Entering 2018, our outlook was uniformly upbeat. Fiscal stimulus in the United States, heightened momentum in Europe and sustained expansion in China provided a strong foundation for global growth. The numeric forecast presented here differs little from our edition of three months ago. But risks in the environment have increased.

Trade frictions are escalating on three key fronts. China and the United States have announced new tariffs against one another; the initial volleys were strategically designed, but modestly scaled. Escalation may precede negotiation.

We are less than a year from Brexit. Both sides would like to show strength while preserving productive commerce. Even if negotiations with the European Union can be successfully completed, the United Kingdom still faces the challenge of negotiating a large number of trade pacts with other parts of the world. Time is short, and the degree of difficulty is high.

And the North American Free Trade Agreement is being renegotiated amid heightened rhetoric and the approach of Mexican and American elections.

Tax reductions and spending increases approved by the U.S. Congress will provide considerable short-term stimulus. But long-run debt sustainability has become an issue. Global interest rates are rising, making leverage a little less comfortable; the U.S. (among other nations) will be challenged to keep borrowing costs under control.

Uncertainty around these situations may give pause to consumers and businesses, which won’t be helpful to economic performance. The renewed volatility in financial markets reflects this. Worst-case outcomes are by no means assured: policy makers still have opportunities to keep the global expansion on track. But achieving ideal results will require renewed dedication to productive, bilateral consultation.

United States: Eyes on the Horizon

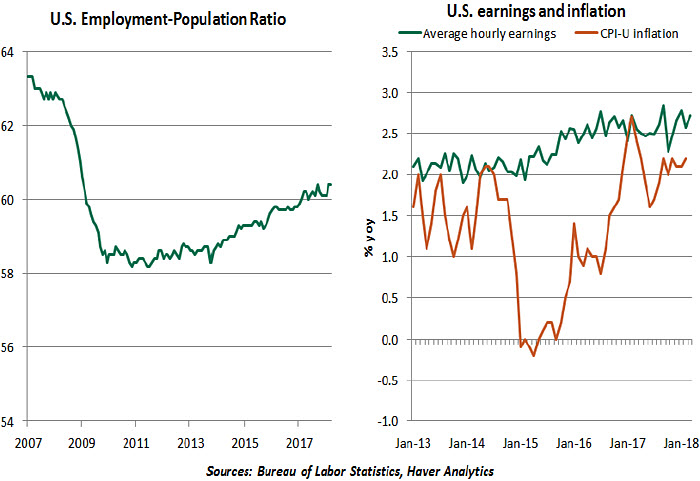

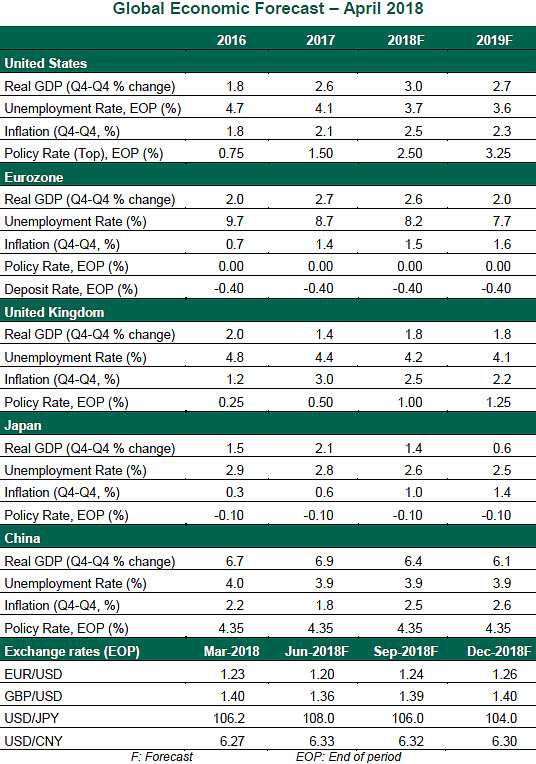

The recovery cycle in the U.S. continues, but against a backdrop of substantial policy shifts. The Tax Cuts and Jobs Act of 2017 is in full effect this year. Employment remains strong, with the employment-to-population ratio improving gradually. More people are rejoining the workforce. Real wages are growing nicely, thanks to modest inflation. All of this should position the American consumer sector to remain vibrant.

We have not yet observed strong effects of tax reform on capital spending, but expanded government spending limits will provide momentum through the remainder of this year and into 2019. Real gross domestic product (GDP) growth is shaping up to be soft in the first quarter, but some of this is expected seasonality; we expect three strong quarters of growth to follow.

Jerome Powell has taken charge as Chair of the Board of Governors of the Federal Reserve. The federal funds rate was increased by a quarter-point in March. In public statements, Powell and his peers have maintained a balanced tone, indicating their willingness to raise rates as long as the economy is performing well. We expect to see three additional rate increases this year.

Eurozone: Clear Sailing

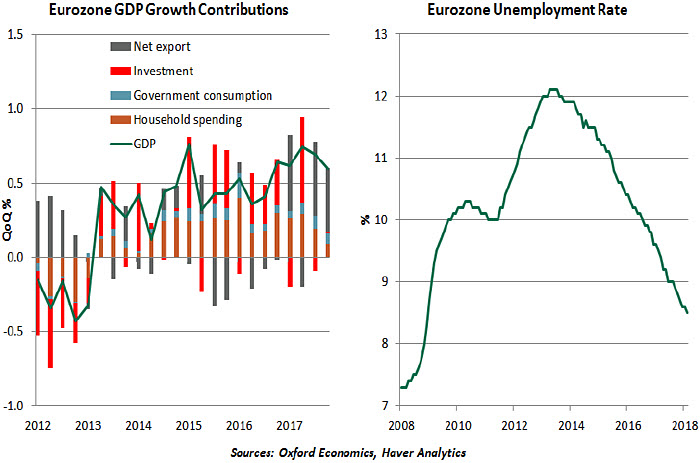

The eurozone economic data released so far in 2018 has included some negative surprises that are pointing to a soft first-quarter performance. In our view, this largely reflects the role of temporary factors (such as bad weather), rather than beginning of a slowdown. As these impediments fade, we expect growth to rebound during the rest of 2018.

Tighter labor markets and subdued inflationary pressures should underpin domestic demand. Strong bank lending to firms and buoyant business surveys are also likely to remain supportive of growth. Real GDP in the common currency region is forecast to grow by 2.6% in 2018 before moderating to 2.0% growth in 2019. Both readings are

well above potential for the eurozone, which should keep the unemployment rate on

a downward trajectory.

Eurozone inflation picked up substantially in 2017, mostly owing to factors relating to energy prices. Higher German wages are a positive step, but other countries need to follow suit to bring inflation closer to the European Central Bank (ECB) target. The ECB seems to be on track to end its asset purchases in the third quarter of 2018, but we do not expect it to raise interest rates through 2019.

Political risks in Europe have declined but not vanished. Italy’s government is unformed, and the eastern part of the European Union is veering rightward. Both situations warrant monitoring.

United Kingdom: No Turning Back

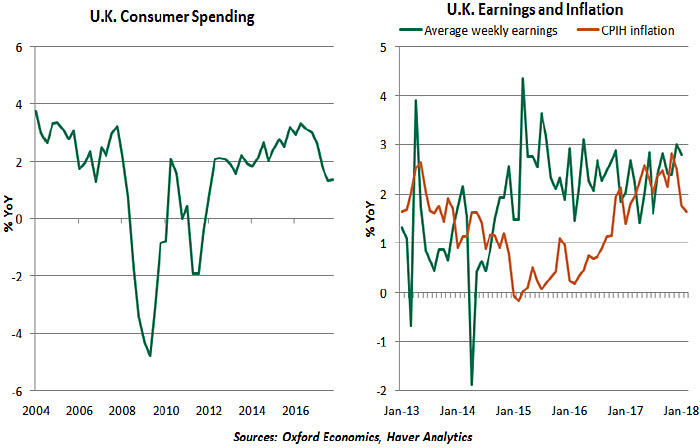

Brexit-related uncertainty has become a familiar theme and will be with us for some time to come. Though progress has been made, there are still reasons for markets to remain cautious. In our baseline scenario, we expect a “soft” Brexit (similar to the relationship between Norway and the EU) that preserves substantial commerce, with the current framework of cooperation maintained in the areas of national security, defense and foreign relations. Even in this optimistic scenario, the long-term gains will be dwarfed by costs for the U.K.

We expect growth to be underpinned by improved household spending, which had been squeezed due to past sterling depreciation that reduced real incomes. The boost from trade owing to the weaker sterling will fade, and Brexit-related uncertainty will continue to weigh on business investments, until more clarity emerges on the future relationship. Overall, the real economy is likely to grow by 1.8% in both 2018 and 2019.

Labor markets should continue to tighten, albeit at a slower pace.

On the monetary policy front, signs of accelerating wage growth, progress on Brexit negotiations and firmer growth should allow the Bank of England to hike overnight interest rates by 25 basis points in May and November of this year, pushing the policy rate to 1.00%. We also assume one hike of 25 basis points after the official Brexit date in 2019 to contain inflationary pressures.

Japan: Focus on Domestic Drivers

Although global recovery supports the Japanese export outlook (U.S. tariffs will have only a minor effect on Japan), it is the stronger yen triggered by flight to safety during risk-off episodes that presents significant downside risks to Japanese exports and the country’s progress on inflation.

We expect Japanese real GDP growth to slow from an expected 1.4% in 2018 to just 0.6% in 2019. Investment is likely to slide as the boost from construction in the run up to the Tokyo Olympics wanes. The planned consumption tax hike (delayed to October 2019) will further weigh on household spending as we move through 2019.

Raising the consumption tax from 8% to 10% will provide a much needed impetus to the price level but won’t be enough to push inflation to the Bank of Japan’s (BoJ) target. We expect inflation to accelerate to 1.0% in 2018 and 1.5% in 2019, with the near-term profile supported by elevated food prices. Against this backdrop, the BoJ is expected to maintain its benchmark policy rate at -0.1% and its yield control target of “around 0%” on 10-year government bond yields.

China: The Balancing Act

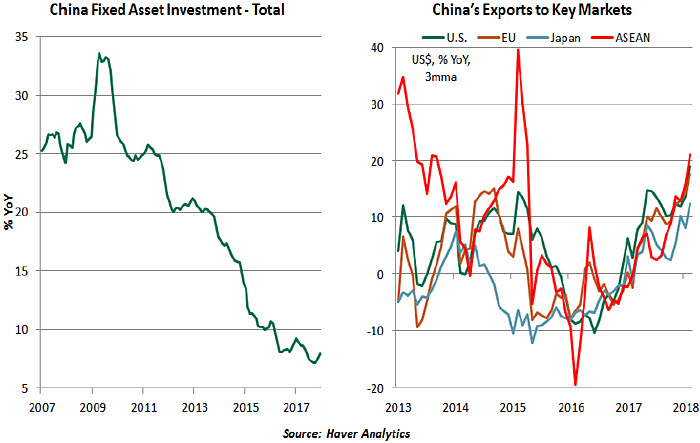

After having recorded a robust performance last year, the Chinese economy seems to have gained further momentum in early 2018, led by export growth and real estate activity. Though off to a positive start, the economy is likely to lose steam in the coming quarters as policymakers’ focus remains on balancing growth with reform and deleveraging. Investments and industrial activity will remain sluggish, thanks to measures aimed at cutting excess capacity. Expect additional tightening of financial regulation and a contractionary fiscal policy.

The favorable trade momentum should also remain supportive of the country’s exports; however, an escalation of trade friction with the U.S. could derail export performance and weigh significantly on Chinese growth. In our baseline scenario, we do not expect the current trade friction to escalate into a full trade war.

Overall, we expect Chinese real GDP growth to cool to 6.4% in 2018 and 6.1% in 2019. Consumer price inflation, which remained benign in 2017, should accelerate on the back of higher energy prices and robust wage growth but will continue to remain below the People’s Bank of China’s (PBoC) 3% target. The PBoC will therefore prefer to remain on hold, but U.S. rate hikes could lead to higher interbank interest rates and additional volatility in the Chinese currency.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2018 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust