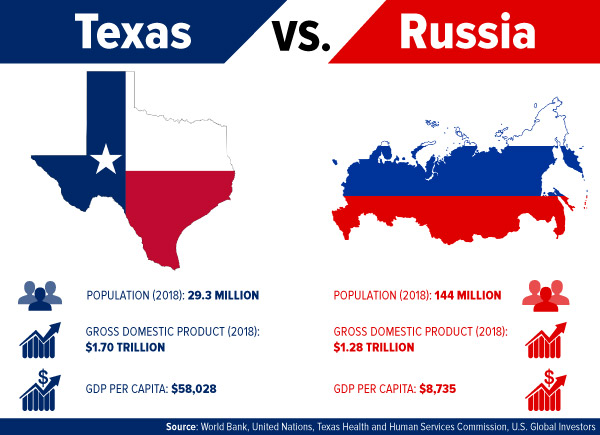

Which Has the Bigger Economy: Texas or Russia?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

You’ve no doubt heard that everything’s bigger in Texas. That’s more than just a trite expression, and I’m not just saying that because Texas is home to U.S. Global Investors.

Want to know how big Texas really is? Let’s compare its economy with that of Russia, the world’s largest country by area. As you probably know, Russia’s been in the news a lot lately, so the timing of this comparison makes sense. The U.S. just levied fresh sanctions against the Eastern European country for its alleged meddling in the 2016 presidential election, and this week President Donald Trump warned Russia that the U.S. military could soon strike its ally Syria in response to its use of chemical weapons.

The Russian ruble traded sharply down following the news, decoupling from Brent crude oil, the country’s number one export.

But back to the comparison. Even though Russia has nearly five times as many residents as Texas, the Lone Star State's economy is more than $40 billion larger. Texans, therefore, enjoy a gross domestic product (GDP) per capita of around $58,000, whereas Russians have one closer to $8,700.

Texas Is So Much More than Oil Country

The Russian Federation is the largest single producer of crude in the world, pumping out 10.95 million barrels per day (bpd) in January, according to the country’s energy minister. Texas is no slouch, though, as its output came close to 4 million bpd in January. That’s the most ever for a January since at least 1981. And from December 2017 to February 2018, its oil and gas industry accounted for nearly 30 percent of the state’s employment growth, according to the Federal Reserve Bank of Dallas.

But whereas Russia’s economy is highly dependent on exports of oil and petroleum products, the Texas economy is broadly diversified. The state ranks first in the U.S. for not only oil production but also wind energy. It has a robust agricultural sector, and it’s a leading hub for advanced technology and manufacturing, aeronautics, biotechnology and life sciences. Austin, the state capital, is steadily emerging as the most dynamic U.S. filmmaking city outside of Hollywood.

All of this has helped contribute to Texas being among the fastest growing states in the U.S. In 2017, it grew by more than 1,000 new residents per day.

Meanwhile, Russia’s population is slowly shrinking because of low birth rates and immigration. Its population peaked at 148 million in the early 1990s—right around when the Soviet Union fell—and by 2050, it’s estimated to sink to 111 million.

Can Russia Root Out Its Corruption?

One area where Russia trumps Texas is in corruption. I’ll admit, the Lone Star State faces a few problems of its own involving corruption, which leaders must address.

But Russia takes it to a whole new level. Last year, it ranked 135 out of 180 countries on Transparency International’s Corruption Perceptions Index (CPI), released in February. Among Eastern European countries, only Uzbekistan, Tajikistan and Turkmenistan ranked lower. Watchdog group Freedom House was similarly critical in its most recent analysis, giving the country an overall democracy score of 6.61 out of 7, with 7 being “least democratic.”

So notorious and widespread is Russia’s mafia that a number of movies have been made about it. One of the best among them is David Cronenberg’s excellent Eastern Promises (2007).

Having said all that, I believe it’s prudent for investors to underweight Russian stocks for the time being and overweight Western Europe. Because of U.S. sanctions, Americans have until May 7 to divest completely from a number of Russian names, including Rusal, En+ Group and GAZ (Gorkovsky Avtomobilny Zavod), all of which saw serious outflows this past week. The MSCI Russia Index, which covers about 85 percent of Russian equities’ total market cap, plunged below its 200-day moving average, but yesterday it jumped more than 4 percent, its best one-day move in two years.

Weaker Greenback and $1 Trillion Deficit Helps Gold Glitter

Gold is rallying right now, but as I told Daniela Cambone in this week’s “Gold Game Film,” it has little to do with Russian geopolitics, or even trade war fears, which have subsided somewhat since last week. Instead, the price of gold is responding primarily to a weaker U.S. dollar. For the 30-day period, the greenback has dipped close to 20 basis points—for the year, more than 11 percent.

I think what’s also driving the yellow metal right now are concerns over the U.S. budget deficit and ballooning government debt. This week the Congressional Budget Office (CBO) said it estimated the deficit to surge over $1 trillion this year and average $1.2 trillion each subsequent year between 2019 and 2028, for a total of $12.4 trillion. By the end of the next decade, then, debt held by the public is expected to approach 100 percent of U.S. GDP.

According to the U.S. National Debt Clock, government debt now stands at over $21 trillion—or, put another way, $174,000 per taxpayer. Imagine what the interest payments on that must be.

The CBO, in fact, commented on this. Believe it or not, the government’s annual payments on interest alone, made even more burdensome by rising rates, are expected to exceed what it spends on the military by 2023. And remember, defense is one of the country’s top expenditures, alongside Medicare, Medicaid and other entitlement programs.

There was even more news this week on debt and the deficit, as Congress tried, and failed, once again to amend the Constitution by requiring a balanced budget. The amendment could not get the two-thirds support it needed.

You can probably tell where I’m headed with all of this. Savvy investors and savers might very well see this as a sign to allocate a part of their portfolios in “safe haven” assets that have historically held their value in times of economic contraction.

Gold is one such asset that’s been a good store of value in such times. As I’ve shown before, gold has tracked U.S. government debt up since 1971, when President Richard Nixon ended the gold standard. I always recommend a 10 percent weighting in gold—5 percent in bars and coins; 5 percent in high-quality gold stocks, mutual funds or ETFs.

Asset Allocation Works

On a final note, I think it’s important that investors remember to stay diversified, especially now with volatility hitting stocks and geopolitical uncertainty on the rise. I’ve discussed Roger Gibson’s thoughts on asset allocation with you before, and I believe his strategy still holds up well today to capture favorable risk-adjusted returns.

In the chart above, based on Gibson’s research, you can see that a portfolio composed of U.S. stocks, international stocks, real estate securities and commodity securities gave investors an attractive risk-reward profile between 1972 and 2015. This diversified portfolio, represented above by the orange circle, delivered good returns with a digestible amount of volatility, compared to portfolios that contained only one, two or three asset classes. Concentrating in only one or two asset classes could possibly give you higher returns, but you’d also likely see much greater risk, which many investors aren’t willing to accept.

I believe adding fixed-income—specifically short-term, tax-free municipal bonds—could improve these results. Munis with a shorter duration, as I’ve explained in the past, have a history of being steady growers not just in times of rising rates but also during market downturns. In the past 20 years, the stock market has undergone two massive declines, and in both cases, short-term, investment-grade munis—those carrying an A rating or higher—helped investors stanch the losses.

Learn more about the $3.8 trillion municipal bond market by clicking here!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.79 percent. The S&P 500 Stock Index rose 1.99 percent, while the Nasdaq Composite climbed 2.77 percent. The Russell 2000 small capitalization index gained 2.39 percent this week.

- The Hang Seng Composite rose 2.57 percent this week; while Taiwan was up 1.33 percent and the KOSPI rose 1.05 percent.

- The 10-year Treasury bond yield rose 5 basis points to 2.82 percent.

Domestic Equity Market

Strengths

- Energy was the best performing sector of the week, increasing by 6.02 percent versus an overall increase of 1.91 percent for the S&P 500.

- Concho Resources was the best performing stock for the week, increasing 13.01 percent.

- Bayer's takeover of Monsanto was approved by the Department of Justice, sending shares of the seed maker up more than 6 percent on Monday.

Weaknesses

- Utilities was the worst performing sector for the week, decreasing by 1.35 percent versus an overall increase of 1.91 percent for the S&P 500.

- American Airlines was the worst performing stock for the week, falling 8.79 percent.

- Bed Bath & Beyond’s stock fell more than 18 percent on Thursday after the company issued 2018 earnings guidance that came up short of consensus expectations and left investors questioning the company's ability to navigate a tricky retail environment.

Opportunities

- According to Charles Payne from Smart Talk, since peaking on January 26, the stock market has been on a wild yet contained ride that saw the S&P 500 hit a low on February 8 and then retest and hold that same level on April 2. According to Payne, this was the “ultimate double buy signal.” Payne also highlights the upcoming earnings season, which could hold encouraging signs for the market.

- JPMorgan is very bullish on first quarter earnings. The firm’s equity strategists are forecasting record breaking results to propel the markets after a volatile start to the year.

- Dell Technology's cloud-computing business Pivotal Software priced its initial public offering at $14 to $16 a share. It will trade under the ticker PVTL.

Threats

- Stocks haven't been interrupted yet, but should be on guard with inflation expectations near three-year highs amid rising macroeconomic pressure, writes Bloomberg Intelligence strategists Gina Martin Adams and Peter Chung. If the Goldilocks backdrop that supported equity markets for years fades, a new inflation regime could result in wider dispersion of returns and spur drawdowns. Similar to the 1960’s period of a post-deflationary rebound, the S&P 500's price-to-earnings multiple may also get squeezed, accompanied by significant turnover in styles and sectors.

- A dispute over who will cover the costs for fixing a production error on more than 200 stealth jets has caused the Pentagon to stop accepting deliveries of most F-35s from Lockheed Martin, Reuters says, citing three people familiar with the matter.

- Apple has reportedly slashed production orders for its HomePod smart speaker because people aren't buying it. According to Bloomberg, Apple began cutting orders for the HomePod in March and existing inventory is piling up.

The Economy and Bond Market

Strengths

- Federal Reserve officials leaned toward a slightly faster pace of tightening at their March meeting as their growth outlook and confidence in hitting the inflation target strengthened, the minutes show. "A number of participants indicated that the stronger outlook for economic activity, along with their increased confidence that inflation would return to 2 percent over the medium term, implied that the appropriate path for the Federal funds rate over the next few years would likely be slightly steeper than what they had previously expected," the records of the March 20-21 FOMC meeting said.

- The March consumer price index (CPI) moved up to 2.4 percent in March from 2.2 percent in the prior month, Labor Department data showed. Core inflation, excluding volatile food and energy prices, rose to 2.1 percent from 1.8 percent. The two CPI inflation measures are now above 2 percent for the first time since February 2017.

- Euromoney’s country risk survey shows a generalized improvement in risk scores in the first quarter of 2018, arising from brighter political and economic prospects, and improving capital access for sovereign borrowers. The resultant unweighted average global risk score for 186 countries has improved for a third consecutive quarter, according to Euromoney’s survey, with 99 countries upgraded, 48 downgraded and 39 unchanged.

Weaknesses

- Sentiment among small U.S. companies took a step back in March as a smaller share of owners said they expected business conditions to improve in coming months, a possible reflection of concerns about tariffs. Expansion plans and sales expectations also eased, pushing the index of small-business optimism to a five-month low of 104.7 (estimate 107), according to the NFIB, from 107.6 prior.

- The U.S. budget deficit widened to $600 billion halfway through the fiscal year, as spending growth outstripped revenue. Receipts rose by 1.6 percent to $1.5 trillion between October and March compared with a year earlier, while outlays climbed by 4.8 percent to $2.1 trillion, the Treasury Department said in its monthly budget statement. Corporate income taxes fell to $78.6 billion in the first half of fiscal 2018, from $100.2 billion a year earlier.

- Total foreign direct investment between the U.S. and China fell 28 percent in 2017 from 2016, driven by a drop in Chinese investment to $29 billion from $46 billion, according to a report by Rhodium Group and the National Committee on U.S.-China Relations. This is a result of China tightening controls over outbound investment, while U.S. national security officials clamped down on Chinese acquisitions of American companies.

Opportunities

- President Trump told lawmakers he is considering rejoining the Trans-Pacific Partnership, the free-trade deal he withdrew from shortly after taking office, as he expressed confidence that the U.S. is headed toward resolving trade conflicts without economic disruption. A week after escalating tensions with his threat to impose tariffs on an additional $100 billion in Chinese products, Trump said the two countries ultimately may end up levying no new tariffs on each other.

- Owners of variable-rate munis are getting a tax-season bonus. Because some investors sell them to get cash to pay tax bills, banks’ inventories of VRDOs surged, causing yields to head higher, according to Barclay’s analysts led by Mikhail Foux. Securities dealers’ holdings of the bonds jumped to $5.1 billion by the last week in March, the most since December, according to the Federal Reserve Bank of New York. That has helped push yields on the securities above those on one-year debt for the past two weeks, a relatively rare occurrence in the municipal market.

- There may be "hope on the horizon" for municipal-bond investors because prices are likely to rise relative to Treasuries, Barclay’s analysts said in a note. "Historically ratios decline in the second quarter, and we think that this year could follow this general trend," the analysts wrote. Flows into municipal mutual funds are typically positive in April and the analysts said they don’t expect much more selling from banks and property and casualty insurance companies.

Threats

- One sign that U.S. inflation may be heading higher is coming from the NFIB monthly survey of small businesses: the net percentage of respondents are saying they’re raising prices. That number rose to 16 percent in March, the highest level since September 2008. While the data point was closely correlated with the headline inflation rate in prior expansions, the relationship has weakened somewhat since the financial crisis.

- Global debt rose to a record $237 trillion in the fourth quarter of 2017, more than $70 trillion higher from a decade earlier, according to an analysis by the Institute of International Finance. At the same time, the ratio of global debt-to-GDP fell for the fifth consecutive quarter as the world’s economic growth accelerated. The ratio is now around 317 percent of GDP, or 4 percentage points below the high in the third quarter of 2016, according to the IIF.

- CBO chief Keith Hall told the Senate Budget Committee that America’s net interest payments will triple over the coming decade, outpacing military expenditures. He called the data point "one of my favorite figures" used to highlight the challenges posed by the country’s ballooning debt. CBO forecasts show net interest payments first outstripping defense outlays in fiscal 2023 and reaching $915 billion five years later. The increase will come as debt held by the public almost doubles to $28.7 trillion in fiscal 2028 from this year, according to the CBO.

Gold Market

This week spot gold closed at $1,345.43, up $11.78 per ounce, or 0.88 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.66 percent. Junior-tiered stocks slightly underperformed seniors for the week, as the S&P/TSX Venture Index came in up 3.48 percent. The U.S. Trade-Weighted Dollar fell this week and lost 0.35 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Apr-10 | PPI Final Demand YoY | 2.9% | 3.0% | 2.0% |

| Apr-11 | CPI YoY | 2.3% | 2.4% | 2.2% |

| Apr-12 | Initial Jobless Claims | 230k | 233k | 242k |

| Apr-13 | Germany Retail Sales YoY | 1.6% | 1.6% | 1.6% |

| Apr-16 | China Retail Sales YoY | 9.7% | -- | 9.4% |

| Apr-17 | Germany ZEW Survey Current Situation | 88.0 | -- | 90.7 |

| Apr-17 | Germany ZEW Survey Expectations | -1.0 | -- | 5.1 |

| Apr-17 | Housing Starts | 1267k | -- | 1236k |

| Apr-18 | Eurozone CPI Core YoY | 1.0% | -- | 1.0% |

| Apr-19 | Initial Jobless Claims | 230k | -- | 233k |

Strengths

- The best performing metal this week was palladium, up 9.16 percent on concerns new Russian sanctions announced at the start of week could disrupt supplies. Gold traders and analysts are at their most bullish on the gold price in a year, according to the weekly Bloomberg survey. Gold ETFs saw holdings increase for seven consecutive days with total holdings at their highest levels since May 2013.This year so far there have been 2.5 million troy ounces added to holdings. According to Bank of America Merrill Lynch, investors have added $7 million into funds that are linked to gold.

- Recent tensions in the market have pushed traders into gold as the cost of bullish options on the SPDR Gold Shares ETF surged to a record relative to bear contracts. Outside of the U.S., investors in Germany are also rushing into gold on fears of trade tensions. According to Bloomberg, the Frankfurt-listed Xetra-Gold stock hit a record high this week.

- Japan’s biggest gold retailer, Tanaka Kikinzoku K.K., says that gold bar sales are up 41 percent in the first quarter of this year compared to the year prior. Bloomberg writes that the local price of bullion in Russia rallied this week to the highest since 2016 on the heels of more sanctions from the U.S. The Russian Central Bank is the fifth-largest sovereign holder of gold.

Weaknesses

- The worst performing metal this week was gold, still up 0.88 percent. Gold futures saw their biggest loss in two weeks as the dollar rose on the heels of President Donald Trump signaling that an attack against Syria would not be imminent. Equities rallied and gold fell earlier this week as Chinese President Xi Jinping is expected to calm the trade dispute between China and the U.S., writes Bloomberg.

- India, the second largest consumer of gold, fell by 47 percent in March to just 64.2 metric tons, down from 121 tons a year earlier. Imports for the first three months totaled 159 tons, down from 42 percent a year prior, according to Bloomberg. Dubai also saw gold sales fall around 50 percent this past quarter after implementing a valued-added tax. Bloomberg News writes that gold demand in the United Arab Emirates has not recovered from the pre-financial crisis levels in 2008 and dropped to a 20-year low in 2017.

- Harmony Gold says that $519,000 of gold was stolen from its Kalgold mine on Tuesday morning in South Africa, totaling 386 ounces of the precious metal.

Opportunities

- This week saw several more indicators that inflation is on the rise, which has historically been positive for the gold price. Royal Bank of Canada noted that the March employment report saw employees quitting their jobs at a rate of 13 percent, the highest level in 17 years. This indicates wage inflation and a tightening labor market. The U.S. Treasury has asked primary dealers about potentially increasing issuance of TIPS over the next 12 months. The Treasury also requested comments from the primary dealer on the drivers and outlook for foreign private and official demand for U.S. Treasuries. It’s interesting that the Fed wants to know what it will take to entice foreign buyers to fund budget deficits.

- This week Jeff Gundlach, who manages over $100 billion at DoubleLine Capital, had very positive thoughts on gold. Gundlach said: “We see that gold broke above its downtrend line. But now we see a massive base building in gold. Massive. It’s a four-year, five-year base in gold. If we break above this resistance line one can expect gold to go up by, like, a thousand dollars.” He continued on to say that now is “a great time to be buying gold straddles.”

- Bridgewater Associates co-Chairman Ray Dalio wrote on LinkedIn this week that he has raised his probabilities of a trade war and other types of wars, such as cyber wars. Dalio said that “one should consider the possibility that this trade war could almost become a capital war,” which “will be even uglier than a trade war,” reports Bloomberg. Robert Burgess wrote on Bloomberg View that investors are losing confidence in President Trump. He reports that Nader Naeimi, an Australian money manager says that “For a growing number of global money managers, the risks of investing in the U.S. are too great right now given all the political uncertainty.” Fewer foreign investments could lead to a depreciated dollar.

Threats

- The risk of an inverted Treasury yield curve, when short-term yields are higher long-term yields, is back on analysts’ radars. An inverted yield curve has proceeded most U.S. recessions over recent decades.

- Bloomberg reports that China is looking into the possibility of gradually devaluing their currency, the yuan, as a tool in trade negotiations with the United States. Senior China officials are said to be examining what would happen if they devalued the yuan to offset any impact of a trade deal that curbs exports.

- On Monday President Donald Trump expressed his optimism that the U.S. will be able to reach a deal with China over trade disputes that have brought volatility and uncertainty to markets in recent weeks. However, not all are confident that a deal with be reached soon, as a former Chinese diplomat suggested that Beijing was not yet ready to hold talks.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended April 13 was MaxCoin, which gained 372 percent.

- On Thursday, bitcoin surged the most on an intraday basis since December after breaching key technical levels, reports Bloomberg. In less than an hour, the biggest digital currency climbed as much as 16.9 percent, the article continues. According to Thomas Lee of Fundstrat Global Advisors, a combination of Santander’s plan for a blockchain-based payment app, tax-related selling nearing an end, and speculative short investors being squeezed out of the market are all to blame for the surge in price.

- Looking over the last week, it appears a handful of the major cryptocurrencies have been seen consolidating. For example, it appears that Ethereum’s consolidation stage that started in April may have established a bottom. Although the current price of Ethereum is still below its 50-day moving average, the digital currency’s recent price action is a much needed step in the right direction.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended April 13 was Bismuth, which lost 68.80 percent. According to Chief Investment Strategist at Bank of America Michael Hartnett, cryptocurrencies are following the same downfalls of other massive price bubbles in history, such as tulips and the Mississippi Company.

- The blockchain conference Global Fintech & Blockchain China Summit 2018 was abruptly shut down by police on Thursday in Shanghai. No reason was given for the cancelation, however, according to Coindesk, a rumor was leaked that investors reported the conference to police after losing a large sum of money in an initial coin offering (ICO).

- One of India’s largest cryptocurrency trading platforms, Coinsecure, lost some 438 bitcoins worth approximately 190 million rupees, or $3 million, reports Bloomberg. The heist was allegedly due to a rogue employee of the platform. Efforts to reimburse users or recover the bitcoins may be hindered as the Reserve Bank of India banned regulated entities from providing services to users, holder and traders of cryptocurrencies last week.

Opportunities

- Another crypto-expert is leaving Goldman Sachs, reports Bloomberg, as “wild swings in prices for bitcoin, Ethereum and other digital currencies attract Wall street traders, tech investors and regulators.” Mike Novogratz’ cryptocurrency merchant bank Galaxy Digital hired Richard Kim from Goldman as its chief operating officer, according to people with knowledge of the matter. Kim, a London-based VP at Goldman, was among those working to set up a Goldman desk for trading cryptocurrencies.

- The Winklevoss twin-operated cryptocurrency exchange, Gemini, will allow traders and investors to purchase large quantities of digital currencies through block trading, reports ETF Trends. Cameron and Tyler Winklevoss are big supporters of cryptocurrencies and pushed to introduce the first U.S. bitcoin ETF, the Winklevoss Bitcoin Trust.

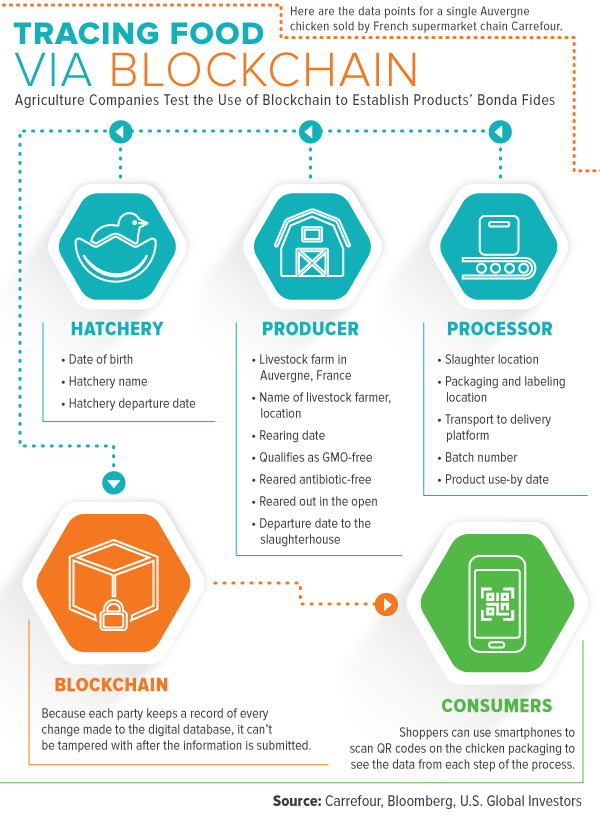

- Thanks to the use of blockchain technology, every chicken that is sold by Carrefour SA, a France-based grocery chain, comes complete with its very own life story. By scanning the label with your smartphone, consumers can get all of the details (where the bird came from, whether or not it ate healthy grains, etc.). This is an example of the trend toward improving food safety by using the same technology that serves as the backbone of bitcoin and other cryptocurrencies, writes Bloomberg’s Luzi-Ann Javier.

Threats

- Russian messaging app, Telegram, has been blocked by telecommunications companies after failing to follow regulations of granting intelligence authorities access to users’ encrypted messages. The app had recently raised $1.7 billion in its initial coin offering and has over 9.5 million users in Russia and over 200 million users globally, according to Bloomberg. Operators of information dissemination in Russia are required to provide encryption keys to authorities to read the correspondence of suspected terrorists.

- Long Blockchain Corp. said on Tuesday that it is being suspended by Nasdaq, pursuant to a rule that gives the exchange operator the ability to remove firms with histories of misconduct. The company saw its share prices skyrocket after shifting focus from iced tea to cryptocurrencies. Another firm that rebranded with blockchain, Longfin, received a Nasdaq noncompliance letter due to failing to file its quarterly report on time, reports Bloomberg. These firms are just two of many who bet on cryptocurrencies and blockchain, and are now struggling after the steep bitcoin price drop over the last few months.

- With 17 million of the 21 million bitcoins already mined, the cost and difficulty of mining virgin coins will only increase, making many firms hesitant to join the game, reports Bloomberg. After running back-of-the-envelope math on Permian producers potentially turning to bitcoin mining, Bernstein analysts concluded the “fleeting thought of becoming a Permian-bitcoin billionaire will remain, for now, a dream.”

Energy and Natural Resources Market

Strengths

- Crude oil was the best performing major commodity this week rising 8.4 percent. The commodity rallied to a three-year high as geopolitical risk took front stage this week with President Trump threatening to launch attacks on Syria, which could further destabilize the Middle East and the global crude supply chain.

- The best performing sector this week was the S&P1500 Oil & Gas Explorers and Producers Index. The index rose 8.9 percent after crude oil posted its largest weekly advance since 2016.

- The best performing stock for the week was TGS-NOPEC Geophysical Company. The Norwegian oil services and data science company rose 23.8 percent after announcing a major expansion of its highly successful multi-client 3D seismic program in the Norwegian Sea.

Weaknesses

- Steel was the worst performing commodity this week. The commodity dropped 4.7 percent after a number of global producers disclosed significantly higher-than-expected production volumes in the first quarter. In addition, fears of a trade war boosting prices have not materialized as producers in Europe and Asia have not halted or reduced output.

- The worst performing sector this week was the S&P1500 Construction and Materials Index. The index dropped 1.5 percent as the much-touted U.S. infrastructure plan takes second stage with the White House showing greater concern over trade issues and the deteriorating situation in Syria.

- The worst performing stock for the week was NovaTek PJSC. The Russian natural gas producer dropped 11.6 percent together with Russian stocks which tumbled the most in more than two years after new U.S. sanctions hit Kremlin-connected billionaires, leading to major stock liquidations and dispositions from U.S. based funds and individual investors.

Opportunities

- OPEC sees a tighter market as oil output drops to the lowest in a year. OPEC said its oil output fell to the lowest in a year last month amid reduced supplies from Venezuela and Saudi Arabia, suggesting global markets may tighten sharply later this year. If Venezuela’s industry continues to deteriorate, and President Trump delivers on threats to sanction Iran, OPEC’s unintended losses could effectively double the cut it set out to implement.

- Further to OPEC’s comments, the International Energy Agency (IEA) said Friday that less than 10 percent of the surplus in oil inventories remains, as OPEC (and its partners) have cut production by even more than they intended while world demand soars. “It is not for us to declare on behalf” of OPEC “that it is ‘mission accomplished,’ but if our outlook is accurate, it certainly looks very much like it,” the IEA said in its monthly report.

- The case for owning commodities has rarely been stronger, according to Goldman Sachs Group Inc. With raw materials rallying on escalating political tensions across the globe and economic growth remaining strong, the bank’s analysts, including Jeffrey Currie, doubled down on their “overweight” recommendation.

Threats

- Senior Chinese officials have studied devaluing the yuan to address the impact of a trade war. Officials have studied a two-pronged analysis of the yuan that was prepared by the government, looking at the effect of using the currency as a tool in trade negotiations with the U.S., while also examining what would happen if China devalued its currency. A Chinese yuan devaluation would make raw material imports more expensive for China, which could lead to a significant drop in demand and prices for commodities.

- Zinc prices tumble on fears China may release stockpiled material to alleviate cost pressures at its steel mills. There’s speculation that China’s State Reserve Bureau plans to release stockpiles, adding to rising supply from newly built mines coming online in 2018, according to Wei Lai, an analyst at Cofco Futures Ltd.

- An expected shortage of pulp and paper products may not materialize after China unexpectedly ramps output. Recent data from market specialists suggest Chenming Paper is set to add 1.0 million tonnes per annum of hardwood capacity, and an additional 300,000 to 600,000 tonnes of softwood capacity this year; much of it in excess of previously announced expansion plans. The larger-than-expected capacity additions address much of the anticipated shortage and may exert downward pressure on pulp prices.

China Region

Strengths

- Taiwan’s year-over-year exports and imports for the March measurement period both beat expectations this week. Exports came in strongly up 16.7 percent, handily beating analysts’ anticipated number of only 8.4 percent. Imports clocked in up 10.4 percent, ahead of an expected 8.8 percent print. Both numbers were up significantly from the prior month.

- China announced it aims to begin a stock-trading link between London and Shanghai sometime later this year, Bloomberg News reports a “top official” as saying. The tie-up would “give investors in the world’s most populous country direct access to shares listed in the U.K. The PBOC Governor Yi Gang also announced that China will raise the daily limit for net buying into Hong Kong [by fourfold] using the HK-Shanghai stock-connect program, beginning May 1.

- China’s foreign exchange reserves increased for the March period, moving higher once again after a minor interruption last month. The actual number was $3.143 trillion, slightly short of expectations for 3.146 trillion, but nonetheless importantly demonstrating stability in the overall situation.

Weaknesses

- Year-over-year exports for the Philippines fell 1.8 percent, well below analysts’ estimates for a gain of 6.4 percent and below the January (most recent) print of 0.5 percent. Imports did come in slightly higher, rising 18.6 percent and ahead of estimates for a 16.0 percent print.

- Domestic vehicle sales in Vietnam declined again, with the year-over-year measurement for the March period down 8.1 percent.

- Malaysia’s year-over-year industrial production came in at 3.0 percent for the most recent (February) period, below analysts’ expectations for a 3.3 percent print.

Opportunities

- Chinese President Xi Jinping’s speech on Tuesday struck a moderately conciliatory tone that global markets liked. It should be stressed that much of what appeared to be offered may well have already been on the table, but so too it can be stressed that the tone of the speech (more of détente, if you will, than of escalation) represented a step away from the rhetoric that seems to have spooked markets of late.

- One thing that may be of particular note in President Xi’s speech is what was not present, namely, anything about a change in policies around Hainan and gambling, meaning that while the door has been opened and the intentions perhaps signaled, Macau remains central for the time being and for the foreseeable future.

- Indonesia plans to narrow its fiscal deficit to below 2 percent of GDP next year by boosting its revenue, Bloomberg News reported this week. Revenue is expected to increase 7.6 percent to 13 percent while spending is projected to rise only about 7 percent, the article reports the Indonesian Cabinet Secretariat as stating. The last time the deficit was below 2 percent was 2012.

Threats

- As the authors of a recent Credit Suisse note point out, should U.S.-China trade disputes drag on, one potential side effect is that it “could make the [Chinese] government more cautious in de-leveraging the economy.”

- Investors will remain attentive to any escalation or perceived escalation with respect to the subjects of U.S.-China trade and tariffs.

- It’s Friday the 13. That counts, right? Otherwise, remember that North Korea can still seize the headlines relatively quickly at this point, as the Trump administration says it is nearing the point at which it can pin down a date for the summit. Recent press reports suggest the Trump administration is considering a demand for denuclearization and a timeframe of six to 12 months. Details remain scanty at present.

Emerging Europe

Strengths

- Poland was the best performing country this week, gaining 1.6 percent. Utilities and banks were the best performing among the 20 biggest stocks trading on the Warsaw stock exchange. PGE and Energa SA gained 7.8 percent and 6.3 percent, respectively. The biggest gainer among banks was Bank Zachodni, whose shares appreciated 6.3 percent.

- The Polish zloty was the best performing currency this week, gaining 1.2 percent against the U.S. dollar. As expected, the central bank of Poland left its key rate unchanged at 1.5 percent. Weakening inflation may allow the monetary authority to keep the benchmark rate at a record low for longer.

- The information technology sector was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 4.6 percent. The U.S. announced new sanctions on Russia, and for the first time, the U.S. banned its American investors from holding publicly listed shares of Rusal and EN Group.

- The Russian ruble was the worst performing currency this week, losing 6.3 percent. According to Russian senior central bank and government officials, this is normal volatility after the U.S. announced new sanctions and regulators are not planning any special steps to stabilize markets.

- Financials was the worst performing sector among eastern European markets this week.

Opportunities

- Renaissance Capital held its twenty-second Annual Russian Investor Conference in Moscow and St. Petersburg this week. The group attended meetings with Russian oil and gas companies and is delivering a message of stability and “business as usual” despite the deteriorating relationship between Russia and the U.S. Top government and Central Bank of Russia officials have promised to adopt selective measures to support Russian companies affected by the recent elevations of sanctions. Within oil and gas producers, Lukoil stands out as least exposed to sanctions risk due to its private ownership structure and low levels of debt, according to RenCap’s research.

- The sharp fall in the Russian ruble this week does not rule out further rate cuts, according to Capital Economics. There is less probability of a rate cut later this month, but the group is still forecasting that the central bank will cut its policy rate to 6 percent by year-end, from the current level of 7.25 percent.

- The European Central Bank (ECB) released minutes from its March meeting. The minuets show that the bank worries about a full-blown trade war with the United States and is concerned with the strength in the euro. Inflation came down and the euro continues to be strong, making for a less forceful case to remove stimulus and increase rates. After the release of the minutes on Thursday, the euro fell against the dollar.

Threats

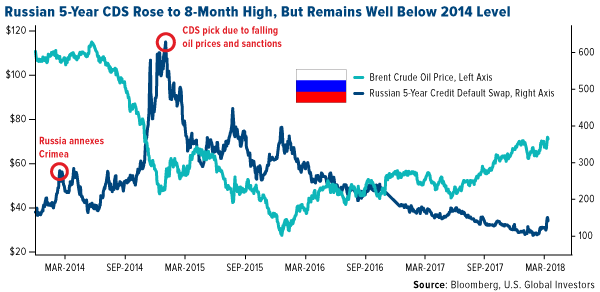

- After new sanctions were imposed on Russia last week, the Russian five-year credit default swaps spiked, but remain below March 2014 levels, when Russia annexed Crimea. The chart below shows that the sharp move in Russian credit default swaps at the end of 2014 was due to abruptly falling oil prices. This year, oil prices are moving higher, supporting the Russian economy. Nevertheless, the threat of U.S. imposing more sanctions on Russia still exists.

- Industrial output in the euro area unexpectedly fell for a third straight month in February. Month-over-month production slipped 0.8 percent, weighed down by activity in Germany and Italy. Momentum has slowed at the start of the year, after GDP growth in 2017 was the fastest in a decade.

- War in Syria is a focus of discussion and geopolitical tension. France claims that western governments have “proof” that a chemical weapon was used in the Syrian city of Douma last week and that it was deployed by the Syrian government. Meanwhile, Russia’s Foreign Minister Sergey Lavrov on Friday claimed his government possesses “irrefutable data” that the chemical attack was “staged” with the help of a foreign intelligence service. Markets may react negatively if there is a wider military escalation in Syria.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits