- Checks and Balances

- The U.S. Faces Daunting Deficits

- U.S./Asia Trade Frictions Are Not New

I still balance our checkbook every month. I realize that I am in the minority; only a third of Americans use checks regularly and only 20% reconcile their personal ledgers with their bank statements. But I’ve always found the discipline useful. At first, it helped ensure that we remained solvent (which was touch-and-go for a while); today, it keeps me in close touch with trends in revenue and expenses.

Some politicians have drawn parallels between public budgets and household checkbooks, and suggested they be managed in a similar fashion. The comparison is not entirely appropriate: households can’t print money or borrow immense sums at low interest rates. Government incomes and costs don’t have to be aligned every month; such a strategy would be ruinous if pursued during a recession.

But the global economy is not in a recession, and yet government budgets are far out of alignment. To make matters worse, government accounting often excludes enormous obligations that will become more pressing in the years ahead. If we are to avoid a worst-case outcome, some checkbook sensibility might just be in order.

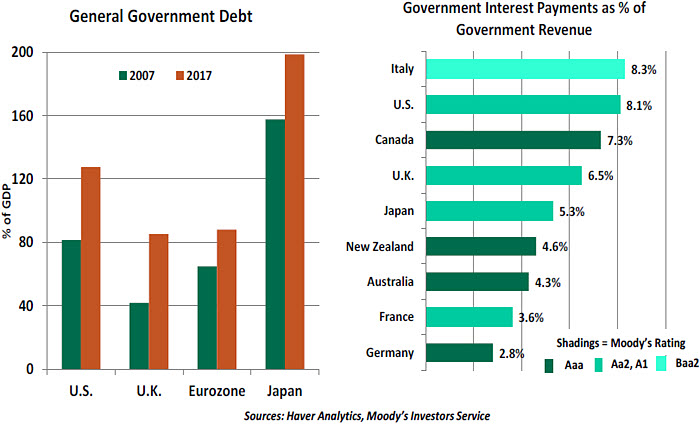

Ten years ago, the world endured its most challenging economic interval since the Great Depression. National incomes fell sharply, and demands on public budgets rose. To arrest the decline, governments in major countries doubled their debt levels, using the proceeds to offset the drop in private demand.

Despite the massive increase in sovereign debt, the cost of borrowing has remained reasonable. Central banks have kept interest rates low and undertaken huge bond purchasing programs. International investors still find liquidity, quality and creditworthiness in U.S. Treasuries, British gilts, German bunds and other government issues. Rating agencies have downgraded a handful of countries, but not to any serious degree.

Happily, fiscal activism had its desired short-term effect. Government borrowing sustained economic growth while consumers reduced their leverage. In all but a handful of developed countries, household debt ratios have improved significantly since 2009. With employment and financial markets strengthening, consumers are again positioned to power growth in gross domestic product (GDP). The global expansion is gaining steam, even at an advanced age.

Ideally, all of this good fortune would swell public coffers and allow debt to stabilize (or even decline). Legislators were understandably reluctant to become too austere too soon, but the strength of the current business cycle could certainly have allowed governments to begin banking some of the fruits of their labors.

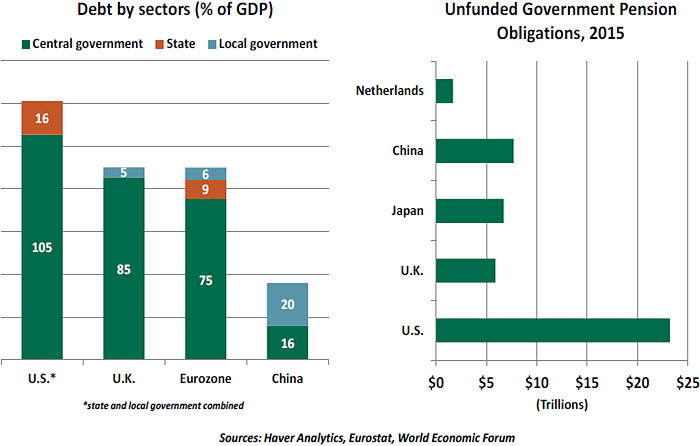

A normal cyclical moderation in borrowing would be welcomed for secular reasons. Aging populations are drawing more from public pension programs and using more government-provided medical care. The cost of these entitlements typically appears in the national ledger only when paid, even though longer-term views often show substantial underfunding. As these obligations migrate from the shadows of government

accounting into the light, it will be harder to achieve any kind of balance in public budgets.

But the opposite seems to be happening. Moderation in public spending encounters stiff resistance, but revenue relief is greeted enthusiastically. There are elections to be won and favor to be curried among voters. Economic consequences that won’t appear until well after all the ballots are counted become an afterthought. Temperance lectures don’t carry much weight.

This also seems to be the spirit at the regional and local levels. States, provinces and cities worldwide have taken on substantial amounts of incremental debt over the last decade, placing the creditworthiness of many into significant question. Their pension and health systems are often severely underfunded. Their borrowing costs are considerably higher, and they do not have access to a printing press to inflate their way out of trouble.

The risk that national authorities may have to step in to resolve and/or backstop a local government has risen significantly, and there is no clear roadmap for how such a situation would be handled. The sad case of Puerto Rico is an imperfect analog, but it illustrates how difficult it is to mutualize debt across governmental levels.

Scolds (like me) warn that a day of reckoning will surely come. Countries have lost control of their fiscal fates in the past, resulting in steep losses for bondholders and severe economic consequences. We seem to be entering a phase where central banks will lighten their ownership of sovereign debt, and overseas investors may reduce their holdings as part of their own demographic evolutions.

But the most extreme failures have occurred in emerging markets, which are poor precedents for what might befall larger countries. Researchers have tried to quantify the tipping point for debt-to-GDP ratios, but the evidence is not conclusive. Where larger economies have been at risk, international financial agencies like the International Monetary Fund, the World Bank, and the Eurosystem have come to the rescue. But the support and resources required for these organizations to fulfill their missions has been flagging, limiting their ability to cushion falls.

Much as citizens might like to disavow responsibility for their government’s actions (“I didn’t vote for that pension plan, so I don’t see why I have to pay taxes to support it”), we all “own” a piece of our government’s debt. If we thought about it at a personal level, we might demand more fiscal responsibility from the politicians we elect. Checks, and balances, are still very important.

When You Find Yourself in a Hole, Stop Digging

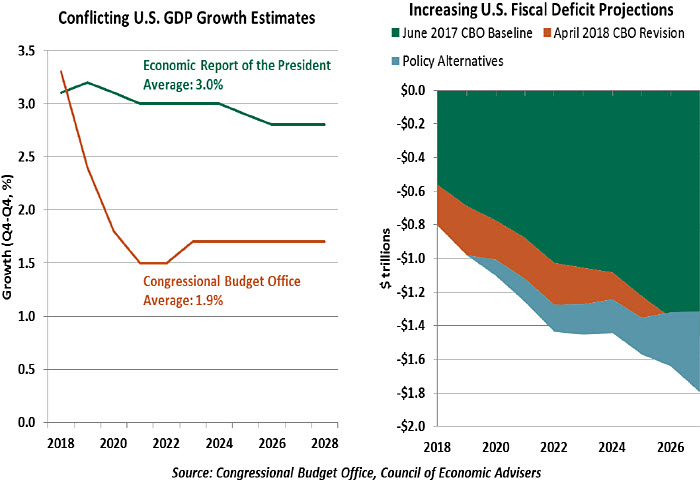

The first significant piece of economic legislation to come out of the Congress last year was the Tax Cuts and Jobs Act (TCJA). Reducing taxes is a reliable plank of the Republican platform, and this legislation was not much of a surprise in its intent. As we discussed at the time, its size and timing were questionable. It stimulated an economy that was already performing well and changed the nation’s fiscal course in a potentially dangerous way.

The TCJA’s supporters claimed that tax reductions would spur greater economic activity, and the ensuing growth would raise sufficient tax revenue to limit the deficit. But this week, the non-partisan Congressional Budget Office (CBO) threw cold water on that expectation. The outlook is sobering: the U.S. is now forecast to reach a $1 trillion annual deficit starting in 2020, and remain at or above that level indefinitely. The increasing burden of interest payments, combined with the obligations of an aging population, will weigh on growth and provide few opportunities to reduce the deficit in the future.

Proponents of the TCJA predicated their positive forecasts on maintaining real U.S. GDP growth of 3%. In a mature economy, 3% growth is difficult to sustain; the U.S. has not held that level since the technology boom of the 1990s. The CBO’s forecast (similar to Northern Trust’s U.S. Economic Outlook) predicts a strong year of growth in 2018, followed by a tapering. In the long run, the U.S. will grow at its potential rate of 1.9% on average, an insufficient rate to provide enough government revenue to control the deficit.

The TCJA was bound by the Byrd Rule, a Senate requirement that halts reconciliation of a bill if it will add to the federal deficit after ten years from the bill’s passage. For compliance, therefore, most of the TCJA’s provisions were set to expire in stages through 2026. But after a tax cut takes effect, even if the cut was advertised to be temporary, any subsequent increase will feel like a tax hike. Voters do not appreciate tax increases; as such, temporary provisions often become permanent. As recently as 2010, Barack Obama continued temporary tax cuts passed by George W. Bush, a concession preferable to raising taxes in the midst of a recession.

The CBO considered the likely case that tax provisions scheduled to expire or reset would be permanently extended, and caps on discretionary federal appropriations (recently increased by $300 billion over the next two years) would remain elevated. In this case (charted above as “Policy Alternatives”), deficits would average nearly 6% of GDP through 2028, a full percentage point higher than under the CBO’s baseline. Debt held by the public would reach about 105% of GDP by the end of 2028 (the largest share since 1946), and continue to rise thereafter.

In its report, the CBO notes that its analysis does not include any legislation or policies introduced from mid-February onward, an allusion to the tariff proposals that may weigh on economic output. It also implicitly assumes that demand for U.S. Treasuries never subsides. As discussed above, what would happen if debt financing were unavailable or

became more expensive?

There is still time to address the situation, although the political will seems lacking. Today’s younger workers are starting their adulthood in a fiscal hole, and we would do well to reduce our digging.

Asian Echoes

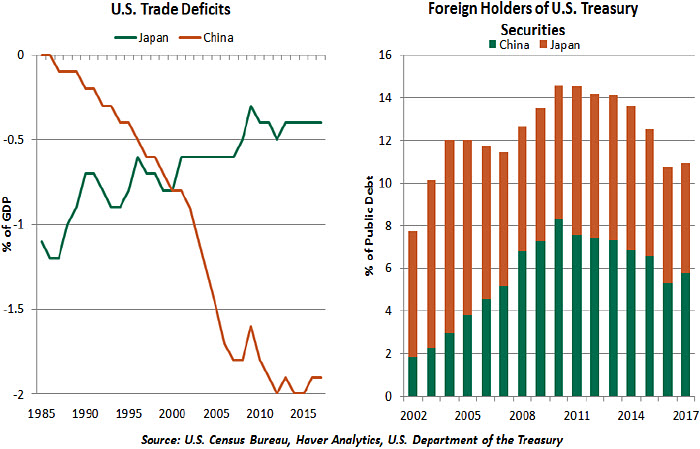

As we try to understand China’s ascent and its prospects as a global competitor, we might consider the rise of Japan from the 1950s through 1990s. At first glance, they are analogous. Both followed strategies of promoting growth through increased manufactured exports and acquisition of foreign technology. The U.S. trade deficit with China, at 1.9% of U.S. GDP, is similar to Japan’s peak of 1.2% in 1986. Both situations generated important anxiety in Washington.

In their times, both countries have been suspected of undervaluing their exchange rates; both have been the largest foreign holders of dollar-denominated U.S. government securities (more than $1 trillion each); and both provided subsidies to certain preferred industries. China and Japan each competed, successfully, with the United States for export market share to both emerging and developed markets.

The two cultures centered on carefully managed capitalism, which nurtured domestic industries without exposing them fully to global competition. The Eastern styles of leadership and management intrigued and influenced Westerners.

However, the China of today presents a different story than the Japan of the 1980s. Unlike Japan in the post-World War II era, China isn’t dependent on the U.S. for its security, nor is it seen a U.S. ally. (In fact, China’s strategic interests are not aligned with those of the U.S. in key areas.)

When handling trade tensions, China is choosing a different course than Japan did. Responding to tariff announcements, China has already started retaliating by targeting U.S. agricultural, plastic and chemical sectors. In contrast, when threatened with 100% tariffs on automobile imports, Japan agreed to buy more American parts and ultimately

made peace by building production facilities in the United States.

China has made friendly promises to further open its manufacturing sector by easing joint venture requirements and opening its financial markets more fully to Western firms. But in other areas, such as technology, it may be quite a while before China matches Japan’s level of conciliation. They may not need to: they are bigger and more powerful (in many ways) than Japan was in the 1980s. And relatively speaking, the U.S. may not be as strong.

An escalation of today’s conflict between the U.S. and China will have far-reaching implications for both sides. Japan offers a case study for China to seek a peaceful steady state. China is likely to maintain a balanced stance, neither retaliating into a full-blown trade war nor conceding to every demand made by the U.S. As the European Central Bank’s Benoît Coeuré recently stated: “There are no winners in trade wars, just different degrees of losers.”

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust