U.S. Energy Is Breaking All Kinds of Records — Are You Participating?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

If you recall, during the second presidential debate in October 2016, Hillary Clinton falsely claimed that the U.S. is “now, for the first time ever, energy independent.” Many were quick to point out the inaccuracies. For one, the U.S. has been a net energy exporter before, most recently in the 1950s. And two, America isn’t currently energy independent.

But that could change very soon. As I told you last month, the Energy Information Administration (EIA) estimates the U.S. will become a net exporter of energy by as early as 2022, and the agency recently shared fresh data that supports the narrative that America is on the cusp of taking the throne as the world’s leading energy powerhouse.

The Quest for American Energy Dominance

According to the EIA, U.S. net energy imports in 2017 fell to their lowest levels since 1982. From its high in 2007 of 34.7 quadrillion British thermal units (Btu), the difference between exports and imports has fallen steadily to 7.32 Btu, slightly above the 7.25 Btu in 1982.

The decline last year was mainly due to record exports of crude oil and petroleum products, made possible since Congress lifted the U.S. oil export ban in December 2015.

And for the first time since 1957, the U.S. exported more liquefied natural gas (LNG) than it imported. Between 2016 and 2017, natural gas exports quadrupled from 0.5 billion cubic feet per day (Bcf/d) to 1.94 Bcf/d. The EIA attributes this acceleration to the expansion of export facilities in Louisiana and Maryland, with six additional ones currently under construction, according to Energy Secretary Rick Perry. As a result, the International Energy Agency (IEA) projects the U.S. will become the world’s leading LNG exporter by the mid-2020s.

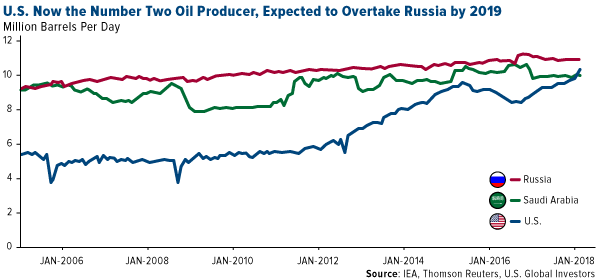

All of this follows news that the U.S. is now the world’s number two crude oil producer. Late last year, U.S. output exceeded 10 million barrels a day for the first time since 1970, thanks largely to the surge in fracking and horizontal drilling activity. This helped push the country ahead of OPEC leader Saudi Arabia, and, by 2019, it could surpass Russia to become the largest producer in the world.

Oil Majors Reward Shareholders

Some resource investors might worry that all this extra supply could depress prices and hurt profits. That’s a valid concern, but it’s worth pointing out that since its recent low of $26 a barrel in February 2016, the oil price has surged nearly 150 percent—all while the number of active wells in North America has risen.

It doesn’t hurt, of course, that demand for petroleum products is just as strong as it’s ever been right now. According to the latest monthly report from the American Petroleum Institute (API), U.S. demand in February reached its highest level since 2007. This was only the third February ever, in fact, that gasoline demand exceeded 9 million barrels a day, reflecting strenthening consumer sentiment and economic growth.

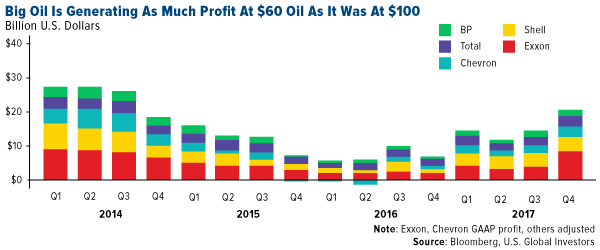

And as I shared with you last month, major explorers and producers’s profits are now in line with what they were when oil was trading for $100 a barrel and more.

According to Bloomberg, the majors are now “prioritizing investors over investments, channeling the extra cash that comes from $60 crude into share buybacks and higher dividends.”

I should add that, besides offering better opportunities for investors, energy independence helps make the U.S., its allies and, indeed, the whole world more secure.

China Launches Oil Futures Contract, OPEC and Russia Enter Historic Pact

Other important developments are happening around the world right now that are already disrupting the global energy space.

The most notable is that China on Monday launched its own crude oil futures contract. Priced in yuan and traded on the Shanghai International Energy Exchange, it’s the first such Asian benchmark for oil deals.

As the world’s largest consumer of crude, China seeks to gain some pricing power in the trillions of dollars of oil that are traded every year around the world. Back in April 2016, the country introduced its own yuan-denominated fix price for gold—which it also consumes more of than any other country. The Shanghai oil futures contract is similarly designed to wrest some control over pricing from the main benchmarks in New York and London—West Texas Intermediate (WTI) and Brent—and to promote the use of the yuan, also known as the renminbi.

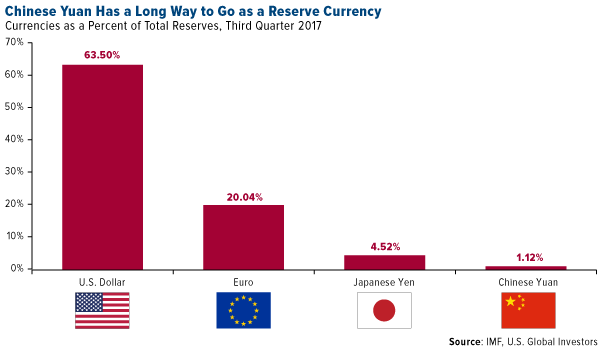

Raising the yuan’s profile and transforming it into a leading global currency has been among Chinese president Xi Jinping’s key endeavors. He scored a big win in 2015, if you recall, when the International Monetary Fund (IMF) agreed to include it in its basket of reserve currencies, placing the yuan in the same league as the U.S. dollar, British pound, Japanese yen and euro.

But as you can see below, the yuan has a long way to go in its quest to challenge other currencies. As of last year, the U.S. dollar accounted for 63.5 percent of countries’ allocated reserve currencies, compared to the yuan, which had only a 1.12 percent share. Shanghai oil futures could possibly help improve that allocation.

The contract opened strong on Monday but has since fallen below WTI prices as speculators placed a series of bearish bets.

In other news, OPEC and Russia are reportedly hashing out the details on a historic alliance that would extend oil production curbs for a number of years, according to a Reuters exclusive. Saudi Arabia’s crown prince, Mohammed bin Salman, told the agency that Riyadh and Moscow were “working to shift from a year-to-year agreement to a 10- to 20-year agreement.”

Although not a member of the Organization of Petroleum Exporting Countries, Russia has often worked alongside the cartel to limit production in an effort to boost prices. A 10- to 20-year deal, however, would be unprecedented.

Oil price weakness has hurt both Russia and Saudi Arabia, as crude exports account for an oversize percentage of their total revenue. And as I’ve shared with you before, Saudi Arabia also seeks higher prices to support a possible initial public offering (IPO) this year of Saudi Aramco, the largest energy company in the world by far.

Staying Hopeful this Easter and Passover Weekend

This weekend, millions upon millions of people across the globe will be observing Easter and Passover, two very

|

important holidays in the Christian and Jewish faiths. It's only appropriate that they should fall in the spring, as both are celebrations of renewal and hope. I'm a firm believer that your thoughts drive your actions, and that your beliefs largely determine the trajectory of your life, from your health and career to the friends you make along the way to even your finances.

This is why I choose to greet every day with positivity, mindfulness and a fresh perspective. Holidays such as Easter and Passover help reinforce this habit. I encourage each of you reading this to take the opportunity this weekend to dare to believe in hope.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.42 percent. The S&P 500 Stock Index rose 2.07 percent, while the Nasdaq Composite climbed 1.01 percent. The Russell 2000 small capitalization index gained 1.28 percent this week.

- The Hang Seng Composite fell 0.57 percent this week; while Taiwan was up 0.21 percent and the KOSPI rose 0.81 percent.

- The 10-year Treasury bond yield fell 7 basis points to 2.74 percent.

Domestic Equity Market

Strengths

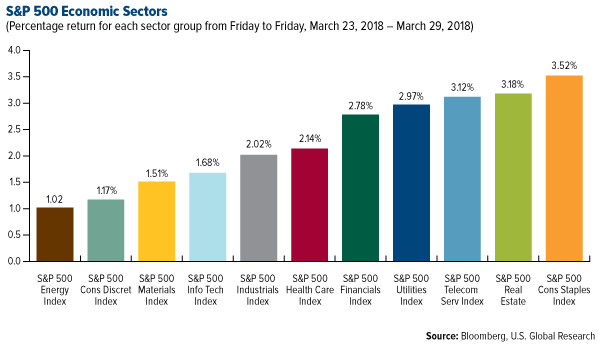

- Consumer Staples was the best performing sector of the week, increasing by 3.52 percent versus an overall increase of 2.34 percent for the S&P 500.

- Macy’s was the best performing stock for the week, increasing 9.30 percent.

- The exchange group CME has agreed to buy the British-headquartered interdealer broker Nex Group for $5.48 billion.

Weaknesses

- Energy was the worst performing sector for the week, increasing by 1.02 percent versus an overall increase of 2.34 percent for the S&P 500. Advanced Micro Devices was the worst performing stock for the week, falling 5.46 percent.

- Amazon fell as much as 7.4 percent Wednesday following an Axios report suggesting President Donald Trump wanted to go after the company. Shares ended the day down 4.29 percent after the White House said it had no immediate plans for policy changes.

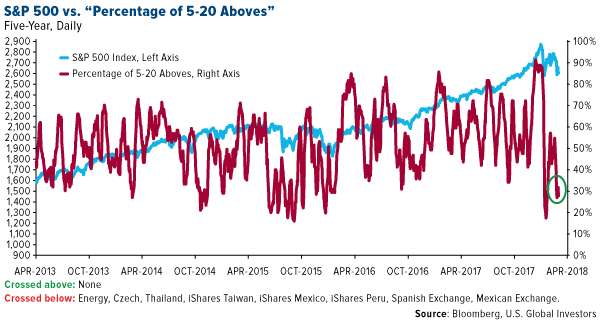

- Among 126 select markets, sectors and assets, the percent of those whose five-day moving averages were above the 20-day moving averages was 27.8 as of March 28. No items crossed above for the day, suggesting muted momentum in the short-term.

Opportunities

- Lululemon beat on both the top and bottom lines and gave strong guidance, saying it expects first quarter earnings of $0.44 to $0.46 a share on revenue of $612 million to $617 million.

- Spotify said it expects revenue growth of 20 percent to 30 percent this year in a forecast published a week before the firm goes public. The company also expects to have signed up between 73 and 76 million paying subscribers for the month.

- Apple released a new 9.7-inch, cheaper iPad and a homework app called "Schoolwork," all designed at boosting its presence in the classroom.

Threats

- Major issues at technology stock market darlings like Facebook, Apple, Amazon, and Tesla have flared up at the same time, threatening to remove strength in a group that has been indispensable during the nine-year bull market.

- Tesla's credit rating was downgraded by Moody's on concerns that the electric car company burns through cash, fails to meet production expectations and may soon have to raise more than $2 billion. The corporate rating was lowered to B3 from B2 and its newly issued $1.8 billion of bonds were cut to Caa1. Shares tumbled more than 7 percent on the news.

- Facebook will close off access to third-party data brokers such as Experian, which advertisers use for highly targeted ads on its platform. The move will likely dent ad revenue but, Facebook said, it will also improve people's privacy. Further, the U.S. Federal Trade Commission said it will investigate Facebook due to the Cambridge Analytica scandal, sending the firm's stock plummeting further.

The Economy and Bond Market

Strengths

- GDP expanded at a 2.9 percent annual rate in the fourth quarter of 2017, instead of the previously reported 2.5 percent, the Commerce Department said in its third GDP estimate for the period.

- U.S. personal income rose 0.4 percent in February, matching economists’ expectations.

- U.S. pending home sales rose 3.1 percent in February, beating expectations of 2 percent.

Weaknesses

- Chicago purchasing managers’ index (PMI) data fell in March to a reading of 57.4, a one-year low, from 61.9 in February. Any reading over 50 indicates improving conditions. Employment expanded in March but orders and production slowed.

- The release of the Dallas Fed Texas Manufacturing Outlook Survey for March showed the latest general business activity index came in at 21.4, down from 37.2 in February and missing expectations of 33.5.

- The U.S. merchandise-trade deficit expanded in February to the widest level in more than nine years, while inventories rose at wholesalers and retailers, according to preliminary figures from the Commerce Department. The goods-trade gap inched up to $75.4 billion (estimated $74.4 billion) from $75.3 billion the prior month. Wholesale inventories rose 1.1 percent from the previous month (estimated 0.5 percent), while retail stockpiles climbed 0.4 percent.

Opportunities

- The Atlanta Fed's GDPNow index for predicting U.S. economic growth rose for the first quarter of 2018. The index now suggests GDP will expand 2.37 percent in the quarter, up from 1.79 percent in its previous release on March 23. The projection compares with the 2.5 percent consensus forecast of 60 economists and contributors in a Bloomberg survey. The New York Fed's GDP forecast for the same period rose to 2.85 percent on March 23 from 2.73 percent a week earlier.

- Next Friday's U.S. employment report will take center stage. Strong jobs growth and a dip in the unemployment rate should confirm that growth is above-trend and any weakness in first quarter GDP is unlikely to persist.

- Wednesday's flash consumer price index (CPI) will be the key data release from the eurozone. The CPI report will tell if the strong growth and absorption of excess supply are translating into higher inflation.

Threats

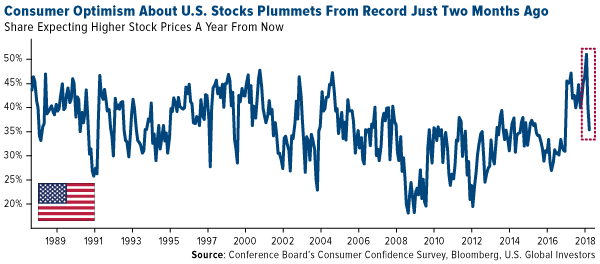

- Two months ago, when equity markets were at all-time highs, a record 51 percent of Americans expected stocks would keep rising in the year ahead, the Conference Board’s consumer confidence data showed. Such optimism quickly unraveled after an early February market slump and increased volatility. Just 35.4 percent of respondents in March anticipated that stocks will move higher in the next 12 months, marking the largest two-month decline in records dating back to 1987.

- Next week’s ISM surveys, manufacturing on Monday and non-manufacturing on Wednesday, will be important indicators of the recent softening in manufacturing data.

- The next recession will originate in the highly-leveraged corporate sector, sparking a sharp decline in employment and profitability, Scott Minerd said in a note. A corporate debt-based recession will be followed by widening spreads in anticipation of more company defaults, said the chief investment officer of Guggenheim Partners, who recommended investors trade up in quality and shorten duration.

Gold Market

This week spot gold closed at $1,325.53, down $21.72 per ounce, or 1.61 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.78 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index slid 2.58 percent. The U.S. Trade-Weighted Dollar reversed course this week and rose 0.72 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-27 | Hong Kong Exports YoY | 7.0% | 1.7% | 18.1% |

| Mar-27 | Conf. Board Consumer Confidence | 131.0 | 127.7 | 130.0 |

| Mar-28 | GDP Annualized QoQ | 2.7% | 2.9% | 2.5% |

| Mar-29 | Germany CPI YoY | 1.7% | 1.6% | 1.4% |

| Mar-29 | Initial Jobless Claims | 230k | 215k | 229k |

| Apr-1 | Caixin China PMI Mfg | 51.7 | -- | 51.6 |

| Apr-2 | ISM Manufacturing | 60.0 | -- | 60.8 |

| Apr-4 | Eurozone CPI Core YoY | 1.1% | -- | 1.0% |

| Apr-4 | ADP Employment Change | 203k | -- | 235k |

| Apr-4 | Durable Goods Orders | -- | -- | 3.1% |

| Apr-5 | Initial Jobless Claims | -- | -- | 215k |

| Apr-6 | Change in Nonfarm Payrolls | 185k | -- | 313k |

Strengths

- The best performing metal this week silver, down 1.13 percent. Gold traders were split this week between bullish and bearish outcomes, according to the weekly Bloomberg survey. The yellow metal is on its best run since 2011 as it wraps up a third consecutive quarter of gains and exchange-traded funds backed by bullion are also near the highest in five years. Following two takeovers announced last week, Goldfields has entered into an agreement to purchase a 50 percent stake in Asanko Gold Ghana’s interest in Asanko Gold Mine for an upfront payment of $165 million. This is the second acquisition whereby Goldfields has elected to purchase at the project level and not takeover the company.

- With U.S. protectionist trade policies ever-increasing, world banks are looking away from the dollar, and seeking to build their currency reserves with the euro. As a U.S. trade war with China is threatened, the European Union is searching for trade deals all over the world, in particular in Asia and Latin America, writes Bloomberg. Jens Nordvig, a former Wall Street top-ranked currency strategist, said “A lot of countries around the world are turning to Europe for increased partnership in trade.” This could weaken the dollar, which is historically positive for the price of gold.

- In January and February, gold demand was lower than expected in India, the world’s second largest consumer of gold, due to a looming goods-and-services tax. However, consumption seems to be returning to the precious metals market after the 3 percent tax has now been implemented.

Weaknesses

- The worst performing metal this week was palladium, down 2.44 percent as some investor turn sour on the metal after its stellar performance last year and poor showing so far this year. Gold saw its biggest two-day loss in more than eight months after the U.S. dollar rebounded earlier this week when Chinese President Xi Jinping announced that North Korea’s leader King Jong Un would be willing to meet with President Donald Trump regarding giving up nuclear weapons, reports Bloomberg News.

- Historical data shows that market corrections since 2009 have taken an average of 200 days to fully recover and have lopped 14 percent from the S&P 500. If the market is entering a correction phase now, it might take until August to fully correct.

- Kinross Gold will pay $950,000 after settling allegations of failure to implement adequate accounting controls at two of its African locations. According to Bloomberg First World, the SEC alleges that the company awarded a “lucrative” contract to a company preferred by Mauritanian government officials and contracted with a “politically-connected” consultant to facilitate contracts with the Mauritanian government without diligence.

Opportunities

- Goldman Sachs is bullish on gold for the first time in five years due to expected increases in inflation and a heightened risk of a stock market correction, reports Seeking Alpha. The company’s computer bull/bear market indicator is above 70 percent, which is associated with high risks for investors. Nicolas Mathier, managing partner at Global Precious Metals, says that gold will trade higher since “Gold is mainly bought as a hedge against systemic risk or counter-party risk.” UBS is also bullish on gold, increasing its price forecast to $1,300 to $1,400 over the next three months, up from a range of $1,275 to $1,375.

- Bloomberg reported this week that the U.S. is brokering a side deal with South Korea to avoid competitive devaluations as part of its exemption from tariffs. The bigger signal is that the U.S. is using the tariff card to extract certain policy objectives, such as the U.S. doesn’t want South Korea to devalue its currency relative to the dollar. This seems to support the notion that the U.S. does not want to see a strong dollar and its extracting agreements to make that a certainty.

- Pandion Mine Finance LP, an investment fund backed by prominent commodities investors, raised $175 million to finance small precious and base metals miners. Many banks have left the sector of funding smaller mining projects, leaving an opening for less traditional sources of capital for raising money. RBC Capital Markets reports that of the around $925 million raised by junior precious metals companies so far in 2018, only 14 percent has come from traditional equity sources with the rest from alternative lenders, streamers/royalties, excreta. The shift in funding has largely been driven by investors blindly buying gold mining stock ETFs for the exposure to gold’s beta, and not conducting any due diligence on the merits of the underlying securities. The net result is there are lots of cheap non-index companies that may see the first benefits of industry consolidation as the seniors scramble to replace their depleting resource base and falling production profile.

Threats

- The Conference Board survey of U.S. consumer sentiment in March shows that retail investors are at their least enthusiastic for stocks since President Donald Trump was elected in November 2016. Bloomberg reports that only 6 percent of those surveyed believe that equities will be higher than they currently are in one year’s time. According to Jonathan Swan of Axios, President Trump is anti-Amazon, as he believes the online retail giant is helping to kill brick-and-mortar retailers.

- One analyst believes that gold may decline to $1,200 by the end of the year due to Fed interest rate hikes. Rajiv Biswas, Asia-Pacific chief economist at HIS Market, said this week at a conference that “Rising interest rates in the U.S. reduce the incentive to hold gold as an investment.” Many disagree with this analysis as gold historically performs well in times of rising interest rates.

- Ivanhoe Mines released a statement saying that several international companies with active mines in the Democratic of Congo are addressing the government and expressing concern that the new mining code changes would negatively impact revenues. The DRC is the world’s largest supplier of cobalt, which is the key element in rechargeable batteries powering most electric vehicles. Recently the DRC government implemented many changes to its mining code for foreign companies, including raising taxes and royalty fees significantly.

March 29, 2018Gold Shines Brighter In the Face of Market Volatility |

March 27, 2018Looking Ahead to $20,000 Bitcoin |

March 26, 2018Could the Stars Be Aligned for $1,500 Gold? |

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended March 29 was VapersCoin, which gained 509.42 percent.

- Coinbase, the most popular platform for trading cryptocurrencies, announced on Monday that it intends to add ERC20 token support to its products. ERC20 is a standard used by Ethereum and smart contracts and is seen as essential to many initial coin offerings (ICOs), according to CCN.

- Tradewind Inc. launched a digital gold platform that is “expected to revolutionize the trading, settlement, and ownership of physical gold” by using blockchain technology, reports Kitco News. Another connection between gold and cryptocurrencies this week is that a 20 pound, solid gold cast of Nelson Mandela’s hand was sold for $10 million in bitcoin. The gold cast was purchased by Canadian cryptocurrency company Arbitrade, who plans to host a world tour of Mandela art.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended March 29 was DMarket, which lost 32.53 percent.

- Joining the ranks of Facebook and Google, Twitter also banned cryptocurrency advertising as of Tuesday to avoid giving publicity to potentially fraudulent practices, writes Reuters. The ban will include advertising of ICOs, token sales, cryptocurrency exchanges and wallet services.

- The cryptocurrency market as a whole has been extremely volatile this week, moving up and down within the range of $280 billion and $350 billion, reports CCN. Several major coins such as bitcoin, Ethereum and Ripple all followed a similar pattern with drops as well as upward swings.

Opportunities

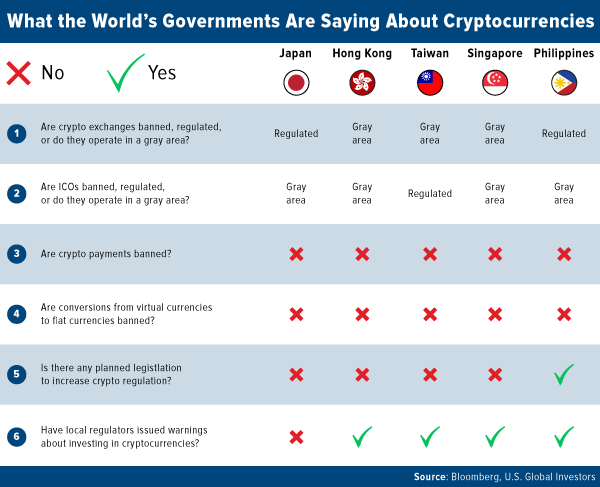

- Ahead of the G20 meeting of global finance ministers in Buenos Aires, Bloomberg compiled an overview of what major countries are doing right now in terms of cryptocurrency regulation. The compilation notes that most of the world’s crypto trading happens in Asia, in particular, Japan and Hong Kong. In Canada, ICOs are treated as securities and stock exchanges have become popular destinations for crypto-related stocks and ETFs, while crypto trading in the U.S. takes place in a legal “gray area.”

- Venture firm Full Tilt Capital LLC was acquired by hedge fund Morgan Creek Capital Management LLC, just two months after announcing that it would be going all-in on cryptocurrencies, reports Bloomberg. Mark Yusko, founder and chief investment officer at Morgan Creek, who has over $1 billion in assets under management, said last week that the company believes “blockchain to be one of the most powerful and valuable technologies to have been developed in the digital age.” As part of the deal, Morgan Creek plans to raise $500 million for a new fund based entirely on blockchain investment opportunities.

- Morgan Stanley analysts issued a report on Monday saying that “the price of bitcoin is worth watching” due to similarities in chart movements of bitcoin and the forward price-to-earnings ratio of the S&P 500 indexes’ stocks, writes Bloomberg. The report also stated that Morgan Stanley does not expect the relationship to continue to be strong, but that the price-to-earnings ratio likely won’t move significantly without a similar move in the bitcoin price.

Threats

- Raphael Bostic, President of the Federal Reserve Bank of Atlanta, told an audience at the Hope Global Forums meeting this week to stay away from cryptocurrency markets since “they are not a currency” and that “if you have money you really need, do not put it in these markets,” reports Bloomberg.

- Longfin Corp. will be removed from the Russell 2000 Index less than two weeks after it joined. The New York-based financial technology company saw its stock rise 2,600 percent after announcing its ties to cryptocurrencies from buying Ziddu.com, a blockchain lending solutions provider. According to Bloomberg Technology, Longfin was removed from the index due to its failure to meet a rule requiring that at least 5 percent of its shares be available to the public.

- According to popular job posting website Indeed.com, interest in cryptocurrency-related jobs has declined in parallel with a fall in cryptocurrency prices. The report released from Indeed on Wednesday shows that crypto-related searches on the site peaked at 39 searches per million in December 2017 and that searches have dwindled by 76 percent since then. However, interest in blockchain-related jobs has remained level, with an average volume of 47 searches per million.

Energy and Natural Resources Market

Strengths

- Natural gas was the best performing major commodity this week rising 5.4 percent. The commodity rallied as weather forecasts show Europe is likely to endure a cold April. After the chilliest February in a decade, and the coldest March in six years, forecasters agree that the cold is likely to extend into April.

- The best performing sector this week was the S&P1500 Steel Index. The index rose 3.53 percent as U.S. Commerce Secretary Wilbur Ross reiterated his suggestion to impose tariffs on imported steel, while seeking to calm investors arguing higher tariffs will have a trivial effect on the nation’s rate of inflation.

- The best performing stock for the week was POSCO. The Korean manufacturer of steel products rose 6.44 percent after unveiling a strategic plan to differentiate by developing technologic capabilities ahead of its peers.

Weaknesses

- Iron ore was the worst performing commodity this week. The commodity dropped 7.24 percent as signals from China disappointed. Despite the short-term trade war announcements giving way, economists in China continue to forecast a poor iron ore market as construction demand is unlikely to beat that of 2017.

- The worst performing sector this week was the S&P/TSX Diversified Metals & Mining Index. The index dropped 77 basis points after two sizeable constituents dropped as a result of heightened political risk elements in Africa, which affected each of the constituents individually.

- The worst performing stock for the week was Fortescue Metals Group LTD. The Australian iron ore miner dropped 6.88 percent after iron ore prices softened in China as demand from steel mills disappoints and economists suggest the construction market, which is the key driver of steel demand, may not surpass the levels seen last year.

Opportunities

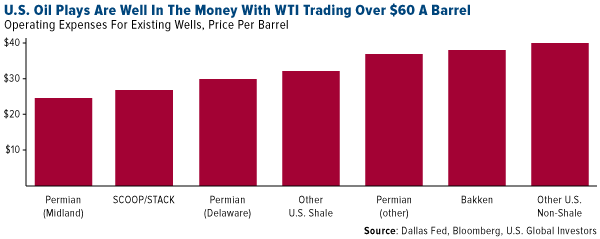

- The shale patch is making money, hiring and ready to drill for more. As Bloomberg reported, the vast majority of shale explorers surveyed for a Federal Reserve Bank of Dallas report said they could profitably drill a new well at current prices. More than half are increasing headcount.

- Renewable energy and battery metals are here to stay. A joint announcement this week by SoftBank and Saudi Arabia reports the Arab nation will spend $200 billion for solar power generation to power millions of homes. In addition, the plan is to store electricity in batteries, thus allowing the plant to supply energy even when the sun isn’t shining. The scale of the project should send major positive shockwaves across the renewable energy and battery metals sectors.

- Gold prices set the best run since 2011 as stars align for bullion investors. Gold is posting a third consecutive quarterly advance amid multi-year highs on physical ETF inventories. According to specialists, the strong physical demand to start the year is being compounded by haven demand as foreign-policy hawks continue to move up the ranks in Washington D.C.

Threats

- Crude oil may be in for a bearish second quarter as weak equity markets and an uncertain trade outlook prompt downward growth revisions amid mounting signs of oversupply. Technical analysts have also pointed out that the chart for WTI is forming a double top, suggesting prices could drop to retest the low $60’s before moving higher.

- Don’t buy the dip in commodities, according to Barclays. The bank’s analysts stated that the outlook for commodities looks even worse as the year progresses, with U.S. shale driving the crude market into another glut and lackluster Chinese demand dragging on metals.

- Zinc prices near peaks with miners set to ramp output, according to ING. ING analysts suggest that higher zinc prices are encouraging a rapid mine response that will reduce tightness in the physical market, and consequently lead to lower prices. The bank suggests more than 400 thousand tonnes of new projects and re-starts will take place in 2018, all of them outside of China, thus increasing the likelihood that prices drop after hitting 10-year highs last month.

China Region

Strengths

- Vietnam’s Ho Chi Minh Stock Index closed up 1.17 percent for the week (through this Thursday). India’s NIFTY 50 and SENSEX Index put in a strong showing for a close second and third, rising 1.16 and 1.14 percent respectively.

- Vietnam put in some solid economic numbers this week as well, with its first quarter GDP number clocking in at a scorching 7.38 percent pace, well ahead of analysts’ estimates for a 5.60 percent print.

- In a week marked by earnings and market volatility, telecommunication was the best-performing sector in the Hang Seng Composite Index, rising by 2.26 percent through Thursday. Hong Kong will be closed in observation of the Good Friday holiday, as will Singapore, the Philippines, India and Indonesia.

Weaknesses

- Thailand’s SET Index declined by 1.50 percent through Thursday in a mixed week for the region, while Singapore’s Straits Times Total Return Index fell by 1.13 percent and Indonesia’s Jakarta Composite by 1.04 percent.

- Information technology was the worst performing sector in the Hang Seng Composite Index this week, dropping by 2.29 percent.

- Hong Kong’s year-over-year exports for the February period missed expectations, coming in up only 1.7 percent, below the 7.0 percent showing analysts expected. Imports also missed, dropping by 3.2 percent, below expectations for 2.3 percent.

Opportunities

- Insurance heavyweight Ping An (2318 HK), China’s largest insurer by market value, is beginning preparations for an initial public offering of its OneConnect financial portal, Bloomberg News reported on Friday. OneConnect, which offers AI-powered services such as risk management to financial firms, could raise as much as $3 billion in an upcoming share sale, which may be as soon as September. Ping An’s most recent earnings report—just last week—also topped all analyst estimates.

- Continuing the IPO theme, Bloomberg also recently reported that Foxconn Industrial Internet Co. (or FII), a unit of Apple’s Taiwanese assembly partner Hon Hai Precision Industry (2317 TT, and perhaps better known as Foxconn), has won approval for a Shanghai initial public offering that could fetch as much as 400 billion yuan by some estimates—on par with Sony Inc.

- North Korea’s Kim Jong Un received a warm and heavily-publicized welcome in an official-in-all-but-name state reception in his trip to China this week. Next up is South Korea, where the leader is now tentatively scheduled to meet with President Moon in late April, before prospective meetings with the United States and the Trump administration in May. It remains difficult to say precisely how everything may turn out—presumably that is at least part of why China’s Xi Jinping cozied up—but any prospect for peace or denuclearization represents at least some sort of an opportunity for the region.

Threats

- Guo Shuqing, China’s top bank regulator, has been named as the Asian nation’s Communist Party Secretary of the People’s Bank of China (PBOC), writes the New York Times. Guo’s new position places him above the newly-appointed PBOC governor Yi Gang, according to a Tweet sent by reporter Keith Bradsher, reports Bloomberg News.

- Even as Beijing pinpointed U.S. goods that it could target in a Sino-U.S. trade dispute, reports Bloomberg, China is still warning the U.S. not to unleash trade ills on the world. “The malicious practices of the United States are like opening Pandora’s Box, and there is a danger of triggering a chain reaction that will spread the virus of trade protectionism across the globe,” said a commerce ministry spokesperson on Thursday.

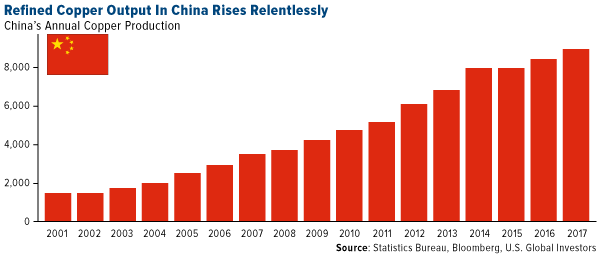

- China—the biggest producer and consumer of refined copper—may need “to eliminate outdated capacity to avoid oversupply as new plants come on stream,” according to Bloomberg News’ citation of an executive at one of the country’s top smelters. The nation must press on with supply-side reform, the executive continued.

Emerging Europe

Strengths

- The Czech Republic was the best performing country this week, gaining 1.2 percent. Komercni Bank and CEZ contributed the most on the Prague exchange. Komercni will continue to pay out more than 60 percent of its profits while maintaining a capital ratio above its regulatory requirement. CEZ, a utility company, may split its assets in preparation to build a nuclear plant.

- The Turkish lira was the best performing currency this week, gaining 90 basis points against the U.S. dollar. The currency was supported by stronger-than-expected gross domestic product data. Turkey’s economy expanded 7.3 percent in 2017, outpacing China and India, thanks to a surge in spending by both households and the government.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Poland was the worst performing country this week, losing 1.8 percent. Poland’s ruling party, Law & Justice, saw its support drop by more than a quarter to 28 percent, from 40 percent a month earlier, according to the latest opinion poll. Clashes with the EU over democratic standards and unpopular government policies weighed on the party’s popularity.

- The euro was the worst performing currency this week, losing 41 basis points. Inflation for the largest European economy, Germany, came out slightly lower than expected at 1.6 percent versus 1.7 percent. This year, once again, Europe is experiencing growth, but without a pickup in inflation. If eurozone inflation does not move close to the European Central Bank’s (ECB’s) target of 2 percent, there is a greater likelihood that the bank will extend its stimulus, which currently is set to run until September.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

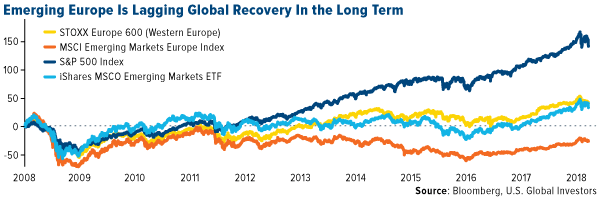

- Emerging Europe stocks are the best performers this year. Year-to-date the MSCI Emerging Europe Index gained 3.5 percent, while U.S. and Western European stocks lost almost 3 percent and global equites lost 50 basis points. According to the long-term chart below, emerging Europe is lagging global markets and has much more room to grow. Despite very good year-to-date performance and good growth last year, emerging European equites should have appreciated more as they did not recover from 2008 losses.

- The French deficit fell below 3 percent of GDP for the first time in a decade last year. It came in a better than expected at 2.6 percent of GDP in 2017, below the government’s 2.9 percent target, and the best reading since the global financial crisis in 2007.

- Bloomberg reports that central banks are expecting to move $500 billion of foreign exchange reserves into euros as rising U.S. protectionism pushes investors away from the dollar. Currently, about 64 percent of global reserves are dominated in dollars, and the euro accounts for 20 percent of reserves, or $1.93 trillion. From 2010 to 2016, the euro lost roughly 30 percent of its value against the U.S. dollar.

Threats

- The U.S. ordered 60 Russian diplomats to leave the country and close Russia’s consulate in Seattle in response to the nerve-agent poisoning of a former Russian spy in Great Britain. Fourteen countries in the eurozone and Canada announced similar orders. Western countries are uniting in a move to punish Russia for its aggression. Vladimir Putin is expected to travel to China in June and strengthen its ties with the East, as the West is pushing him away.

- Euro area economic confidence continued sliding in March. Optimism slipped in the region’s five biggest economies, taking its overall index to the lowest in six months. This is the third drop from a 17-year high in December.

- Romania’s January to February budget shortfall is the widest since 2010, after the government implemented tax cuts and state-salary increases. Public expenses have surged almost 40 percent from a year ago, and the fiscal gap may surpass the European Union’s limit of 3 percent of GDP. Capital Economics’ research team estimates that the budget gap will stand at 3.3 percent of GDP this year, up from 2.4 percent.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits