An Olympian's Guide to the Market Selloff: Seeking Rewards In High-Risk Situations

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefitss

Today I’d like to share a few words about the Olympics, but first, two words: Don’t panic.

The stock selloffs on Monday and Thursday were the two biggest daily point drops in the history of the Dow Jones Industrial Average, but in terms of percentage point losses, they don’t even come close to cracking the top 10 worst days in the past 10 years alone.

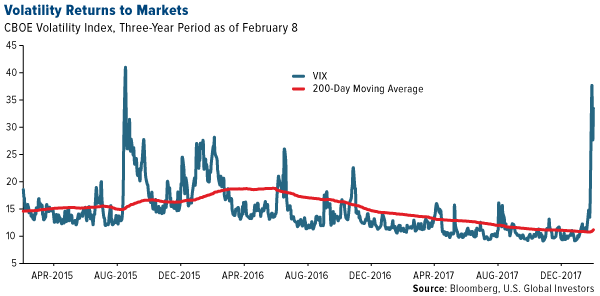

After a year of record closing highs and little to no volatility, it was expected that the stock market would need to blow off some steam. On Monday, the CBOE Volatility Index, or VIX, surged nearly 116 percent, its biggest one-day increase since at least 2000.

As I explained earlier in the week, the selloff appears to have been triggered by a number of things, including last Friday’s positive wage growth report. This stoked fears of higher inflation, which in turn raised the likelihood that the Federal Reserve, now under control of newcomer Jerome Powell, will raise borrowing costs more aggressively than expected to prevent the economy from overheating.

Also contributing to the uncertainty was news from the Treasury Department this week that the U.S. government plans to borrow nearly $1 trillion this year, compared to almost half that last year. In the first quarter alone, the Donald Trump administration will issue $66 billion in long-term debt, the first such boost in borrowing since 2009, as the U.S. Treasury seeks to cover budget deficits brought on by higher entitlement spending, not to mention the recently passed tax overhaul.

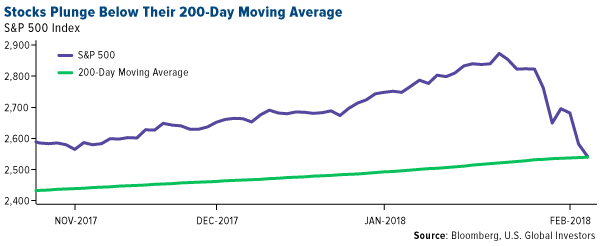

On Friday, the S&P 500 Index briefly plunged below its 200-day moving average before rebounding in volatile trading.

With stocks down more than 10 percent from its closing high on January 26, we could be in correction territory. Historically, it’s taken four months for stocks to recover from a correction, according to Goldman Sachs analysis. By comparison, a bear market, which is generally defined as more than a 20 percent drop, can take up to two years.

I’m not saying a bear market is imminent—only that it might be time to reevaluate your tolerance for risk and, if appropriate, act accordingly. It’s times like these that highlight how important it is to be diversified in a number of asset classes such as gold, commodities, municipal bonds and international stocks.

Diversity Is Key in Volatile Times

I remain bullish on the U.S. market, but there will always be risks even in a booming economy. This is one of the biggest reasons why I recommend a 10 percent weighting in gold and gold stocks, with additional diversification in commodities, international stocks and other asset classes.

But to get the greatest benefits, it's important to rebalance at least once a year, based on your risk tolerance.

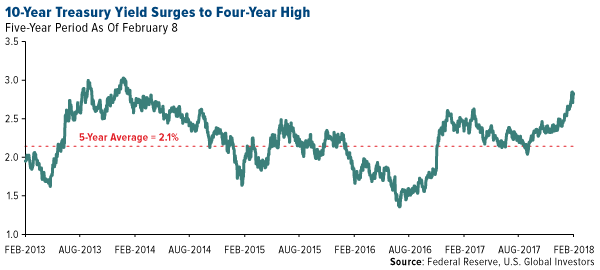

This week, gold was under pressure from surging Treasury yields. Since its 52-week low in September, the 10-year yield has increased almost 40 percent on safe haven demand. Not only is it at a four-year high but it's also above its five-year average of 2.1 percent.

Keep in mind that fundamentals remain robust. The U.S. economy is humming along. Unemployment is at a 17-year low, and wage growth is finally bouncing back after the financial crisis. The global manufacturing sector began 2018 on strong footing, with the purchasing manager’s index (PMI) registering 54.4 in January.

Like an Olympic cross-country skier, take the long-term approach and keep your eyes on the prize.

A Year for Olympic Record-Breaking

Before it even began, this year’s Winter Olympics was breaking records. A historic number of athletes, around 3,000, qualified to compete for an unprecedented 102 medals. For the first time ever, an African country—Nigeria—will be represented in the bobsled category, making this also the country’s first visit to the Winter Games. And not only is this South Korea’s first go-round hosting the Winter Olympics, but PyeongChang could be among the coldest host cities ever, with wind chills in some cases dropping temperatures to an arctic negative 25 degrees Celsius, or negative 13 degrees Fahrenheit.

|

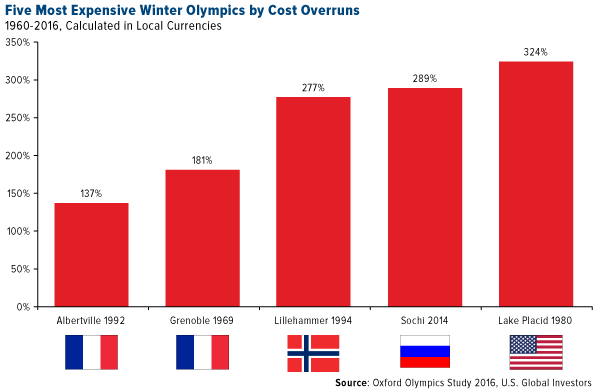

One record that won’t be broken, though, is the cost to host the Games. South Korea spent an estimated $13 billion to bring the rugged, mountainous ski destination up to Olympic standards, building not just stadiums and arenas but also rail, roads, energy infrastructure and more. Amazingly, newly-constructed wind farms in Gangwon Province will generate more than enough energy to power the 16-day event, according to Hyeona Kim, a project manager with the PyeongChang Organizing Committee for the 2018 Olympic Games (POCOG).

Thirteen billion dollars sounds like a lot, but it pales in comparison to the record-breaking $50-55 billion Russia spent to host the Sochi Olympics in 2014.

Sochi Gets Soaked in Debt

Sochi is the most expensive Olympics ever—Winter or Summer. But because Russia’s original price bid was $16 billion, it’s also among the most expensive in terms of cost overruns, according to a 2016 report by the University of Oxford. Looking just at Winter Games, only Lake Placid in 1980 has a bigger cost increase. (The 1976 Summer Olympics in Montreal is biggest of all at 720 percent over budget.)

To put Sochi’s overrun in perspective, the average cost per event is now estimated at $223 million, or a mind-boggling $8 million per athlete.

Contributing to the budget bust was Russia’s need to boost the region’s electricity capacity by as much as 800 percent, leading to the construction of 49 new energy projects. As one deputy minister put it, the undertaking was the country’s largest since Stalin’s time.

Of course, this all raises the question of what economic benefits, if any, hosting the Olympics brings to a city. It took Montreal 30 years to pay off its debt. The 2004 Summer Games in Athens—the birthplace of the Olympics—is now partially blamed for triggering the Greek debt crisis. And in Rio de Janeiro, Brazil, host of the 2016 Summer Games, a number of multimillion-dollar stadiums and arenas sit unused and have become eyesores. (PyeongChang, by contrast, plans to raze the stadium it built for opening and closing ceremonies after the Games are complete.)

Like any other type of investing, there’s no reward without some risk—and, as this week has proven, it’s all about how you manage it.

A Case Study in Good Financial Planning

One city that got it right was Los Angeles.

For many of you, California might not immediately come to mind as a shining example of good fiscal management. But when the city was awarded the Olympics for 1984, the reins were turned over to Major League Baseball (MLB) commissioner Peter Ueberroth, who had previously founded and run a successful travel company. Under his leadership, the 1984 Summer Olympics became the first privately financed Games. A committee was set up that operated more like a corporation. Financing came from private fundraising, corporate sponsorships, TV deals and more.

|

It certainly didn’t hurt that L.A. was already a highly developed metropolitan area with world-class infrastructure, but Ueberroth urged fiscal restraint and rationality. The results were better than anyone could have anticipated. Remember Sochi’s $8 million price tag per athlete? L.A. ended up spending only around $100,000 per competitor (in 2015 dollars), among the best records ever in Olympic history.

What’s more, the L.A. Games turned a tidy profit, netting the city more than $225 million, all of which was plowed back into the U.S. Olympic Committee. As recently as 2016, those profits were still helping athletes gear up for Olympic glory, according to Ueberroth himself.

In 1984, Ueberroth was selected as TIME’s Person of the Year for developing “a new model for the Games” and proving that “in a free society, anything is possible.”

This week I had the chance to speak with Peter Smyrniotis of Market One Media Group about cryptocurrencies, blockchain technology and initial coin offerings (ICOs). Watch the interview by clicking here!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 5.21 percent. The S&P 500 Stock Index fell 5.16 percent, while the Nasdaq Composite fell 5.06 percent. The Russell 2000 small capitalization index lost 4.49 percent this week.

- The Hang Seng Composite lost 9.79 percent this week; while Taiwan was down 6.78 percent and the KOSPI fell 6.40 percent.

- The 10-year Treasury bond yield rose 1 basis point to 2.85 percent.

Domestic Equity Market

Strengths

- Utilities was the best performing sector of the week, decreasing by 2.77 percent versus an overall decrease of 5.02 percent for the S&P 500.

- Tripadvisor was the best performing stock for the week, increasing 11.53 percent.

- Nvidia posted a record-setting quarter. The company beat across the board and said it was a record quarter by all measures. The success comes amid strong demand for its graphics cards from cryptocurrency miners and artificial intelligence.

Weaknesses

- Energy was the worst performing sector for the week, decreasing 8.45 percent versus an overall decrease of 5.02 percent for the S&P 500.

- CBOE Global Markets was the worst performing stock for the week, falling 20.45 percent.

- The Dow Jones Industrial Average fell more than 1,000 points, or about 4 percent on Thursday, extending its drop from the January highs to more than 10 percent, officially marking correction territory.

Opportunities

- Snap shot up 45 percent after earnings. "This is what happens to a stock when sentiment is overwhelmingly negative, expectations are super low and the company shows what seems to be an inflection point," RBC Capital Markets' Mark Mahaney told Business Insider.

- Amazon has started offering Whole Foods deliveries through its Prime subscription service where subscribers can receive deliveries within two hours. The service is currently only in four U.S. regions of Cincinnati, Austin, Dallas and Virginia Beach.

- Tesla reported a smaller-than-expected loss as its cash burn slowed. The electric-car maker lost $3.04, topping expectations, and said it burned through $276.8 million of cash, down from a record $1.42 billion cash burn in the previous quarter.

Threats

- Disney missed on revenue. The company reported that revenue rose by 3.8 percent year-over-year in the first quarter to $15.35 billion, missing the $15.44 billion that was expected.

- The stock market's fear gauge spiked the most on record. The CBOE Volatility Index, or the VIX, spiked 84 percent on Monday, its largest single-day increase on record, according to data going back to 1990.

- Lululemon's CEO unexpectedly resigned after falling short on the company's code of conduct, a company press release said. Shares slumped by more than 3 percent in after-hours trading Monday.

The Economy and Bond Market

Strengths

- Figures from the Institute for Supply Management showed that, in January, America’s service industries – which make up almost 90 percent of the economy – grew at the fastest pace in at least a decade. The group’s 59.9 mark in its non-factory index beat all forecasts in a Bloomberg survey, while its employment gauge rose to 61.6 – the strongest since July 1997 – and the measure of new orders surged to a seven-year high of 62.7.

- The number of Americans filing for unemployment benefits fell last week, dropping to its lowest level in nearly 45 years as the labor market tightened further and reinforced expectations of faster wage growth this year.

- The U.S. economy remains fundamentally strong despite the stock market plunge this week.

Weaknesses

- The U.S. trade deficit widened to the biggest monthly and annual levels since the last recession. The deficit increased 5.3 percent in December to $53.1 billion, the widest since October 2008, as imports outpaced exports, according to Commerce Department data. During 2017, the gap grew 12 percent to $566 billion, the biggest since 2008. This outcome highlights the inherent friction in President Trump’s goal of narrowing the gap while enjoying faster economic growth.

- New York City’s economy slowed in the fourth quarter as the private sector curtailed hiring, according to Comptroller Scott Stringer. The city's economy grew 1.2 percent, compared with a 2.6 percent growth for the U.S.

- Rising bond yields have begun to hit equities, which in turn could lead to tighter financial conditions.

Opportunities

- Chicago was upgraded by Kroll Bond Rating Agency by two levels to A as a result of the city’s progress in addressing underfunded pensions. “The upgrade reflects identification and dedication of permanent ramp-up revenue sources to address severely underfunded pensions,” said Kroll, noting its “expectation that addressing these pension obligations long-term will prove to be affordable and sustainable for the city’s wealth base.”

- California cities will see their general fund contributions to public pensions nearly double over the next seven years, according to a study commissioned by the League of California Cities. This report found that, for the average city, the percentage of the general fund that goes to the California Public Employees’ Retirement System in fiscal 2025 will be nearly double from the percentage in fiscal 2007, going to 15.8 percent from 8.3 percent.

- The Climate Bonds Initiative predicts $20 billion of U.S. green municipal bond issuance in 2018, almost double last year’s record-setting $11 billion. “More than ten new U.S. municipalities entered the green muni market in 2017. We expect this trend to sharpen as institutional investors increasingly seek green investment products for their portfolios," said Justine Leigh-Bell, CBI Director of Market Development.

Threats

- The focus of the week will be Wednesday's U.S. CPI report. Following the recent rise in bond yields, investors will be watching for evidence that core inflation is making progress to the Fed's target. That could put further pressure on bonds.

- Other U.S. economic releases will include the National Federation of Independent Business' small business survey (Tuesday), retail sales (Wednesday) and February's preliminary consumer sentiment (Friday). It will be interesting to see if the recent market turmoil is beginning to have an effect on consumer confidence.

- Kansas’s finances continue to show signs of stress despite projected higher revenue from recent tax increases, S&P Global Ratings said in a report. The state may have a $355 million structural deficit next year because of pension underfunding, higher expenses and use of one-time revenue, said S&P.

Gold Market

This week spot gold closed at $1,316.23 down $16.67 per ounce, or 1.25 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 7.15 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index finished slightly up 0.21 percent. The U.S. Trade-Weighted Dollar reversed course this week and surged 1.32 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-8 | Initial Jobless Claims | 232k | 221k | 230k |

| Feb-14 | Germany CPI YoY | 1.6% | -- | 1.6% |

| Feb-14 | CPI YoY | 1.9% | -- | 2.1% |

| Feb-15 | Initial Jobless Claims | 227k | -- | 221k |

| Feb-15 | PPI Final Demand | 2.4% | -- | 2.6% |

| Feb-16 | Housing Starts | 1230k | -- | 1192k |

Strengths

- The best performing metal this week was gold, down 1.26 percent. China’s demand for gold jewelry rose 10 percent last year to around 700 metric tons due to increasing wealth of residents. China is the largest market for gold in the world.

- Gold demand is also on the rise in India, the second largest consumer of gold, with purchases expected to rise to 800 metric tons, up from 727 tons last year.

- Although gold might be on track for its largest weekly loss since December, gold bulls haven’t lost confidence; instead, they believe that the dollar’s advance won’t last. Gold trading was 133 percent above its 30-day average on Tuesday according to BullionVault, the largest online market for precious metals. John Sharma, an economist at National Australia Bank said, “The recent rout in equity markets should be supportive of gold, although not immediately.”

Weaknesses

- The worst performing metal this week was palladium, down 6.84 percent. According to the weekly Bloomberg survey, gold traders are more bearish than bullish on prices for the first week since early December. The yellow metal is on track for its second weekly drop amid rising interest rate fears. Gold ETF holdings decreased for five days straight while silver ETFs saw three straight days of additions.

- Gold demand in the United Arab Emirates hit a 20-year low last year, its fourth consecutive annual decline, reports Bloomberg. Overall gold demand by central banks and ETFs is at an eight-year low, according to the World Gold Council survey, down 7 percent globally. South Africa, one of the top gold producing nations, saw its output fall the most in 10 months in December by 12.4 percent.

- Credit Suisse is redeeming its note in the highly volatile XIV exchange-traded fund. The VelocityShares Daily Inverse VIX Short-Term ETN, known as XIV, dropped 14 percent on Monday then fell another 80 percent in late day trading.

Opportunities

- Silver may be on the rise as the ratio between gold and silver is nearing a five-year high. If the ratio does reach its five-year average, the trend could reverse and silver could outperform gold, reports Bloomberg. The silver price might also rise due to improving global economic growth and the expanding middle class in China fueling demand for jewelry and solar panels.

- During periods of negative equity returns, gold has historically outperformed equities 79 percent of the time, according to Bank Credit Analyst. Further, the group notes that in periods of rising volatility, gold outperformed 64 percent of the time. Goldman Sachs raised its price outlook for gold to $1,350 per ounce in three months and $1,450 in 12 months, up from $1,225 and $1,255, respectively. With inflation set to return, gold might see a boost as the yellow metal generally performs well during times of rising interest rates. Scotiabank reports that exposure to gold equities in general active portfolios is at the lowest since 2000, which presents an opportunity for buying of shares to match benchmarks.

- Klondex Mines reported its year-end resource statement which was likely going to be a disappointment considering the company spent much of last year trying to bring the True North Mine up to commercial levels and get the Hollister Mine acquisition back into production too. Ultimately True North was put on care and maintenance. Shutting down the distraction of True North should remove a cash drain from the company and allow management to focus on just their core assets in Nevada. Like many gold companies, the Street tries to get the gold companies to grow by acquisitions because that typically leads to investment banking fees. The capitulation downgrade by four analysts after the resource update is more of a looking backward view on what went wrong. The Bloomberg Automation system creates an analysis of past analysts’ recommendations and often is the case you would have done much better by ignoring the timing of these recommendations. For a 200,000 ounce gold producer in Nevada with a significant land package, which shows an array of “Fire Creek” like structures from a geophysical survey conducted on the land package northwest of the high-grade Fire Creek Mine (that only is valued at $278 million), there is a lot of room for improvement in 2018 either by focusing on the core properties or the subject of a takeover.

Threats

- Veteran investor Jim Rogers believes that the next bear market will be the worst in his life, saying that “debt is everywhere, and it’s much, much higher now.” Chief investment strategist at BMO Capital Markets Brian Belski says that markets will hit rock bottom this coming Monday, which is the worst day of the week in terms of historical price performance, writes Bloomberg News. Blackstone Group LP President Tony James said this week that equity markets could fall as much as 20 percent this year adding that “every historic norm says that stocks are very, very fully valued.”

- Investors are seeing more risks with owning longer-dated government debt in the form of bonds with term premiums surging in the Treasuries market, reports Bloomberg. The 10-year Treasury yield is at 2.85 percent, which is well below the 4.45 percent average during the decade beginning in 2000 or the 6.66 percent average the decade before that.

- Randgold CEO Mark Bristow criticized governments and mining companies for what he calls “short-termism,” whereby the push is to extract as many minerals as possible, as fast as possible, from the ground. Bristow says this drives up production costs and doesn’t generate value for countries in the long term.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended February 9 was Unity Ingot, which gained 1,243 percent.

- Singapore Airlines announced Monday that it plans to use blockchain technology to give its frequent flyers a new way to spend their accumulated miles, writes Reuters. This will be done through the launch of a digital wallet app for its loyalty program, beginning in about six months. “The Singapore Airlines technology is its own private blockchain involving only merchants and partners,” the company said in a statement.

- Despite a drop in digital currencies this week, with the total crypto market seeing over $550 billion wiped off its value on Tuesday alone, experts told CNBC that cryptocurrencies could go on a bull run greater than last year and pass the trillion-dollar mark in terms of value. In an email to CNBC, Thomas Glucksmann, head of APAC business development at Gatecoin, wrote that “increasing regulatory recognition of cryptocurrency exchanges, the entrance of institutional capital and major technology developments will contribute to the market’s rebound and push cryptocurrency prices to all new highs this year.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended February 9 was DavorCoin, which lost 33 percent.

- Bitcoin, which surged over 1,300 percent in 2017, has lost nearly half of its value so far in 2018, reports Reuters, as more governments and banks show signs of cracking down on the space. On Monday, other cryptocurrencies also suffered double-digit declines, the article continues, with drops continuing throughout the week.

- China plans to block anyone in the country who tries to access websites that offer cryptocurrency trading services or initial coin offerings, reports Fortune. Chinese authorities already banned ICOs and shut down domestic exchanges, but it is now looking to solve the issue of people accessing foreign services within the country, the article continues. Blocking unwanted foreign websites is nothing new to the Asian nation, using the so-called “Great Firewall of China.”

Opportunities

- According to an article from the International Business Times, Venezuela is the cheapest place in the world to mine bitcoin. Given the differences in electricity, mining in Venezuela is only about $530, which is less than half of what it costs to mine the digital currency in Trinidad and Tobago. On the flipside, the most expensive country in the world for mining bitcoin is South Korea, the article continues, where it costs $26,170.

- Swedish utility company Vattenfall AB, one of Europe’s biggest energy traders, plans to expand further and needs blockchain technology to “do some of the heavy lifting in its computer systems,” writes Bloomberg. Head of business development Kilian Leykam says that by using the digital ledger for more mundane paperwork, resources would be freed up to pave the way for more trading.

- Although the slide in the broader market and the plunge in cryptocurrencies this week, is by no means “good news” for investors in either space, an opportunity lies in understanding the perceived resemblance between the two. As Bloomberg reports, using the chart below, “a regression analysis of the past two years shows a correlation of 0.7 between Bitcoin’s price and the S&P 500, where 0 is the weakest correlation and 1 the strongest.”

Threats

- Following the lead of JP Morgan Chase and Citigroup, Lloyds Banking Group in Britain said on Sunday it would ban its credit card customers from buying cryptocurrencies, reports Reuters. The move is aimed to protect customers from running up huge debts, the article continues, with the banks fearing “a plunge in their value will leave customers unable to repay their debts.”

- Over the next six to 12 months, the most widely used digital coin could lose its spot as a dominant payment system on the dark web, writes Bloomberg. According to cybersecurity firm Recorded Future, Bitcoin has become more expensive and less efficient, pointing people to make use of its competitors instead – most notably, Litecoin and Dash. With an increased percentage of dark web vendors now accepting Bitcoin alternatives, Bloomberg reports that more criminals will turn their sights to these other coins as well.

- The European Central Bank (ECB) has “woken up to the risks digital currencies can pose to policy maker’s bread-and-butter business: the economy,” Bloomberg Technology writes. Executive Board member Yves Mersch noted in an interview this week that by increasingly bridging the virtual world and the real world, a potential collapse in the virtual world could drain liquidity from the real world. Mersch notes that this could become a major concern for the central bank.

Energy and Natural Resources Market

Strengths

- Steel was the best performing major commodity this week rising 0.2 percent. The commodity outperformed as investors continue to profit from China’s environmentally-focused steel production curbs which are expected to last until next month.

- The best performing sector this week was the S&P 1500 Fertilizers and Agricultural Chemicals Index. The index dropped 3.0 percent for the week, outperforming the global equity rout amid speculation that there could be further consolidation in the space, even after the proposed Bayer-Monsanto tie-up.

- The best performing stock for the week was Terra Nitrogen Company LP. This small-cap fertilizer rose 4.9 percent after CF Industries Holdings Inc. announced its intention to exercise its right to purchase all outstanding units of Terra.

Weaknesses

- Crude oil was the worst performing commodity this week. The commodity dropped 9.5 percent as the worst equities collapse since the financial crisis compounded concern over unprecedented supply growth from U.S. oil fields. U.S. production surged to 10.25 million barrels a day last week, according to government data released Wednesday and is forecast to top 11 million a day this November, a year earlier than previously expected.

- The worst performing sector this week was the S&P 1500 Oil & Gas Producers and Explorers Index. The index dropped 10.0 percent tracking crude oil’s largest weekly drop since at least 2016.

- The worst performing stock for the week was Devon Energy Corp. The major oil and gas producer dropped 11.8 percent as energy prices fell. In addition, JPMorgan analysts reiterated their cautious view into the company’s annual report, expecting weaker guidance as a result of a slower start at the company’s Eagle Ford locations.

Opportunities

- Oil majors are generating as much profit at $60 oil as they did when oil reached $100 per barrel in 2014. Oil majors say their focus has changed to earning more from each barrel, rather than pumping it out at all costs. The opportunity for shareholders lies in these companies maintaining or increasing their dividend payout while pledging share buybacks to offset shareholder dilution that occurred during the slump.

- The U.S. dollar may continue to drop, according to commentary from technical analysts. Despite the recent rally in the U.S. dollar, the severity of the breakdown on the weekly charts suggests that the recovery is only a short-term oversold reversion rally. Medium-term, analysts expect the weakness in the U.S. dollar to continue, which should be positive for the overall commodities complex.

- Gold prices may outperform as economists forecast inflation could return “with a vengeance.” A cadre of economists and investors are suggesting higher inflation is around the corner as average hourly earnings grow at the highest rate since 2009.

Threats

- China’s yuan slumped 1.2 percent, the most since the shock devaluation in August 2015, after China’s trade surplus plunged in January. January imports rose 37 percent, smashing earlier forecasts and providing a boost to global commodity demand. However, the ensuing 50 percent drop in trade surplus weakened the Chinese currency, making commodity imports more expensive and suggesting we may see a deceleration in February.

- Eurozone investor confidence is starting to wobble, according to the FT. German investors were markedly glummer about the country’s prospects, with expectations dropping to the lowest since summer 2016.

- West Texas Intermediate crude dipped below $60 a barrel for the first time this year on concern that supply from U.S. shale oil fields is growing too much too fast. In addition, the EIA said on Wednesday that American crude in storage tanks and terminals increased by 1.9 million barrels last week as refiners shut or limited operations to conduct seasonal maintenance.

China Region

Strengths

- The Caixin China Services PMI came in stronger than anticipated. Analysts expected 53.5, but the actual reading came in at 54.7, up from last month’s 53.9.

- Indonesia’s Jakarta Composite Index was the best of a bad bunch this week, declining “only” 1.86 percent in a week that saw selloffs across not just the region, but the world.

- China’s foreign reserves number came in steadily once again, marking the 12th straight monthly gain as the currency stockpile rose to $3.16 trillion.

Weaknesses

- It was an ugly week for most global markets, and Asia was no exception. The Hang Seng Composite Index dropped 9.79 percent over the last five days, and the Shanghai Composite dropped 9.60 percent. Korea’s KOSPI and Taiwan’s TWSE both dropped more than 6 percent in the same time.

- Taiwanese exports missed this month, coming in up 15.3 percent for the January period and missing expectations for a gain of 18.1 percent.

- Both imports and exports missed in Malaysia for the December, or most recent, period. Year-over-year imports gained only 7.9 percent, shy of 13.6 percent expectations, while exports came in at a 4.7 percent pace, well below expectations of a 12.7 percent gain. Industrial production also came in lighter than expected for the December period, growing at a 2.9 percent pace, short of an anticipated 4.6 percent rate.

Opportunities

- Walmart is in talks to purchase up to 20 percent of Indian e-commerce leader Flipkart, Bloomberg News reports, perhaps putting the company’s valuation as high as $20 billion. While the talks are reportedly in advanced stages, the deal has not yet been finalized.

- Indonesia’s economy is forecasted to grow 5.3 percent this year, according to the predictions of the International Monetary Fund (IMF). The inflation outlook remains steady at 3.5 percent.

- China is launching a yuan-denominated crude oil futures contract—set to debut late in March in Shanghai—that could at some point down the road offer a significant alternative to U.S. dollar-denominated global oil transactions.

Threats

- China is reportedly studying the potential impact of imposing various trade measures upon soybeans imported from the United States.

- Sentiment on global markets in the very short term took a significant downturn this week, manifested in the wave of selling and volatility. While global fundamentals continue to appear robust and growing, sometimes fear and selling beget more of the same for a time.

- The Olympics are great, and a joint North-South Korea team is a nice touch, but North Korea remains on its current course nonetheless. Arguably, by making nice for the Olympics, sending in a well-publicized team of some 230 smiling North Korean cheerleaders, and staying atop the press cycle lately, North Korea may actually be winning at a different sort of game.

Emerging Europe

Strengths

- The Czech Republic was the best relative performing country this week, losing 2 percent. The Czech Republic is one of the strongest and faster growing countries in Eastern Europe. Stocks trading on the Prague exchange sold off less than their peers during this week’s global stock slump. Pegas Nonwovens, a textile producer, was the best performing stock, gaining 5.8 percent.

- The Turkish lira was the best relative performing currency this week, losing 1.4 percent against the U.S. dollar. Inflation dropped to 10.35 percent in January from a prior reading of 11.92 percent in December. This was a positive sign for economic stability, as the government is trying to bring inflation down to 5 percent.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 5.3 basis points. Greece has made huge progress toward exiting its bailout program in the summer. However, equities trading on the Athens stock exchange sold off the most among its emerging European peers during this week’s global stock slump. On a positive note, Greece tapped the international markets by issuing a seven year bond, with high investment interest, raising 3 billion euros. Bonds offered a 3.5 percent rate.

- The Russian ruble was the worst performing currency this week, losing 3.1 percent against the U.S. dollar. The ruble weakened with the price of Brent crude oil dropping to five week lows on reports that U.S. oil production is surging even faster than previously forecast.

- Real estate was the worst performing sector among eastern European markets this week.

Opportunities

- The European Union raised its forecast for eurozone growth to 2.3 percent in 2018 from 2.1 percent in November 2017. Acceleration in global growth and a boost in trade are supporting Europe’s economy. Germany, the EU’s primary economic growth driver, is expected to maintain its growth around 2.2 percent, the fastest pace of expansion in six years.

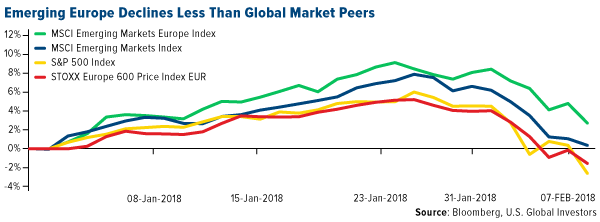

- Global markets have been selling off, but emerging European equites look to be a good hiding place so far. U.S. equites, represented by S&P 500 Index and Western European stocks, represented by STOXX Europe 600 Index, wiped out all year-to-date gains, while emerging Europe declined less than its global peers.

- Russia’s central bank reduced interest rates for the fourth meeting in a row and said it may complete its move to looser monetary policy a year earlier than planned. The rate was lowered by 25 basis points to 7.5 percent, in line with most forecasts. Inflation fell below the central bank’s target of 4 percent last year, which was supportive for the bank’s policy to cut rates faster and support economic growth.

Threats

- Fitch rating agency said that good relations with the EU are important for Poland’s economy, as rising tensions and BREXIT implications could lead to cuts in EU funds for the next budget cycle. Poland is a main beneficiary of EU funds, and if these are cut, it could weaken the country’s economic growth and public finance beyond 2021, says Fitch analyst Arnaud Louis. However, tensions with the EU did not appear to have much impact on investment last year.

- Chancellor Angela Marker of Germany reached a coalition deal with her previous governing partner Martin Schulz. After five months, significant progress was made to form a new government, but there is still more work to do. Next, Marin Schulz needs to convince his Social Democratic Party members, many of whom oppose joining another administration led by Ms. Merker, to approve the coalition. If members reject the deal, the country may face more uncertainty along with a snap election. The result of the Social Democratic Party (SDP) vote is expected by March 4.

- The International Monetary Fund estimates the share of the shadow economy in Russia at 33.7 percent of gross domestic product, reaching the level of African countries. Within the European Union, a similar level of shadow economy is noted in Romania and Bulgaria. In Italy, the shadow economy is also high, about 24 percent. United States, Singapore and Japan have shadow economies at around 15-25 percent of their country’s GDP.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits