Enjoy It While You Can

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsY2K Relief

Federal Compulsions

Rewind the Tape to 1987

Correction Odds Rising

Sonoma, San Diego and SIC, and Elsewhere

If you travel as much as I do, you come to value nonstop flights. Connections introduce uncertainty and potential delays, not to mention what often feels like wasted time; but sometimes connections are just unavoidable. But you don’t want them to be too tight. Those five-minute sprints from one concourse to another are never fun. Better to have some breathing room.

So it is with economic cycles. Rarely do we move directly from boom to bust; but when the shift comes, it can develop quite quickly, even though the transition isn’t usually obvious in real time. As I look at the data and talk to my contacts, I’m beginning to conclude that we’re approaching one of those transitional phases. I think we’ll look back at 2018 as an in-between year… from good times to something eventually not so good.

Getty Images

Now, let me stress that I’m not predicting imminent doom. As you’ll see below, I think the party can last another year, maybe even longer. But I do see storm clouds on the horizon, and they’re blowing our way.

That ominous horizon means that some strategy adjustments are probably in order. You need to be aware that the volatility we have seen in the stock market the past few days will become more the norm. I’ll get to that later. Let’s start by considering where we are now.

So far, economically and GDP-wise, 2018 looks not too different from 2017. Economically, the first full-year estimates for 2017 show US real GDP rose 2.3%, or 4.1% in current (nominal, not inflation-adjusted) dollars. That’s not stellar performance, but not awful either. I expect about the same in 2018, and perhaps we’ll see even slightly stronger growth in the first six months, but that growth may be front-loaded and thus lower in the second half.

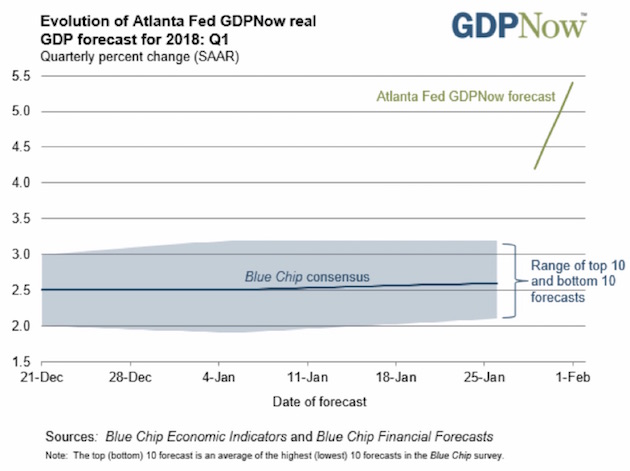

A great chart from the Atlanta Fed on their GDP Now page shows the blue-chip consensus on growth at 2.6%, with a range from just above 2% to just above 3%.

But notice the green line jutting upward in the upper right-hand corner. That is the Atlanta Fed GDP Now forecast, which was raised just this week from 4.2% to 5.4% for 2018. That’s massively more bullish than the blue-chip consensus is. For those of you unfamiliar with the Atlanta Fed’s forecasting methodology, I should note that they have been more bearish than blue-chip forecasters in most recent years. This is the most bullish I can recall them being since they created this methodology a few years ago.

If this kind of thinking infects the rest of the Fed’s researchers, you can expect them to suggest more than three rate hikes this year. Just saying…

For now, though, this week’s Federal Open Market Committee statement sums it up well: “Gains in employment, household spending, and business fixed investment have been solid, and the unemployment rate has stayed low.”

Recently volatility notwithstanding, stocks still point higher as analysts raise earnings estimates almost incessantly. Investors aren’t shying away from risk assets. Quite the opposite: The Conference Board reported that Americans are now more bullish on stocks than they have been since January 2000 – notwithstanding yesterday’s 666-point drop (-2.54%) on the Dow.

Let’s stop right there. What was happening in January 2000? We had just made it through the Y2K scare with barely an economic or societal blip, much to the chagrin of doomsayers who stocked up on beans, bullets, and Band-Aids. I had written a book saying to expect some hiccups but not disaster. As it turned out, even I was too pessimistic.

But people had other reasons to feel good that January. The NASDAQ 100 Index had just doubled in 1999 and looked to be headed higher still. It did – until March 2000, when the picture changed dramatically for the worse.

Fast-forward 18 years, and now we have Bitcoin and all its little crypto-cousins in addition to tech stocks. They are off their highs, but few fans are throwing in the towel. I suspect that instead of competing, Bitcoin and stocks may be feeding each other. Both contribute to the general “risk-on” attitude among investors. This feedback may get to be a problem if they pull each other down, too, but that’s not happening yet.

The Republican tax cuts have a lot to do with the current good feelings. The package’s corporate impact is already apparent. Numerous companies have announced bonuses, pay raises, and expansion plans. One key tax change is behind much of this activity: Companies can now deduct equipment purchases from taxable income immediately instead of amortizing them over several years. This change both simplifies planning and encourages quick decisions. There are numerous stories about companies purchasing equipment so they can write it off this year and reduce their tax costs, rather than postponing the purchases.

Deregulation is helping, too – or at least the promise of it. Some readers correctly reminded me that most of the Trump administration’s desired changes are still in process. While that’s true, I think it misses a broader point: Perception matters. Business owners may not see specific relief yet, but they believe it is coming. They are hearing optimism from their respective business associations. They also see a more cooperative attitude from regulatory agencies. Those changes give them confidence the regulatory burden will at least get no worse, and that confidence shows up in their investment decisions.

So, all this is good news. I think it’s enough to keep the expansion phase going through the end of 2018. Why not longer? Several reasons – one of which looms darkly over the others.

Getty Images

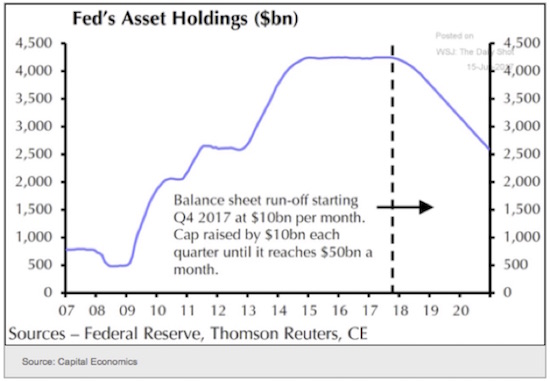

Our Federal Reserve leaders believe keeping inflation under control is their key mission. Fair enough. The problem is that inflation is not now a threat – yet they still feel compelled to stamp it out. Worse, they are doing so while simultaneously undoing their much-larger-than-it-should-have-been QE stimulus program. This is a massive monetary experiment, and they have nothing more to go on than a few models, which assure them that reducing their balance sheet by $1 trillion over the next two years will have no effect on the asset markets.

Even though they told us, and most of us believe, that QE was responsible for the inflation of asset prices across the board, somehow quantitative tightening (QT) is not supposed to have the opposite effect.

The Fed’s main justification for tightening is the persistently low unemployment rate. They think it will spark wage inflation. Maybe so, but so far we have seen only sporadic evidence of it. Real wages have been falling, not rising.

And now I have to add, “Except for yesterday’s jobs report.” We find that in January wages rose by 0.3%, or by 2.9% year-over-year. A few more reports like this and the Fed governors are going to have a real excuse to talk about wage inflation. Two hundred thousand new jobs is a very good report, much higher than the average over the past two years. The ding on the report was that average hours fell a few tenths of a percent, so that actual wages paid did move all that much. Was that impact weather-related? Let’s look at the February and March data and decide.

Nothing in this jobs report will discourage the Fed from raising interest rates at least three times this year, and there is reason to worry about four rate hikes. And maybe even more hikes going into 2019. Yesterday’s report certainly moved the bond market in the US, as 10-year Treasury yields went to 2.84% and the 30-year bond went to 3.09%. TIPS are suggesting that the implied inflation rate is closing in on 2.2% for the next 10 years.

What is happening here? Despite today’s job numbers, when we look at the last two years, if the job market is so tight then why are wage gains so muted? That’s a mystery. I think people who left the labor force and those working part-time for economic reasons amount to a sizable hidden labor supply. At some point the economy will have soaked up that supply, but we don’t seem to be there yet.

In fact, I know that many Millennials are working two and three part-time jobs in order to make ends meet. If they could actually get a full-time job? With some benefits? They would jump on that opportunity. Now, nothing will change in the employment picture when these workers go from being employed part-time to being employed full-time, which still just counts as “employed.”

There are now 96 million potentially employable people in America who are not in the labor force now – almost 30% of the population. That is unusually high number for this late in a GDP growth cycle, but I expect the number would drop if opportunities develop. Not everyone in the “not in labor force” group would turn down a job if one became available. I can’t find any real data or research on that, but it just seems like common sense to me.

I can understand the Fed’s raising rates from the near-zero level to something more normal. That makes sense. What we don’t need is to raise rates and wean the bond market off its quantitative easing bottle at the same time. Yet that is what the Fed is doing.

I think many investors don’t realize that the reverse of quantitative easing, what my friend Peter Boockvar calls “quantitative tightening,” is only just beginning. The chart below from Investopedia shows the projected path. Right now we are still at the top of that big purple slide.

The Fed intends to stop buying bonds at the very time the US Treasury will issue more bonds to fund a growing budget deficit. The Treasury announced last week that net borrowing will be an estimated $441 billion this quarter and another $176 billion in the second quarter. It was “only” $282 billion in 4Q 2017. It would not be surprising to see the US official deficit at $1 trillion, with another $500 billion in off-book debt increases. Remember, these are the numbers in relatively good economic times, at least GDP-wise.

The US debt is officially $20,622,176,525,000 as I write this: $20.6 trillion. We could be easily north of $22 trillion going into 2019 (or at least scaring $22 trillion) if the economy is supposedly still doing well. What happens when we go into recession? We will be at $30 trillion in total debt within three to four years. Using government projections, we could easily be there, even without a recession, shortly after the middle of the next decade.

Sidebar: Projected revenues from this tax cut are not going to be near what Congress or the CBO expect. My accountant and I have already looked at the new tax rules; and, annoyingly, if you are a small businessman or a contractor, you cannot just deduct expenses that are employer-reimbursed. It’s not quite that simple, but it’s close. The business actually has to pay for those expenses. What that means for me is that my accountant/associate will have to write a few more checks at the end of the month from both my personal account and my business account in order to not have to declare additional income. I can guarantee you that any small business that normally just reimburses is going to change their policies in order to help not only the owners but the employees. That will mean less revenue than the feds are probably projecting.

The tax games played by corporations from small to large to gigantic are only starting to come into the public awareness. There is simply no way to project what actual revenues will be as a result of this tax cut. But I think it is safe to say that businesses small and large are going to do their best to pay the least possible amount of taxes. And something as broad-reaching as this new tax law opens up many new opportunities.

As a second sidebar, it looks right now as if this tax “cut” that I’m supposed to be getting is kind of a push, as they are taking away so many deductions that I really don’t see any more money appearing in my bank account than I would have under the old system. And I’m having to do a lot of extra work to meet the new requirements. I’m hearing much the same from friends all over the country. This was actually a tax cut that benefitted the bottom 50–70% of the individual income structure more than it did the top. And corporations made out really well. Now back to the letter.

When the supply of available bonds rises and demand falls, the result is lower prices, which in the bond market means higher rates. For T-bonds in particular it means higher long-term interest rates. How much higher remains to be seen. Inflation expectations – which again, I think are misplaced – are also driving rates up. But short-term rates are rising, too, and at an even faster pace for now, so the yield curve is still flattening.

This trend has spillover effects outside the Treasuries market – in mortgages, for one. Here’s Peter Boockvar from last Wednesday:

With the highest average 30 year mortgage rate since March 2017 at 4.41% (and moving higher still), purchase applications fell 3.4% w/o/w but is still up 10% y/o/y. Refi apps were down by 2.9% w/o/w but still up 3.2% y/o/y. Maybe because long term fixed rates are now moving higher, there was a pick up in ARM's as a % of total loans. The MBA forecasts that refinancing volumes will be about $425b in 2018 which would be the smallest amount since 2000 and that would be down by 60% from where it stood in 2016.

At some point higher rates will start cutting into housing purchases and potentially reduce the mild inflation the Fed sees. Meanwhile, other central banks are beginning to plan their own policy turns. The Bank of England and the Bank of Canada are both theoretically in tightening mode already. The European Central Bank is starting to reduce its own QE program – a first step toward tightening. The Bank of Japan might do likewise at some point.

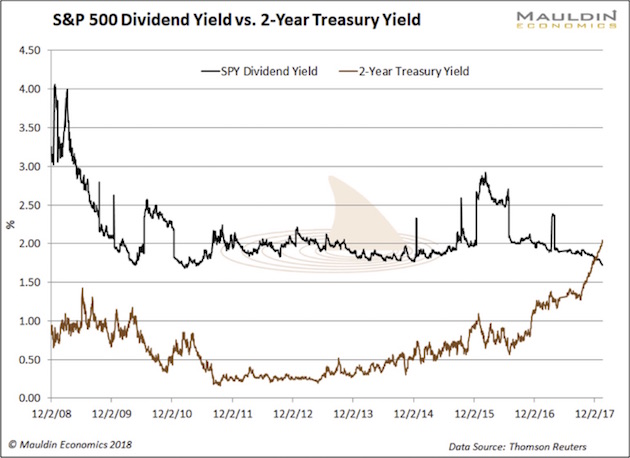

If we see global liquidity conditions tighten, the impact on stocks will turn more serious. The two-year Treasury yield recently surpassed the S&P 500 dividend yield for the first time since before the crisis. As that gap widens, the incentive to own bonds instead of stocks grows.

We are actually going to look at two years, 1987 and 1994. 1987 is instructive because the prelude to the market crash of October was a selloff in the bond market that started a few months earlier, combined with the weakening of the dollar. Sound familiar?

I should point out that bear markets like 1987 or 1998, when not accompanied by a recession, are typically V-shaped and quickly over. It’s when you have a bear market, no matter how deep, that is accompanied by a recession that you really have to worry about lengthy recoveries.

1994 is instructive because the Fed commenced a tightening cycle and there was an inflation scare. It didn’t help that there was a great deal of leverage in the bond market, which caused a lot of pain during the selloff. Historians will note that even though the 10-year yield rose significantly, inflation never really picked up. And the market recovered relatively quickly.

That being said, it should come as no surprise that correlations among asset classes are up to 90% (source: Deutsche Bank). Everybody seems to be playing the global growth and global reflation trade. In almost every asset class, all the traders are on the bullish side of the boat – or at least they were until the last few days.

That level of correlation means that pain in one asset class could easily translate to pain in other classes, even as the economic news seemingly gets better and better. Because, what if the Atlanta Fed is right? The Fed will have to lean into the market with more than three hikes this year, with more to follow next year. Other major central banks would also have to initiate tightening cycles. We have been addicted to easy money and low interest rates for so long that regime change is scary. We’re not unlike addicts who finally realize they’re going to have to give up their drug of choice.

In the US equities, mutual fund exposure rose to a six-year high while short interest in stocks and ETFs fell to the lowest level since 2007 in other assets fund exposure to oil is a now about 2.8 standard deviations above the average while long euro shows similar extreme readings. (Source: Bloomberg)

Much of the current good feeling hinges on consumer spending, which is up. This uptick in spending reflects confidence in the future, but its flip side is a lower savings rate. The Commerce Department reported last week that the savings rate was 2.4% of disposable household income, the lowest since September 2005. That was a housing boom year when people were flipping homes and pulling out equity with wild abandon. Many would regret it a couple years later.

My friend Steve Blumenthal just posted a note in which he talked about his top ten recession indicators. Nine of them were signaling no problem for at least the next nine months. The signals don’t go further than that. GDP growth is not the problem this year.

The problem is overstretched markets and the potential for the Fed to go too far. We simply don’t know what will happen when the Fed starts removing $150 billion per quarter from its balance sheet by the end of this year. Maybe they’re right, and it means nothing. Maybe running a $1 trillion yearly deficit doesn’t make a difference. Maybe four interest rate hikes don’t matter.

None of these factors are serious yet, but they will add up over time. Maybe the market will shrug them off, we’ll actually see the 25% earnings growth projected by analysts, and the S&P will end up much higher for the year.

Any number of tail-risk events could change the picture quickly, though: war in Korea or the Middle East, a major terrorist incident or cyberattack, spiraling trade disputes, a bank failure – you know the list. The world can change quickly.

Now is a good time to plan your de-risking strategy. You want to balance it with staying involved in growth assets, if they are part of your plan. Rather than trying to diversify asset classes, which are marching in lockstep both up and down, I would try to diversify trading strategies. Think about what you’re going to do when the market turns against you.

Hope is not a strategy. You need to have a plan, or you need to find somebody who has a plan that you feel comfortable with.

To sum up, I’m not expecting a major bear market, but a correction is a real possibility. This is going to be a much more volatile year than 2016 or 2017. Overbought and overstretched markets moving in concert with each other are just the right witches’ brew for volatile corrections. Just saying…

Sonoma, San Diego and SIC, and Elsewhere

In three weeks Shane and I will be going to Sonoma, where I’ll speak at my Peak Capital friends’ annual client conference. Then we’ll come back to Dallas, and I’ll continue the preparations for the Strategic Investment Conference. This is really going to be the best conference we have ever done, and you don’t want to miss it. We have been holding teleconferences with the various speakers on what they’re going to be presenting and how we’ll work the moderating and Q&A panels, and I’m adjusting the lineup a little to make the ideas flow better.

This will be our 15th annual conference, and we have learned a few things about making SIC more interesting and allowing attendees more interaction with the speakers. Further, we use software now that allows attendees to ask questions and for people to vote on those questions that they want moved to the top of the questions queue. It works amazingly well, and the attendees do get their most important questions answered.

Sunday night is the Super Bowl, and Shane and I are throwing our fourth annual Super Bowl party. We don’t do more than three or four parties a year (and Shane actually does most of the work now), but our house is really set up for entertaining, and the parties are an enormous amount of fun. Plus, we do have a lot of TVs here, so it’s kind of like living in a big sports bar. It’s actually perfect for people to come and watch the game, enjoy some chili, chips and guacamole, etc. I don’t really have a dog in this hunt, which means that I’ll probably be pulling for the underdog, which is obviously Philadelphia. But mostly, I’ll spend my time walking around, talking with friends, and just enjoying the fun.

One last bit of market commentary. My friend Steve Blumenthal sent me this link to MarketWatch. It is about the “maturity wall” that high-yield bonds are getting ready to walk into over the next three years. If for some reason we see a recession during that time, it is going to be difficult for these high-yield bonds issuers to refinance their debt at anything close to the rates they enjoy today. Sell signals were tripped at several major high-yield bond-timing services over the last few days, and there is little liquidity in the high-yield bond market as it is. If we get into an actual recession, the remaining liquidity will dry up, and high-yield bonds will fall in value even farther than they did in the last recession. Dodd–Frank changed the levels at which banks can make markets in the bond market, and they had been the main source of liquidity. Bids are going to simply disappear, and it will be a rout. Maybe it won’t happen this week or next; but if you are invested in high-yield, you need to have your exit strategy and timing well planned. Just for the record, this is the type of thing I often cover in my Over My Shoulder service. Over My Shoulder is an inexpensive way to have curated information delivered directly to your inbox. You get the news and reports that I find to be the most interesting and actionable.

And with that I will hit the send button and wish you a great week. And I hope your team wins!

Your expecting more volatility analyst,

John Mauldin

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All