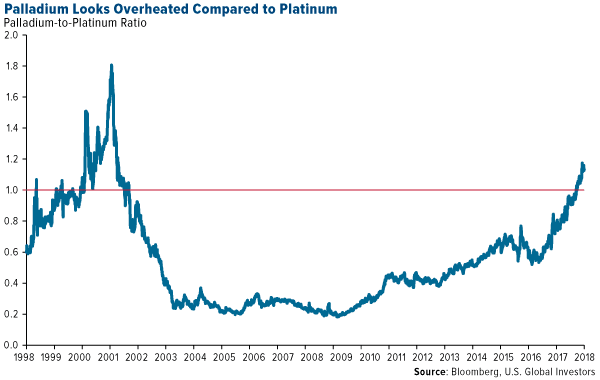

Palladium was the best performing commodity of 2017, climbing more than 56 percent on a weaker dollar, concerns of a supply crunch and a robust global auto market. Along with its sister metal, platinum, palladium is used primarily in the production of catalytic converters, which curb emissions from gasoline-powered vehicles.

For the first time since 2001, palladium traded higher than platinum beginning in September, and last week it hit an all-time intraday high of $1,099 an ounce. A healthy correction at this point wouldn’t be surprising, as the metal’s looking overbought compared to platinum.

“Pressured by diesel-emission scandals, platinum appears too low vs. palladium,” writes Bloomberg’s Mike McGlone. We might be in for another price reversal this year.

As I wrote last week, gold’s Fear Trade growth drivers are firmly in place. If a “Fed rally” occurs similar to the past two rallies, we could see gold climb to as high as $1,500 an ounce by summer. We also have the Chinese New Year to look forward to, which falls on February 16.

I believe 2018 could also be silver’s year to shine. The white metal rose 6.42 percent in 2017, with Indian silver bullion imports jumping an amazing 90 percent compared to imports the previous year, according to Metals Focus. Goldman Sachs analysts point out that silver has historically fared better than gold near the end of the business cycle, “as it is more strongly leveraged to global growth, given its significant industry use.”

A recent online survey conducted by Kitco News found that nearly 40 percent of respondents believed silver would outperform in 2018, compared to four other metals. Twenty-seven percent of readers said gold would outperform, followed by a quarter for copper. About 10 percent were most bullish on either platinum or palladium.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.01 percent. The S&P 500 Stock Index rose 1.57 percent, while the Nasdaq Composite climbed 1.74 percent. The Russell 2000 small capitalization index gained 2.05 percent this week.

- The Hang Seng Composite gained 2.04 percent this week; while Taiwan was up 0.04 percent and the KOSPI fell 0.04 percent.

- The 10-year Treasury bond yield rose 7 basis points to 2.55 percent.

Domestic Equity Market

Strengths

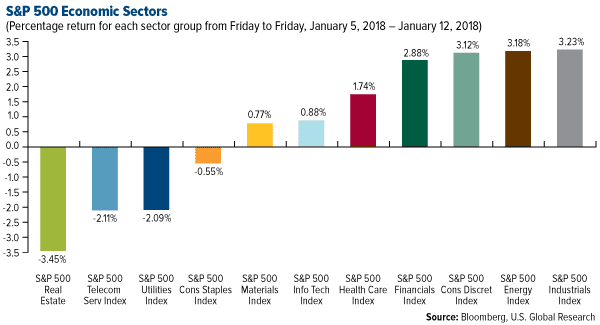

- Industrials was the best performing sector of the week, increasing by 3.23 percent vs an overall increase of 1.59 percent for the S&P 500.

- Seagate Technology was the best performing stock for the week, increasing 19.38 percent.

- JPMorgan beat earnings expectations after accounting for a $2.4 billion hit from tax reform. The firm is the first of the big banks to report on what is expected to be an unconventional earnings cycle for the industry, mostly on account of the tax law that has caused many banks to book losses on deferred tax assets that declined in value.

Weaknesses

-

- Real Estate was the worst performing sector for the week, falling 3.45 percent vs an overall increase of 1.59 percent for the S&P 500.

- Acuity Brands was the worst performing stock for the week, falling 14.36 percent.

Opportunities

- Kohl's is defying the retail collapse as the company's same-store sales spiked 6.9 percent during the holiday period. The growth suggests Kohl's is scooping up market share from the rash of stores closing across the country, most of which are tied to shopping malls. The company said nine out of 10 Kohl's stores are in suburban strip malls and other areas away from enclosed shopping malls.

- There's a strategy that may help you crush earnings season, according to Goldman Sachs. It involves the purchase of options straddles that are cheap relative to history and that capture a company's earnings period. The strategy has provided outsized returns for the past two decades.

- Dropbox filed paperwork for an initial public offering (IPO). The company, which grabbed a $10 billion valuation during a 2014 funding round, plans to list shares in the first half of the year.

Threats

- While U.S. stocks are now in an "accelerating phase," billionaire investor Jeffrey Gundlach is predicting that the S&P 500 will post a negative rate of return in 2018. The S&P 500 "may go up 15 percent in the first part of the year, but I believe, when it falls, it will wipe out the entire gain of the first part of the year with a negative sign in front of it," Gundlach said. His bearishness on the S&P and other risk assets including U.S. corporate bonds stems from the notion that the Federal Reserve has begun its era of "quantitative tightening."

- A stock trade that trounced the market last year could come crashing back to earth. According to Bank of America Merrill Lynch the growth trade may lose ground to its rival, the value trade.

- Jefferies downgraded Snap as the company’s new app redesign may not have the desired effect and could turn users away from publishers' content. Further, Cowen downgraded the stock last week after a survey of senior ad buyers revealed that 96 percent of them would prefer to advertise on Instagram, as opposed to Snap.

The Economy and Bond Market

Strengths

- The Labor Department said its consumer price index (CPI), excluding the volatile food and energy components, rose 0.3 percent last month as prices for new and used cars and trucks, as well as motor vehicle insurance increased. That was the biggest advance in core CPI since January 2017 and followed a 0.1 percent gain in November. The core CPI increased 1.8 percent in the 12 months through December, picking up from 1.7 percent in November.

- U.S. consumers shopped at stores and online outlets at a strong pace in December, closing out a healthy holiday season for retailers. The Commerce Department said Friday that retail sales rose 0.4 percent last month, after a 0.9 percent increase in November. 2017 retail sales rose 4.2 percent, the most in three years.

- Small-business confidence hit a record high in 2017, according to the National Federation of Independent Businesses. The index came in at 104.9 in December. The NFIB says the index's average monthly level last year was 104.8, the highest in the history of its survey.

Weaknesses

- Prices for U.S. exports fell 0.1 percent in December, the first monthly decline for the index, the U.S. Bureau of Labor Statistics reported Wednesday. The export prices drop was led by falling agricultural prices.

- According to the World Bank, between 2013 and 2017 global potential output growth was half a percentage point below its long-term average. In many countries, the output gap—the difference between the actual output and the maximum potential output of an economy—is closing or has already closed. This will restrain future economic growth, the World Bank said.

- Initial jobless claims came in at 261,000 for the week, higher than the forecast for 245,000.

Opportunities

- The municipal market’s performance in 2018 should be "slightly ahead" of last year, said Jeffrey Lipton, head of municipal research at Oppenheimer. The Bloomberg Barclays Municipal Bond Index returned 5.45 percent in 2017. “Munis are well-positioned entering 2018 against a backdrop of compelling market technicals that will likely bring substantively lower supply and active buyer interest from individuals and mutual funds," he said.

- John Williams, president of the Federal Reserve Bank of San Francisco, thinks the central bank needs new tools to fight chronically low inflation. Williams, speaking at a Brookings Institution conference in Washington, made the case for a shift to a price-level target, which would have called for more aggressive interventions during the Great Recession. Williams is worried the Fed has a "credibility problem" because it has fallen short of its 2 percent inflation target for much of the economic recovery.

- Sales of U.S. municipal green bonds could be headed for yet another record in 2018. States, localities, public authorities and nonprofits sold almost $11 billion in green bonds in 2017, a 45 percent jump from the prior year. That marked the sixth straight year of increased issuance of the bonds, which are used to finance projects with an environmental benefit. This year will likely see another uptick in issuance from U.S. municipalities because of an increased focus on climate change, especially in Democratic states like New York and California, said Sean Kidney, co-founder of the Climate Bonds Initiative.

Threats

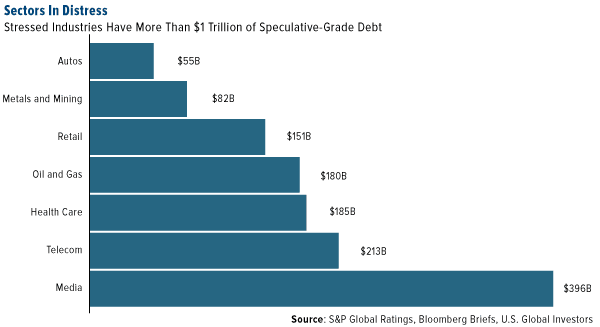

- Almost 40 percent of industries are weakened or stressed this year, up from just 9 percent in 2015, loan market data from Highland Capital shows. Issuers with junk ratings are also spread across a wider range of industries, rather than clustered in the usual categories such as retail and energy, according to S&P.

- Since 2010, the largest increase in municipal bond holdings has been at banking institutions and insurance companies, rising 49 percent and 15 percent, respectively. Prior to the 2009-10 federal stimulus — the American Recovery and Reinvestment Act (ARRA) — banks could only deduct interest related to bank-qualified muni bonds, while ARRA bonds allowed deduction of 80 percent of the interest costs. The latest tax-reform measures that lower the corporate rate have the potential to lower some of this growing demand.

- The volatility surrounding state credit ratings will likely remain "elevated," according to S&P Global Ratings. "We believe much of the negative pressure on credit quality reflects demographic trends more than cyclical factors. Therefore, the fiscal imbalances and liability pressures now buffeting numerous states — largely unalleviated by the economic expansion — may be harbingers of structural stress that becomes more endemic to the sector."

Gold Market

This week spot gold closed at $1,338.63, up $19.28 per ounce, or 1.46 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.29 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index came in off just 1.95 percent. The U.S. Trade-Weighted Dollar reversed course this week and closed down 1.10 percent.

|

Date |

Event |

Survey |

Actual |

Prior |

|

Jan-11 |

PPI Final Demand YoY |

3.0% |

2.6% |

3.1% |

|

Jan-11 |

Initial Jobless Claims |

245k |

261k |

250k |

|

Jan-12 |

CPI YoY |

2.1% |

2.1% |

2.2% |

|

Jan-16 |

Germany CPI YoY |

1.7% |

-- |

1.7% |

|

Jan-17 |

Eurozone CPI Core YoY |

0.9% |

-- |

0.9% |

|

Jan-18 |

China Retail Sales YoY |

10.2% |

-- |

10.2% |

|

Jan-18 |

Housing Starts |

1270k |

-- |

1297k |

|

Jan-18 |

Initial Jobless claims |

250k |

-- |

261k |

Strengths

- The best performing metal this week was palladium, up 3.02 percent. After polling neutral last week, gold traders and analysts are back to a bullish view of gold, according to the Bloomberg survey. This week gold ETFs added 91,867 troy ounces of gold to their holdings, the largest one-day increase since early December.

- Inflation increased last month due to higher housing costs, reinforcing the outlook that the Federal Reserve will possibly raise interest rates several times throughout 2018. The core consumer price index also increased 1.8 percent from a year earlier, according to Bloomberg. Higher inflation is generally linked to higher gold prices.

- Open interest on gold, the tally of outstanding futures contracts, posted the longest stretch of gains in more than a decade. Futures margins were cut for gold from $4,000 to $3,500 and for silver from $4,700 to 4,000; this will make it easier to buy a futures contract for both precious metals.

Weaknesses

- The worst performing metal this week was silver, up just 0.67 percent. The price of oil climbed to a three-year-high to $70 this week, amid OPEC production cuts and growing demand. America may be on its way to being the top oil producer with output headed for 11 million barrels a day in 2019, according to Bloomberg. A higher oil price has the potential to negatively affect miners.

- The Fort Worth, TX, branch of the Securities and Exchange Commission joked on Twitter this week that it was going to add “blockchain” to its Twitter name in order to increase the number of social media followers. Many believe the cryptocurrency frenzy is coming to an end after digital currencies have performed poorly since the start of 2018. Grant’s Interest Rate Observer said this week that cryptocurrencies are not money and that in troubled times people will still turn to gold.

- Torex Gold announced it has regained access to the El Limon-Guajes Mexico mine after worker strikes prevented production for several months. The company also announced that its Chief Financial Officer, Jeff Swinoga, will be leaving after four years of service.

Opportunities

- Many countries around the globe are experiencing labor shortages, including Japan and Germany. Labor shortages often lead to higher wages, which in turn increases inflation. Although this has not happened to the U.S. yet, Federal Reserve Bank of New York President William Dudley noted in remarks this week that if labor markets were to tighten much further there would be greater risk that inflation could rise substantially as some think the economy is at risk of overheating due to the tax cuts.

- Officials in China who review foreign-exchange holdings have recommended slowing or halting purchases of U.S. Treasures. The market for U.S. government bonds may become less attractive relative to other assets, and trade tensions between the U.S. and China may provide a reason to slow or stop buying American debt, writes Bloomberg. The following day Chinese officials denied these reports and said they are not slowing purchases of U.S. Treasuries. Although higher bond yields are traditionally negative for gold, some say gold is actually benefitting from this growing uncertainty in financial markets and a weaker U.S. dollar.

- Klondex Mines followed through on putting the True North Mine on care and maintenance this week after the operation failed to achieve planned operation and cash flow metrics in 2017 with production coming in at 24,000 – 27,000 ounces, which is about 10,000 ounces short of guidance. The mill will continue to process exiting stockpiles and reprocess tailings running at 1.2 Au/gpt for between $2 to $4 million of annual free cash flow. The original purchase price was around $30 million for True North out of receivership, so this was a fairly low risk endeavor. Ultimately, however, Klondex could not get the economic margins needed to profitably run the operation and this was the smartest decision for management to stop allocating capital to a low return project. While this was a painful learning experience for Klondex, we expect it will remove a distraction from the story as Klondex returns to focus only on its Nevada operations. The company’s share price hit a 52-week low and certainly could be at risk of a takeout offer at these levels.

Threats

- The Democratic Republic of Congo proposed to more than double the taxation of cobalt exports. The nation supplies two-thirds of the world’s supply of cobalt, which is a critical metal for battery production. Royalty miners could pay a tax of 5 percent of exports, up from 2 percent if the rule is formally adopted.

- As a part of the new tax overhaul, the endowments of wealthy private universities will now have to pay a 1.4 percent levy. The new tax measure disproportionately affects Democratic states with 22 of the 28 colleges subject to the tax reside in blue-heavy districts.

- Australia’s government expects the price of gold to drop in the next two years due to increasing yields on U.S. Treasuries as the Federal Reserve tightens their monetary policy, according to Bloomberg. Australian gold production is expected to increase annually by 3.7 percent to 306 tons, up from 285 tons the previous year.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by Bloomberg, the best performing for the week ended January 12 was Litecoin, which lost 4.46 percent.

- JP Morgan’s Jamie Dimon, who previously called bitcoin a “fraud,” has reversed his stance on the digital currency space, reports CNBC. Dimon says he regrets his statement and told Fox Business this week that he believes in the technology behind bitcoin, stating that “the blockchain is real.”

- KFC Canada announced that, for a limited time, it would accept bitcoin via BitPay as payment for a cryptocurrency-themed bucket of chicken. KFC’s decision is just the latest among many companies hopping on the bitcoin bandwagon to raise its publicity and integrate the digital currency into its payment system.

Weaknesses

- Of the cryptocurrencies tracked by Bloomberg, the worst performing for the week ended January 12 was Ethereum, which fell 32.84 percent.

- The Financial Times reports this week that bitcoin investors in the United Kingdom were turned away by mortgage lenders and brokers who apparently feared being targeted by anti-money laundering (AML) regulators.

- Speaking to CNBC this week, billionaire investor Warren Buffett said that he believed cryptocurrencies “will come to a bad ending,” adding that Berkshire Hathaway will “never have a position in them,” including shorts. Buffett has famously avoided asset classes and sectors he does not personally understand, and his attitude toward digital currencies is no exception. “Why in the world should I take a long or short position in something I don’t know anything about?” he said.

Opportunities

- Treasury Secretary Steven Mnuchin said this week that he wants to be able to prevent “bad people” from using cryptocurrencies “to do bad things.” If a satisfactory solution were reached and implemented, it could potentially raise some reluctant investors’ sentiment of the space.

- According to an article by CNBC this week, in the world of cryptocurrency buzz, blockchain is the real winner. “Blockchain is a robust technology that resembles the internet in the early ‘90s: It packs the potential to change the way we live, work, consume and interact,” the article reads.

- Reuters reports that Bitmain Technologies, a Beijing-headquartered semiconductor company, is scouting out bitcoin mining sites in Quebec as the Chinese government continues to crack down on cryptocurrencies. The company also reportedly seeks to expand into Switzerland.

Threats

- On Thursday, Bitcoin took a hit following South Korea’s justice minister announcing that a bill was being prepared to ban cryptocurrency trade in the country. As of Friday, a petition on the website of the presidential Blue House had drawn more than 120,000 signatures opposing the move, reports Reuters.

- Several notable companies have grown cold on bitcoin as a form of payment or, in some cases, completely reversed course, reports Cointelegraph. Microsoft, for one, announced it would no longer accept bitcoin after three years of doing so; however, the company resumed payments shortly after. Gaming platform Steam canceled bitcoin payments in early December. And ironically, tickets for the upcoming North American Bitcoin Conference in Miami can no longer be purchased with bitcoin.

- Swiss investment bank Credit Suisse found that wealth in bitcoin is highly concentrated, meaning “few players in the game can have a massive influence” on the markets. Ninety-seven percent—nearly 100 percent—of all bitcoins are held by only 4 percent of addresses. “Significant proportions of bitcoin and other cryptocurrencies are apparently being held like precious assets, thereby severely restricting the flow and availability of the digital currencies,” bank analysts say.

Energy and Natural Resources Market

Strengths

-

- Natural gas was the best performing major commodity this week rising 14 percent. The commodity rallied as the government’s Global Forecast System weather model shows the deep freeze in the eastern half of the U.S., expected to last through January 16, is getting even colder.

- The best performing sector this week was the S&P/TSX Diversified Metals and Miners Index. The index rose 7.6 percent, propelled higher by Teck Resources Ltd. after the stock was raised to outperform by Scotiabank analysts in Toronto.

Weaknesses

- Steel prices dropped 4.0 percent this week; the most among major commodities. The commodity dropped as Chinese mills go on pushing out supplies and nationwide stockpiles expand. Even as that clampdown remains through to spring, mills are still making enough rebar for holdings to grow. Buyers were concerned prices had risen too fast and consumption has now dropped, China Merchants Futures Co. said.

- The worst performing sector this week was the S&P/TSX Gold Index. The index advanced 0.2 percent as gold prices rallied on the back of a weaker U.S. dollar; however, it was offset by negative reactions to news by producers Klondex Mines and Alamos Gold.

- The worst performing stock for the week was Nutrien Ltd. The major Canadian fertilizer company dropped 3.8 percent after reports that low corn and other crop prices have significantly reduced farmer economics, and as a result are challenging fertilizer and agricultural input suppliers.

Opportunities

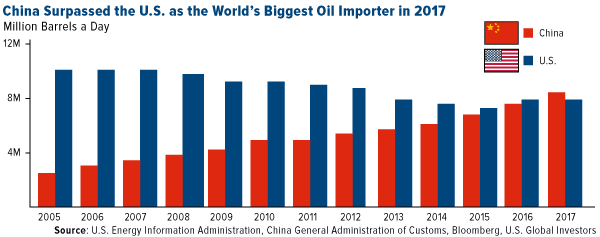

- China continues to gobble up the world’s commodities, setting new records for consumption of everything from crude oil to soybeans, according to Bloomberg data. Despite the much touted industrial capacity cuts, environmental curbs and financial deleveraging programs in the Asian nation, demand for raw materials has continued to grow in the world’s biggest consumer. As a result, the crown of the world’s biggest oil importer now sits firmly atop China after the nation’s shipments surpassed the U.S. on an annual basis for the first time ever.

- A bipartisan group of U.S. senators met with administration officials this week to discuss legislation to spend $1 trillion to improve infrastructure. U.S. construction, engineering, building materials and other companies tied to infrastructure spending stocks are set to be in focus in the coming weeks as President Donald Trump seeks legislation geared at overhauling the country’s aging roads, bridges and other infrastructure, which could result in a sizeable uptick for commodity demand.

- Auto parts manufacturers and suppliers were upgraded to market weight from underweight by Wells Fargo analyst Richard Kwas, who says demand for the group is likely to stay resilient in 2018. The sector is one of the major consumers of steel and aluminum products, hence the upgrade reads very well for sustained demand in these commodities.

Threats

- China’s import growth slowed dramatically in December, with a year-on-year rise of just 4.5 percent undershooting expectations of a 13 percent climb and down substantially from the prior month’s pace of 17.7 percent. Among the largest contributors to the disappointing read were unwrought copper imports, which fell 4.3 percent in December from a month earlier, according to Chinese customs data.

- Goldman Sachs warns that OPEC may talk oil prices down if Brent crude tops $70 a barrel. OPEC doesn’t want U.S. shale investments to rise, so the cartel will try to talk oil prices down if Brent exceeds $70 per barrel in the coming days, with Goldman adding that “we’ll probably see more noise and rhetoric if prices trade above $70 a barrel in the coming days to push this market back down to lower levels.”

- Greater regulatory and trade disputes threaten dislocations in commodity markets in 2018. Just this week, the U.S. International Trade Commission (ITC) issued a preliminary ruling against imports of aluminum sheet from China. If the ITC issues a final ruling and duties are imposed, U.S. aluminum prices could rise, but prices for producers outside of the U.S. could see negative price momentum.

China Region

Strengths

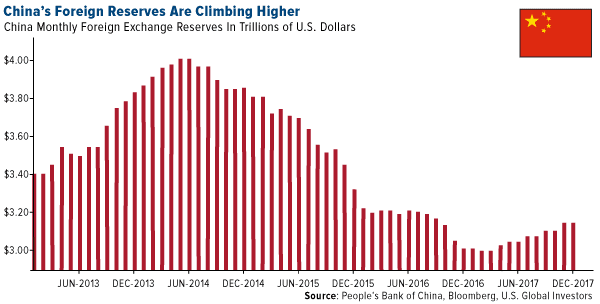

- Sometimes, boring is good. China’s foreign reserves number came in at $3.140 trillion, ahead of expectations and capping a year of slow, steady boosts to the FX reserves. The yuan climbed this week, approaching multi-month highs.

- Among the strongest of regional performers this week was Hong Kong’s Hang Seng Composite, which climbed more than 2 percent, while Vietnam’s Ho Chi Minh Stock Index jumped 3.77 percent in the same time.

- Taiwan’s exports surprised to the upside this week, rising to a 14.8 percent growth rate for the December period, outperforming expectations for a pace of only 10.9 percent.

Weaknesses

- Korea’s KOSPI declined by a very mild 4 basis points, turning in a relatively weak performance in a mostly green week for the region.

- Year-over-year exports in the Philippines for the December period fell to a 1.9 percent growth rate, far underperforming expectations for a pace of 9.0 percent. Imports jumped, however, to 18.5 percent, much higher than the 9.7 percent that analysts expected.

- Aggregate financing, new yuan loans, and money supply all came in a little lighter than expected for China. Aggregate financing clocked in at 1.140 trillion yuan, shy of 1.500 expected, while new yuan loans came in at 584.4 billion, shy of 1.000 trillion expected. Both readings came in lighter than the prior. Money supply also dropped to 8.2 percent—shy of expectations for a 9.2 percent reading—from November’s 9.1 percent.

Opportunities

- Chinese airlines jumped this week after the government announced more freedom for carriers to price domestic flights.

- As North and South Korea started formal, and relatively low pressure, talks this week, South Korea’s President Moon specifically credited U.S. President Donald Trump for helping to move the North to dialogue and for openness to holding broader talks under appropriate circumstances. This is, perhaps, a step in the right direction. Possible free bonus: North Korea wants to send a delegation to the winter Olympics in South Korea (Sport, 1, Diplomatic resolutions, 0).

- Thailand announced this week that the country’s economy may expand by as much as 5 percent in 2018, as the government seeks to speed up spending and investment.

Threats

- Chinese officials clamped down on some bitcoin miners due to high power usage rates, Bloomberg News reported this week.

- The world’s second-biggest economy could be facing domestic-demand pressure, reports Reuters, as evidenced in a sharp slowdown in December imports. The pressure comes as authorities turn off cheap credit and restrict speculative financing, the article continues. Despite the slowdown last month, the overall picture for the economy shows strong global appetite for Chinese products.

- Regulators in South Korea have a history of hardline stances on speculative investments, Elaine Ramirez writes in Forbes this week, and cryptocurrencies are no exception. No official decision has made by the president’s office just yet, but according to Justice Minister Park Sang-ki on Thursday, the government is drafting legislation that could shutter all virtual currency exchanges in the country.

Emerging Europe

Strengths

- Ukraine was the best performing country this week, gaining 5.22 percent.

- The Czech koruna was the best performing currency this week, gaining 1.73 percent against the U.S. dollar. The annual inflation rate fell to 2.4 percent from 2.6 percent a month earlier, the Czech Statistics Office said on Wednesday. Czech price growth eased last month but remained above the central bank’s target as policy makers prepare further steps to cool one of Europe’s fastest-growing economies.

- Information technology was the best performing sector among eastern European markets this week.

Weaknesses

-

- Turkey was the worst performing country this week, losing 1.71 percent. Turkey’s current account deficit was reported at $4.2 billion, higher than the estimate at $3.85 billion. Turkey’s Foreign Ministry warned citizens to avoid travel to the U.S., citing the growing risk of terrorist attacks and other violence -- a day after the U.S. State Department said the same about Turkey. This tit-for-tat diplomacy adds to the recent deterioration in relations between the U.S. and Turkey.

- The Ukrainian hryvnia was the worst relative performing currency this week, losing 1.06 percent against the U.S. dollar.

Opportunities

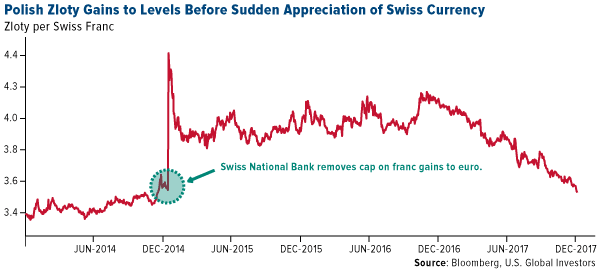

- The Polish zloty strengthened against the Swiss franc to the highest level since January 2015, when the Swiss central bank removed the currency peg to the euro, making popular Swiss franc mortgages more costly in Poland. Now there is a higher probability that the Polish government will not press banks into helping Swiss franc mortgage holders.

- Russian consumer inflation was reported at 2.5 percent in December, in line with estimates. Low inflation and a slowdown in economic activity are supportive of policy easing. JPMorgan’s research team expects 75 basis points cuts in the first half of the year, and additional 25 basis points cut is expected toward the end of the year. CEE countries like the Czech Republic and Romania started the tightening policy, and Russia could be the only country to keep its easing monetary policy in place.

- JPMorgan recommends overweighting Russia as the rise in oil is not priced into consensus earnings according to its oil versus earnings model. Russia is up 7.6 percent in the last 12 weeks versus 18.7 percent on average when oil is up by more than 19 percent. This gap in performance between Russia and oil could shrink.

Threats

- Poland’s new prime minister, Mateusz Morawiecki, put his stamp on the government Tuesday in a wide-ranging Cabinet reshuffle that saw many of the country’s most controversial ministers lose their jobs. It was a move designed to put more friendly faces in the government to the outside world. However, Zbigniew Ziobro, the Justice Minister who was responsible for the implementation of the controversial and highly criticized by European Commission judicial reform, kept his post.

- Months after elections took place in Germany the country is still without a government. German are hoping to enter the final state of the coalition talks very soon. Should they not be able to form a coalition, the only paths ahead would be a Merkel-led minority government or fresh elections.

- The European Central Bank has indicated it is preparing to cut is stimulus program faster. With the eurozone seeing its best growth in a decade, the ECB should gradually shift its stance to avoid a more disruptive move later and look at a broader revision of its policy guidance to reduce the focus on bond purchases and raise the emphasis on interest rates, accounts of the ECB's December meeting showed. Most ECB watchers still think quantitative easing will continue until September, but expectations of purchases continuing beyond that are diminishing.

Leaders and Laggards

|

Weekly Performance |

|||

|

Index |

Close |

WeeklyChange($) |

WeeklyChange(%) |

|

Russell 2000 |

1,591.97 |

+31.96 |

+2.05% |

|

S&P Basic Materials |

397.22 |

+3.03 |

+0.77% |

|

Nasdaq |

7,261.06 |

+124.50 |

+1.74% |

|

Hang Seng Composite Index |

4,365.36 |

+87.20 |

+2.04% |

|

S&P 500 |

2,786.24 |

+43.09 |

+1.57% |

|

Gold Futures |

1,339.10 |

+16.80 |

+1.27% |

|

Korean KOSPI Index |

2,496.42 |

-1.10 |

-0.04% |

|

DJIA |

25,803.19 |

+507.32 |

+2.01% |

|

S&P/TSX Global Gold Index |

200.38 |

+3.76 |

+1.91% |

|

SS&P/TSX Venture Index |

878.20 |

-17.51 |

-1.95% |

|

XAU |

89.11 |

+1.72 |

+1.97% |

|

S&P Energy |

572.02 |

+17.61 |

+3.18% |

|

Oil Futures |

64.41 |

+2.97 |

+4.83% |

|

10-Yr Treasury Bond |

2.55 |

+0.07 |

+2.91% |

|

Natural Gas Futures |

3.20 |

+0.41 |

+14.49% |

|

Monthly Performance |

|||

|

Index |

Close |

MonthlyChange($) |

MonthlyChange(%) |

|

Korean KOSPI Index |

2,496.42 |

+15.87 |

+0.64% |

|

Hang Seng Composite Index |

4,365.36 |

+337.64 |

+8.38% |

|

Nasdaq |

7,261.06 |

+385.26 |

+5.60% |

|

XAU |

89.11 |

+9.22 |

+11.54% |

|

S&P/TSX Global Gold Index |

200.38 |

+10.90 |

+5.75% |

|

Gold Futures |

1,339.10 |

+90.50 |

+7.25% |

|

S&P 500 |

2,786.24 |

+123.39 |

+4.63% |

|

S&P Basic Materials |

397.22 |

+24.66 |

+6.62% |

|

DJIA |

25,803.19 |

+1,217.76 |

+4.95% |

|

Russell 2000 |

1,591.97 |

+67.53 |

+4.43% |

|

SS&P/TSX Venture Index |

878.20 |

+79.63 |

+9.97% |

|

Oil Futures |

64.41 |

+7.81 |

+13.80% |

|

S&P Energy |

572.02 |

+60.98 |

+11.93% |

|

Natural Gas Futures |

3.20 |

+0.49 |

+17.86% |

|

10-Yr Treasury Bond |

2.55 |

+0.21 |

+8.79% |

|

Quarterly Performance |

|||

|

Index |

Close |

QuarterlyChange($) |

QuarterlyChange(%) |

|

Korean KOSPI Index |

2,496.42 |

+22.80 |

+0.92% |

|

Hang Seng Composite Index |

4,365.36 |

+400.32 |

+10.10% |

|

Nasdaq |

7,261.06 |

+655.26 |

+9.92% |

|

Natural Gas Futures |

3.20 |

+0.20 |

+6.67% |

|

Gold Futures |

1,339.10 |

+30.20 |

+2.31% |

|

S&P 500 |

2,786.24 |

+233.07 |

+9.13% |

|

S&P Basic Materials |

397.22 |

+31.62 |

+8.65% |

|

S&P/TSX Global Gold Index |

200.38 |

-2.40 |

-1.18% |

|

XAU |

89.11 |

+1.82 |

+2.09% |

|

DJIA |

25,803.19 |

+2,931.47 |

+12.82% |

|

Russell 2000 |

1,591.97 |

+89.31 |

+5.94% |

|

SS&P/TSX Venture Index |

878.20 |

+80.76 |

+10.13% |

|

S&P Energy |

572.02 |

+67.51 |

+13.38% |

|

Oil Futures |

64.41 |

+12.96 |

+25.19% |

|

10-Yr Treasury Bond |

2.55 |

+0.28 |

+12.09% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2017): Teck Resources Ltd.CopperBank Resources Corp. Klondex Mines Ltd.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The Bloomberg Commodity Index (BCOM) is a broadly diversified commodity price index distributed by Bloomberg Indexes. The index was originally launched in 1998 as the Dow Jones-AIG Commodity Index (DJ-AIGCI) and renamed to Dow Jones-UBS Commodity Index (DJ-UBSCI) in 2009, when UBS acquired the index from AIG.The S&P GSCI (formerly the Goldman Sachs Commodity Index) serves as a benchmark for investment in the commodity markets and as a measure of commodity performance over time. It is a tradable index that is readily available to market participants of the Chicago Mercantile Exchange.The Standard & Poor's 500 Index, often abbreviated as the S&P 500, or just the S&P, is an American stock market index based on the market capitalizations of 500large companies having common stock listed on the NYSE or NASDAQ. The S&P 500 index components and their weightings are determined by S&P Dow Jones Indices.The Purchasing Managers' Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.Frank Holmes has been appointed non-executive chairman of the Board of Directors of HIVE Blockchain Technologies. Both Mr. Holmes and U.S. Global Investors own shares of HIVE, directly and indirectly.The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange.M2 Money Supply is a broad measure of money supply that includes M1 in addition to all time-related deposits, savings deposits, and non-institutional money-market funds.S&P/TSX Capped Diversified Metals and Mining Index is an index of companies engaged in diversified production or extraction of metals and minerals.The S&P/TSX Global Gold Index is an international benchmark tracking the world's leading gold companies with the intent to provide an investable representative index of publicly-traded international gold companies.The National Federation of Independent Business’s (NFIB) Index of business optimism is based on responses from 1221 member firms.The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.The Bloomberg Barclays 3-Year Municipal Bond Index is a total return benchmark designed for short-term municipal assets. The index includes bonds with a minimum credit rating BAA3, are issued as part of a deal of at least $50 million, have an amount outstanding of at least $5 million and have a maturity of 2 to 4 years.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits