Rick and Russ argue that the recently enacted U.S. tax cut and an evolving monetary policy backdrop provides both greater clarity on expected increases in volatility and underscores the need to remain flexible and opportunistic in allocation.

In our final blog post of 2017, we argued that the 2018 investment “vintage” would likely be defined by history as marking a cyclical turning point within a much larger secular bull market for global risk assets. We suggested that the ongoing low-volatility, quantitative easing-driven, deflationary boom cycle would likely pivot toward an inherently more volatile fundamental environment. While longer term investment forecasts are by definition opaque, a great deal of clarity has been provided by the events of the past several weeks. Now, in possession of these new and substantive fundamental realities, we are emboldened by our previous prediction, and seek to provide more granularity about our view of 2018’s likely evolution.

Greater clarity with the turn of the year

As 2017 came to a close there were numerous virtuous factors providing a tailwind for risk assets, including about $1.7 trillion of new global liquidity injections during the last three quarters, despite the commencement of Federal Reserve balance sheet runoff. Moreover, accelerating synchronous global growth was basking in the glow of proliferating wealth creation, accelerating wage growth and a deregulatory dawn for the U.S. economy. And then to add to all these tailwinds, with an unexpected swiftness and breadth, came the afterburners of sweeping fiscal stimulus. This cocktail of powerful factors has facilitated an evolution into a new and inherently more volatile cycle that will feature accelerating economic and earnings growth and a nascent rise in inflation.

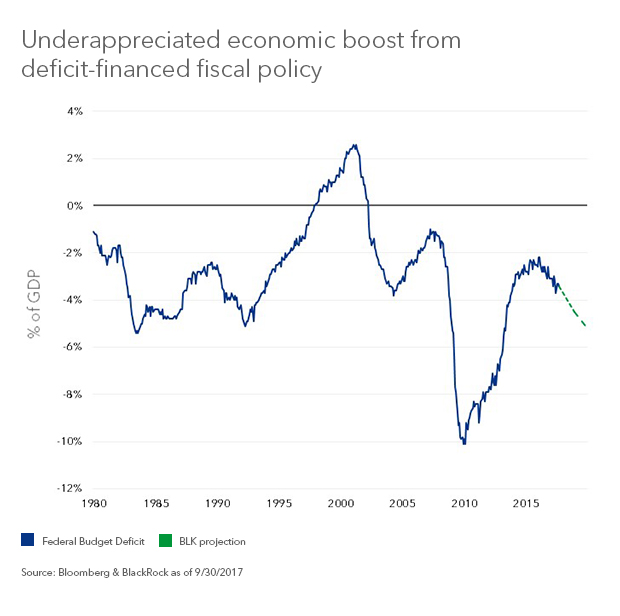

Indeed, in our estimation, the Tax Cuts and Jobs Act of 2017 is a game changer representing a massive deficit-financed pro-growth shock (see graph). Moreover, Congress seems ready to deliver still greater deficit-financed stimulus with a generous budget deal, and possibly a third layer of infrastructure spending. The immediate positive response from corporate America has been impressive as the transmission mechanism of fiscal stimulus has been expressed with intentions to increase wages and bonuses, repatriate billions of dollar of foreign-domiciled capital, boost investment (capital expenditure and research and development), and bolster shareholder outlays. All of this will likely pull 2020–2021 growth forward, adding as much as 0.75% to annual real gross domestic product growth over the near term, by our estimates, alongside an uptick in cyclical inflation driven by accelerating wage growth. At the same time, this fiscal policy regime change creates tremendous uncertainty about the ways in which these initiatives will be funded down the road, which sows the seeds of rising volatility in coming quarters.

Putting it all together it feels like the paradigm shift we foresaw is playing out in ways that resemble the 1986-87 experience. Then, like now, an ongoing secular bull market was enjoying a deregulatory tailwind, a weak U.S. dollar, a relatively stable interest rate environment, and solid organic real growth that led to a collapsing output gap. In the midst of this demonstrable momentum, the 1986 Tax Reform Act catalyzed a powerful incremental risk rally during the first half of 1987, which eventually gave way to an interval of notably higher rates and historic market volatility. But we’re confident that today’s deeper and more mature financial markets will dictate less volatility than that seen in 1987.

Asset allocation in this environment

Over the long run, a risk parity strategy (which is to say, generally being long both risky and less risky assets) is a highly effective way to provide diversified exposure through the ongoing ebb and flow of market cycles. But there are instances in this evolutionary process where that conventional approach must be eschewed in favor of a proactive and tactical strategy that identifies and positions exclusively in positively convex assets with favorable prospective risk-adjusted returns. We firmly believe that 2018 is one of those times.

Specifically, long-dated developed market bonds now offer a precarious combination of ultra-long duration and low yields, which may result in carry breakevens that don’t cover even one half a standard deviation move higher in yields. Similarly, low or negative, yields in short-dated European and Japanese government bonds represent essentially no value whatsoever to investors today, in our view. In contrast, the front end of the U.S. rates curve now offers compelling carry with minimal duration risk on the heels of the late 2017 rate backup.

With respect to global credit sectors, both investment grade and high yield assets provide a negatively convex risk-adjusted return profile, given their highly compressed spreads, while still cheap implied volatility for equities offers attractive, and positively convex, positioning opportunities to express our bullish global economic fundamental view.

In our view, rate-hedged municipal bonds are still attractive in a balanced portfolio for carry (after-tax) as are securitized assets, which are largely impervious to rate and beta volatility. And we think emerging markets local currency assets are a compelling combination of carry and valuation upside potential on a risk-adjusted basis.

Correctly identifying major cyclical turning points that are embedded within larger and persistent secular trends is a critical component to investment outperformance. We are confident that just such a regime change is at hand in early 2018 and are at the ready to embrace a more volatile environment for both the real and financial economy.

Rick Rieder, Managing Director, is BlackRock’s Chief Investment Officer of Global Fixed Income and is a regular contributor to The Blog. Russell Brownback, Managing Director, is an absolute return portfolio manager with a macro focus, and he contributed to this post.

Investing involves risks including possible loss of principal. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. International investing involves special risks including, but not limited to currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of January 2018 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

©2018 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

407458

© BlackRock

Read more commentaries by BlackRock