Russ discusses why the case for emerging market stocks right now simply rests on concept of solid global growth.

The mood in Davos was buoyant and the IMF just upgraded estimates for global growth. Cynical investors could be forgiven for viewing both of these developments as contrary indicators. Nonetheless, growth does appear solid, with most real-time and leading indicators suggesting some acceleration.

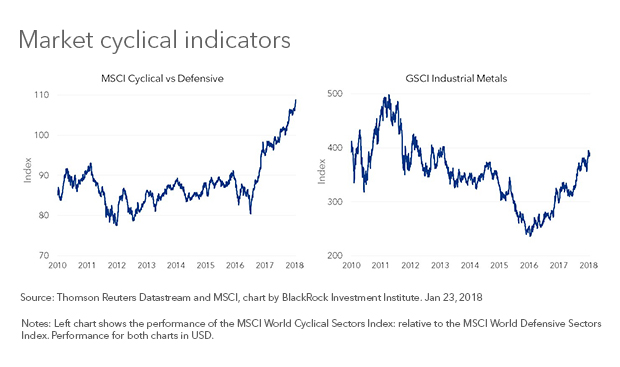

Given the run-up in economically sensitive assets, many investors appear to be buying into this thesis; witness the surge in industrial metal prices (see the chart below). For investors looking for an equity play on global growth, consider a higher allocation to emerging market (EM) equities.

It’s not just about the dollar

Before focusing on the case for emerging markets, it is worth disposing of two myths: EM stocks are cheap and they are a play on a weak U.S. dollar. While both have some validity, they oversimplify the case.

Today, like most asset classes, EM stocks cannot really be described as cheap. They are trading close to their historical norm, both on an absolute basis and relative to developed markets; the MSCI Emerging Market Index is currently trading at about a 25% discount to developed markets, in line with the long-term and post-crisis average.

Many investors would also point to a weak dollar as a catalyst for EM stocks. The truth is more nuanced. Historically, there has been a negative relationship between EM stocks and the direction of the dollar. That said, the relationship is modest, explaining less than 2% of the variation in monthly relative returns. And even that may not be the case going forward. To the extent EM countries have become less dependent on dollar funding and have improved their current account balances, they are less vulnerable to changes in the dollar.

A levered play on global growth

Rather than valuations or the dollar, the best case for EM equities ties back to global growth. Although global GDP is difficult to measure in real time, historically, changes in industrial metal prices have been a reliable proxy. If emerging markets are a levered play on global growth, they should be more inclined to outperform when industrial commodities are rising. Historically, this is exactly what has happened.

Looking at quarterly data, since 1990 every one percentage point rise in industrial commodity prices (using the JOC Industrial Metals Index) has translated into roughly 0.30% outperformance by emerging markets. Put differently, in quarters when industrial metal prices rose, emerging market equities outperformed developed markets by roughly 3.5% on average. Conversely, during quarters when industrial metal prices were declining, emerging markets underperformed by approximately 2.5%.

The takeaway is that industrial commodities, along with broader leading indicators, suggest growth should remain solid and is likely to accelerate from last year’s pace. Should this prove to be the case, EM equities potentially have further to run.

Russ Koesterich, CFA, is Portfolio Manager for BlackRock’s Global Allocation team and is a regular contributor to The Blog.

Investing involves risks, including possible loss of principal. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of January 2018 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

©2018 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

412736

© BlackRock

Read more commentaries by BlackRock