The Historic Bull Market Faces Off Against Steel Tariffs

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

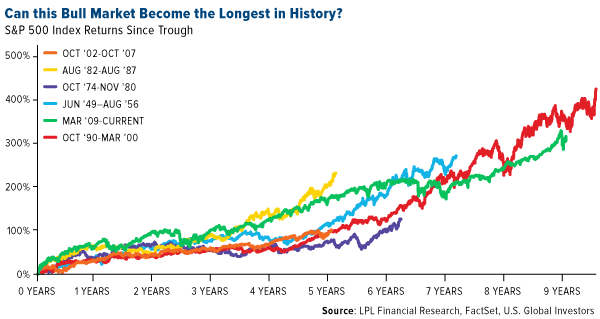

Today marks the ninth anniversary of the stock bull market, the second longest since World War II following the spectacular run in the 1990s that finally met its match when the tech bubble burst in March 2000. The current expansion, which some consider the “most hated bull market in history,” has largely been fueled by extraordinarily accommodative monetary policy in the form of massive money printing and near-zero interest rates. It’s withstood a number of significant headwinds, including a relatively slow economic recovery, the collapse in the price of oil and other commodities, ongoing conflict in the Middle East and an especially nasty presidential campaign cycle. If it can avoid dropping more than 20 percent in the next six months, it will become the longest-lasting ever.

No doubt you’ve heard before that bull markets don’t die of old age. I can’t say for sure what will end this particular business cycle—no one can—but we’re seeing huge shifts in monetary and fiscal policy right now that investors can’t afford to ignore. As I often say, government policy is a precursor to change.

Unintended Consequences of Steel Tariffs

For one, the decade-long era of easy money is coming to an end. The Federal Reserve is unwinding its enormous balance sheet, its enormous balance sheet, which carries some risk.

|

|

Meanwhile, the Trump administration is ratcheting up its protectionist trade policies. After surprising markets last week with plans to impose tariffs on steel and aluminum imports, President Trump signed the authorization yesterday, applying taxes broadly to all countries except Canada and Mexico. It was greatly feared that Canada, the number one supplier of steel and aluminum to the U.S., would be included, but it appears someone managed to change the president’s mind. When former President George W. Bush imposed a steep 30 percent tariff on steel imports in 2002, Canada was likewise spared.

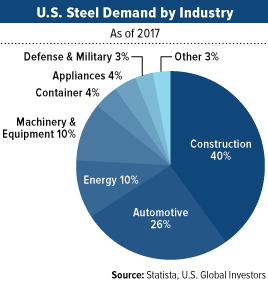

The 2002 tariff, by the way, had some serious unintended consequences that critics of Trump’s policy hope are not repeated. A report put out by the Consuming Industries Trade Action Coalition (CITAC) found that about 200,000 Americans, in every U.S. state, lost their jobs in 2002 as a result of higher steel prices, representing some $4 billion in lost wages. More people, in fact, lost their jobs than the total number of people working in the domestic steel industry itself. Not surprisingly, a quarter of lost jobs occurred in steel-consuming industries such as machinery and equipment, automotive and parts manufacturers.

To be clear, U.S. steel companies did benefit from the tariffs, with profits in the first three quarters of 2002 rising $2.1 billion. This growth was offset, though, by a $15 billion decline in profits for steel-consuming companies.

Today, representatives of those same industries warn that the current tariffs could do more harm than good.

Roy Hardy, president of the Precision Metalforming Association, claims that they “will damage downstream U.S. steel and aluminum consuming companies.” Hardy estimates the tariffs could cost the U.S. economy 146,000 jobs this year alone, a figure that—as was the case in 2002—outnumbers the 140,000 Americans currently employed by the domestic steel industry.

As many as 107 House Republicans expressed deep concerns this week, writing in an open letter to the president that the “new taxes in the form of broad tariffs would undermine” the “remarkable progress” made by the tax overhaul. Meanwhile, outgoing Republican senator Jeff Flake of Arizona said he would introduce a bill that would block Trump’s tariffs.

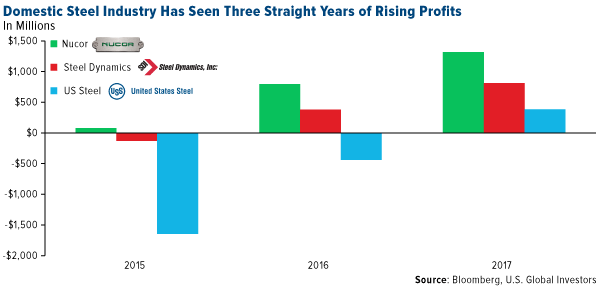

The tariffs come at a time when domestic steel producers’ balance sheets are steadily improving. According to Bloomberg data, the industry posted net profits totaling $2.5 billion in 2017, up from $60 million in 2016. The group lost a whopping $2.5 billion in 2015, with Pittsburgh-based U.S. Steel contributing the heaviest losses at $1.6 billion.

In the coming days and weeks, the tariffs should serve to boost domestic steel production and employment. The Wall Street Journal reports that U.S. Steel has plans to reopen a blast furnace in Granite City, Illinois, and call back 500 workers. This follows an announcement by Century Aluminum that it will double its workforce to 600 at a Kentucky smelter.

I’m pleased to hear this news but remain skeptical on the long-term impact. The U.S. now faces retaliation from its trading partners, from China to the European Union.

A Recession in the Near Term Doesn’t Look Likely

Despite some of the negativity, I see no cause for alarm with regard to the U.S. economy. The country added a whopping 313,000 jobs in February, the most since July 2016 and the 89th straight month of gains—a new record. Economists had anticipated only 200,000. Earlier, Moody’s chief economist Mark Zandi called the job market “red hot,” adding that with “government spending increases and tax cuts, growth is set to accelerate” even more.

One of the most historically reliable economic indicators currently looks very healthy. The Conference Board Leading Economic Index (LEI) opened 2018 on sure footing, posting a 108.1 in January, up a full percent from the previous month. The reading reflects “an economy with widespread strengths coming from financial conditions, manufacturing, residential construction and labor markets,” the Conference Board writes.

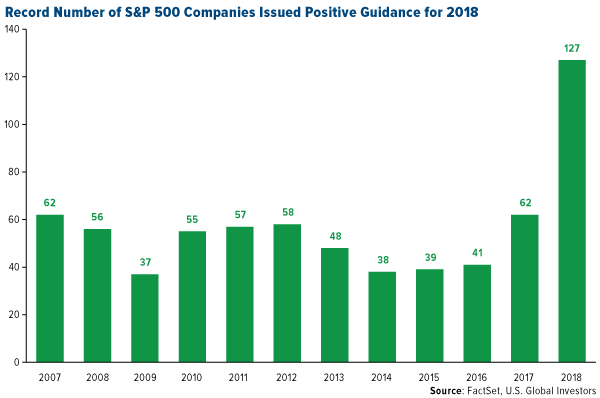

According to FactSet, a record number of S&P 500 companies have issued positive earnings per share (EPS) guidance for 2018. The financial data firm classifies positive guidance as an EPS estimate that’s higher than the mean estimate before the guidance was issued. As many as 127 companies shared positive EPS guidance for the year, more than double the 10-year average of 49 companies for the same period. FactSet attributes this optimism to tax reform, an improving global economy and weaker U.S. dollar.

And it’s not just large S&P 500 companies that are feeling confident. January’s Small Business Optimism Index found that a record percentage of small business owners are eager to expand. Thirty-two percent of owners said that “now is a good time to expand,” the highest such reading in the survey’s 45-year history.

Could Fertility Be a Leading Economic Indicator?

On a final note, a new study lends additional credibility to the theory of “wisdom of crowds,” which states that large groups of people are smarter and better at analyzing data than an elite few. In one recent example, I showed you how investors accurately predicted the election of Donald Trump as far back as July 2016.

But could declining fertility rates predict the next recession? A team of researchers from the University of Notre Dame think so, and they have some compelling evidence to support their idea.

Granted, there's nothing unique about the idea that birth rates drop during and after economic downturns. Married couples have tended to put off expanding their families when they see friends and neighbors being laid off and a greater number of foreclosed homes in their neighborhoods.

What makes this study worth discussing is that it suggests conceptions, those that result in live births, noticeably begin to drop months before a recession strikes. This pattern, according to the study’s authors, can be observed in recessions beginning in 1990 and 2001, as well as the Great Recession.

Above, you can see the percent change in conception rates tumbled sharply some time before GDP growth began to stall or even reverse course. Conception, then, could be used to anticipate recessions just as well as any other economic indicator.

In fact, conception rates could end up being even more accurate “in situations where employment significantly lags the overall economy, and where conceptions lead the economy,” the authors write.

So how are families able to anticipate and act on economic trends more reliably than professional economists? Again, the wisdom of crowds prevails. Everyday people no doubt sense the tremors before the earthquake by hearing things in their firms and comparing observations with friends and acquaintances. There’s no way to quantify this, of course, but live birth records in the U.S. are readily available.

You might be wondering what the data tells us about the economy’s health in the near term. Sadly, the study makes no mention of this. But in January, the Pew Research Center reported that U.S. fertility rates fell to 62 births per 1,000 women of childbearing age in 2017—a new all-time low.

Before you begin to panic, though, it’s important to know that there are different ways to measure fertility, which could skew the data. Also, the drop in fertility could just be further evidence that young adults are choosing to delay starting a family.

Regardless of the rate, people will continue to have babies, increasing the need for even more raw materials and resources.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 3.25 percent. The S&P 500 Stock Index rose 3.54 percent, while the Nasdaq Composite climbed 4.17 percent. The Russell 2000 small capitalization index gained 4.17 percent this week.

- The Hang Seng Composite gained 1.51 percent this week; while Taiwan was up 1.56 percent and the KOSPI rose 2.38 percent.

- The 10-year Treasury bond yield rose 3 basis points to 2.90 percent.

Domestic Equity Market

Strengths

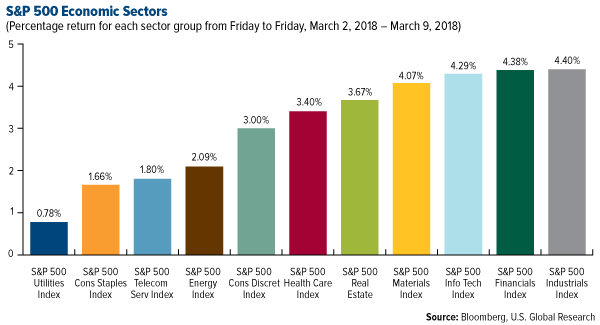

- Industrials was the best performing sector of the week, increasing by 4.40 percent versus an overall increase of 3.32 percent for the S&P 500.

- XL Group was the best performing stock for the week, increasing 28.57 percent.

- IBM told investors Thursday that it has over 400 clients with projects on its blockchain platform. Among its biggest clients are companies like Walmart and Nestlé. It also disclosed a list of banks and trade companies using its blockchain technology.

Weaknesses

- Utilities was the worst performing sector for the week, increasing 0.78 percent versus an overall increase of 3.32 percent for the S&P 500.

- Kroger was the worst performing stock for the week, falling 11.96 percent.

- U.S. stocks plunged on Thursday, with the S&P 500 Index falling 1.3 percent for its third straight weekly loss of 1 percent or more, after U.S. President Donald Trump promised to impose substantial tariffs on foreign metals. The benchmark has had a volatile year so far, closing above or below the 1 percent threshold 15 out of 41 trading days, or 37 percent of the time. That easily surpasses the total of last year.

Opportunities

- Forecasting where the markets are headed is getting more difficult as swings get bigger. While some see a correction in the cards, others favor a buying opportunity. The spike in the CBOE Volatility Index last month is a signal to load up on stocks, according to Credit Suisse’s Jonathan Golub, who found that the S&P 500 Index has historically increased an average of 6.9 percent three months after the VIX rose above 25.

- Apple is rumored to be planning to release a smaller, more affordable HomePod this year. The new HomePod would reportedly cost between $150 and $200.

- Google wants to extend its mobile-accelerated pages (AMP) project to the whole web. This would require building a web standard that uses the principles of AMPs to make web pages across the entire web much faster to load and browse.

Threats

- The U.S. tax overhaul is likely to fuel smaller-than-anticipated dividend and stock-buyback boosts from multinationals. This is due to cautious repatriation by many companies seeking to avoid adverse accounting treatment, writes Bloomberg Intelligence analyst Andrew Silverman.

- Goldman Sachs says a new 'scenario worth worrying about' could cause the next selloff in the stock market. This flash crash and others during post-recession bull markets have occurred against the backdrop of a relatively good economy — and that's the worrying scenario, according to Charles Himmelberg, Goldman Sachs' co-head of global markets research.

- Toys R Us is reportedly about to liquidate its U.S. assets. The retailer has been unable to reach an agreement with lenders and liquidation is the most likely outcome, Bloomberg reports.

The Economy and Bond Market

Strengths

- The U.S. economy added 313,000 jobs in February, the most since mid-2016 and more than expected, Labor Department figures showed Friday. The jobless rate held steady at 4.1 percent for the fifth straight month.

- February’s ISM non-manufacturing composite index came in at a strong 59.5, in line with recent highs. The survey’s gauge of business activity, new orders and backlogs all rose during the month, suggesting continued strength going forward.

- Americans’ sentiment rose last week to the second-highest level since 2001, as the benefits of increased take-home pay from tax cuts outweighed concerns about stock-market volatility, according to the weekly Bloomberg Consumer Comfort Index released Thursday.

Weaknesses

- The U.S. trade deficit widened more than forecast in January to a post-recession high, adding to figures cited by President Donald Trump as evidence of American weakness while he brings the nation to the brink of a trade war. The gap increased 5 percent to $56.6 billion, the biggest since October 2008, from a revised $53.9 billion in the prior month, Commerce Department data showed Wednesday. Exports fell 1.3 percent from December, the most in more than a year, while imports were little changed.

- U.S. average hourly earnings increased just 2.6 percent from a year earlier, less than forecast, following a downward revision to the January figure that previously spooked markets.

- Data from the Commerce Department earlier in the week showed U.S. factory orders in January posted their largest drop in six months. It also revealed business spending on equipment slowed. After five straight months of gains, new orders for factory-made goods in January fell 1.4 percent from December, the largest drop since July.

Opportunities

- Next Tuesday investors will be watching for further evidence that core inflation is making progress to the Federal Reserve’s target.

- Next Wednesday, following a decline in real consumer spending in January, expectations are for a rebound in February's retail sales given the strong consumer fundamentals.

- House Republicans will break President Trump’s infrastructure plan into multiple pieces of legislation as a way to make progress this year, House Speaker Paul Ryan said. Ryan said the House will first address airports and runways as part of a must-pass reauthorization of the Federal Aviation Administration, then work on more traditional highway and bridge issues. Congress will start on infrastructure legislation in the coming weeks, he said.

Threats

- Bond traders have to contend with both larger auction sizes and a condensed schedule when the U.S. Treasury sells $28 billion of three-year notes and $21 billion of 10-year notes on March 12. To JPMorgan Chase & Co. strategists, that combination signals a weak reception. Last month’s offerings, the first since 2009 to increase in size, priced at yields higher than the market was indicating heading into the sales. The 3- and 10-year auctions are usually spaced out over two days, but when they came on the same day in December, yields also missed higher.

- The New York Fed’s GDP Nowcast model sees U.S. first quarter GDP at 2.83 percent versus 3.05 percent in the prior week. A negative surprise from exports data accounted for most of the decline. The St. Louis Fed Real GDP model now sees first quarter GDP at 3.37 percent versus 3.45 percent previously. The Atlanta Fed’s GDP Nowcast model sees first quarter GDP at 2.5 percent compared to 2.8 percent forecast earlier.

- The economic impact of U.S. tariffs is minimal over the near term, said S&P Global Ratings. However, the rating agency said the pending tariffs increase the risk of "retaliatory action" from affected trade partners such as the European Union and China. U.S. steel and aluminum producers are likely to benefit, while other corporate sectors would suffer from higher input costs. Aerospace and defense, capital goods and midstream energy industries are likely to suffer from higher input costs.

Gold Market

This week spot gold closed at $1,323.30, up $0.55 per ounce, or 0.04 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.27 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index came in up 0.35 percent. The U.S. Trade-Weighted Dollar gained 0.22 percent over this week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-6 | Durable Goods Orders | -3.6% | -3.6% | -3.7% |

| Mar-7 | ADP Employment Change | 200k | 235k | 244k |

| Mar-8 | ECB Main Refinancing Rate | 0.00% | 0.00% | 0.00% |

| Mar-8 | Initial Jobless Claims | 220k | 231k | 210k |

| Mar-9 | Change in Nonfarm Payrolls | 205k | 313k | 239k |

| Mar-13 | CPI YoY | 2.2% | -- | 2.1% |

| Mar-14 | Germany CPI YoY | 1.4% | -- | 1.4% |

| Mar-14 | PPI Final Demand YoY | 2.8% | -- | 2.7% |

| Mar-15 | Initial Jobless Claims | 228k | -- | 231k |

| Mar-16 | Eurozone CPI Core YoY | 1.0% | -- | 1.0% |

| Mar-16 | Housing Starts | 1295k | -- | 1326k |

Strengths

- The best performing metal this week was silver, up 0.43 percent as hedge funds cut their bearish outlook. After mostly bearish opinions last week, gold traders are leaning more bullish this week on the yellow metal’s performance. BullionVault’s Gold Investor Index rose last month to 54.1, up from 52.7 the prior month, when it was at the lowest level since August 2017, according to Bloomberg.

- The gold price fell briefly after the release of jobs numbers on Friday; however, it recovered as the dollar fell. On Thursday the gold price rose after China warned of a response to the recently imposed steel and aluminum import tariffs.

- Australian gold mine production in 2017 hit its highest level since 1999 at 301 tons, worth almost A$16 billion, according to Bloomberg First World. Australia is the world’s second largest gold producer behind only China. Those rankings may change as findings released this week from Wood Mackenzie say that Canada’s gold output could grow 80 percent, making it the second largest global producer. Canada is currently the fifth largest producer.

Weaknesses

- The worst performing metal this week was gold, up 0.04 percent. Gold was heading for its third weekly decline as tensions rise with North Korea as President Trump announced he would be willing to meet with the regime’s leader. The largest consumer of gold, India, saw imports fall 31 percent in February on the heels of a 10 percent import tax. Imports for the nation spiked in January knowing that the tax would be implemented February 1.

- Africa’s largest copper producer, the Democratic Republic of Congo, cancelled contracts last minute that guaranteed some producers would be exempt from a royalty increase. Congo is also the world’s biggest source of cobalt and could implement a royalty of 10 percent on the metal, up from 2 percent. These new regulations significantly increase the cost of doing business in the mineral-rich African nation.

- Tahoe Resources Inc. announced that its Guatemalan mine will be required to undergo further environmental and anthropological testing, resulting in additional delays to the restart of production.

Opportunities

- Ecuador’s new mining minister, Rebeca Illescas, reassured investors in an interview this week that the nation will continue to be a burgeoning hotspot for gold and copper mining, reports Bloomberg. Illescas said “We are working to improve tax conditions. It’s important that everyone wins – companies, communities and the state.” At least 28 mining companies have established a presence in Ecuador. Illescas also said that Ecuador is working to eliminate a windfall tax.

- The CBOE/COMEX Gold Volatility Index fell for a third straight week and the largest ETFs tracking gold prices saw their longest run of inflows since last September, writes Bloomberg. This indicates investors are turning to gold as a hedge against the prospect of rising inflation. Dominic Schnider, head of commodities and Asia-Pacific foreign exchange at the UBS wealth-management unit, said this week that “gold has done its job in a portfolio as a diversifier” and that if a trade war does occur it will hit base metals and benefit gold.

- Cardinal Resources Limited released positive drill results at its Namdini Gold Project in Ghana. The company reported a 50 percent increase in the indicated category, up from the previous estimate in September. Highlights include 6.5Moz of gold contained at 1.13g/t. Leagold also reported positive findings at its Los Filos gold mine in Mexico, with reserves increasing by 59 percent from the previous year, which will increase the life of the mine.

Threats

- An economic contraction could happen as soon as next year, reports Bloomberg, with indicators such as Fed policy makers boosting rates and record corporate debt backing up this theory. But if you add in the tariffs that Trump signed this week, will other countries respond by purchasing less U.S. debt? See the chart below. Speaking of debt, U.S. household debt rose in the fourth quarter at the fastest pace since 2007. Other concerns regarding a market correction come from JPMorgan’s executive Daniel Pinto, writes Bloomberg. Pinto warns that equity markets could fall as much as 40 percent in the next two to three years.

- It may be positive that Victoria Gold Corp announced this week it has entered into documentation with Orion Mine Finance, Osisko Gold Royalties and Caterpillar Financial Services. This comprehensive financing package will fully fund the development of the Eagle Gold project, reports Bloomberg. The package totals approximately C$505 million. Osisko has agreed to purchase on a private placement basis, 100 million common shares of Victoria at C$0.50 per share, for total financing by Osisko of C$148 million including the Royalty Purchase, the article continues. The fact that the project was financed with only corporate interest, and not by the street, speaks to the issue that investors are only chasing exposure to gold’s bullion beta and they are not taking the time to analyze the merits of an investment that might deliver some alpha.

- Should Gold Fields’ local unit in Ghana receive government permission to dismiss more than 2,000 of its staff, as it starts the process of hiring a contractor to operate its biggest mine in the West African Nation, the company might end up answering to union members. According to Bloomberg, Ghana’s largest mineworkers’ union plans to protest and strike throughout the operations if the government gives its go-ahead for the layoffs, allowing the contractor to take over the operation.

March 6, 20184 Reasons Why Short-Term Muni Bonds Should Excite You |

March 5, 2018Are Trump's Steel and Aluminum Tariffs Good for America? |

February 27, 2018The World's Cobalt Supply Is in Jeopardy |

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended March 9 was Quebecoin, which gained 202.34 percent. Coinbase will now offer exposure to all cryptocurrencies on its private exchange through an index fund, the Coinbase Index Fund, reports Seeking Alpha. The fund will be weighted by market cap and as new assets are added to the exchange, they will automatically be added to the fund.

- Coinbase also announced this week that it has hired Emilie Choi as vice president of corporate and business development. Choi previously held the same position for eight years at LinkedIn Corp., overseeing 40 deals and predicting similar activity coming up for Coinbase, Bloomberg reports.

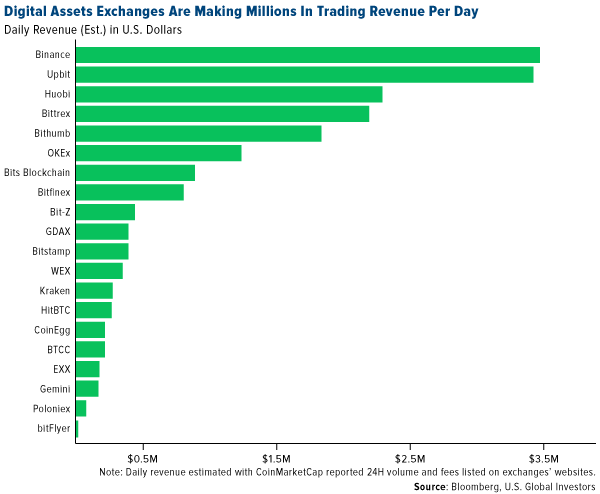

- It looks as though digital-asset exchanges are coming in as one of the biggest winners of the cryptocurrency boom, reports Bloomberg. According to estimates compiled by Bloomberg and CoinMarketCap.com, the top 10 exchanges are generating as much as $3 million in fees a day, or approaching over $1 billion per year.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended March 9 was Tao, which lost 46.73 percent.

- Quebec’s potential as a hub for Bitcoin miners is starting to fizzle, writes the Financial Post. Hydro-Quebec has warned there won’t be cheap power available for every company looking to set up shop in the province, the article continues, and even suggested setting higher tariffs for cryptocurrency miners. “If you want to come settle here, plug in your servers and do Bitcoin mining, we’re not really interested,” Premier Philippe Couillard said.

- Brazil’s Securities and Exchange Commission (CVM) has moved to suspend the offer of securities related to a local Bitcoin mining operation, writes Annaliese Milano for Coindesk.com. The CVM declared the offering for HashBrasil was not authorized, pointing out how it was being solicited across social media platforms. If the operators of HashBrasil fail to comply with the suspension, the securities regulator threatened to fine them, the article continues.

Opportunities

- PayPal has filed a digital currency patent, according to a report dated March 1, for an “expedited virtual currency transaction system,” reports Investor’s Business Daily. The aim of this new system would be to boost the speed of cryptocurrency payments on the platform, Coindesk.com explains.

- According to its latest job postings for equity research positions on LinkedIn, Morgan Stanley is looking to add those with knowledge of the cryptocurrency space to its research team, reports Business Insider. Compared to other Wall Street heads, the chief executive of Morgan Stanley has had a more positive view of bitcoin and digital currencies, the article continues.

- The Commodity Futures Trading Commission (CFTC) can legally classify and regulate cryptocurrencies as commodities, reports Seeking Alpha. According to a court case that the CFTC brought against a cryptocurrency operator, a ruling from federal judge Jack Weinstein has backed this new classification. “Virtual currencies are ‘goods’ exchanged in a market for a uniform quality and value,” Weinstein wrote. “They fall well within the common definition of ‘commodity.’”

Threats

- Austrian banks must take extra steps to comply with rules against money laundering when dealing with virtual currencies like Bitcoin, reports Bloomberg. In a letter to lenders earlier this year, the FMA, which is Austria’s financial markets cop, wrote “Given virtual currencies’ high degree of anonymity, the risks of money laundering and terrorism financing is elevated.” Banks were instructed to demand documentation for alleged Bitcoin gains, the article continues.

- In December, Google searches for the term “bitcoin” peaked, reports Seeking Alpha, just about the time the digital currency crested around $20K. However, as the price “subsequently plunged about 80 percent,” online Google searches have also crashed.

- Cryptocurrencies fell on Wednesday after the SEC issued a statement reiterating the fact that online trading platforms for these digital currencies have to be registered, reports Seeking Alpha. The statement also warned on investor misconceptions with crypto platforms.

Energy and Natural Resources Market

Strengths

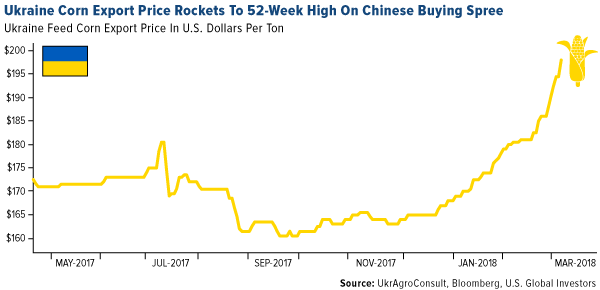

- Corn was the best performing major commodity this week rising 1.52 percent. Corn outperformed other major commodities as Chinese appetite for Ukrainian corn is upending the grain market. The Asian country boosted purchases of corn destined for animal feed, driving the commodity price to a 52-week high.

- The best performing sector this week was the S&P1500 Oil & Gas Refining & Marketing Index. The index rose 5.36 percent as U.S. gasoline stockpiles normalized this week, backed by strong domestic demand and recovering exports. Similarly, U.S. refiners have started spring maintenance season which may result in lower refined product supply in the coming weeks.

- The best performing stock for the week was Smurfit Kappa Group PLC. The Irish manufacturer of paper packaging products rose 25.70 percent after the company announced it had rejected an unsolicited bid from U.S. peer International Paper Co.

Weaknesses

- Iron ore was the worst performing commodity this week. The commodity dropped 4.29 percent as Chinese steelmakers are in a destocking phase as they try to run down stockpiles of iron ore days before state-mandated curbs on steel output are expected to be lifted.

- The worst performing sector this week was the S&P1500 Steel Index. The index dropped 1.25 percent after President Trump signed his steel tariff order Thursday, which now excludes the main sources of U.S. steel imports - Canada and Mexico – in a turn of events compared to a more encompassing tariff outlook that sent this same sector to a 52-week high last month.

- The worst performing stock for the week was International Paper Co. The Memphis-based packaging giant dropped 5.69 percent after Smurfit Kappa rejected a takeover approach by the company, leading investors to believe the company may make a second, and significantly higher bid for the Irish competitor. In addition, Moody’s warned it would view the transaction as credit negative for International Paper.

Opportunities

- China has moved to demonstrate its commitment to growing free trade by agreeing to lower import tariffs for vehicles and some consumer goods. In addition, China will ease or lift restrictions on the shares of foreign-owned equity in companies in sectors including banking, securities, fund management, futures and financial asset management, and explore opening free trade ports.

- The oil industry’s biggest names gathered this week at CERAWeek, the largest energy industry get-together in the Americas. A key turning point this year was the attendance of companies such as Alphabet Inc., and General Motors, which coincide with major discussions on how the oil industry is funding research into big-data, cloud computing and applying new technology to its operations to cut costs and boost production.

- The House Republicans will break President Donald Trump’s infrastructure plan into multiple pieces of legislation as a means to accelerate the economic impact of the plan. House Speaker Paul Ryan said the House will first address airports and runways as part of a must-pass reauthorization of the Federal Aviation Administration, then work on more traditional highway and bridge issues. Congress will start on infrastructure legislation in the coming weeks, he said.

Threats

- President Trump introduced proclamations hammering global steel and aluminum imports with tariffs of 25 and 10 percent. Trump signed the documents at the White House, surrounded by steelworkers, while announcing they go into effect in 15 days. These tariffs threaten to kick start a global trade war, with the EU and China having already announced their intention to introduce countervailing measures. On a positive note, Trump announced allies may apply to be exempt from the tariffs, with two countries are getting relief: Canada and Mexico.

- China’s government said its 2018 economic-growth target would remain around 6.5 percent and predicted a reduction in its budget deficit. The government also announced it would cut excess capacity in the steel sector by 30 million metric tons and by 150 million in coal. The announcement suggests a slowing down of the rate of economic advance seen over the previous two years.

- U.S. shale oil output is set to surge over the next five years as drillers recover rapidly from a three-year slump, the International Energy Agency said on Monday, sharply upgrading its previous growth forecasts. Shale oil production will account for over half of the world’s output growth of 6.4 million barrels per day (bpd), the IEA said in its five-year outlook report. U.S. crude oil production will rise by 2.7 million bpd to 12.1 million bpd by 2023.

China Region

Strengths

- Strongest in the region was South Korea’s KOSPI Index, which jumped 2.38 percent this week. The Shanghai Composite, Taiwan Stock Exchange Weighted Index, and Hong Kong’s Hang Seng Composite all put in strong showings as well, rising 1.62 percent, 1.56 percent and 1.51 percent respectively.

- Consumer goods had a solid week. The best-performing sector in the Hang Seng Composite rose 3.11 percent over the last five trading days.

- A recent Moody’s report notes that China has made significant progress in deleveraging and that containment of financial risk remains a priority, per Bloomberg News. Non-performing loans appeared to remain relatively flat at around 1.74 percent.

Weaknesses

- Indonesia’s Jakarta Composite Index fell by 2.24 percent for the week, while Thailand’s SET Index declined by 1.59 percent.

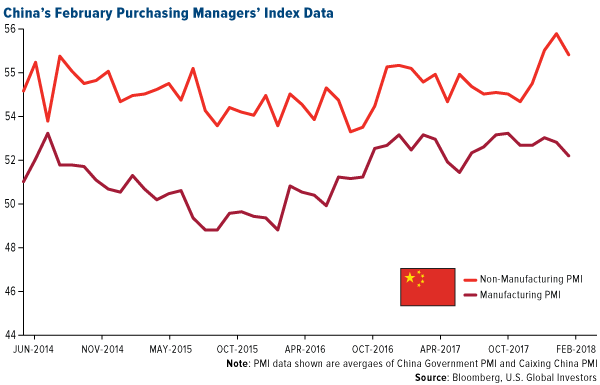

- Last week the official Manufacturing PMI in China came in significantly weaker than expected, falling to 50.3, while Non-Manufacturing had fallen to 54.4. Both were below expectations. Caixin Manufacturing for China came in at 51.6, actually up slightly, and this week we can now add the 54.2 for the Caixin Services PMI, a slight miss.

- The materials sector was the worst-performing of the Hang Seng Composite Index for the week, falling 52 basis points.

Opportunities

- At China’s National People’s Congress this week, policymakers suggested 2018 GDP growth of around 6.5 percent once again. Retail sales growth expectations were set around 10 percent for the year, with consumer price index (CPI) targets set for 3.0 percent and unemployment targets of under 5.5 percent.

- The Trans-Pacific Partnership officially lives again—just not with the United States this time, and under a slightly new name. The 11 signatory nations of the new Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) closed the deal this week, bolstering free trade for an area of about 500 million people, about 13 percent of global GDP, and roughly 14 percent of global exports. The CPTPP nations are Japan, Vietnam, Brunei, Malaysia, Singapore, Australia, New Zealand, Canada, Mexico, Peru and Chile.

- Volvo Cars CEO Hakan Samuelsson suggested this week that “producing [parent company Geely Auto’s] Lynk & Co. vehicles in the U.S. is an option,” and that “if that’s done, we’re ready to support them.” Mr. Samuelsson also noted that Volvo is creating 4,000 jobs at its planned South Carolina plant.

Threats

- Tariffs, tariffs, tariffs. No change here since the initial announcement last week. This week, President Donald Trump proclaimed global tariffs on steel and aluminum, although NAFTA trading partners Mexico and Canada have been exempted for “national security” reasons. All other countries have been invited to negotiate for exemptions, and presumably some will seek them. Of course, some countries may simply retaliate, and China is already discussing U.S.-specific tariffs on coal, steel and some agricultural products, according to Bloomberg News.

- North Korea, North Korea, North Korea. Like tariffs, the announcement on yet-to-be-determined-when historic sit-down with the rogue regime represents a wager of sorts. How precisely said wager plays out is hard to say, but the rough reality is that the North Korean situation remains rife with potential new and plenty of pre-existing problems. There is no simple solution. There is certainly a case to be made that diplomatic contact may improve relations—or at least clarify them, or perhaps bring more transparency to them—but North Korea generally (and the Kim Jong Un regime specifically) has much reputation at risk here, and given the nuclear situation, may even be in the driver’s seat. One might, however, do well to remember that even in the midst of the Cold War, the United States did not cease to talk to its enemy. One also might do well to notice there are some major differences between the Soviet Union and the Kim regime. In sum, once again, this is something of a gamble—and as with all gambles, one must recognize the threat of potential loss.

- While not likely marking a major shift at this point, China’s foreign reserves came in lighter for the first time since early 2017. Reserves came in around 3.13 trillion, down 27 billion from January and shy of analysts’ expectations for 3.16 trillion. The number remains closely watched.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 4 percent. During the Hungarian Chamber of Industry and Commerce conference, Prime Minister Viktor Orban said that Hungary can achieve 4 percent annual economic growth through 2022. He also promised to keep the budget deficit below 3 percent of GDP. Hungary will hold a parliamentary election on April 8. Recent polls show that Orban’s ruling party is losing support.

- The Hungarian forint was the best performing currency this week, gaining 60 basis points against the U.S. dollar. Strong economic data supported the country’s currency this week. Trade balance, retail sales and industrial production surprised to the upside. Inflation fell to 1.9 percent year-over-year in February from 2.1 percent, and final GDP was reported at 4.4 percent, in-line with the prior reading.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst relative performing country this week, gaining 5 basis points. Moody’s cut Turkey’s credit rating one notch lower to Ba2 from Ba1, two levels lower than investment grade. The Turkish government is focused on short-term measures, undermining effective monetary policy and economic reform, according to Moody’s. The ratings agency also pointed out the country’s growing debt level, and worsening geopolitical risk due to military attacks on Kurds in Syria.

- The Czech koruna was the worst performing currency this week, losing 50 basis points. Inflation dipped below the central bank’s target of 2 percent, and policy makers may not be able to continue hiking rates.

- Industrials was the worst performing sector among eastern European markets this week.

Opportunities

- Two important events took place last weekend in Europe. In Germany, Social Democrats voted in favor of a coalition with Angela Merkel, ending a five-month political stalemate. In Italy, the anti-euro Five Start Movement and the anti-migrant League parties gained the most votes, while the ruling Democratic Party got hammered. There was no sign of panic after the voting results were announced in Italy, but now we have to wait and see how the new government will be formed. No formal collation talks can start until March 23, and the process may take weeks or months.

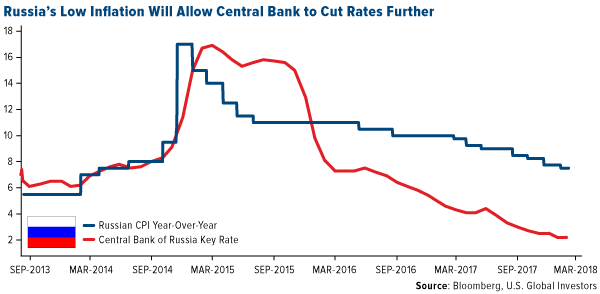

- Annual inflation in Russia remained unchanged at 2.2 percent year-over-year in January, well below the central bank’s target, paving way for more rate cuts. Renaissance Capital predicts a 25 basis points cut to 7.25 percent from the current 7.5 percent on March 23. Further rate cuts should support faster economic recovery.

- The European Central Bank (ECB) has a favorable economic outlook and increased euro-area gross domestic product this year to 2.4 percent from 2.3 percent. It expects inflation to reach 1.7 percent by 2020, which is still below the central bank’s target of 2 percent. In Thursday’s press conference, the ECB dropped the reference to increasing the monthly bond buying program in size and duration. After the meeting the euro lost 80 basis points against the U.S. dollar.

Threats

- The euro-area composite PMI slipped to 57.1 in February from 58.8, below the flash estimate of 57.5 and the weakest reading in four months. Germany grew the least in the three month period and France cooled too. Italy’s gauge also declined.

- Europe is getting ready to retaliate against Trump’s tariffs on imports of steel and aluminum. The European Union proposed taxes on U.S. motorbikes, T-shirts, jeans, corn and bourbon, among other goods. According to Bloomberg, the total value of the imports that would be subject to a 25 percent tariff is 2.8 billion euros ($3.45 billion). ECB President Mario Draghi, during the ECB’s news conference said, “If you put tariffs against your allies, one wonders who the enemies are.”

- Angela Merkel, German Chancellor, suggested that the EU’s funds, for the distribution period between 2021 and 2027, should be linked to member countries’ willingness to accept and integrate migrants. Britain’s departure from the EU, one of the biggest contributors to the budget, will leave a hole of $14 billion per year in the budget. If EU funds are linked to countries’ migrant integrations, Poland and Hungary will receive much less funding, as they are the biggest opponents of the EU’s migrant policy.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits