You'll Want to Read This Living Legend's Thoughts On Copper

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

This week the U.S. Global Investors office was visited by a living legend in the junior mining industry, billionaire founder and executive chairman of Ivanhoe Mines, Robert Friedland. In case you don’t know, back in the mid-1970s, Robert was caretaker of an apple orchard south of Portland that one of his buddies from Reed College would often visit. That buddy’s name was Steve Jobs, who later went on to found a little company he named—what else?—Apple.

Before Robert and Steve Jobs began palling around, Jobs was known as shy and withdrawn. It was Robert who taught him his skills in what’s been described by many as “reality distortion.” Having seen numerous speeches by Robert over the years, I can attest to his masterful ability to utterly command a room of hundreds with his electric charisma. Some of that charisma must have rubbed off on Jobs, helping the future iPhone innovator evolve into the shrewd, larger-than-life business leader he’s celebrated as today.

|

Robert’s “reality distortion” was on full display during his visit. I was pleased and honored, as were my U.S. Global team members, to have the opportunity to hear his unique insights on a wide range of issues, from the debilitating smog in Delhi, India; to China’s efforts to become the world’s leading electric vehicle (EV) economy; to Ivanhoe’s development of the Kamoa-Kakula Copper Project in the Democratic Republic of Congo, independently ranked as the largest high-grade copper discovery in the world.

Robert made a very compelling case for Kamoa-Kakula, which he calls “the most disruptive Tier One copper project in the world today.” In its first year of production, its average copper grade is estimated to average an ultra-high 7.3 percent. Because the site is flat and uninhabited, and wages are paid in local currency, the cash cost for the life of the mine is projected to be a low, low $0.64 per pound of copper. As of my writing this, copper is priced at $3.20 a pound, so the margin is significant. After an initial $1.2 billion in capital costs to develop the project, the company expects a payback period of only 3.1 years.

It’s all a very attractive proposition.

Robert Friedland: You're Going to Need a Telescope

I reminded Robert that we’re bullish on both copper and the industries it supports, including the imminent EV revolution and massive electricity demand in emerging markets, especially China and India. EVs, as I’ve pointed out before, require three to four times as much copper as traditional gas-powered vehicles. By 2027, as much as 1.74 million metric tons of copper will be needed to meet EV demand alone, up from only 185,000 tons today, according to the International Copper Association.

The red metal was one of the best performing commodities last year, surging more than 30 percent, and with investment demand near all-time highs, I predict another year of phenomenal returns. That would represent a third straight year of positive gains, something copper hasn’t accomplished this decade.

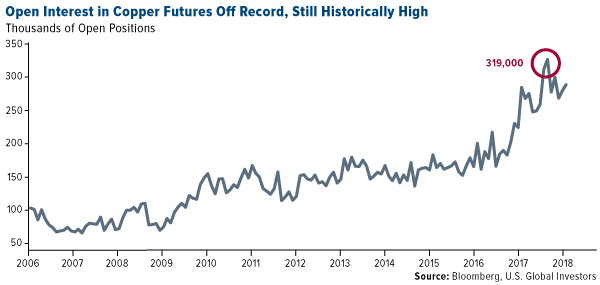

As you can see below, open interest in copper futures on the Chicago Mercantile Exchange (CME) is still historically high, even after cooling somewhat from its all-time high set in late July, when contracts hit an average 319,000 contracts. Open positions last month averaged more than 285,000, up 7.3 percent from the previous month and 26.9 percent from December 2016.

Robert expressed confidence that copper—along with aluminum, cobalt, nickel, platinum and scandium—will be among the biggest beneficiaries of the global transition to EVs and clean energy.

“You’re going to need a telescope to see copper prices in 2021,” he told us theatrically.

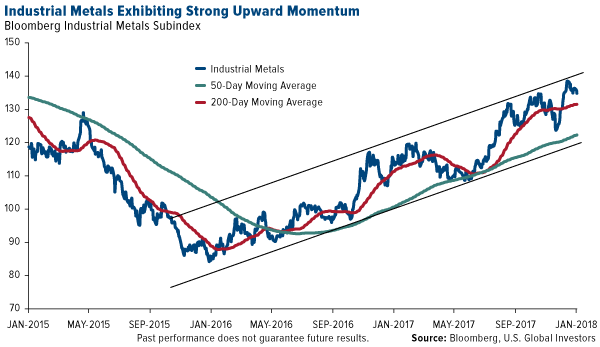

A rally is already in the works. From its recent low two years ago this month, the Bloomberg Industrial Metals Subindex, which tracks aluminum, copper, nickel and zinc, has surged more than 65 percent. Support looks strong, and copper prices could be headed even higher on global supply disruptions, as labor negotiations continue in Chile, the world’s top producer of the red metal.

“There are between 20 and 25 collective negotiations expected. If some of them lead to significant strikes, that would have a positive impact on [copper] prices,” explained Sergio Hernandez, vice president of Cochilco, Chile’s state copper commission.

Other fundamental trends are driving commodities, as I’ve noted earlier. The global purchasing manager’s index (PMI), a gauge of the manufacturing industry, is near a seven-year high. Construction confidence in the eurozone turned positive. And construction spending here in the U.S. hit $1.257 trillion in November, a new high.

China and India Cleaning Up Its Act

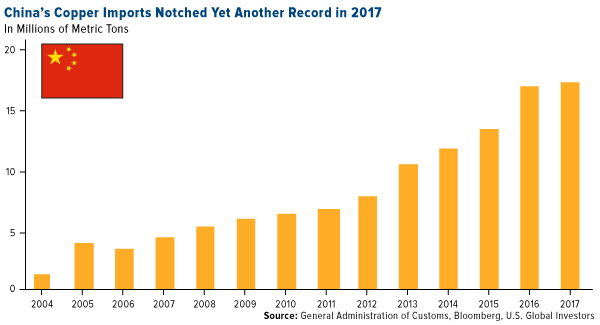

About half of all the copper produced globally every year is consumed by China. Last year, the Asian giant set a new record in importing the red metal. Imports climbed to a never-before-seen 17.35 million metric tons in 2017, up 2.3 percent from the previous year.

The metal is needed not just for the construction of new buildings but also to manufacture millions of new electric vehicles in the world’s largest auto market. Sometime this year, China is expected to announce when it plans to outlaw gas-powered vehicles, joining a growing number of other countries, including the U.K. (which is shooting for a 2040 ban), France (2040), Germany (2030), India (“next 13 years”) and more.

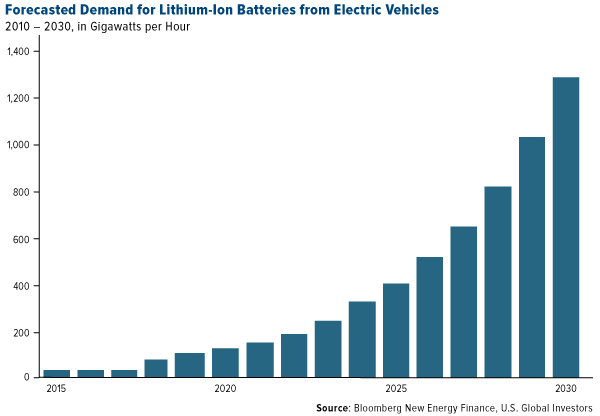

According to Bloomberg New Energy Finance, about 1,293 gigawatts per hour (GWh) are forecast for the lithium-ion battery market. That’s up spectacularly from only 19 GWh in 2015. About two thirds of the demand will come from China and the U.S.

To accommodate all these new EVs, China has pledged to build a charging station for every vehicle on the road by 2020. That equates to around 4.8 million charging outlets and stations, requiring a total investment of $19 billion. China had 190,000 charging stations at the end of September, so to call this goal ambitious is an understatement. The U.S., by comparison, has a little over 64,000 outlets and stations around the country, according to the Department of Energy.

Even William Ford Jr., Ford Motor’s executive chairman, acknowledged that the Chinese are more aggressive than most in their mission to fully embrace the electric vehicle. “When I think of where EVs are going,” Ford said in Shanghai last month, “it’s clearly the case that China will lead the world in EV development.”

Not only was China the largest importer of copper, crude oil, natural gas and other natural resources, it also outspent every other country in new clean energy capacity. The country invested as much as $132.6 billion in 2017, about 16 percent more than the U.S. and Europe combined. The government’s efforts already seem to be having a positive effect, as sales of face masks and air purifiers in Beijing have fallen dramatically compared to last winter.

Another market that’s in urgent need of clean energy is India. In Delhi, the country’s capital territory, the air quality has become so noxious and filled with heavy metals that the World Health Organization has likened it to smoking at least 50 cigarettes a day. The city’s chief minister, Arvind Kejriwal, went so far as to call it a “gas chamber.”

Shell Shelling Out for Electricity Provider

It’s not just governments seeking to diversify their energy mix. Royal Dutch Shell, the largest oil company in Europe, is steadily acquiring smaller providers of electrical power and natural gas. In December it announced a deal to buy retail energy provider First Utility. It’s just the latest in a series of purchases by large oil and gas companies looking ahead to the day when charging stations, rather than gas stations, might be the norm.

In an interview this month, Shell CEO Ben van Beurden sees the current energy transition as an opportunity.

“We have to embrace the future, and the future will include battery electric cars,” van Beurden said. “Importantly, I believe Shell can achieve this without destroying value in the company. It is about identifying real business opportunities to thrive through the energy transition.”

As my friend Robert Friedland sees it, those business opportunities lie in copper, aluminum, cobalt and other key industrial metals.

“We’re in the battery business,” he told us, adding that very little of lithium-ion batteries is actually lithium.

Racing for Bitcoin

At the moment I’m in Delray Beach, Florida, attending the Black Diamond Investment Conference, where I was excited to see a 2007 Lamborghini Murcielago for sale. It wasn’t so much the fact that it was a Lamborghini but that the sellers were seeking payment in cryptocurrency only. In case you have 48 bitcoins lying around—valued at a little over half a million dollars at today’s price—you could be the proud new owner of a top-quality sports car. I’m pleased to see even more transactions being made in bitcoin and other cryptocurrencies.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.04 percent. The S&P 500 Stock Index rose 0.86 percent, while the Nasdaq Composite climbed 1.04 percent. The Russell 2000 small capitalization index gained 0.36 percent this week.

- The Hang Seng Composite gained 2.31 percent this week; while Taiwan was up 2.45 percent and the KOSPI rose 0.95 percent.

- The 10-year Treasury bond yield rose 10 basis points to 2.66 percent.

Domestic Equity Market

Strengths

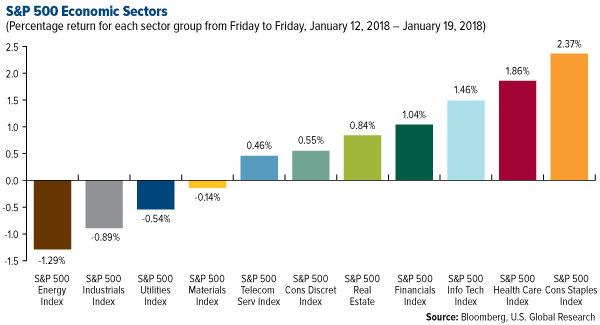

- Consumer staples were the best performing sector of the week, increasing by 2.37 percent versus an overall increase of 0.77 percent for the S&P 500.

- Lam Research was the best performing stock for the week, increasing 10.09%.

- Morgan Stanley beat Wall Street expectations on quarter four earnings despite a big hit to trading revenue. The firm reported adjusted earnings of $0.84 a share, surpassing the consensus analyst estimate of $0.77 a share.

Weaknesses

- Energy was the worst performing sector for the week, falling 1.29 percent versus an overall increase of 0.77 percent for the S&P 500.

- General Electric was the worst performing stock for the week, falling 13.33 percent.

- General Electric shares fell for a fifth straight session on Friday and were on the cusp of their biggest weekly percentage drop since the financial crisis after the company flagged a possible breakup and more than $11 billion in charges earlier in the week.

Opportunities

- If you’re looking for detail on what’s driving the stock market’s record-breaking surge, all you need to do is chart the S&P 500 against major corporate earnings releases. Doing this shows the degree to which the S&P 500 has tracked corporate earnings revisions, with a recent spike in revisions pushing the index to new all-time highs.

- Apple announced it plans to contribute $350 billion to the U.S. economy over the next five years. The plan sees the company repatriating overseas profits, implementing new infrastructure projects and hiring about 20,000 new employees.

- Microsoft is bringing the Surface Book 2 - in both the 13- and 15-inch versions - to all markets where the Surface brand is already present. The initial rollout will bring the new models to 17 countries, with more to follow throughout March and April.

Threats

- A key metric is flashing the stock market at 'extreme' levels that are the most stretched in 20 years. While the measure - the relative-strength index - being overextended does not necessarily mean a correction is imminent, it should give investors caution as they consider adding to positions going forward.

- Intel has admitted the Spectre and Meltdown patches have impacted the performance of a broad range of processors. Those include chips of the Ivy Bridge, Sandy Bridge, Skylake, and Kaby Lake families, with a performance impact between 2 and 25 percent.

- Stock market volatility was locked near record lows for much of 2017 and Credit Suisse says it has nowhere to go but up.

January 16, 2018"Quants Have Taken Over" |

January 16, 2018"Recipe Calls for a Broad Commodities Rally in 2018" |

January 9, 2018Emerging European Markets Ended 2017 up 20 Percent |

The Economy and Bond Market

Strengths

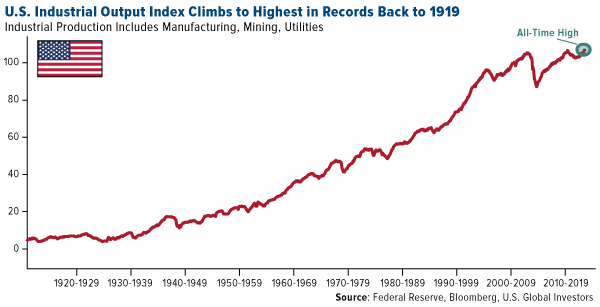

- America’s industrial production hasn’t been this strong in almost a century, according to one gauge from the Federal Reserve. A strong run at factories, improvement in mining and a colder-weather boost to utilities lifted December’s industrial output index 0.9 percent to 107.46, the highest in records back to 1919.

- Capacity utilization rose to 77.9 percent in December, the highest rate since February 2015. This was up from the previous month’s rate of 77.1 percent and beat forecasts of 77.4 percent.

- San Francisco Fed President John Williams said three rate increases this year still make sense, as the risks to the economy are balanced, and the economy could perform better than expectations.

Weaknesses

- U.S. home building fell more than expected in December, recording its biggest drop in just over a year, amid a steep decline in the construction of single-family housing units. Housing starts decreased 8.2 percent to a seasonally adjusted annual rate of 1.192 million units, the Commerce Department said. November's sales pace was revised up to 1.299 million units from the previously reported 1.297 million units. Economists polled by Reuters had forecast housing starts decreasing to a pace of 1.275 million units last month.

- Consumer sentiment unexpectedly declined in January to a six-month low as households viewed the economy less favorably. Sentiment index dropped to 94.4 from 95.9 in December, while the forecast was 97.

- The New York Federal Reserve’s index of manufacturing conditions began 2018 with a worse-than-expected expansion. In a report, the Federal Reserve Bank of New York said that its general business conditions index fell to 17.70 this month from a reading of 19.60 in December. Analysts had expected the index to hold steady at 18.00 in January.

Opportunities

- The U.S. data highlight of the week will be Friday's advance Q4 GDP report. An average of the Atlanta and NY Feds' nowcasts stands at a solid 3.7 percent. Other notable U.S. data releases will be the Conference Board's leading economic indicator (Thursday) and durable goods orders (Friday). The former should signal accelerating growth and the latter should show an improving outlook for business investment.

- Residents in New York, New Jersey and Connecticut who waited in queues to pay their property taxes early and take advantage of an expiring tax deduction may line up in 2018 to buy municipal bonds issued in their home states. Strategists from Barclays and Charles Schwab say demand for munis could increase in high tax states this year as the Republican tax bill caps state and local property and income tax deductions at $10,000.

- The state of New York is looking to end income taxes on wage earners and make up the revenue with an employer payroll tax that is federally deductible. This measure is part of a restructuring plan that Governor Andrew Cuomo is recommending in order to mitigate harmful effects of the new federal tax code.

Threats

- Puerto Rico’s fiscal turnaround plan may have been doomed from the start, even before Hurricane Maria swept across the island, according to a study by a group of economists including Nobel Prize winner Joseph Stiglitz. The roadmap, which island officials are revising in light of the storm, underestimated the degree to which austerity would slow economic growth, wrote Pablo Gluzmann, Martin Guzman and Stiglitz.

- The dollar dipped near 3-year lows amid fears of a US government shutdown. The dollar has already lost 2 percent in the early days of 2018, reflecting investor nervousness, Reuters reported.

- In the wake of debates following the FCC's decision to repeal net neutrality rules in the US, a Harvard study found that community-owned broadband prices are up to 50 percent cheaper than the lowest services offered by ISPs. These services are also more transparent, less confusing, and more practical to deal with for customers.

Gold Market

This week spot gold closed at $1,332.14, down $5.81 per ounce, or 0.43 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.13 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index rose 0.26 percent. The U.S. Trade-Weighted Dollar fell 0.35 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-16 | Germany CPI YoY | 1.7% | 1.7% | 1.7% |

| Jan-17 | Eurozone CPI Core YoY | 0.9% | 0.9% | 0.9% |

| Jan-18 | China Retail Sales YoY | 10.2% | 9.4% | 10.2% |

| Jan-18 | Housing Starts | 1275k | 1192k | 1299k |

| Jan-18 | Initial Jobless Claims | 249k | 220k | 261k |

| Jan-23 | Germany ZEW Survey Current Situation | 89.5 | -- | 89.3 |

| Jan-23 | Germany ZEW Survey Expectations | 17.9 | -- | 17.4 |

| Jan-25 | Hong Kong Exports YoY | 7.2% | -- | 7.8% |

| Jan-25 | ECB Main Refinancing Rate | 0.00% | -- | 0.00% |

| Jan-25 | Initial Jobless Claims | 235k | -- | 220k |

| Jan-25 | New Home Sales | 675k | -- | 733k |

| Jan-26 | GDP Annualized QoQ | 3.0% | -- | 3.2% |

| Jan-26 | Durable Goods Orders | 0.9% | -- | 1.3% |

Strengths

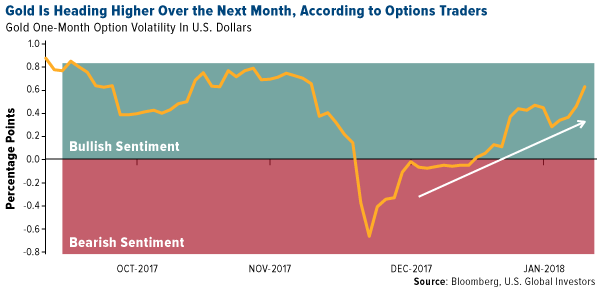

- The best performing metal this week was platinum, up 1.92 percent as traders boosted their net long position. Gold traders remain bullish on the yellow metal for a second week as gold reached the highest since September on Monday, reports Bloomberg. The U.S. dollar posted five straight weekly losses, even as U.S. Treasury yields rose. Earlier in the week, 5,000 call options with a strike of $1,650 on gold were purchased, indicating a bullish view on the price of the metal.

- Bullion is up in reserve currencies such as yen, euros and pounds, which might show there is some instrinsic value in gold’s rally. This could be due to concerns of global inflation or an imminent stock market correction, according to Fawad Razaqzada, an analyst at Forex.com.

- This week ETF holdings rose to their highest since 2013 and holdings in gold ETFs jumped to 13.7 tons, the most since September. Indian gold imports rose 53 percent in 2017, from 550 tons imported in 2016, to 846 tons last year.

Weaknesses

- The worst performing metal this week was palladium, down 1.59 percent as traders lowered their longs this past week. Bloomberg Intelligence highlighted that conditions favor platinum over palladium based on history. The top three North American gold producers – Barrick Gold, Newmont Mining and Goldcorp – have all seen their bondholders reap greater rewards for less risk than their equity investors, according to Bloomberg. Share performance of the three companies has been mixed for a year with their bonds outperforming their stocks.

- SQM, one of the largest lithium producers, secured a deal with the Chilean government to boost annual capacity at its mine from 66,000 tons to 216,000 tons. This could potentially flood the market, as other lithium stocks fell sharply this week at the news of potential oversupply.

- The U.S. Treasury views digital currencies as an evolving threat and it might be pulling money away from investors in gold, according to Bloomberg. When Bitcoin fell below $10,000 briefly this week, investors sharply turned to see if they could invest in gold. This demonstrates gold as being seen as a safe-haven investment versus volatile cryptocurrencies, however, it also shows investors may have left gold for the new currencies.

Opportunities

- According to Bloomberg, silver may stand to benefit the most from cryptocurrency falls, thanks to strong global PMIs and a weak U.S. dollar. Bart Melek from TD Securities released a 2018 outlook saying “Considering silver’s underperformance, its traditionally higher volatility and historic relative strength during periods when investors are building gold exposure; the white metal is on track to outperform.”

- Gold might continue to rally as demand in China is strong during this year’s Chinese New Year buying season. The yellow metal is also trading near the cheapest relative to crude oil in more than two years, according to Bloomberg. Bloomberg Intelligence analyst Mike McGlone said the gold-oil ratio has backed up into the key support zone favoring gold.

- Institutional investors are showing renewed interest in gold due to a weakening U.S. dollar and higher bond yields. Speaking to Bloomberg News, Sprott Asset Management’s CEO John Ciampaglia said that investors don’t think there will be a gold price rally; rather, they are seeking a safe haven for their assets. Sprott also said it is seeing increasing interest in investing in mining and gold ETFs.

Threats

- The world’s major gold producers have cut back on mergers and acquisitions with industry transactions totaling just $8.95 billion in 2017, tumbling by a third from the previous year, according to Bloomberg. In a rush to boost output in 2011 when gold was at an all-time high of $1,921.17 an ounce, companies spent a record $38.7 billion on acquisitions. The lack of takeovers may signify that the gold market is nowhere near a top at this point.

- Bond traders are piling into Treasury Inflation Protected Securities, TIPS, as a measure to purchase inflation protection. This could potentially backfire as the flattening of the U.S. yield curve have sent the spread between 30- and 10-year breakeven rates below zero for the first time since 2013, writes Bloomberg. When this spread turns negative it’s colloquially referred to as the “widowmaker” trade as it has led to quick and sharp losses such as during the taper tantrum which gripped bond markets in 2013.

- Since the recently passed tax overhaul, large corporations have stated they will be bringing back to the U.S. billions in cash stored overseas. This significant unloading of cash might strengthen the dollar, which is historically bad for the price of gold. Many think the repatriating of money will lead to distributions to shareholders, rather than promises of the Trump administration for companies to reinvest in their own businesses.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by Bloomberg, the best performing for the week ended January 19 was bitcoin, which lost 18.05 percent.

- An evangelical church in Switzerland began accepted bitcoin as an offering, according to local media reports. Nicolas Legler, spokesperson for Zurich’s ICF Church, told Swiss media on Wednesday that “digital currencies and the blockchain technology will change our daily lives more and more in the next years,” reports Newsweek.

- Blockchain, a U.K.-based digital currency wallet, expanded into the U.S. market this week, challenging Coinbase. The company already allows its British customers to buy and sell bitcoin via its service, reports CNBC, and is now launching the function in one of the biggest cryptocurrency markets in the world.

Weaknesses

- Of the cryptocurrencies tracked by Bloomberg, the worst performing for the week ended January 19 was ripple, which fell 23.56 percent.

- On Tuesday, former Wells Fargo Chairman and CEO Dick Kovacevich told CNBC that he believes bitcoin is a scam or a pyramid scheme. “It makes no sense,” he said. “I’m just surprised it isn’t even lower.” Although just last week Jamie Dimon, CEO of JP Morgan, retracted his earlier criticisms on the space, Kovacevich joins a growing list of bankers who have denounced the cryptocurrency craze, CNBC writes.

- Bitcoin fell to below $10,000 this week, reports CNBC, losing $30 billion market value in 24 hours. “Focus has shifted to negative regulation with headlines out of South Korea, China and even minor headlines from France and the U.S.,” Ari Paul, CIO of BlockTower Capital (a cryptocurrency investment firm), said in an email.

Opportunities

|

- The Dallas Mavericks will begin accepting cryptocurrency payments during their next season, reports CoinDesk.com. Owner and investor Mark Cuban was asked about the possibility of paying for tickets with cryptocurrency on Twitter this week, to which he replied “next season,” and later confirmed to CoinDesk, along with “possibly some other currencies.”

- Crypto bull Thomas Lee isn’t discouraged by bitcoin’s recent slide, reports Bloomberg. In fact, Lee predicts the value of cryptocurrencies will climb to more than $1.2 trillion this year. Lee also believes Ethereum will climb to $1,900 by the end of this year, the article continues.

- In a whitepaper released this week, the St. Louis Fed writes that blockchain presents a number of “promising applications,” including not just currency but also smart contracts and data integrity. According to the group “cryptoassets are well suited to become an important asset class.”

Threats

- Reality Shares and Amplify ETFs are both launching blockchain ETFs this week, reports Business Insider. However, there’s a catch to these launches, explains Eric Ervin, chief executive of Reality Shares. Ervin says the SEC is wary about the mania surrounding blockchain, so has requested that the term “blockchain” be removed from the names of the ETFs.

- The U.S. Treasury has warned investors in the U.S. about Venezuela’s proposed “petro” currency, writes Reuters. “It may contravene U.S. sanctions against the government of Venezuelan President Nicolas Madura,” the article continues. A spokesman from the Treasury told Reuters that the petro currency appears to be an extension of credit to the Venezuelan government, therefore exposing U.S. persons to legal risk.

- In a closed-door meeting on Wednesday, the People’s Bank of China allegedly outlined a plan to limit power use by some bitcoin miners, reports Bloomberg. According to people familiar with the matter, Chinese officials are concerned that bitcoin miners have taken advantage of low power prices in some areas and affected normal electricity use in some cases,” the article reads.

Energy and Natural Resources Market

Strengths

- Iron ore was the best performing major commodity this week, rising 6.4 percent. The commodity rallied despite Chinese port inventories hitting record highs, as steel mills announced they are set to continue building inventory ahead of the Chinese New Year celebrations, which normally lead to a rebound in industrial activity.

- The best performing sector this week was the NASDAQ Clean Edge Index, which tracks renewable energy companies. The index rose 1.5 percent for the week despite solar power companies closing the week lower, as chip makers rallied on the back of a successful sequence of meetings at the CES conference in Las Vegas last week.

- The best performing stock for the week was Braskem SA. The major Brazilian petrochemicals company rose 9.9 percent after press reports suggest that the corporate links between defamed Brazilian giant Odebrecht and Braskem were legitimate and not used to hide illegal activities.

Weaknesses

- Both thermal and metallurgical coal prices dropped this week. The commodities dropped as coal’s share of China’s energy mix slipped further as the world’s biggest consumer and producer of the fuel seeks cleaner sources to satisfy its growing energy use. Coal’s share of total energy consumption inched lower by 1.7 percentage points last year, while natural gas, hydro, nuclear, wind and other less-polluting sources gained 1.5 percentage points.

- The worst performing sector this week was the S&P/TSX Diversified Metals and Miners Index. The index dropped 3.3 percent, as industrial commodities dropped lower on the week, but also dragged lower by Turquoise Hill Resources, the base metals producer operating in Mongolia, which declared force majeure for its shipments due to an unrelated road blockade at the Chinese border.

- The worst performing stock for the week was FMC Corp. The major fertilizer company, which is considered one of the three global major lithium producers, dropped 8.4 percent on concerns of lithium market oversupply after SQM, the largest producer, reached a deal to ramp up production in Chile.

Opportunities

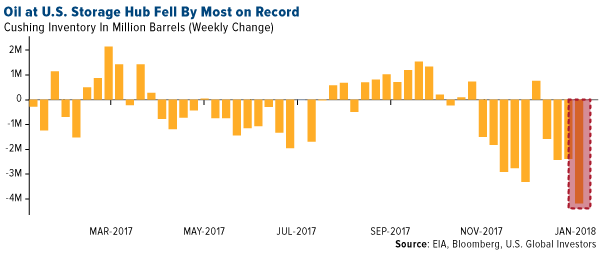

- Oil supplies at the biggest U.S. storage hub dropped most on record. U.S. crude oil inventories in Cushing, Oklahoma, fell 4.18 million barrels last week, the biggest drop since 2004. That brought supplies to the lowest level since January 2015, suggesting the market may have rebalanced. Growing foreign demand for America’s crude and strong margins at U.S. refineries keeps oil flowing out of storage tanks, even as U.S. production continues to rise.

- China’s renminbi rose after Germany’s central bank said it would include the currency in its reserves, a move seen as boosting the internationalization of China’s currency. A stronger Chinese currency is favorable for commodity demand as it makes imports of raw materials into China more accessible for processing companies and consumers at the world’s largest raw material importing nation.

- China’s economy grew at 6.9 percent in 2017, the fastest pace in two years, despite policymakers making headway towards curbing financial risk from excessive debt. The country’s 6.8 percent growth for the fourth quarter locked in China’s first yearly gross domestic product acceleration since 2010. Net exports contributed 0.6 percentage points to overall growth, the highest contribution since 2008, as a buoyant global PMIs boosted trade, according to the Financial Times.

Threats

- Secretary of Commerce Wilbur Ross formally submitted to President Donald J. Trump the results of the Department’s investigation into the effect of steel mill product imports. The President has 90 days to decide on any potential action based on the findings of the investigation. In theory, analysts suspect the government may introduce tariffs on steel and aluminum imports, which may be beneficial for domestic U.S. producers, but may exert downward pressure on global steel, aluminum and iron ore prices.

- U.S. oil and gas producers are among companies hit hardest by new restrictions on tax relief for interest payments. The new tax code sets limits on deductions for interest payments, which will put pressure on heavily indebted companies to reduce their borrowings, and could push over-burdened companies into steeper decline if their earnings fall. Companies in industries including oil and gas, coal mining, and trucking are among those likely to be most affected, according to the Financial Times analysis.

- In its latest monthly report, OPEC warned that according to secondary sources, December oil production by the cartel rose by 42.4 thousand barrels per day from November. In addition, non-OPEC supply is expected to expand by almost 1.2 million barrels a day this year, a sizeable upward revision to previous expectations. With oil prices having advanced nearly 50 percent in the past six months, both OPEC and the IEA are revising supply growth upward for 2018, which could cap the advance is energy prices.

China Region

Strengths

- Several indices put in new 52 week and/or all-time highs in a green week for the region. India’s SENSEX Index finished up a whopping 2.66 percent, while Taiwan’s TWSE Index closed up 2.45 percent on the week. Hong Kong’s Hang Seng Composite also put in a strong showing, finishing up 2.31 percent over the last five trading days, and notably the blue chip Hang Seng Index put in record highs.

- The Chinese yuan has quietly strengthened—as the U.S. dollar has weakened—and this week climbed to the 6.4 level for the first time since 2015.

- China released its fourth quarter GDP numbers this week, which also affords China-watchers a final 2017 GDP reading. Fourth quarter numbers clocked in at 6.8 percent year-over-year growth, beating estimates for 6.7 percent, while overall 2017 GDP finished at 6.9 percent, beating final full year analysts’ estimates for 6.8 percent, as China both adds to and profits from the tailwinds of synchronized global growth. China thus posts its first full-year growth since 2010.

Weaknesses

- This was, quite frankly, a green week for the region, but Malaysia’s FTSE KLCI finished up only 34 basis points, while Thailand’s SET closed up 63 basis points.

- China retail sales actually underperformed expectations, as year-over-year numbers for the December period came in at 9.4 percent, below estimates for a showing of 10.2 percent and down from November’s reading of 10.3 percent.

- Both imports and exports missed by a little bit in Indonesia this week. Year-over-year imports declined to a gain of 17.83 percent, shy of estimates for 18.13 percent and also down from the prior month’s reading of 19.62 percent. Exports were a much bigger miss: a gain of only 6.93 percent, well below estimates for 13.85 percent and down from November’s reading of 13.18 percent.

Opportunities

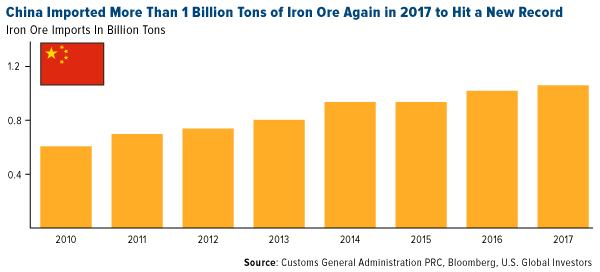

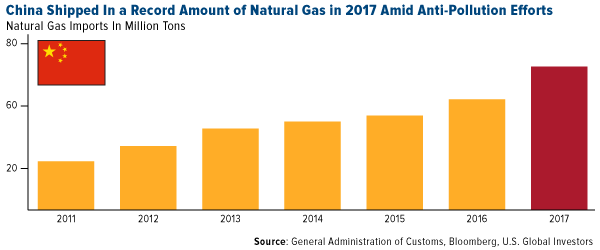

- Amid the backdrop of seemingly steady global growth China’s fourth quarter and overall 2017 numbers certainly provide cause for some optimism. On a slightly more specific level, it remains worth noting that as China seeks cleaner skies it has imported record amounts of less-polluting (as opposed to coal) iron ore and natural gas.

- Thailand’s foreign tourist arrivals jumped 15.5 percent, Bloomberg reports, to a record 3.5 million, according to the most recent release by the Thai government. Tourism throughout the region—powered by a growing Chinese middle class—remains an ongoing theme.

- Urbanization—with all its admitted difficulties—continues to drive that middle class theme, as China reported that 2017’s urbanization rate was 58.52 percent, climbing more than 1 percent from 2016, according to Bloomberg.

Threats

- Continuing the urbanization theme is the ongoing issue of housing prices in China. This week the authorities released the latest new home price data for China, which showed prices up in 57 major cities, higher than the prior month’s gain in only 50 cities. Despite some cooling in the mainland market, housing remains a double-edged sword, in some ways, and spots like Hong Kong have seen tremendous demand despite various attempts to curb it.

- Continuing the housing and Hong Kong topics a step further, it must be noted that the discussion about developing more land in an attempt to alleviate China’s housing issues comes up more frequently now. Of course, one must acquire land in order to develop it, but with the deleveraging campaign in full swing, the issuance of debt has proven moderately more challenging. Country Garden Holdings issued a share sale instead this week, raising a substantial sum to fund its war chest for development, which may send other property developers scrambling to follow suit.

- The coordinated cryptocurrency crackdown continues, as South Korea and China expand and consider additional measures to counteract trading and speculation in their respective countries while encouraging similar efforts in others’.

Emerging Europe

Strengths

- Poland was the best performing country this week, gaining 2.1 percent. Strong economic data supported fund flows to the country. The Warsaw stock exchange soared to a four-year high, led by a banking stocks rally.

- The Czech koruna was the best performing currency this week, gaining 60 basis points against the U.S. dollar. This strengthening occurred despite political noise.

- The information technology sector was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 42 basis points. However, there is some profit-taking in Greece after banks rallied more than 50 percent in the past two months.

- The Turkish lira was the worst performing currency this week, losing 1.5 points against the U.S. dollar. The lira weakened after the president of Turkey, Recep Tayyip Erdogan, warned of an attack on the Syrian Kurds in northwest Syria. The central bank left its main interest rate unchanged, as expected.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

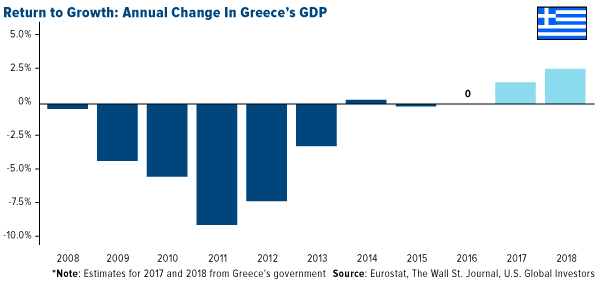

- The Greek parliament approved another package of reforms that will pave the way for creditors to release the next tranche of bailout funds, which is expected to be between 6 and 7 billion euros. Greece is expected to end the country’s bailout program this summer and it should be able to meets its financial needs without support from creditors. The country began growing again last year after nearly a decade of recession. According to official estimates, it could grow 2.5 percent in 2018.

- Romania quickly agreed on a new prime minister after Mihai Tudose resigned on Monday following crisis talks over his plans to reshuffle the cabinet. Viorica Dancila is set to become Romania’s third premier in a year. A European Parliament lawmaker and ally of ruling-party boss Liviu Dragnea, Dancila would be the first women to take the job of prime minster. Her next steps will be to select a cabinet, win a confidence vote - scheduled for January 29 - and lead a more stable government.

- European banks are cleaning their balance sheets, and the amount of non-performing loans (NPL) is falling. The European Commission said NPL’s accounted for 4.6 percent of bank’s total loans in second quarter of 2017. This is a one percentage drop from a year earlier. Banks in Greece still have nearly half of its loans classified as NPLs, while Germany and Netherlands have less than 3 percent. The Commission is planning new legislation in March that will allow banks to speed up the process of cleaning their balance sheets of bad debts.

Threats

- Eurozone inflation is not moving higher to the central bank’s target of 2 percent. The final December consumer price index (CPI) was reported at 1.4 percent. This is in line with the six month average but a tick below the twelve month average, according to Macro Strategy Research. Core inflation rose 0.9 percent, which is below both the six and twelve month moving averages of 1.0 percent. Energy and unprocessed food prices rose the most.

- According to Wall Street Journal, bullish speculative bets on oil futures are at the highest level ever. Typically, that is a sign of overconfidence and the market tends to fall. When price of oil falls, the Russian stock market usually follows its path. Russian equites may also be under pressure when the Treasury report comes out on January 29, analyzing the implications of sanctions of sovereign ruble bonds.

- Political instability has increased in central Eastern Europe. Last month, Poland replaced its prime minister and reshuffled its ministers recently. Romania’s new prime minister was appointed this week. Three months after Andrej Babi’s party won the general election in the Czech Republic without an outright majority, his government quit following its failure to secure approval in parliament. During this past weekend, presidential elections took place in Czech Republic, but current President Milos Zeman failed to win in the first round of elections. He will face a runoff in two weeks.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits