Could the Stars Be Aligned for $1,500 Gold?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

In a January post, I showed how the price of gold rallied in the months following the 2015 and 2016 December interest rate hikes—as much as 29 percent in the former cycle, 17.8 percent in the latter. Gold ended 2017 up double digits, despite pressure from skyrocketing stocks and massive cryptocurrency speculation.

I forecast then that we could see another "Fed rally" this year following the rate hike in December 2017. Hypothetically, if gold took a similar trajectory as the past two cycles, its price could climb as high as $1,500 this year.

As I told Kitco News’ Daniela Cambone this week, I stand by the $1,500 forecast. Before this week, investors might have been slightly disappointed by gold's mostly sideways performance so far this year. But now, in response to a number of factors, it's up close to 3 percent in 2018, compared to the S&P 500 Index, down 2.4 percent.

Living with Volatility

While I'm on the topic of equities, the S&P 500 dividend yield, for the first time in nearly a decade, is now below the yield on the two-year Treasury. Historically, the economy has slowed around six months after dividends stopped paying as much as short-dated government paper. This could spur some stock investors to trim their exposure and rotate into other asset classes, including not just bonds but also precious metals, which I believe might help gold revisit resistance from its 2016 high of $1,374 an ounce.

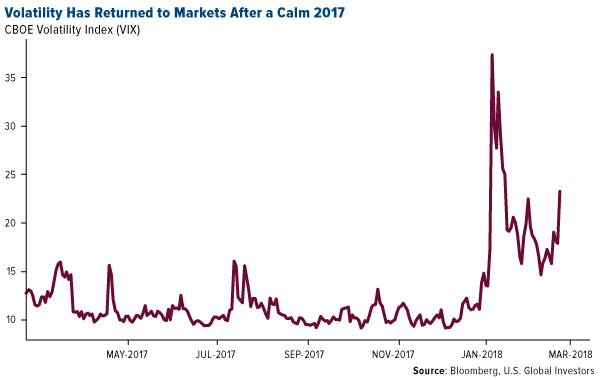

Volatility has also crept back into markets. It began with the positive wage growth report in February, implying the possibility of faster inflation. More recently, the CBOE Volatility Index (VIX), or “fear gauge,” has surged on the departures of Gary Cohn as chief economic advisor and Rex Tillerson as secretary of state, as well as the application of tariffs on steel and aluminum imports. This week, President Donald Trump ordered tariffs on at least $50 billion of Chinese goods, stoking new fears of a U.S.-China trade war. In response, the Asian giant proposed fresh duties on as much as $3 billion of U.S. products, including wine, fruits, nuts, ethanol and steel pipes.

As I see it, there could be other contributing factors pushing up the price of gold. A good place to start is with Trump’s recent appointment of former CNBC star Larry Kudlow as White House chief economic advisor.

Kudlow’s Kerfuffle Over Gold

Between 2001 and 2007, I appeared on Kudlow’s various CNBC shows a number of times, and though he always struck me as highly intelligent, informed and accomplished—he served as Bear Stearns’ chief economist and even advised President Ronald Reagan—it was clear he had a strong bias against gold. This was the case even as the price of the yellow metal was on a tear, rising from $270 in 2001 to more than $830 an ounce by the end of 2007.

Kudlow showed his true colors toward gold as recently as this month, telling viewers: I would buy King Dollar and I would sell gold. As you can see below, this has't been a prudent trade for more than a year now.

Earlier this month, Kudlow wrote that falling gold is good, as it “bodes well for the future economy.” He said he agreed with a friend, who called the metal an “end-of-the-world insurance contract.”

While there are those who would agree with him, it’s important to remember that gold is used for much more than as a portfolio diversifier, and its price is driven by a number of factors. These include Fear Trade factors, from inflation to negative real interest rates, and Love Trade factors such as gift-giving during cultural and religious festivals. The precious metal has important industrial applications as well.

And since I first went on Kudlow’s program, gold has outperformed the S&P 500’s price action nearly two-to-one, as I showed you back in December. Even with dividends reinvested, the market is still trailing the yellow metal.

So it’s fine if gold isn’t your favorite asset, but to dismiss it wholesale as Kudlow has again and again is, with all due respect, irrational.

It’s Not About Steel, It’s About Stealing

Kudlow isn’t just anti-gold, however. He’s also anti-China, and even though he’s traditionally opposed tariffs in general, he supports Trump’s efforts to levy taxes on Chinese imports. Specifically, the duties are designed to offset the cost of intellectual property allegedly stolen by the Chinese over the past several years.

China’s J-31 fighter jet, for example, is believed to be a knockoff of Lockheed Martin’s F-35, the most expensive piece of U.S. military equipment. It’s for this reason that Lockheed’s CEO, Marillyn Hewson, was present when Trump signed the authorization to impose new tariffs.

Our intellectual property is hugely important to the U.S. economy. As important as steel and aluminum are, they account for only 2 percent of world trade, and in the U.S., it’s even less than a percent of gross domestic product (GDP). Technology exports, on the other hand, represent about 17 percent of U.S. GDP.

That said, the implications of a trade war with the world’s second-largest economy certainly have many investors concerned—all the more reason to consider adding to your gold allocation at this time. As always, I recommend a 10 percent weighting, with 5 percent in gold bullion, 5 percent in high-quality gold mining stocks and ETFs.

Is Trump Betting on the Wrong Guy?

On a final note, we were pleased to have an old friend visit our office this week. Michael Ding, a veteran of the U.S. Global investments team, joined us to share some laughs and his thoughts on what’s happening in Asian markets right now.

Specifically, Michael said that Ray Dalio, founder of mammoth investment firm Bridgewater Associates, which manages around $160 billion, has become something of an economic guru for members of the Chinese ruling party’s highest-ranking members, including Premier Li Keqiang. Dalio—whose most recent book, Principles, nowtops China’s bestseller list—is reportedly advising the country’s top bankers and economists on how to deleverage safely without triggering a so-called “hard landing.”

A trade war between the U.S. and China, Ray Dalio said recently, would be a “tragedy.”

So to put it in perspective: Whereas Trump has just now brought on Kudlow, the Chinese are leaning on a fellow American, Dalio, one of the smartest, most gifted money managers in the world—not just of our time but of all time.

Did Trump make the right call? Which player would you want on your team: Kudlow or Dalio? For my money, I would pick Dalio.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 5.67 percent. The S&P 500 Stock Index fell 5.95 percent, while the Nasdaq Composite fell 6.54 percent. The Russell 2000 small capitalization index lost 4.79 percent this week.

- The Hang Seng Composite lost 4.30 percent this week; while Taiwan was down 1.85 percent and the KOSPI fell 3.10 percent.

- The 10-year Treasury bond yield fell 3 basis points to 2.81 percent.

Domestic Equity Market

Strengths

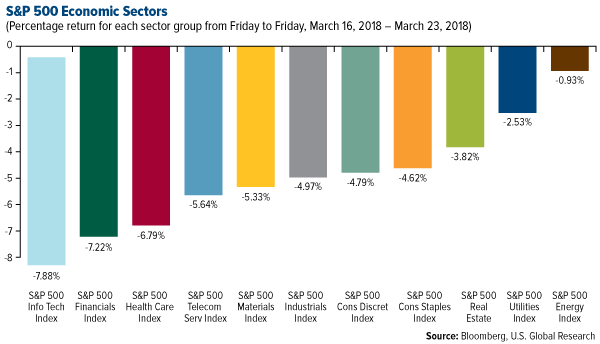

- Energy was the best performing sector of the week, decreasing by 0.93 percent versus an overall decrease of 5.71 percent for the S&P 500.

- EOG Resources was the best performing stock for the week, increasing 5.39 percent.

- Amazon is now the second most valuable company in the U.S. The company finished the week with a market capitalization near $725 billion, trailing only Apple as the most valuable company. Amazon took the number-two spot from Alphabet.

Weaknesses

- Information technology was the worst performing sector for the week, decreasing 7.88 percent versus an overall decrease of 5.71 percent for the S&P 500.

- Oracle was the worst performing stock for the week, falling 14.31 percent.

- The Dow Jones fell more than 700 points, or nearly 3 percent, Thursday after President Donald Trump announced tariffs on $50 billion worth of Chinese exports.

Opportunities

- Nike reported third-quarter earnings that beat analysts' forecasts for earnings and revenue on Thursday. The footwear maker reported $0.68 in adjusted earnings per share, excluding charges related to the Tax Cuts and Jobs Act, and $8.98 billion in revenue.

- JPMorgan Chase & Co is considering a spin-off of its marquee blockchain project Quorum believing independence from the bank could increase the platform's appeal.

- Dropbox priced its initial public offering on Thursday at $21 a share, which was above its previously expected range. That price yielded a valuation of $9.2 billion which was better than expected, but still below what it was worth in its last funding round, according to The Wall Street Journal.

Threats

- Shares of Facebook fell more than 13 percent this week on news that the research firm Cambridge Analytica accessed data from 50 million users without their permission. Further, lawmakers are calling for increased digital regulation which could negatively impact the company’s profitability.

- Boeing looked headed for its biggest monthly drop in two years as of Thursday amid concerns that U.S.-China tensions over tariffs would ignite a wider trade war and stifle demand for its airliners. Shares tumbled to bring its March decline to almost 12 percent by the end of regular trading.

- Spotify's public filings reveal that the company is hemorrhaging money on fees for licensed content and music royalties, and Duncan Davidson, a general partner at the venture-capital firm Bullpen Capital, says the company needs to become a music label to become profitable.

The Economy and Bond Market

Strengths

- The first FOMC meeting under new Federal Reserve Chairman Jerome Powell showed important signals of continuity with the Janet Yellen-led Fed. Powell approved the widely expected quarter-point hike that puts the new benchmark funds rate at a target of 1.5 percent to 1.75 percent. It was the sixth rate hike since the FOMC began raising rates off near-zero in December 2015. The outlook showed Fed officials are opting to do more tightening in future years rather than accelerate the pace in 2018 in order to avoid the risk of stifling potential economic gains from tax reform and to avert excessive flattening of the yield curve. Policy makers acknowledged the soft patch in the economy at the start of the year, but signaled little concern of a lasting slowdown by emphasizing that the “economic outlook has strengthened in recent months.”

- New orders for key U.S.-made capital goods rebounded more than expected in February after two straight monthly declines while shipments surged, which could temper expectations of a sharp slowdown in business spending on equipment in the first quarter. Overall orders for durable goods jumped 3.1 percent last month as demand for transportation equipment soared 7.1 percent.

- The Senate narrowly averted a government shutdown by passing a $1.3 trillion spending bill early Friday. The bill increases military and domestic spending and strengthens background checks for gun buyers.

Weaknesses

- Sales of new U.S. single family homes unexpectedly fell for a third straight month in February, weighed down by steep declines in the Midwest and West. The Commerce Department said on Friday new home sales dropped 0.6 percent. Economists polled by Reuters had forecast that new home sales would rise 4.4 percent.

- While the U.S.’s plan for more tariffs on China hasn’t yet fully reverberated through global markets, some commodities and related measures are already looking fragile. That may be an early indication of an economic slowdown, according to Bank of New York Mellon’s chief currency strategist Simon Derrick.

- With Louisiana fast approaching a self-imposed "fiscal cliff," state legislators are looking for solutions and compromises to balance a $692 million budget deficit and stave off bond-rating downgrades and severe cuts to healthcare and higher education. The problem is that all the options available have been on the table for years and have been rejected multiple times. No measure has gained the bipartisan support necessary to move forward to enact tax increases or spending cuts despite five special legislative sessions focusing solely on budget shortfalls triggered in part by a drop in oil prices four years ago. The latest 17-day special session, which ended in gridlock on March 6, failed to reach an agreement on how to replace the revenue generated by a temporary sales tax-hike that’s set to expire July 1. Lawmakers are preparing for another legislative session before then to try and tackle the deficit.

Opportunities

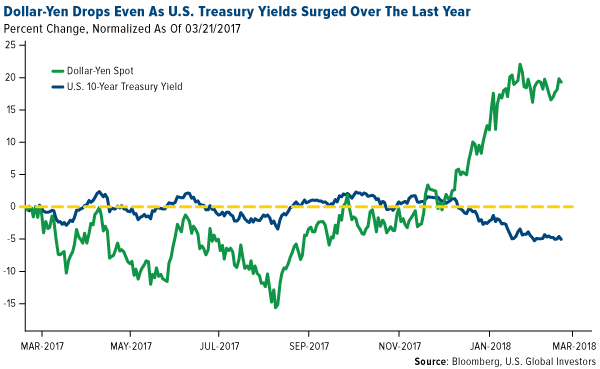

- The U.S. dollar has weakened against the yen even as the divergence between rates in the U.S. and Japan is set to deepen. Interest rates are the base drivers for currency movements, but that link seems to have “somewhat frustratingly broken down so far this year,” said James Binny, global head of currency at State Street Global Advisors. The Bank of Japan has repeated its commitment to its ultra-loose monetary policy, while the Fed is on course to continue tightening policy this year.

- Despite downturns in the stock market and residential construction, an index forecasting economic conditions in the United States continues to forecast growth through the coming year. The Conference Board reported its Leading Economic Index (LEI) rose 0.6 percent to 108.7 in February. Separate measures of current and past conditions also increased.

- Americans’ outlook for the economy climbed in March for a third straight month to match the highest level since 2002, data from the Bloomberg Consumer Comfort Index showed. The monthly gauge of economic expectations increased to 56 from 54.5. The positive outlook could signal a turnaround in consumer spending.

Threats

- China’s ambassador to the U.S. wouldn’t rule out the possibility of the Asian nation scaling back purchases of Treasuries in response to tariffs imposed by President Trump. “We are looking at all options,” Ambassador Cui Tiankai said. “That’s why we believe any unilateral and protectionist move would hurt everybody, including the United States itself. It would certainly hurt the daily life of American middle-class people, and the American companies, and the financial markets.”

- President Trump has put new pressure on Nafta negotiations with an order saying he will impose steel and aluminum tariffs on Canada and Mexico on May 1 if he’s not satisfied with talks. Trump has signed an order to exclude the EU, Argentina, Australia, Brazil, Canada, Mexico and South Korea from steel and aluminum tariffs through May 1, according to a statement from the White House. European Commission President Jean-Claude Juncker said the period is too short and that the EU seeks a permanent exemption from tariffs.

- U.S. companies are finding that the flow from foreign investors is slowing. Foreigners showed signs of being net sellers of U.S. investment-grade corporate debt this week, according to Bank of America data. Any selling pressure comes after international investors bought just $38 billion of U.S. investment-grade corporate debt in the fourth quarter, according to UBS, the least since the beginning of 2016, when the corporate bond market was in a freefall.

Gold Market

This week spot gold closed at $1,347.25 up $32.90 per ounce, or 2.5 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.02 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index came in off 1.90 percent. The U.S. Trade-Weighted Dollar fell 0.82 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-20 | Germany ZEW Survey Current Situation | 90.0 | 90.7 | 92.3 |

| Mar-20 | Germany ZEW Survey Expectations | 13.0 | 5.1 | 17.8 |

| Mar-21 | FOMC Rate Decision (Upper Band) | 1.75% | 1.75% | 1.50% |

| Mar-22 | Initial Jobless Claims | 225k | 229k | 226k |

| Mar-23 | Durable Goods Orders | 1.6% | 3.1% | -3.5% |

| Mar-23 | New Home Sales | 620k | 618k | 622k |

| Mar-27 | Hong Kong Exports YoY | 10.0% | -- | -3.0% |

| Mar-27 | Conf. Board Consumer Confidence | 131.0 | -- | 130.8 |

| Mar-28 | GDP Annualized QoQ | 2.7% | -- | 2.5% |

| Mar-29 | Germany CPI YoY | 1.7% | -- | 1.4% |

| Mar-29 | Initial Jobless Claims | 230k | -- | 229k |

Strengths

- The best performing metal this week was gold, up 2.50 percent. Gold traders are the most bullish they’ve been since January 26, according to Bloomberg’s weekly survey. Gold is headed for its largest gain in five weeks after the Fed projected three interest rate hikes in 2018, easing concern that they would be more aggressive with four rate hikes for the year. The yellow metal historically rises after the Federal Reserve tightens monetary policy.

- Hecla Mining Company will acquire Klondex Mines for $462 million. Klondex shareholders will receive $2.47 per share in cash or shares of Hecla. This is a 59 percent premium to Klondex’s 30-day average. Another big buy happened this week with Alio Gold entering an agreement to buy all the remaining shares of Rye Patch Gold Corp.

- This week saw worldwide holdings in exchange-traded funds backed by gold soar to 2,267 metric tons to reach the highest levels since May 2013. ETFs added 460,196 troy ounces of gold to their holdings last trading session, the most in 6 months, writes Bloomberg. Commodity ETFs also expanded more than fivefold this past week with precious metal ETFs leading the pack. Swiss gold exports rose 39 percent in February to 145.9 metric tons, with exports to India up by 94 percent and up 67 percent to China, the world’s two largest gold consuming countries.

Weaknesses

- The worst performing metal this week was palladium, down 1.91 percent. The government of Mali is looking to revise their mining code, just as other African nations have done recently, which could negatively impact mining companies such as B2Gold who have 40 percent of their production located at their Fekola mine in Mali.

- Zambia will be conducting a tax audit of mining companies that have been operating in the nation in the past six years after uncovering that First Quantum Mineral Ltd. underpaid import taxes on mining equipment. The company revealed on Tuesday that Zambia is demanding $8 billion in interest, penalties and reassessment charges, reports Bloomberg. The Democratic Republic of Congo, who recently updated their mining code to increase royalties and taxes, will likely not be giving any concessions to mining companies who operate there.

- Eldorado Gold has been bumped down to a “sell” versus “hold” after the company’s ability to realize its long-term value was questioned and downside risk has been increasing, reports Bloomberg. Desjardins analyst Josh Wolfson estimates that it will take more than 5 years for Eldorado Gold to realize value from its asset portfolio.

Opportunities

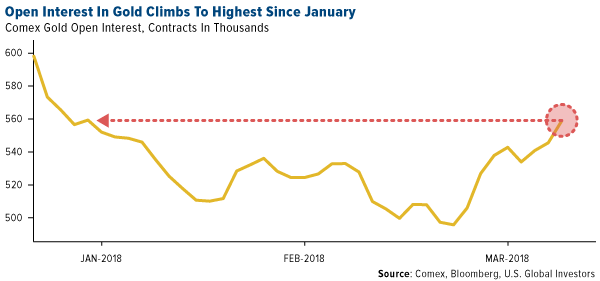

- Open interest in gold futures contracts rose to the highest level since January, ahead of President Trump’s announcement of tariffs on China, reports Bloomberg. President Trump also announced this week that his new national security advisor will be John Bolton. China was reported to have intervened to support its stock market today after fears of a trade led to the steepest intraday selloff in six weeks.

- According to a Bank Credit Analyst report, net inflows to U.S. stocks and bonds have slowed from 3 percent of GDP in 2016 to 1 percent as of now. The broad basic balance (current account plus net Foreign Direct Investment) is worsening, which usually coincides with a weaker U.S. dollar. One of the most renowned gold investors, John Paulson, closed his gold fund amid investor sentiment of indifference to gold. However, from a contrarian this seems like a classic capitulation trade occurrence near a cyclical bottom.

- Bloomberg Intelligence’s Mike McGlone writes that gold may soar to $1,400 per ounce if the dollar remains week and the trend doesn’t reverse. The yellow metal is also showing signs of “increased life” after a second straight quarter of rising deals and slumping to the lowest levels in 4 years in Q3 of 2017, writes Bloomberg. Acquirer’s seem to be more interested in mid –tier producers or near production projects. Cardinal Resources has been bumped to status of “buy” with PT set to A$0.93, up 71 percent from its last close and is just such a company that fits the mold of near production ready decision, as the size of the Namdini Project approached 8 million ounces.

Threats

- Libor-OIS, the London interbank offered rate for dollars over the overnight indexed swap rate, has more than doubled this year to the widest gap since 2009, reports Bloomberg. Some believe that this increase is due to changing investment behavior after the tax overhaul was passed last month. If the Libor-OIS continues to widen, this could lead to a sharper tightening of financial conditions than originally anticipated by central bankers, writes Liz Capo McCormick from Bloomberg News. Citigroup strategists Matt King and Steve Kang wrote that Libor “is still the reference point for the majority of leveraged loans, interest-rate swaps and some mortgages.” The widening could also lead to funding and credit issues for banks.

- Deutsche Bank AG said that the euro’s gain against the dollar will take a toll on their revenue this year. Europe’s biggest investment bank expects a headwind of 300 million euros from currency effects and 150 million euros from higher funding costs of Libor-OIS. The VIX futures curve has traded into backwardation versus its normal contango, which is a sign that the stock market is under stress, reports Bloomberg.

- Leonid Bershidsky, writing for Bloomberg View, reported that President Trump’s import tariffs are designed to benefit industries in political swing states, citing a study by researchers at the University of International Trade and Economics in Beijing and at the University of Virginia. The report shows that the 5 states who employ the most furnace operators are Indiana, Pennsylvania, Alabama, Ohio and Michigan – all swing states. In his first press conference since becoming chairman of the Federal Reserve, Jerome Powell said that policy makers “don’t have the ability to see that far into the future” and advised investors against reading too far into the central banks’ 2020 projections for interest rates.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended March 23 was High Voltage, which gained 367.63 percent.

- According to Fundstrat Global Advisors LLC, the bear market for alt-coins is coming to a close. The firm analyzed three previous alt-coin bear markets where the selloffs lasted around the same time as the surges that preceded them, and now predict that the current drop of 64 days is likely over. The firm says that its data implies “a bull market for alt-coins really starts mid-August to mid-September.”

- Bitcoin gained $1,000 per coin early this week ahead of the G-20 meeting of global finance ministers. The Financial Stability Board issued a letter to the ministers writing that cryptocurrencies do not post a near-term systemic risk to the global financial system.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended March 23 was Desire, which lost 45.10 percent.

- Twitter is following suit of Google and Facebook announcing a ban on cryptocurrency advertisements due to concerns about illegal activities. Ads will be prohibited for initial coin offerings (ICOs), token sales and cryptocurrency wallets globally, reports Sky News. Google announced its ban of cryptocurrency ads last week. More companies are expected to implement similar restrictions in order to avoid putting users at unnecessary risks.

- This week at the G-20 summit in Buenos Aires, world finance ministers have expressed that they increasingly see cryptocurrencies as an asset, not as a currency, reports Bloomberg. Classifying cryptos as an asset would mean that trades could be subject to capital gains taxes. Klaas Knot, president of De Nederlandsche Bank NV, said “I don’t think any of these cryptos satisfy the three roles money plays in an economy.”

Opportunities

- This week Britain’s junior finance minister, John Glen, announced that the government will conduct new research exploring potential risks of cryptocurrencies. Glen added that he plans to continue London’s status as a leading global hub for financial technology experimentation and blockchain technologies, writes CoinDesk. In 2017 the U.K.’s financial technology sector attracted around $1.8 billion.

- A blockchain-based virtual game, CryptoKitties, has been spun off as a separate venture and has already raised $12 million led by Andreessen Horowitz and Union Square Ventures, reports Bloomberg. The game was successful on the Ethereum network when released last November and aims to make blockchain technology more accessible and relevant for everyday consumers.

- According to Morgan Stanley, bitcoin’s path looks much like that of the Nasdaq during the tech bubble’s heyday in 2000, writes Business Insider. The firm argues that bitcoin’s 70 percent fall into a bear market is “a totally normal turn of events” and that the price may soon rise again, just as the Nasdaq did. Morgan Stanley says that “these types of weak spots have historically preceded rallies” – a sign of positivity in times of falling cryptocurrency prices.

Threats

- President Trump signed an executive order on Monday banning U.S.-based financial transactions using Venezuela’s cryptocurrency, the petro. The President warned that the petro is a scam by the Venezuelan government and transactions with the cryptocurrency would amount to supporting the nation’s dictatorship. The petro was announced in December 2017 as a way to help combat out of control inflation, as around 80 percent of the population lives in poverty.

- Cryptocurrency mining has been suspended in the small town of Pattsburgh, New York, after complaints from residents of miners using up much of its low-cost electricity. The city has imposed an 18-month moratorium on crypto mining, reports Bloomberg.

- Researchers from the RWTH Aachen University in Germany discovered files stored in bitcoin’s blockchain linking to websites containing illicit sexual content. The researchers wrote that their analysis “shows that certain content, i.e. illegal pornography, can render the mere possession of a blockchain illegal.” This can endanger bitcoin’s future as those who have downloaded the cryptocurrency’s blockchain may be considered as owning illegal content, reports the Guardian.

Energy and Natural Resources Market

Strengths

- Crude oil was the best performing major commodity this week rising 5.81 percent. The commodity outperformed other major commodities as President Donald Trump welcomed Saudi Crown Prince bin Salman to the White House. Geopolitical experts believe bin Salman and Trump will adopt a stronger posture against Iran, which could result in a drop in Iranian crude exports.

- The best performing sector this week was the S&P/TSX Oil & Gas Producers and Explorers Index. The index was down just slightly by 0.03 percent on the back of a bullish reversal in crude prices. Canadian crude producers outperformed their U.S. peers as expert commentary suggests some of Trump’s tariff announcements against China may result in certain LNG projects not being built. This could re-open the door for development of similar Canadian projects.

- A key performing stock for the week was Fresnillo PLC. The Mexican precious metals miner rose 0.37 percent, outperforming the major London indices as frightful investors traded industrial metals for precious metals exposure as the risk-off environment permeated global markets.

Weaknesses

- Copper was the worst performing major commodity this week. The commodity dropped 3.51 percent on risk-off sentiment resulting from trade disputes between China and the U.S. The metal was also a victim of speculative investors liquidating a near all-time-high long holding.

- The worst performing sector this week was the FTSE 350 Mining Index. The index dropped 4.95 percent after industrial metals posted a sharp weekly decline over the announcement of U.S. tariffs specifically applicable to China. The Asian nation vowed to retaliate, thus risking a global trade war.

- The worst performing stock for the week was Nucor Corp. The U.S. manufacturer of steel products dropped 10.74 percent as the U.S. government said it will shield a list of allies from import tariffs on steel, eroding the benefits to domestic mills.

Opportunities

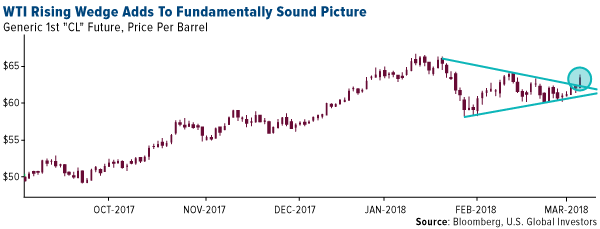

- The visit of Saudi Arabia Crown Prince bin Salman to the White House this week led to a very bullish reversal in crude prices. As evidenced by the chart below, crude oil stuck its head out of a triangular wedge pattern, breaking out to one-month highs as a result of market expectations that bin Salman’s visit will result in a tougher U.S. stance against Iran. Technical analysts have long associated this type of technical behavior with further upward gains, with analysts at the Bank of Montreal suggesting prices could rise to $75 per barrel.

- The copper market continues to be in a supply-demand deficit, according to the International Copper Study Group (ICSG). The group’s preliminary assessment is that the headline shortfall was 163,000 tonnes, or about 0.7 percent of global demand. Albeit marginal, the imbalance facilitates the ongoing destocking and should be supportive for prices.

- Gold buyers continue to defy the Fed interest rate hiking cycle, with global ETF holdings of the yellow metal rising back to the 2013 high. Worldwide ETF holdings have increased nearly 2 percent this year, bringing the total to the highest since May 2013. Analysts suggest the increased interest is a result of higher geopolitical instability.

Threats

- President Trump announced plans to enact $50 billion of tariffs against China over the next 60 days, arguing the Asian nation has engaged in intellectual property violations. The announcement sent global markets into risk-off territory, with commodities and commodity-related equities at the forefront of the selling.

- Similarly, China – which had ignored the provocation up until now – has vowed to retaliate with its own set of tariffs. Albeit much narrower in size and impact (at $3 billion in quoted value), the announcement led to further risk-off sentiment, resulting in sizeable drops in base and industrial metals.

- Inflationary pressures should continue to creep into the profitability of producers of metals and agricultural commodities. The worrying slump in industrial metals and agricultural prices are coming at a time when crude oil prices are rising. Since energy is one of the largest costs in the extraction and production of these commodities, the profitability margins of producers should suffer.

China Region

Strengths

- Malaysia’s FTSE Bursa Malaysia KLCI climbed 1.02 percent amid a relatively rough week for the rest of the region. Malaysia is the region’s only net exporter of energy. Vietnam’s Ho Chi Minh Stock Index also rose for the week, though only 31 basis points.

- The utilities sector of the Hang Seng Composite Index (HSCI) managed to close up 13 basis points for the week, the only HSCI sector to finish in the green during that time frame.

- The Philippines posted a budget surplus of 10.2 billion pesos in January, marking the first budget surplus since last August. The bulk of the revenue rise, as reported by Bloomberg News, was driven by a 19 percent rise in the Bureau of Internal Revenue following the tax reform implementation.

Weaknesses

- Hong Kong’s HSCI was the worst performer in the region for the trading week, finishing down 4.30 percent. The Shanghai Composite closed down 3.58 percent for the week, while South Korea’s KOSPI Index finished down 3.10 percent.

- The HSCI’s information technology sector got pummeled this week, dropping 8.91 percent.

- Taiwan’s year-over-year export orders for the February period declined by 3.8 percent, well short of expectations for a gain of 3.5 percent. Industrial production also declined, with the year-over-year measurement for the February period falling by 1.93 percent, shy of analysts’ expectations for a gain of 1.7 percent.

Opportunities

- In a statement on Wednesday, the People’s Bank of China said that it will permit foreign companies to access its $27 trillion payments markets, reports Bloomberg. This further opens up the world’s second-largest economy. “Applicants must set up local units, establish payment infrastructure, and store client information domestically, the PBOC explained.

- According to a report from CLSA earlier this year, China has rapidly boosted its number of patent applications, particularly in comparison to other global giants (as seen in the chart below). Innovation has been identified as a key goal of China’s next five-year plan through 2020. “Innovation will drive broad productivity gains as the two traditional sources of growth – labor force expansion and capital stock expansion – are fading,” the CLSA report continues.

- Casino operator Galaxy Entertainment Group Ltd. (27 HK) announced a stake in Wynn Resorts Ltd. in what Bloomberg News has called “a surprise move that could have implications for the casino industry in the U.S. and China.” Wynn sold some 5.3 million newly-issued shares to Galaxy Entertainment, giving Galaxy a roughly 4.9 percent stake and solid positioning if the company decides it wants more.

Threats

- “Alex [Trebek, host of Jeopardy], I’ll take ‘Trade Wars’ for $50 billion…”

- In the midst of the ongoing hullabaloo about an (alleged) economics-oriented trade war with China, the media have seemingly abandoned the prospect of any potential deterioration in developments around North Korea and the reportedly upcoming summit.

- According to a widely read Chinese state-run newspaper, China should remain prepared for military action over self-ruled Taiwan, reports Reuters. In addition, the Asian nation should “pressure Washington over cooperation on North Korea after the United States passed a law to boost ties with Taiwan,” the article continues. Beijing has been infuriated with Trump legislation encouraging the U.S. to send senior officials to Taiwan to meet Taiwanese counterparts, and also about trade restrictions. And while U.S. Deputy Assistant Secretary of State Alex Wong said in Taipei this week that America’s commitment to Taiwan has never been stronger, China claims Taiwan as its own. President Xi Jinping made a remark on Tuesday that Taiwan would face “the punishment of history” for any attempt at separatism, Reuters reports.

Emerging Europe

Strengths

- The Czech Republic was the best performing country this week, gaining 17 basis points. Vienna Insurance Group was the best performing equity trading on the Prague exchange, gaining 2.6 percent in the past five days.

- The Czech koruna was the best performing currency this week, gaining 51 basis points against the U.S. dollar.

- Information technology was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 5.02 percent. MOL Hungarian oil and gas company had the most negative effect on the Budapest Index underperformance, losing 6.37 percent in the past five days. MOL and Japan Synthetic Rubber Corporation inaugurated a synthetic rubber plant on Monday. The company plans to invest $4.5 billion in its chemical business by 2030.

- The Turkish lira was the worst performing currency this week, losing 1.71 percent. Geopolitical pressure and rising rates in the Unites States are pushing the Turkish currency lower against the U.S. dollar.

- The health care sector was the worst performing sector among eastern European markets this week.

Opportunities

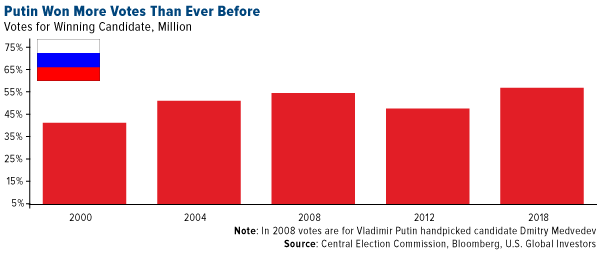

- Presidential results published by the Russian Federation show Vladimir Putin was supported by 77 percent of voters, winning more votes than ever before. Turnout was 67.5 percent, about 2 percentage points higher than in the 2012 election. However, Putin’s biggest opponent Alexey Navalny, says that the official turnout was inflated by 10 percentage points. The opposition is calling this election a “widespread fraud.”

- Great Britain and the EU announced that there will be a two-year transition period following the U.K.’s departure from the EU in March 2019. The deal covers the rights and status of EU citizens in the U.K. and British citizens in the EU, and will allow the U.K. to pursue new trade agreements. It should be a positive development as it will give the U.K. more time to work on outstanding issues and will allow it to have access to the common market for an additional two years.

- Currency analysts predict further euro appreciation against the U.S. dollar. The euro is one of Goldman’s preferred G-10 currencies. The euro is trading around $1.23 to a dollar. And, Morgan Stanley sees the euro ending this year at $1.3, while ING has a high conviction call of $1.35 in 2019. A stronger currency may point to a strong economy, but on the other hand, a strong local currency may put pressure on companies’ exports.

Threats

- Russia will expel 23 diplomats within a week in response to Britain’s decision to expel 23 Russian diplomats from the U.K. It also said it would close the British Council in Russia, which promotes cultural ties between the nations, and the British Consulate in St. Petersburg. The U.K. accused Russia of poising an-ex spy and his daughter in the U.K., but the Russian government denies any involvement in the attack. Russia’s relationship with the U.K. has worsened.

- A slew of weaker economic data is coming out of the eurozone. German ZEW Economic Sentiment plunged to 5.1, down from 17.8 a month ago, the lowest reading since September 2016. Eurozone ZEW Economic Sentiment followed the same path, dropping to 13.4, from 29.3. German business confidence continued to drop in March, making it the second month of declines. Preliminary March manufacturing PMI and service PMI data for the euro block came out weaker as well.

- Kepler Cheuvreux expects major equity markets to fall by another 7 to 9 percent during the month of April. A catalyst for this second phase of declines will be the same one as in January; bond yields continue to rise in reaction to stronger inflationary pressure and expectations of tighter monetary policy. Western Europe’s equites will underperform U.S. equites for two main reasons. First of all, an escalating trade war will hurt European equites as the region is more exposed to foreign markets. Secondly, Europe has weaker profit momentum, with 8 percent EPS growth in 2018 for the STOXX 600 versus 19 percent for the S&P 500, as the tax reform is boosting U.S. profits.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits