Throughout 2017, fiscal and monetary policy continued on a steady path. Janet Yellen remained in charge of the Federal Reserve, and no significant economic legislation was passed until the end of the year. With the passage of the Tax Cuts and Jobs Act, the installation of Jerome Powell as chair of the Federal Reserve board of governors, and a spending resolution that loosened government expenditures, we have entered a new era.

Tariff pronouncements and retaliations have dominated the financial press coverage in the past month. The Section 232 (steel and aluminum) tariffs went into effect with a host of trading partners exempted. The Section 301 tariffs, targeting China specifically, remain in negotiation, with new headlines breaking almost daily. It is far too soon to anticipate how these dynamics will impact the U.S. outlook, but they have introduced additional uncertainty to the forecast.

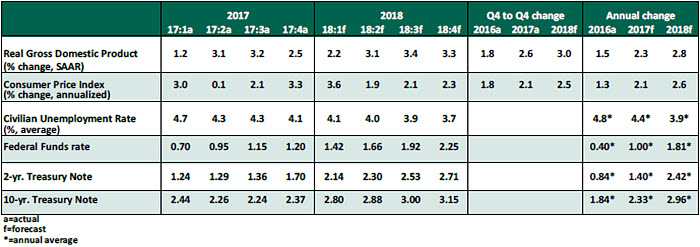

Key Economic Indicators

Influences on the Forecast

- The March payrolls report showed employment rising by only 103,000 jobs, well below expectations. However, the February estimate was revised to 326,000 jobs created. This measure can be volatile, and the three-month average of 202,000 jobs remains very healthy. Unemployment remained steady at 4.1%, as more workers re-entered the labor force.

Wage gains moved up only modestly, but the strength in employment bodes well for consumer spending during the balance of the year.

- Purchasing Managers’ Index values remained elevated. Though they have fallen from recent high levels, they reflect a manufacturing sector that continues to perform well. The report included another very high reading of 78.1 for the inputs factor, reflecting higher raw materials prices. This could be the first indication of price increases due to tariff actions, but may also simply reflect the recent growth of energy costs.

- In its final revision, real gross domestic product (GDP) for the fourth quarter of 2017 moved upward to a 2.9% annualized pace. The increase was primarily driven by an upgrade to final sales, reflecting the continued strength of consumer spending. Low inventory growth and the growing trade deficit continued to weigh on GDP.

- Early estimates for first quarter economic growth suggest a soft start to the year. We expect this is largely a seasonal impact, as the northeast was battered by harsh weather. Also, consumers in areas affected by storms in 2017 spent heavily late last year to rebuild (this was especially evident in auto sales data) and are now taking a pause.

- Early surveys of the Tax Cuts and Jobs Act’s influence paint a picture of uneven benefits. Dividends and share repurchases are climbing as a large share of proceeds are paid to shareholders. Equity owners have thus seen the most benefit from tax reform, but the gains have not demonstrably flowed economic participants who do not own shares.

- The risk of a government shutdown briefly re-emerged before being put to bed for several years, as Congress passed and the president ratified a new spending framework. The increase in spending caps is set to expire in 2020, but few think federal spending will be reduced in an election year.

- Personal income grew by 0.4% and nominal spending by 0.2% in February, both in line with expectations. The core personal consumption expenditures deflator rose to 1.6% year-over-year, approaching but stubbornly remaining under the Fed’s 2% inflation target.

Nonetheless, the immense fiscal expansion passed by Congress will lead the economy to grow well above its potential rate for the balance of 2018. For that reason, inflation is expected to rise steadily in the coming months.

- To little surprise, the Federal Open Market Committee voted to increase the federal funds target rate range by 25 basis points last month. Short-term interest rates rose accordingly. Meanwhile, trade tensions prompted some movement of capital out of equities and into fixed income, which lowered long-term yields.

With inflation expected to increase during the balance of 2018, we continue to expect three additional rate increases this year from the Federal Reserve, and we expect the 10-year U.S. Treasury yield to exceed 3% by year-end.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2018 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust