Seeking an Antidote to Global Trade Jitters? Check Out These Buying Opportunities!

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

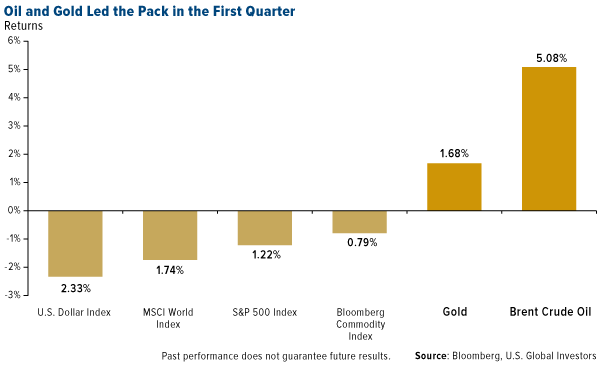

After being mostly absent in 2017, volatility has made a comeback. The S&P 500 Index closed down for the first three months of 2018—the first time it’s done so in 10 quarters. It also had its worst start to April since 1929. Gold performed as expected during the quarter, serving as a safe haven and delivering positive returns, while the price of oil surged more than 5 percent on U.S. dollar weakness and news that OPEC and Russia could be cooperating to limit output for a long period.

Before continuing, I think it’s important for investors to remember that each asset class has its own DNA of volatility. For the 10-year period as of April 4, the 60-day, or quarterly, standard deviation for the S&P 500 was ±8 percent. What this means is that, even though the S&P was down 1.22 percent in the first quarter, the decline was well within its expected range of one standard deviation, which occurs roughly 68 percent of the time.

The same can be said for oil and gold. For the same time period, oil had a standard deviation of about ±20 percent, while gold bullion’s is right in line with the S&P: ±8 percent. That all of these assets stayed within one standard deviation for the 60-day trading period makes their performance a non-event. It’s when they exceed two standard deviations that investors might want to consider a trade, as the asset could be ready to revert back to its mean.

To learn more about standard deviations and other technical issues, download my whitepaper, “Managing Expectation: Anticipate Before You Participate in the Market.”

Look Past the Short-Term Noise

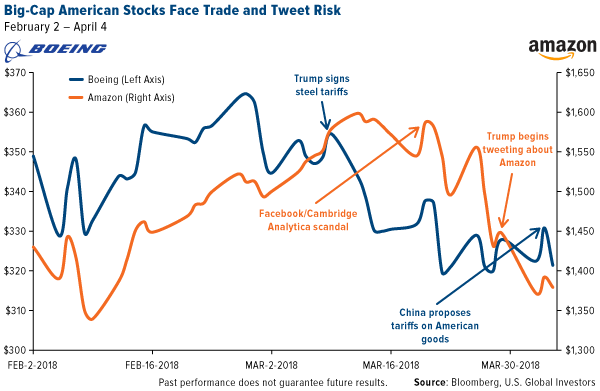

Much of the recent selloff has been related either to fears over a potential trade war with China, the world’s second-largest economy, or expectations that tech stocks—most notably Facebook and Amazon—could face additional regulatory scrutiny.

Although U.S. tariffs on Chinese imports, and China’s proposed taxes on American goods, have not been imposed yet, markets are already beginning to price in the news. Shares of Boeing, the largest U.S. exporter by value, have dropped more than 8 percent since its high on February 27, following announced U.S. tariffs on imported steel and aluminum and China’s plan to levy as much as 25 percent on American-made aircraft. Aircrafts, by the way, are hands-down the United States’ most valuable export, followed by gasoline.

Meanwhile, Trump’s criticism of Amazon’s shipping deal with the U.S. Postal Service, not to mention the media’s negative coverage of Facebook’s relationship with British political consulting firm Cambridge Analytica, weighed especially hard on tech stocks.

(This is nothing new, though. To educate investors on how quants comb through social media and use sentiment analysis to make their trades, I like to show this video featuring the Trump and Dump Bot, which you can watch here.)

To be clear, I believe this is all short-term noise—even after Trump suggested adding tariffs on an additional $100 billion of Chinese goods this morning to combat the effects of alleged intellectual property theft. A trade war could be a concern sometime down the road, but I’m confident U.S. and Chinese officials can work together to avert a full-blown tit-for-tat standoff. And it’s possible Trump’s Amazon tweets are nothing more than personal jabs against founder and CEO Jeff Bezos.

But if these risks are too great at the moment, an attractive place to be could be in domestic-focused, small- and mid-cap stocks, which have limited exposure to international trade compared to their large-cap siblings. They therefore could see little impact from any imposed tariffs.

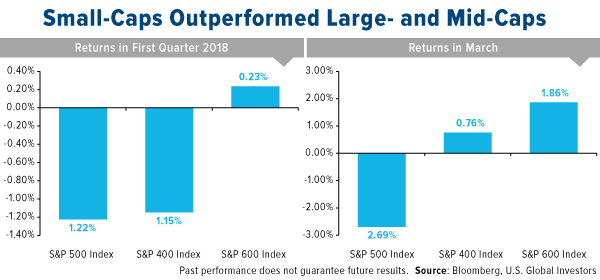

Small-Cap Stocks, Big-League Growth

For the first quarter of 2018 and for the month of March, small-cap domestic stocks, as measured by the S&P 600 Index, ended with a positive gain. The S&P 400 Index, composed of mid-cap stocks, did slightly less better in March and gave up more than 1 percent in the first quarter.

Both groups fared better than the 500 largest U.S. companies, which were hit by international trade jitters. S&P 500 firms, after all, derive about half of their profits from overseas markets.

If you recall, small-caps skyrocketed in the days immediately following the 2016 presidential election as investors anticipated the implementation of “America first” policies—deep corporate tax cuts, deregulation, tariffs on imported goods—that would greatly favor inward-facing companies.

Investors are making a similar bet today.

That’s not to say investors should rotate completely out of blue-chip stocks. Earnings per share (EPS) for S&P 500 companies are expected to come in very strong in the first quarter, according to FactSet data. However, it might be prudent to consider increasing your exposure to smaller firms with less dependence on trade with China and other countries.

Consider what small business owners themselves are saying. The most recent monthly Index of Small Business Optimism, conducted by the National Federation of Independent Business (NFIB), came in at 107.6, the second-highest reading in the survey’s 45-year history. And 32 percent of small business owners say now is a good time to expand, the highest percentage ever. This prompted NFIB economists William Dunkelberg and Holly Wade to write: “After years of small businesses sitting on the sidelines and not benefiting from the so-called recovery, Main Street is again on fire.”

Hedge Funds Are Jumping Back into Gold—What About You?

At the same time, there are some early warning signs of potential economic turbulence on the horizon. I would highly urge investors to ensure a portion of their portfolio is in a historically reliable store of value—investment-grade municipal bonds, for instance, and gold bullion and gold mining stocks.

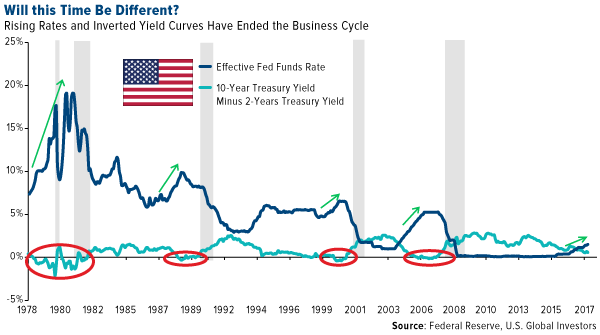

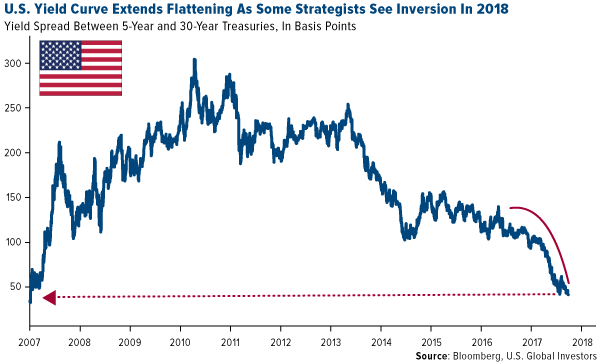

One of the indicators some economists have their eye on right now is what’s known as the flattening yield curve—or the difference between long-term and short-term Treasury yields. When the latter exceeds the former, the yield curve is said to invert, and in the past this has often preceded an economic slowdown.

Recently, the difference between the 10-year and two-year T-note dropped below 50 basis points for the first time since October 2007. And with interest rates expected to be hiked three or four times this year, the yield curve could very well flatten even further.

It could be for this reason, among others, that we’ve seen a huge jump in hedge funds betting on gold. According to Kitco News, citing Commodity Futures Trading Commission (CFTC) data, money managers increased their speculative long positions in gold futures by 34,928 contracts to a total of 183,080 for the week ended March 27. This represents the most significant jump in bullish sentiment in two years.

Investors’ attention is “back on gold,” George Gero, managing director with RBC Wealth Management, told Kitco. He added: “The gold market has solid geopolitical underpinnings.”

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.71 percent. The S&P 500 Stock Index fell 1.38 percent, while the Nasdaq Composite fell 2.10 percent. The Russell 2000 small capitalization index lost 1.05 percent this week.

- The Hang Seng Composite lost 0.34 percent this week; while Taiwan was down 0.22 percent and the KOSPI fell 0.28 percent.

- The 10-year Treasury bond yield rose 3.4 basis points to 2.774 percent.

Domestic Equity Market

Strengths

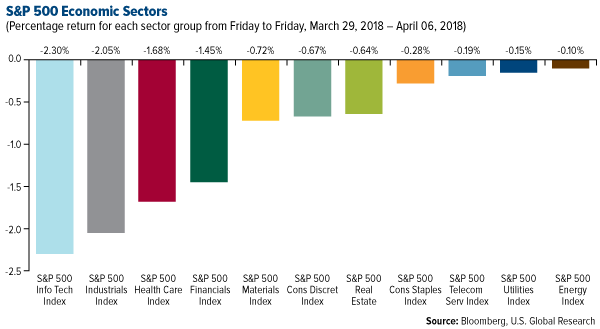

- Energy was the best performing sector of the week, giving back only 0.10 percent, compared to an overall drop of 1.46 percent for the S&P 500 Index.

- Baker Hughes was the best performing stock for the week, increasing 6.52 percent.

- Home-builder Lennar’s stock jumped after beating Wall Street expectations Wednesday by reporting better-than-expected first quarter profits and revenues after selling more homes at higher prices and gaining a boost from its purchase of onetime rival CalAtlantic.

Weaknesses

- Information technology was the worst performing sector for the week, falling 2.30 percent versus an overall drop of 1.46 percent for the S&P 500 Index.

- Incyte was the worst performing stock for the week, falling 23.17 percent.

- Shares of Incyte plunged on Friday after the company said an external data monitoring committee (eDMC) determined that results from a phase 3 study evaluating Incyte's epacadostat with Merck's Keytruda in patients with metastatic melanoma did not meet the primary endpoint of improving progression-free survival.

Opportunities

- Pharmaceutical stocks are trading at one of their largest discounts to the market in nearly 10 years, J.P. Morgan told clients Monday. "This underperformance reflects ongoing drug pricing concerns, many of which are either well reflected in estimates or unlikely to come to fruition for the foreseeable future," analyst Chris Schott wrote. "We see an attractive opportunity to revisit an admittedly out-of-favor sector with a mix of new launch driven sales/earnings upside and capital deployment/M&A representing potential catalysts for the space."

- Economies around the world are the most synchronized in years, but Bernstein argues they'll start diverging soon. The firm offers a two-part recommendation for best handling this fissure in global economic growth. First, go long growth factor stocks. This will capture assets that will deliver outsized growth, something many Wall Street firms track using the Sharpe ratio, which measures relative returns. Second, offset slowing growth with counter-cyclical low-leverage stocks, while also gaining exposure to stocks with high free cash flow.

- Morgan Stanley says the rocky stock market could be rescued by the record $400 billion of dividend payments that will boost investor cash holdings during the period from March through May.

Threats

- President Donald Trump says he is taking a serious look at policy options on Amazon. While speaking with reporters on a trip back to Washington, Trump said that Amazon was not operating on a level playing field and that the "sales-tax situation" would be examined soon by the Supreme Court, Reuters reports. Additionally, Trump might ask the U.S. Postal Service to renegotiate the shipping fees it charges Amazon as part of his wider campaign against the firm. White House advisers also think the president should cancel the Pentagon's cloud contract deal with Amazon.

- Barclays was downgraded at Moody's. The rating agency lowered Barclays' credit rating one notch to Baa3, or just one step above junk, Bloomberg says.

- China's tariffs are negative for Tesla given that about 17 percent of Tesla's 2017 revenue came from China. Charlie Chesbrough, a senior economist at Cox Automotive, says the country's newly announced 25 percent tariff on automobiles made in the U.S. are “certainly going to slow down sales.”

The Economy and Bond Market

Strengths

- The nation's unemployment rate remained at a 17-year low of 4.1 percent for the sixth straight month, the Labor Department said Friday.

- Average hourly earnings rose 0.3 percent from the prior month, in line with estimates.

- The New York Fed’s GDP Nowcast model now sees U.S. first quarter GDP at 2.77 percent, compared to 2.71 percent in the prior week. The model sees quarter two growth of 2.91 percent.

Weaknesses

- Payrolls rose 103,000, compared with the median estimate of economists for 185,000, Labor Department figures showed Friday.

- America's trade deficit widened in February as its international trade hit a monthly record. The deficit was $57.6 billion, the largest monthly gap between exports and imports of goods and services since 2008, the US Commerce Department said.

- The Institute for Supply Management (ISM) said its index of national factory activity fell to a reading of 59.3 last month, down from 60.8 in February.

Opportunities

- Moody’s says it expects the U.S and China to avoid a "severe escalation of trade restrictions" given the detrimental impact added ones would have on both economies. The macro-economic impact of the measures that have actually been implemented so far is likely to be limited to a small short-term effect on growth and inflation.

- President Trump said the U.S. may reach a deal soon on a revamped NAFTA while playing down expectations the announcement will come next week at a regional summit in Peru. "We’re working very hard on NAFTA with Mexico and Canada. We’ll have something, I think, fairly soon,” Trump said at an event in West Virginia.

- Atlanta Fed President Raphael Bostic sees a buoyant U.S. economy lifting inflation to the central bank’s 2 percent target "sometime in the next quarter or two" but said he doesn’t think this should prompt the central bank to choke off the expansion. "I am actually very comfortable going above the 2 percent by some amount — 2.2, 2.3 — I don’t think that is a crisis of overheating," he told Bloomberg TV. "I think it is also important that we take a stance so that everyone understands that the 2 percent level is an average, not a ceiling."

Threats

- As the second quarter begins, the Treasuries yield curve from 5 to 30 years is at its flattest in more than a decade, with the spread falling below 40 basis points on Monday. Some Wall Street strategists have forecast that the curve will invert in 2018. Ian Lyngen and Aaron Kohli at BMO Capital Markets, among those who have predicted such a move, said in a note Monday that traders should next watch for the curve from 2 to 10 years—currently around 47 basis points—to also get to 40 basis points by mid-April. A yield curve inversion has historically preceded recessions.

- Trump floated the possibility of tariffs on an additional $100 billion in Chinese goods. A White House statement released Thursday said that in response to China's threat of retaliatory tariffs, President Donald Trump had instructed the U.S. trade representative to consider additional tariffs on Chinese goods.

- The 'synchronized global economic recovery' is showing signs of slowing. The JPMorgan-IHS Markit Global All-Industry Output Index fell to 53.3 in March, making for its lowest level in 16 months.

Gold Market

This week spot gold closed at $1,333.01, up $7.47 per ounce, or 0.56 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.62 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index came in down 3.45 percent. The U.S. Trade-Weighted Dollar was down 0.03 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Apr-01 | CH Caixin China PMI Mfg | 51.7 | 51 | 51.6 |

| Apr-02 | US ISM Manufacturing | 59.6 | 59.3 | 60.8 |

| Apr-04 | EC CPI Core YoY | 1.10% | 1.00% | 1.00% |

| Apr-04 | US ADP Employment Change | 210k | 241k | 235k |

| Apr-04 | US Durable Goods Orders | --- | 3.00% | 3.10% |

| Apr-05 | US Initial Jobless Claims | 225k | 242k | 215k |

| Apr-06 | US Change in Nonfarm Payrolls | 185k | 103k | 313k |

| Apr-10 | US PPI Final Demand YoY | 2.90% | -- | 2.80% |

| Apr-11 | US CPI YoY | 2.30% | -- | 2.20% |

| Apr-12 | US Initial Jobless Claims | 230k | -- | 242k |

| Apr-13 | GE CPI YoY | 1.60% | -- | 1.60% |

Strengths

- The best performing metal this week was gold, up 0.62 percent. Gold posted its third quarterly gain last quarter, for the longest run since 2011, according to Bloomberg. The weekly Bloomberg survey of trader sentiment showed that most gold traders were neutral this week, while last week they were bearish on the yellow metal. The Perth Mint released sales figures showing gold coin and bar sales were up in March at 29,883 ounces, versus 26,473 ounces in February. Exchange-traded funds backed by gold saw $58.1 million in inflows this week bringing total assets to $97.5 billion.

- The potential trade war and tensions escalating this week proved to be positive for gold as a safe haven asset. Kirill Chuyko, head of research at BCS Global Markets in Moscow, said this week that, “Gold is advancing on the risk of trade wars, in particular between the U.S. and China, which increases the metal’s appeal as a safe haven.” George Gero, a managing director at RBC Wealth Management, indicated that gold is on the rise to hit $1,400 an ounce and that investors are “buying back hedges” due to fear of trade wars. The gold price rose earlier today to $1330.78 per ounce after President Donald Trump proposed $100 billion in additional tariffs on China.

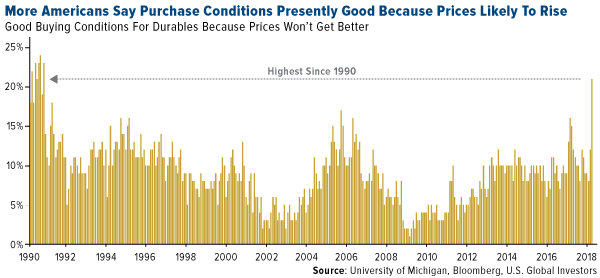

- In a survey of consumer sentiment, 21 percent of American consumers are convinced that now is the time to make large purchases, rather than later, because discounts and deals won’t be around for much longer, reports Bloomberg. This is the highest percent of consumers positive in 27 years and indicates that fear of inflation is on the rise.

Weaknesses

- The worst performing metal this week was palladium, down 5.1 percent. Metals producers fell on Wednesday on fears of a trade war, but then rebounded later in the week. The BullionVault Gold Investor Index fell overall in March to 53.7, compared to 54.1 in February.

- Randgold Resources Ltd., known for its ability to operate successfully in Africa, is now one of the worst performing gold miners in the industry with its stock falling 20 percent this year, according to Bloomberg. Other gold producers fell in the first quarter with 10 of the top 14 gold producers down so far in 2018. Even as gold gained, the BlackRock Gold and General Fund, one of the largest gold funds, lost 15 percent last quarter due to the underperformance of royalty companies.

- Reuters reports that sales in March of U.S. Mint American Eagle gold fell and sales of silver coins fell to their lowest levels in 11 years. Sales of gold coins amounted to 3,500 ounces, down 36.3 percent from the prior month.

Opportunities

- Chakana Copper Corp. announced positive drill results from its copper-gold-silver Soledad project in Peru this week. The report indicates four new drill holes with one hole showing a high-grade margin zone with 19.4m of 2.7 percent copper, 14.36 g/t of gold and 26 g/t of silver. Positive news came this week for South African mining companies after they won a ruling that producers won’t need to top up black-shareholding levels if they previously met the minimum 26 percent requirement, reports Bloomberg. The judgement should boost certainty and confidence for investors in one of the top mineral-producing nations.

- Bloomberg Intelligence analyst Mike McGlone writes that an industrial metals and gold rally is increasingly favorable. McGlone says that the stock bull market is slowly retiring and, in combination with the Fed’s March interest rate hike, gold should see the next stage of its recovery. Commodities overall may be on the rise due to diminishing dollar returns and the increased pace of rate hikes weakening the dollar.

- According to Sprott’s CEO Rick Rule, gold is on its way to $1,400 an ounce due to trade war risk. Bloomberg writes that the trade war could hinder demand for U.S. assets and the dollar could be vulnerable if international buyers turn away from American debt. Other signs that gold could move much higher is the oil to gold ratio. One ounce of gold now buys 21 barrels of oil compared with the 25.4 barrel two-year average, according to Bloomberg. Crude oil is around $64 currently and if the gold-to-crude ratio reverts back the mean, bullion would trade in the $1,600 an ounce range.

Threats

- Manhattan home sales continue to fall for the second quarter in a row with sales of all condos and co-ops falling 25 percent last quarter. Homeownership expenses are rising due to increased borrowing costs and federal limits on tax deductions for mortgage interest, writes Bloomberg News. Around 52 percent of all sales last quarter were for less than the asking price.

- Overall the first quarter of this year was negative for U.S. markets as debt continues to rises significantly compared to gross domestic product (GDP) growth. According to Jim Paulsen, chief investment strategist at Leuthold Weeden Capital Management, investors should proceed with caution in all asset classes as signs of stress have emerged. Since investors are positioning themselves defensively into safe haven assets, gold has started to outperform copper, driven by fear in the reports, writes Bloomberg.

- Zimbabwe, with the world’s second largest platinum reserves, released a Mines and Mineral Bill on Thursday citing that no mining right or title will be granted to a public company unless at least 85 percent of the company’s shares are listed on the local exchange. The nation’s effort to hold mining companies more accountable is meant to spur economic growth and exports. Jee-A van de Linde, an analyst at NKC African Economics said “to compel firms to list a majority of their shares on the Zimbabwe’s stock market may not necessarily yield the desire results, and may end up creating more uncertainty – especially for foreign investors.”

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended April 6 was Antimatter, which gained 777.08 percent.

- A subsidiary of Foxconn, one of the world’s largest electronics manufacturers that produces products such as iPhone and Kindles, will help develop and produce a new blockchain phone from startup Sirin Labs, reports Bloomberg. The phone, called the Finney, seeks to integrate all kinds of digital tokens and allow owners to shop on cryptocurrency friendly websites and convert cash into tokens.

- Health insurance rivals UnitedHealth and Humana announced their intent to pursue a blockchain pilot in cooperation with MultiPlan and Quest Diagnostics. “The pilot will examine how sharing data across health care organizations on blockchain technology can improve data accuracy, streamline administration and improve access to care,” said the involved companies’ statement. Data reconciliation is a major pain point within the healthcare industry, costing an estimated $2.1 billion annually according to according to Coindesk.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended April 6 was FirstCoin, which lost 31.86 percent.

- Blockchain program lead Amber Baldet is leaving JPMorgan Chase & Co. to pursue her own venture. “Amber is extremely talented and helped build the outstanding team we have today,” said a JPMorgan spokesperson to Reuters. Banks like JPMorgan are exploring blockchain technology to streamline and reduce the cost of digital transactions, such as security settlements and payment processing.

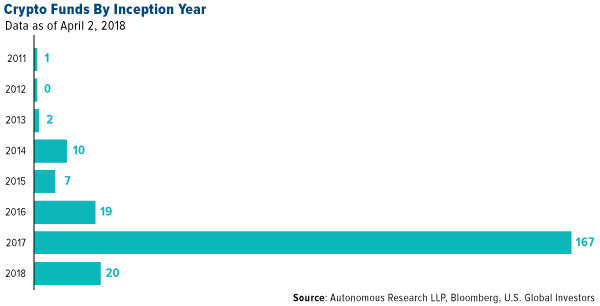

- During the first three months of 2018, at least nine cryptocurrency hedge funds were shuttered, reports Bloomberg. The 50 percent plunge in the value of bitcoin has many investors thinking twice, the article continues. Even more well established funds have been hit. “New capital has slowed, even for a higher profile fund like ours,” said Kyle Samani of Multicoin Capital.

Opportunities

- Members of the tech industry are increasingly looking at blockchain as a solution to recent negative headlines, ranging from data breaches at Equifax to improper data collection with Cambridge Analytics. “Everything is moving toward people saying, ‘I want all the benefits of the internet, but I want to protect my privacy and my security,” says Bradley Tusk, founder of Tusk Strategies. “The only thing I know that can reconcile those things is the blockchain.” Venture capitalists have invested half a billion dollars in 75 blockchain projects during the first three months of 2018.

- Founding Director of the Bitcoin Foundation Jon Matonis told Business Insider this week that he believes that bitcoin is not a bubble. Rather, “[t]he bubble is the insane bond markets and the fake equity markets that are propped up by the central banks.” Despite this view, Matonis is enthusiastic about big banks like Goldman Sachs potentially entering the crypto world as they would add new liquidity and reduce volatility.

- Bitman, a bitcoin mining hardware firm, announced its application-specific integrated circuit (ASIC) for Ethereum mining on Monday. It is preparing its supply chain for shipments of the new product in the second quarter of 2018.

Threats

- Researchers from ETH Zurich University suggest that bitcoin’s value is based on the network of people using it and that the currency may be overvalued. Based on current support levels for the cryptocurrency, these analysts think the Bitcoin market is “in the range of $22–$44 billion, at least four times less than the current level.”

- The U.S. Internal Revenue Service treats taxation of bitcoin transactions the same regardless of size, resulting in taxpayers needing to calculate capital gains taxes for every single purchase they made. By requiring bitcoin users to report every miniscule transaction, the IRS could unintentionally encourage Americans not to report portions of their taxes or to use unregulated foreign cryptocurrency exchanges. Executive Director of Coin Center Jerry Brito suggests that a de minimus exemption for cryptocurrency gains under $200 could resolve this issue.

- Cryptocurrency volatility has captured the Federal Reserve’s attention, according to Federal Reserve Governor Lael Brainard. In her remarks to New York University’s Stern School of Business this week, Brainard said cryptocurrencies are a highly speculative market and that “individual investors should be careful to understand the possible pitfalls of these investments and the potential for losses.”

Energy and Natural Resources Market

Strengths

- Iron ore was the best performing major commodity this week rising 5.5 percent. The commodity rallied after Anglo American PLC said on Tuesday it would halt production and transportation of iron ore for 90 days from its Minas-Rio mine in Brazil to inspect a pipeline that has leaked twice.

- The best performing sector this week was the BI Global Integrated Oils Valuation Peers Index. The index rose 3.1 percent as energy investors replaced riskier E&P exposure with more stable integrated oil names amid a surprise slide in crude oil prices.

- The best performing stock for the week was Daqo New Energy Corp. The Chinese manufacturer of photovoltaic products rose 14.1 percent after announcing that it has signed a major supply agreement with LONGi Green Energy Technology Co., Ltd., the world's leading mono-crystalline solar products manufacturer.

Weaknesses

- Crude oil was the worst performing commodity this week. The commodity dropped 4.6 percent as shale explorers boosted drilling activity in the U.S. oil patch to the highest in three years, even after American crude output touched unprecedented levels. The data suggests that U.S. crude production may continue its vertiginous rally, leading investors to fear a return to an oversupplied global market.

- The worst performing sector this week was the S&P1500 Oil & Gas Exploration & Production Index. The index dropped 2.4 percent following crude oil’s largest weekly drop since February.

- The worst performing stock for the week was Ferrexpo PLC. The iron ore miner dropped 10.4 percent after announcing its first quarter iron ore pellet production dropped 7.4 percent from the previous quarter.

Opportunities

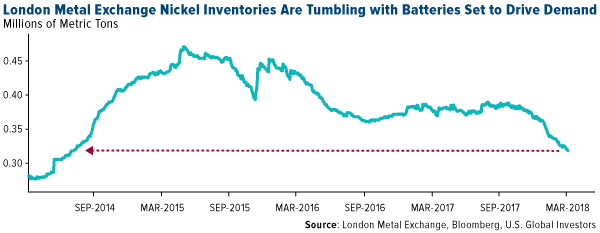

- Nickel stockpiles slumped to their lowest levels in more than three years as the industry bets on battery usage. The mass roll-out of electric vehicles may still be years away, but there are signs the nickel industry is already preparing for surging usage of the metal in car batteries. Nickel inventories on the London Metal Exchange have tumbled to their lowest level since 2014, in what Macquarie Bank Ltd. analysts say could be evidence of stocking up in the battery-making supply chain.

- The gold-to-oil ratio signals the yellow metal could be poised to rise. If history is a guide, either gold is set to rally or oil is poised for a correction, according to Bloomberg Intelligence. One ounce of gold now buys about 21 barrels of oil compared with the 25.4 two-year average. With WTI crude around $64 a barrel, if gold-to-crude reverts to the mean in this rate-hike cycle, bullion would trade near $1,600 an ounce, according to strategist Mike McGlone.

- Russia says it's open to a long-term formal alliance with OPEC. The alliance between OPEC and Russia that coordinated historic oil-output cuts could last "indefinitely" and be formalized by setting up a new organization. The involvement of Russia, the world’s largest energy producer, was a crucial factor in the effectiveness of the production cuts, which removed a large part of a global stockpile surplus and ended a three-year price rout.

Threats

- Global manufacturing activity is showing signs of fatigue after nearly two years of surging growth. Manufacturing activity slowed in 19 out of the 28 economies tracked by JP Morgan and Markit in March, particularly in the European region. The synchronized manufacturing advance of the past two years provided a strong tailwind for resources and commodity demand.

- Trade war fears were heightened this week as China unveiled retaliatory duties on U.S. food imports. The tariffs covering imports of U.S. agricultural products were enacted as a response to the Trump administration’s new tariffs on steel and aluminum imports.

- Construction demand in China may slow as the Asian nation is set to enact new property tax measures to curb house speculation. After years of delay and quiet opposition, China will push ahead with a property tax that is viewed as crucial to taming the country’s housing bubble. President Xi Jinping’s declaration that “houses are for living in, not for speculation” has strengthened the momentum for the introduction of the new tax.

China Region

Strengths

- Hong Kong’s year-over-year retail sales for February rose 29.8 percent, well ahead of analysts’ estimates for a gain of 8 percent.

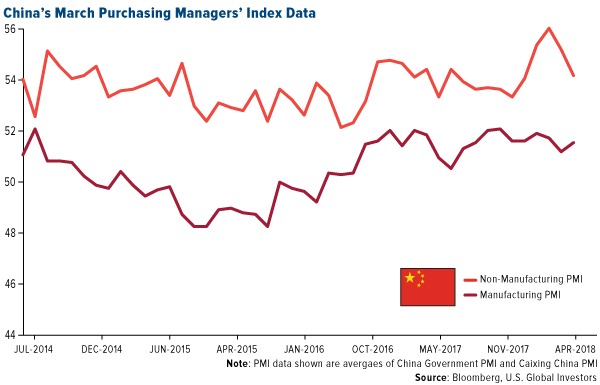

- China’s official Non-Manufacturing PMI came in steady at 54.1, in line with analysts’ estimates but up from the prior showing of 54.4. The official Manufacturing PMI was a solid beat, though, coming in at 51.5, well ahead of estimates for a 50.6 print.

- Macau’s March casino revenue rose more than expected, Bloomberg reports, citing Maca’s Gaming Inspection and Coordination Bureau. Analysts anticipated a roughly 17 percent year over year rise; actual revenue came in at a 22.2 percent growth rate.

Weaknesses

- The Caixin China numbers missed estimates. The Manufacturing PMI print at only 51.0, shy of expectations for a 51.7 showing and down from last month’s 51.6. The Services number, which came in later in the week, clocked in at only 52.3.

- The Nikkei Indonesia Manufacturing PMI for the March measurement period dropped to 50.7, down from 51.4 in February. The Nikkei Malaysia PMI also dropped, falling to a contractionary 49.5 print, down from the prior showing of 49.9. The Nikkei Vietnam Manufacturing PMI also declined, falling to 51.6 from February’s measurement of 53.5, while the Nikkei Taiwan Manufacturing PMI also dropped—albeit a small amount and from a solid position—to 55.3 from last month’s 56.0. The Nikkei South Korea Manufacturing PMI came in at 49.1, falling below last month’s 50.3 reading and dropping into a contractionary reading.

- Thailand’s year-over-year exports and imports both missed in the most recent (February) measurement period. Exports clocked in at a growth rate of only 7.7 percent, well below estimates for a 16.7 percent, while imports rose 21.8 percent, below estimates for 22.5 percent.

Opportunities

- Geely Automobile put in a strong showing for its first quarter sales numbers, rising 39 percent for the January through March period versus the same period last year. The company also noted that the sales volume of its new Lynk & Co. model 01 was 8,507 for March.

- China recently “took a major step toward seeing Alibaba Group Holding Ltd., Baidu Inc. and others list in its domestic market,” Bloomberg News reported over the weekend, after China’s State Council “announc[ed] a trial program that would allow the technology giants to see their shares bought and sold in the world’s most populous country.” The Chinese Depositary Receipt (CDR) program does not yet have a firm start date, but the prospect of at least a secondary listing may be supportive for Chinese tech companies.

- On a similar note, HKEX (the Hong Kong stock market operator) announced that it may expand its reforms to permit the listings of technology companies with more flexible structures, like the dual-class shareholding structure favored by many tech firms. There is also a possibility that HKEX may allow the listing of biotechnology firms without revenue. HKEX is expected to launch reforms later this month, reports the South China Morning Post.

Threats

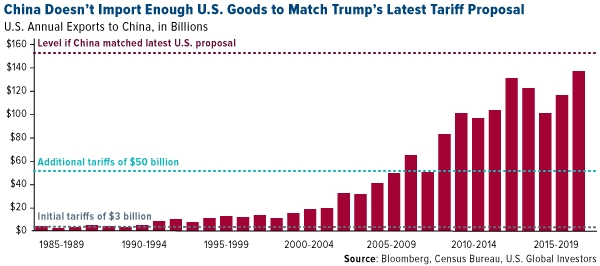

- Tariffs and counter-tariffs remain atop investors’ minds this week, after the United States announced $50 billion in tariffs on China that was matched by $50 billion in retaliatory tariffs from China on various goods from the United States, including soybeans, automobiles, chemicals and aircraft. The United States responded through the issuance of even more tariffs, totaling an additional $100 billion on China. As of the time of writing, China had issued a statement promising to counter U.S. protectionism “to the end, at any cost” but had not issued any additional retaliation. Indeed, China does not import enough goods from the United States to match the American tariffs dollar for dollar, so it remains to be seen precisely what steps might next be taken. It remains important to stress that much of the rhetoric of late may well be posturing ahead of the negotiations that both sides seem to expect to have; perhaps all this is merely “the art of the deal,” so to speak. Bear in mind that Chinese exports to the United States only account for about 4 percent of China’s GDP, according to a recent note from Credit Suisse.

- South Korea also raised the possibility of retaliatory tariffs this week, though this seems moderately unlikely.

- In the midst of the latest media focus on the possibility of a trade war, the upcoming North Korea summits with South Korea (this month) and the United States (next month) could potentially force North Korea back to the top of investors’ minds, though it seems more likely that both major meetings will be spun positively.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 2.6 percent. Banks recorded big gains on the Athens stock exchange and Greek banks stressed that test results should be announced on May 5 while the fourth bailout review should be finished by June 21.

- The Polish zloty was the best relative performing currency this week, losing five basis points against the dollar. Next week central banks will meet and most analysts expect the key rate to stay unchanged at 1.5 percent. This week inflation surprised to the downside, reported at 1.3 percent versus the expectation of 1.7 percent and below the central bank’s target.

- The information technology sector was the best performing sector among eastern European markets this week.

Weaknesses

- The Czech Republic was the worst performing country this week, losing 1.8 percent. Central European Media was the worst performing equity on the Prague Stock Exchange, losing more than 3 percent.

- The Turkish lira was the worst performing currency this week, losing 2.3 percent. Rumors swirled in the market that the prime minister resigned and weaker economic data pushed the lira to a record low against the dollar. The Central Bank of Turkey is meeting on April 25 with most analysts predicting no change in rates.

- The industrial sector was the worst performing sector among eastern European markets this week.

Opportunities

- Hungarian parliamentary elections are scheduled for Sunday and could be a non-event for the local economy. Most economists predict Prime Minister Victor Orban to win the majority of seats, which should lead to the continuation of current polices. Growth numbers have been good for the past couple years, and if the current government stays in power, it should continue.

- Kostas Tsigkourakos from Wood & Company recommends overweighting Greece during the European Union (EU) slowdown. Greece has a low correlation with the EU and global growth, therefore during market corrections it could be a good place to hide. From the EU perspective, Greece has the lowest downside (assuming bank stress test results are positive) and may have the highest upside, Kostas wrote in his daily commentary.

- Russian Energy Minister Alexander Novak said that Russia is open to a long-term formal alliance with the Organization of Petroleum Exporting Countries (OPEC). The production limits agreed on by OPEC, Russi, and allies including Mexico and Kazakhstan have relieved global supply and supported the price of oil. In simpler terms, higher oil prices should benefit Russia, as most revenue Russia generates is from the sale of oil and gas.

Threats

- A global trade war may spread to Europe, as Trump’s tariffs on Chinese imports may be just the beginning in imposing protectionist measures from other major trade partners. A trade war with the EU may come eventually as the eurozone generates one of the largest trade surpluses with the United States. Aside from Germany, the Czech Republic, Hungary and Slovenia are the most open in the world and could be negatively exposed to trade wars, according to Dan Bucsa, CEE chief economist at Unaccredited Bank.

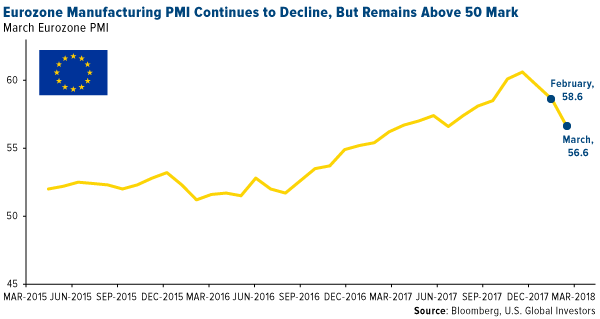

- The global manufacturing PMI fell from 54.2 to 53.4 in March, and the Eurozone PMI has declined the most this year among major economies. According to Capital Economics, a decline in the euro area PMI was mostly due to a stronger euro and weaker domestic demand. Per the chart below, it looks like the PMI peaked in December, but still remains at a high level, well above the 50 mark that separates growth from contraction.

- Dutch lawyer, Alex van der Zwann, tied to former deputy campaign Chairman Rick Gates, was sentenced to 30 days in prison and ordered to pay a $20,000 fine for lying to special counsel Robert Mueller’s team. He was the first person sentenced in Mueller’s investigation into Russian interference in the 2016 U.S. elections. New sanctions were imposed on Russian oligarchs and companies.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All