A $1.5 Trillion Opportunity You Don’t Want to Miss!

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

On the campaign trail, then-presidential candidate Donald Trump pledged to invest as much as $1 trillion in U.S. infrastructure if he were elected. This week during his first State of the Union address, now-President Trump added half a trillion dollars more to that figure.

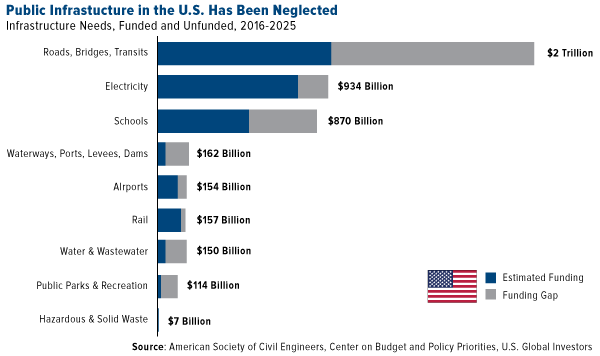

The hefty price tag likely raised some eyebrows among Congress members, but Trump is right in aiming high to fix the country’s “crumbling infrastructure,” as he calls it. According to the American Society of Civil Engineers (ASCE), the U.S. faces an infrastructure funding gap of more than $2 trillion between now and 2025, resulting in potential losses of nearly $4 trillion in gross domestic product (GDP), or $34,000 per household.

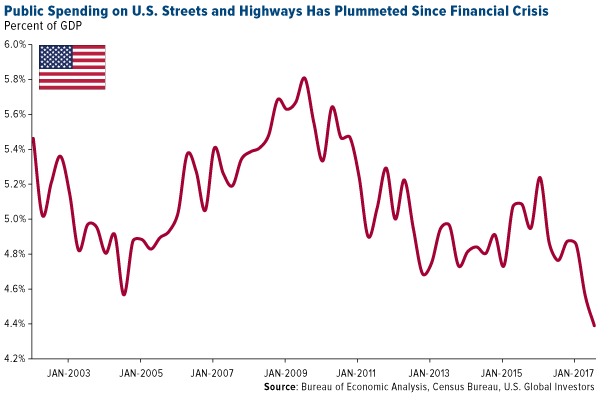

Take a look at public spending on U.S. streets and highways as a percent of GDP. Since the financial crisis a decade ago, investment has tanked, and anyone who regularly drives can see firsthand the consequences of this negligence. Americans spend 42 hours on average sitting in congestion every year, costing each driver roughly $1,400, and this week the American Roads & Transportation Builders Association (ARTBA) reports that more than 54,000 of the country’s 612,677 bridges are rated “structurally deficient.”

Anticipating a shift in priority toward infrastructure, contractors and construction firms are gearing up to take on new projects, with a whopping 75 percent of them planning to expand their headcount this year. This comes after an estimated 192,000 new construction jobs opened up every month in 2017, a figure that’s significantly up from the 88,000 new positions that came online every month only five years ago.

But contractors shouldn’t be the only ones getting ready for a new American construction boom. As I shared with you last month, the recipe calls for a broad commodities rally this year, and I would hate for investors to miss out. With global synchronized growth underway and demand outstripping supply in a number of cases, not to mention the U.S. dollar in decline and inflation on the rise, commodities are poised to be among the best performing asset classes in 2018.

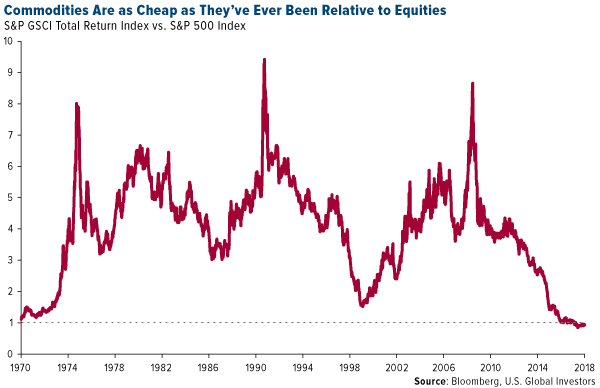

Commodities as Cheap as (or Cheaper Than) They’ve Ever Been

Pay close attention to where commodities are relative to equities right now. Compared to the S&P 500 Index, materials are extremely undervalued, the most since at least 1970. This makes now a very attractive entry point—or as natural resource investors Goehring & Rozencwajg Associates writes in its quarterly report, there could be “a proverbial fortune to be made” if investors take advantage of this once-in-a-generation opportunity.

“When commodities are this cheap relative to stocks, the returns accruing to commodity investors have been spectacular,” the firm continues:

For example, had an investor bought the Goldman Sachs Commodity Index (or something equivalent) in 1970, by 1974 he would have compounded his money at 50 percent per year. From 1970 to 1980, commodities compounded annually in price by 20 percent. If that same investor had bought commodities in 2000, he would have also compounded his money at 20 percent for the next 10 years.

Past performance doesn’t guarantee future results, of course, but the implications here are very compelling if mean reversion takes place. There have been few times that I can remember when an asset class looked as favorable as commodities do now. If you agree, it might be time to consider adding exposure to materials, energy and mining to your portfolio.

Oil Just Had Its Best January Since 2006—Further Gains Ahead?

Energy in particular looks very attractive. West Texas Intermediate (WTI) crude oil, the American benchmark, logged its best January since 2006, gaining more than 7 percent on scorching hot demand, sustained production cuts by the Organization of Petroleum Exporting Countries (OPEC), deteriorating output from Venezuela and a record-setting stockpile drawdown. U.S. oil inventories declined for 10 straight weeks as of January 24, the longest stretch ever recorded, before jumping again in the week ended January 31.

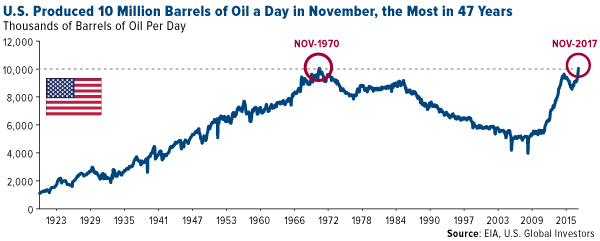

What’s more, the U.S. Energy Information Administration (EIA) just reported that, thanks to the revitalized shale revolution, the U.S. produced over 10 million barrels of oil per day in November, the first time it’s done so since 1970. This puts the country on a path to catch up with and possibly exceed Russia, which produced an average 11 million barrels a day in 2017, and world leader Saudi Arabia, whose energy behemoth Saudi Aramco produces around 12.5 million barrels a day.

As I’ve written many times before, the American fracking industry is largely responsible for keeping global oil prices low, which has been a huge windfall to the world economy. In its coverage of the news that U.S. output topped 10 million barrels, the Financial Times put it best, writing that American frackers have “boosted the U.S. economy, creating tens of thousands of jobs, bolstered its energy security, created new international relationships and given Washington new freedom to use sanctions as a tool for strategic influence.”

But shouldn’t all this extra supply halt the oil rally and put a damper on producer and explorer stocks? Not so fast.

Companies Just as Profitable with $65 Oil as They Were with $100 Oil

In the years since oil prices cratered—and subsequently began to rise—energy companies have become much more efficient and have learned to do more with less. As the Financial Times notes, U.S. frackers are producing what they are today while employing only three quarters of the workforce they had in the days of $100-a-barrel oil. ExxonMobil, the largest American producer, is in expansion mode, with plans to ramp up its shale mining in the Permian Basin to 500,000 barrels a day by 2025.

It’s not just American companies that have grown lean and mean in this climate of lower oil prices. Says the chief financial officer of Royal Dutch Shell: “We are able to do the same for less.”

Europe’s largest producer this week reported that profits tripled in 2017, generating nearly as much cash flow as when oil prices hovered around $100.

According to the Wall Street Journal, the company has “fundamentally revamped the way it designs and executes projects and is working to deliver another $9 billion to $10 billion of savings in the coming years” through restructuring and by paying down loads of debt.

As a result, Shell has rewarded its shareholders well, delivering a dividend yield of nearly 6 percent, among the highest in the entire industry.

These rewards could continue, as Goldman Sachs now sees Brent jumping to $82.50 within the next six months, up from just under $70 today. Hedge funds’ net long position on Brent hit an all-time high of more than 584,000 contracts last week, according to ICE Futures Europe and reported by Bloomberg. WTI net long positions also surged, according to the U.S. Commodity Futures Trading Commission, to nearly 500,000 contracts, the most since 2006.

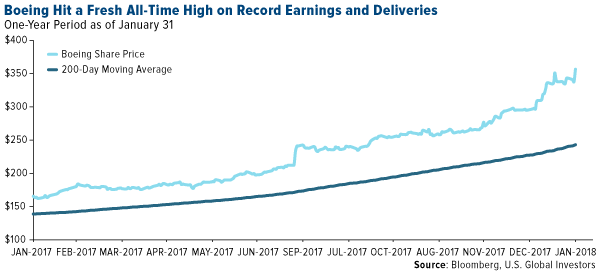

Boeing Now the Largest U.S. Industrial Firm by Market Cap

On a final note, Boeing—the world’s largest aircraft manufacturer—hit fresh new highs this week after the company crushed Wall Street expectations, reporting record operating cash flow of $13.4 billion for 2017, up more than a quarter percent from $10.5 billion in 2016. The company now forecasts operating cash flow of $15 billion by the end of 2018.

Core earnings per share (EPS) for the fourth quarter came in at $4.80, an incredible 94 percent increase from $2.47 during the same quarter in 2016. In 2017, Boeing delivered a record 763 commercial jets, and its backlog of orders stands at close to 6,000 aircraft, valued at $488 billion.

Boeing was the best performing stock in the Dow Jones Industrial Average last year, a trend that has continued into the new year.

As the Chicago Tribune reports, company stock has “more than doubled since the start of 2017 as Boeing surpassed General Electric to become the largest U.S. industrial company by market value.”

In my view, Boeing’s meteoric success is indicative of the overall health of the airline industry. That the company delivered so many new aircraft in 2017 and logged a high number of new orders suggests international carriers are optimistic about long-term air passenger and cargo demand.

In September, American Airlines CEO Doug Parker told CNBC he was very bullish on the industry’s ability to stay profitable, saying, “I don’t think we’re ever going to lose money again.”

A little skepticism would be forgiven here, but the sheer volume of new airline orders suggests other carriers feel the same way Parker does.

Read more about Boeing here.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 4.12 percent. The S&P 500 Stock Index fell 3.85 percent, while the Nasdaq Composite fell 3.53 percent. The Russell 2000 small capitalization index lost 3.78 percent this week.

- The Hang Seng Composite lost 2 percent this week; while Taiwan was down 0.19 percent and the KOSPI fell 1.92 percent.

- The 10-year Treasury bond yield rose 17 basis points to 2.84 percent.

Domestic Equity Market

Strengths

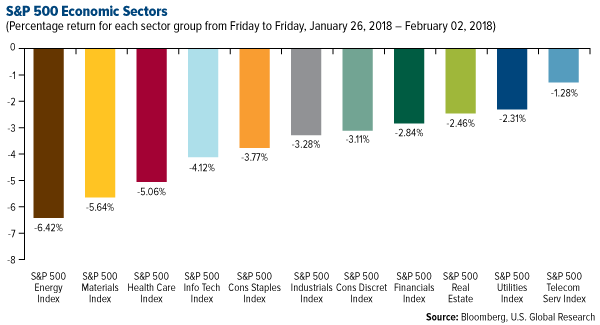

- Telecommunications was the best performing sector of the week, although decreasing by 1.28 percent versus an overall decrease of 3.79 percent for the S&P 500.

- Dr. Pepper Snapple was the best performing stock for the week, increasing 24.11 percent.

- Amazon beat Wall Street's expectations for its fourth quarter earnings, with $60.5 billion in revenue, up 38 percent year-over-year.

Weaknesses

- Energy was the worst performing sector for the week, decreasing 6.42 percent versus an overall decrease of 3.79 percent for the S&P 500.

- Chesapeake Energy was the worst performing stock for the week, falling 16.75 percent.

- Deutsche Bank posted a third straight annual loss. CEO John Cryan cited a "challenging market" as a reason for his bank's full-year loss of $621 million.

Opportunities

- Walmart is reportedly in talks to acquire a stake in Flipkart, Amazon's biggest rival in India.

- AMD beat across the board. The company’s results were boosted by a 60 percent explosion in computing and graphics sales.

- Harley-Davidson is working on an electric motorcycle for 2019. The announcement came alongside the company's disappointing fourth-quarter earnings. Entering the growing electric vehicle market is an opportunity to grab market share.

Threats

- Facebook said its users are spending a lot less time on the platform. The social-media company said the amount of time users were spending on the site declined by 50 million hours a day.

- An analyst from BMO Capital Markets downgraded Apple and said that the iPhone has hit a plateau.

- GDPR could wipe 2 percent from Google's revenues, according to Deutsche Bank. The European Union's new privacy and data protection act comes into force in May.

January 31, 2018Electric Car Demand Set to Drive Copper Sky High |

January 31, 2018Bitcoin Is Just the Latest in the Trend Toward Decentralization (INFOGRAPHIC) |

January 29, 2018What Do Quincy Jones, Serena Williams and Blockchain Have in Common? |

The Economy and Bond Market

Strengths

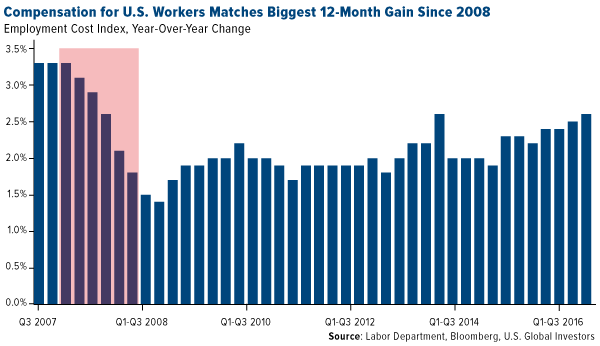

- Total U.S. employee compensation rose in the fourth quarter and matched the biggest 12-month gain since 2008, as private-sector pay picked up, according to the Labor Department. Several industry groups registered wage increases of 3 percent or higher, including transportation and services such as leisure.

- Nonfarm payrolls rose by 200,000 in January, beating analyst estimates, while the unemployment rate held at 4.1 percent.

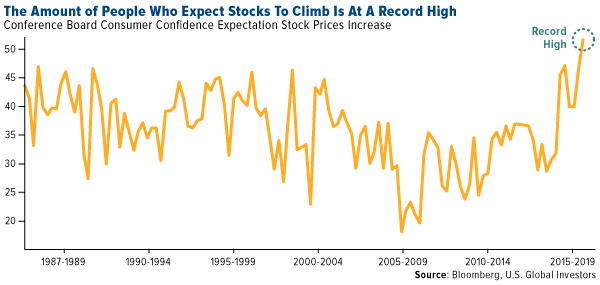

- Consumer optimism pushed higher than anticipated in January, after a surprise decline the previous month. The Conference Board's measure of consumer confidence rose to 125.4 in January, higher than the 123.1 anticipated by economists polled by Reuters.

Weaknesses

- State revenues are growing slower than the underlying economies, a divergence that highlights the fiscal challenges facing state governments, Fitch said. State tax collections grew slower and less consistently than real state GDP in the third quarter of 2017, with median state GDP growth of 3 percent, compared with 0.4 percent growth in state tax collections, according to Fitch.

- Even with solid U.S. economic growth, construction spending rose in 2017 by the least in six years, as nonresidential building slowed and outlays by governments declined.

- Productivity in the U.S. unexpectedly fell for the first time since early 2016 as working hours slightly outpaced output in the fourth quarter, highlighting a sluggish pace of efficiency gains during this expansion, a Labor Department report showed.

Opportunities

- A weak U.S. dollar may make the municipal bond market more attractive to foreign investors, though hedging costs could become an issue. "International buyers are probably the fastest growing segment in the market," said Eric Friedland, director of municipal research at Lord Abbett. A weaker dollar "would probably bring more buyers into the muni market," he said.

- The municipal bond market will benefit from new tax rules for life insurance companies, according to Anne Walsh, CIO for fixed income at Guggenheim Investments, which oversees $20 billion in municipals. "The tax cuts were interesting in that they created a new buyer of tax-exempt bonds, and that’s life insurance companies," Walsh said at a panel in New York City. Under new law, insurance companies pay tax on 30 percent of income from muni bonds, which could make the asset class more attractive to them. That’s a shift for companies that previously didn’t know how income from tax-exempt bonds would be treated until they calculated their final tax bills, a process that made them less interested in owning the securities, Walsh said. The potential pool of muni investors expanding to life insurance companies is a "very strong positive" for the muni market, she said.

- Hartford, the Connecticut capital which narrowly escaped bankruptcy, had the outlook on its debt revised to "developing" from "negative," reflecting the creation of a new state oversight board that could provide financial assistance to the city, Moody’s said. The city's Caa3 rating was affirmed.

Threats

- Illinois lawmakers voiced concerns about a proposal to issue $107 billion of pension-obligation bonds to shore up the state’s underfunded retirement system, which would be by far the biggest debt sale in the history of the municipal market. If it’s even feasible to go to market, “what is the opportunity cost to the state to issuing $100 billion in bonds in terms of going forward if we need to issue bonds for other things?" said Representative Scott Drury, a Democrat.

- Public pension plans expect less and less from their investments: 21 percent of retirement plans for state and local government workers plan to reduce their assumed rate of return, according to a survey of 164 pension funds by the National Conference on Public Employee Retirement Systems. The average investment assumption was 7.5 percent and 2.9 percent inflation is expected, the NCPERS survey showed.

- In an interview with Bloomberg, Janus Henderson fund manager Bill Gross said the U.S. jobs report should send the 10-Year Treasury yield to 3 percent and ensures the Federal Reserve will continue to hike rates, both of which are bearish scenarios for bonds.

Gold Market

This week spot gold closed at $1,331.51, down $18.19 per ounce, or 1.35 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 5.85 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index came in off 8.88 percent. The U.S. Trade-Weighted Dollar reversed course at the end of the week and closed with a slight gain of 0.14 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-30 | Germany CPI YoY | 1.7% | 1.6% | 1.7% |

| Jan-30 | Conf. Board Consumer Confidence | 123.0 | 125.4 | 123.1 |

| Jan-31 | Eurozone CPI Core YoY | 1.0% | 1.0% | 0.9% |

| Jan-31 | ADP Employment Change | 185k | 234k | 242k |

| Jan-31 | FOMC Rate Decision (Upper Bound) | 1.50% | 1.50% | 1.50% |

| Jan-31 | Caixin China PMI Mfg | 51.5 | 51.5 | 51.5 |

| Feb-1 | Initial Jobless Claims | 235k | 230k | 231k |

| Feb-1 | ISM Manufacturing | 58.6 | 59.1 | 59.3 |

| Feb-2 | Change in Nonfarm Payrolls | 180k | 200k | 160k |

| Feb-2 | Durable Goods Orders | -- | 2.8% | 2.9% |

| Feb-8 | Initial Jobless Claims | 235k | -- | 230k |

Strengths

- Despite the headwinds of rising interest rates, gold was the best performing metal this week, although down slightly by 1.24 percent. Gold traders are bullish for the fourth week in a row after the yellow metal posted its biggest monthly advance in five months in January, according to Bloomberg’s weekly survey. The government of India is presenting a policy to develop gold as an asset class and establish a trade-efficient system of regulated gold exchanges. This would allow bank customers to deposit their gold holdings for a fixed period of time in return for a 2.25 percent to 2.50 percent interest rate.

- Gold consumption in China rose 9.4 percent in 2017, a big hike from a 6.7 percent slump the previous year. Jewelry demand was also strong at 10.4 percent, up from the 19 percent drop in 2016. The rise in consumption is in part due to lower-tier cities accumulating income and using it to buy gold products.

- China’s gold production, on the other hand, dropped 6 percent in 2017, the first major drop since 2000, reports Bloomberg. The reduced production is due to environmental protection taxes, resources taxes and the closure of some mines.

Weaknesses

- The worst performing metal this week was silver, down 4.63 percent. Bloomberg reports that gold futures dropped this week after hiring and wages picked up in January with nonfarm payrolls rising 200,000, compared with the median estimate for an 180,000 increase. The unemployment rate held at 4.1 percent while average hourly earnings rose 2.9 percent, higher than expected.

- A power failure due to a storm on Wednesday night at South Africa’s Sibanye Gold Ltd.’s Beatrix mine left almost 1,000 workers trapped underground overnight. All workers made it out of the mine without injuries after power was restored using backup generators. South Africa has some of the deepest mines in the world and the mine expects to reopen on Monday.

- The Democratic Republic of Congo made last minute changes to a mining law that will go into effect immediately and will negatively affect every mining project, reports Bloomberg. DRC lawmakers hiked royalties for mining companies and added a new 50 percent tax on super-profits. The country is the world’s biggest source of cobalt and is potentially raising the royalty from 2 percent to 10 percent on the mineral.

Opportunities

- Goldman Sachs is the most bullish it’s been on commodities since 2008, expecting copper to rise 12 percent in the next 12 months to $8,000 a metric ton. Bloomberg Intelligence writes that broad demand versus supply measures are the most favorable in a decade with the CBOE Volatility Index at the lowest for the longest period in 30 years. Bill McQuaker, multi asset investment manager at Fidelity, says that gold is a prudent investment right now because it can perform well regardless of market conditions.

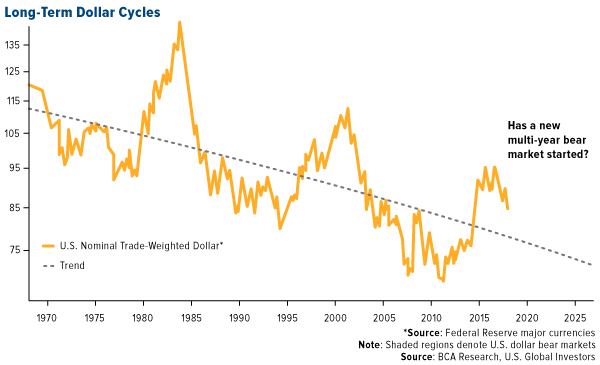

- According to Pacific Investment Management Co., the U.S. is fighting and winning a “cold currency” war, as the U.S. dollar has fallen almost 12 percent since the start of 2017. According to Pimco global economic advisor Joachim Fels, a widening trade deficit will foster a continued American interest in a weaker dollar. Bank Credit Analysts released a report showing that the dollar has oscillated between bear markets lasting 10 years and bull markets lasting five years. If this holds true, the dollar’s five-year bull market from 2011 to 2016 fits the pattern of the dollar entering a bear market now for the next 10 or so years.

- Matthew Sigel, portfolio strategist at CLSA, released a report detailing that the U.S. dollar has “broken down” after the policy error of tax cuts were passed. This is due to lost relevance as a means of exchange as the dollar percentage of foreign exchange reserves and its use for SWIFT payments continues to decline. In addition, Sigel notes that U.S. recently fell out of the top 10 in the Bloomberg Innovation Index, and in terms of patents, China has filed 10 times more over the last 10 years than the U.S. Gold has historically performed positively when the U.S. dollar is weak.

Threats

- Wells Fargo analysts are warning of a commodities bear market and said they doubt a weakening dollar will result in commodity performance rising. They released a report saying “We expect bear market dynamics (over-supply and range bound prices) to dominate commodities for the next five to 10 years.” Austin Pickle wrote.

- Bloomberg reports that OPEC and Russia will allow prices to rise as high as the market can take. The downside of higher oil prices is that mining costs can rise as well. Unit costs for miners might rise 5 to 10 percent this year as commodity prices are rallying.

- Renaissance Technologies, the world’s most profitable hedge fund, warns of a significant risk of a market correction and is preparing for possible market turbulence. The group cites rising valuations as being unjustified entirely by accelerating global growth and corporate tax reform. In the prior week there were all-time highs in money flows into equities.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended February 2 was Smartlands, which gained 1,018 percent.

- After regulatory crackdowns, China’s first Bitcoin exchange, BTCC, announced that it has been acquired by a Hong Kong-based blockchain investment fund. This acquisition is seen as a positive move that will give BTCC more resources to grow the business and continue operating in the face of heightening regulations.

- Europe’s largest utility provider, Enel SpA, is in talks to sell power from renewable energy plans to Swiss cryptocurrency company Envion AG. The deal sparked conversations from other energy providers on whether they should supply excess power to crypto mining companies, as they require huge amounts of electricity to mine digital currencies.

Weaknesses

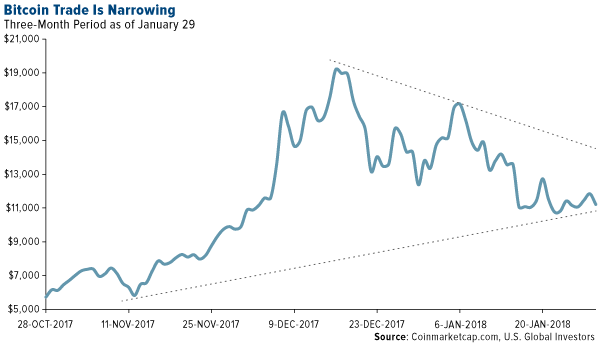

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended February 2 was Spectre.ai Utility Token, which lost 50.81 percent. Bitcoin fell below $8,000 this week for the first time since November. The popular cryptocurrency has been trading in a narrow range of $10,000 and $11,000 recently after hitting a peak of $19,000 in December. Bitcoin lost $44.2 billion in market cap and fell 25 percent overall in January.

- Last Friday morning in Japan someone hacked into the digital wallet of Japanese cryptocurrency exchange Coincheck to pull off one of the largest heists in history, stealing around $534 million in digital coins, according to Bloomberg Technology. Although Coincheck reassured customers they would be partially reimbursed, this theft has spurred increased calls for regulation.

- The U.S. Securities and Exchange Commission (SEC) froze the cryptocurrency assets of Texas-based AriseBank after its initial coin offering raised more than $600 million. The SEC alleges that the company illegally raised funds from investors by not registering with regulators and making misleading statements.

Opportunities

- The first two blockchain ETFs, Amplify Transformation Data Sharing ETF (BLOK) and Reality Shares Nasdaq NexGen Economy ETF (BLCN) already have over $250 million in assets under management combined in less than two weeks since they began trading. A third blockchain was launched this week on the NYSE Arca exchange, Innovation Shares LLC’s NexGen Protocol ETF (KOIN).

- Tom Lee, head of research at Fundstrat Global Advisors and an early bitcoin investor, spoke with CNBC this week about a new “crypto-rotation” where smaller cryptocurrencies have been rallying as much as 300 percent. Lee describes how this rotation of digital currencies allows investors who missed the initial big wave of investment like bitcoin to invest in the new cycle of booming cryptocurrencies.

- Line Corp., Japan’s largest messaging service, has applied for a license to open a cryptocurrency exchange after reporting a $37 million loss for the previous quarter. The company is also considering expanding its cryptocurrency operations to Hong Kong and then Luxembourg.

Threats

- On Tuesday, South Korea’s Financial Services Commission confirmed that new measures have been implemented tackling the issues of anonymity and money laundering. The new rules only allow trading of cryptocurrencies from real-name bank accounts. Fears of regulation in South Korea, a country with a high volume of digital currency trading, spooked investors and traders earlier this month.

- Facebook announced that it will be banning ads that promote cryptocurrencies and initial coin offerings (ICOs) in a measure to prevent users from being exposed to fraudulent operations. The company released a statement saying “We want people to continue to discover and learn about new products and services through Facebook ads without fear of scams or deception.”

- The Indian government released a statement this week saying it does not consider cryptocurrencies to be legal tender. Anshul Vashist, a Delhi-based support manager at cryptocurrency Coinsecure, said after the announcement that “people are getting scared” and “we have seen some dumping of bitcoins.” India’s government did, however, indicate that it will be exploring potential adoption of blockchain technology for ushering in the digital economy, reports Bloomberg.

Energy and Natural Resources Market

Strengths

- Iron ore was the best performing major commodity this week, rising 3.2 percent. The commodity rallied as Goldman Sachs increased its price forecast, arguing that market participants will look to restock in the coming weeks in anticipation of the proposed end to the steel mill supply curbs this spring.

- The best performing sector this week was the Bloomberg Global Coal Producers Index. The index rose 1.2 percent as thermal coal prices rallied on the back of colder weather across China, coupled with gas shortages in regions of the country, leading to bid on thermal coal as a heating fuel substitute.

- China Shenhua Energy was the best performing stock in the broader resource market this week. An integrated coal-based energy company in China, Shenhua rallied 7.8 percent for the week to fresh 52-week high. The stock rose on the back of rallying thermal coal prices in China as a result of cold weather fronts and a shortage of natural gas available for heating.

Weaknesses

- Natural gas prices dropped 16.9 percent this week, the most among major commodities. The commodity dropped the most in at least four years after forecasts for a bone-chilling February in the U.S. have turned warmer.

- The worst performing sector this week was the S&P 1500 Construction and Materials Index. The sector dropped 7 percent following President Donald Trump’s State of the Union speech Tuesday. Investors had been looking for more color on any infrastructure bill, but the details were few in number and did not outline any funding sources.

- The worst performing stock for the week was Ivanhoe Mines. The Canadian developer of mineral properties in South Africa and the Congo dropped 24.8 percent to a 52-week low. The stock dropped on reports that the Congolese government is considering an onerous increase in royalties that would require a cancellation of contract guarantees, which would significantly raise the cost of doing business in the country.

Opportunities

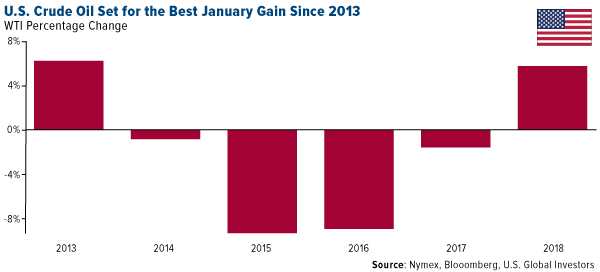

- Crude oil prices posted their best start in five years as the U.S. glut declined. West Texas Intermediate (WTI) crude had its best start since 2013, temporarily advancing above $66 per barrel as U.S. crude inventories capped a record run of declines and are approaching the five-year average.

- Thermal coal futures in China rose to a new high amid cold weather warnings and in the face of tight gas supplies as Beijing pushes for less polluting fuels. China’s meteorological service renewed cold weather warnings in western and southern parts of the country while gas supply shortages were reported in the northern part of the country.

- Members of OPEC, the Organization of Petroleum Exporting Countries, exceeded crude supply curtailments by the most since the cuts were announced in November 2016. OPEC compliance rose to 127 percent of the agreed cuts, the highest level since 2016, as Venezuela production continues to collapse. Production at the South American nation dropped by 30,000 barrels per day in January alone as the industry continues to battle years of underinvestment.

Threats

- Fears of a U.S.-China trade war rose again this week after China targeted chemicals imports from the U.S. and he European Union (EU). China’s commerce ministry said that it would launch an anti-dumping review of industrial solvents imported from its main trading partners.

- The EU gave President Trump a fresh warning about any U.S. curbs on imports for Europe by pledging swift retaliation, highlighting the risk of a trans-Atlantic trade war. The announcement follows Trump’s decision to invoke rarely used “safeguard” rules to impose tariffs on solar panels from Europe and elsewhere.

- China may extend its steel supply curtailments from March all throughout May. According to UBS analysts, if the supply cuts were extended, there is a risk that crude steel output could fall in 2018 relative to 2017. The extension to cut supply could lead traders to panic and advance the timing for restocking.

China Region

Strengths

- In an otherwise down week for markets, Malaysia’s FTSE Bursa Malaysia Kuala Lumpur Composite Index easily takes the cake for the last five trading days, finishing (in rather lonely fashion) in the green, up 89 basis points.

- Macau casino revenue jumped in January, rising 36 percent year-over-year and coming in ahead of expectations for an increase of only 27 percent growth.

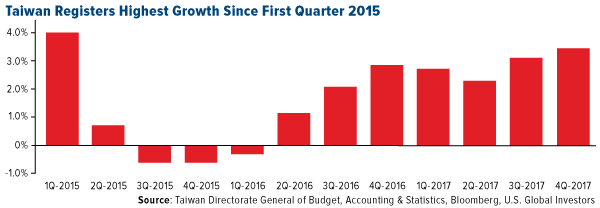

- Taiwanese economic growth accelerated into the end of the year. Fourth quarter preliminary GDP growth came in at a year-over-year pace of 3.28 percent, yielding an annual (2017) year-over-year growth rate of 2.84 percent.

Weaknesses

- Shanghai closed down 2.70 percent for the week, while the Philippines Stock Exchange Index closed down 2.55 percent. India also had a rough week, as both the SENSEX and the NIFTY indices closed down more than 3 percent since Monday (India was closed for Republic Day on January 26, so it is not precisely apples to apples with the other indices since last week, but adequately demonstrates the selling pressures in some global markets this week).

- While China’s official Non-manufacturing PMI did beat analysts’ expectations (coming in at 55.3, ahead of an anticipated 54.9), the official Manufacturing PMI missed by a little bit, coming in at 51.3, down from last month’s print and an expected reading of 51.6 for this month. The Caixin China Manufacturing PMI was in line at 51.5, as expected and steady from last month. We’ll get the Caixin Services numbers this weekend.

- Industrial production missed in South Korea for the December period, coming in down 6.0 percent, shy of expectations for a decline of only 1.5 percent and down from the prior month’s revised year-over-year decline of 1.7 percent.

Opportunities

- “U.S. Firms Are Upbeat on China,” an article in Tuesday’s Wall Street Journal reported, noting that “U.S. companies are more optimistic than a year ago about business prospects in China despite a backdrop of escalating trade tensions and worries over regulation, according to the latest annual survey by the American Chamber of Commerce in China.” Three-quarters of respondents, the article observes, said they “planned to increase investment in China next year.”

- Ping An’s health care and technology unit is closer to its Hong Kong IPO, Bloomberg reported this week, noting that the Softbank is now set to invest $400 million in the “Good Doctor” listing.

- In the midst of U.K. Prime Minister Theresa May’s recent trip to China, Bloomberg News reported that the U.K. and China will seek to develop a “finance-tech city” in the Xiongan New Area.

Threats

- Bloomberg reports the Shanghai Environmental Monitoring Center warned that it would be best if the young and elderly tried to stay indoors this week as air pollution reached “heavily polluted” levels, the second-to-worst ranking of air quality.

- “China is drafting a proposal to allow gambling on Hainan Island,” Bloomberg News reported people familiar with the talks as having said, “in what would be an unprecedented move that could reshape gaming in China’s territories and transform the economy of a strategic southern province.” While perhaps bullish for the long term, the move—which reportedly considers online gambling but clearly could open the doors to eventual physical casinos—could also represent a threat to Macau’s preeminence. Macau stocks stumbled initially on the news and then took it largely in stride, finishing down relatively mildly on Friday.

- India announced this week that the government will seek to eliminate payments using cryptocurrency—not entirely surprising, perhaps, given the Modi administration’s recent demonetization scheme—while nonetheless allegedly embracing the concept of blockchain technology.

Emerging Europe

Strengths

- The Czech Republic was the best relative performing country this week, losing 25 basis points. Banking stocks were the best performing equites trading on the Prague exchange. Komercni Bank appreciated 2.2 percent, after Raiffeisen Centrobank raised it to a “buy” from a “hold.” Moneta Money Bank gained 1.2 percent after its investment grade rating was reaffirmed by S&P Global Rating Agency.

- The Czech koruna was the best performing currency this week, gaining 60 basis points against the U.S. dollar. The central bank of the Czech Republic raised its key rate by 25 basis points to 0.75 percent, in line with expectations. This was the third increase in the past six months.

- The industrial sector was the best performing sector among eastern European markets this week.

Weaknesses

- Poland was the worst performing country this week, losing 2.8 basis points. Poland’s manufacturing PMI reading disappointed, coming in at 54.6 versus expected 55.2. President Andrzej Duda approved this year’s budget; the deficit will be higher than previously calculated.

- The Polish zloty was the worst performing currency this week, losing 65 basis points against the U.S. dollar. The central bank of Poland left its main rate unchanged at 1.5 percent. Sharp zloty appreciation over the past couple months is already a substitute of monetary policy tightening, said Eryk Lon, member of the Polish Monetary Policy Council.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

- According to a report released by Eurostat, the European Union’s statistic agency, the EU bloc grew by 0.6 percent in the fourth quarter, and 2.5 percent in the full year 2017. The preliminary GDP data shows 2017 was the best performing year for growth in the eurozone bloc since 2007, when it recorded economic growth of 3 percent. For the second year, the eurozone grew faster than United States, which expanded by 2.3 percent in 2017. The EU’s manufacturing PMI was reported at 59.6. Slightly weaker than the prior reading of 60.6, but still close to a record high.

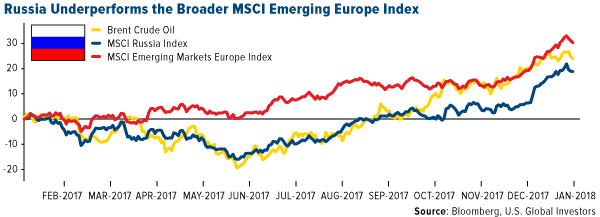

- Russian equites are the biggest laggards among Emerging Europe stocks in the past 12 months. The MSCI Russia Index gained only 19 percent in the past 12 months, mostly supported by higher oil prices, while the broader MSCI Emerging Europe Index appreciated more than 30 percent during the same period. Once the noise around additional sanctions on Russia settles down, it may be a good time to pick up this underperforming market. According to Wood & Company, the growing dividend payout ratios and a new budget rule are the most important factors that call for higher valuation multiples.

- Emerging markets could outperform again in 2018, says Bretton Woods Research Team. Emerging markets should benefit from the weaker dollar. Exporters of commodities, agriculture products and raw materials should perform well during a period of a weaker dollar. The group’s favorite emerging markets are Chile, China, the Czech Republic, Hungary, the Philippines and Russia.

Threats

- Polish president Andrzej Duda has signed into law a bill that largely limits trade on Sundays. As of March 1, shops and markets will be closed on two Sundays per month, in 2019 only one Sunday a month will be open for shopping; and starting in 2020, there will be no Sunday shopping, with few exceptions. Larger supermarket chains will be the most exposed to this change, as most of their profits are earned during the weekends.

- On Wednesday, the European Banking Authority (EBA) formally launched the 2018 EU-wide stress test and unveiled the scenarios against which the largest 48 banks across the eurozone bloc will be tested. It will be a tough test, analyzing banks’ resistance to the bloc’s economy shrinking cumulatively by 8 percent by 2020, or residential-property prices dropping by 27.7 percent. Results are expected to be published by early November.

- The current Czech president, Milos Zeman, has secured a second five-year term as a head of the state. His reappointment should have minimal effect of country’s growth which is supported by robust global demand and strong internal monetary and fiscal stimulus, but it is also showing that Czech voters’ are Eurosceptic. Zeman is viewed as anti-immigration, anti-Islam and Eurosceptic with pro-Russian tendencies.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits