Commodities Are Flashing a Once-in-a-Generation Buy Signal

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Since the commodities supercycle unwound nearly 10 years ago, many investors have been waiting for the right conditions to trigger mean reversion and lift prices. I believe those conditions are either firmly in place right now or, at the very least, in their early stages. Among them are factors I’ve discussed at length elsewhere—a weaker U.S. dollar, a steadily flattening yield curve, heightened market volatility, overvalued stocks, expectations of higher inflation, trade war jitters, geopolitical risks and more.

In addition, nearly 60 percent of money managers surveyed by Bank of America Merrill Lynch believe 2018 could be the peak year for stocks. A recent J.P. Morgan survey found that three quarters of ultra-high net worth individuals forecast a U.S. recession in the next two years.

All of this makes the investment case for commodities, gold and energy more compelling than at any other time in recent memory.

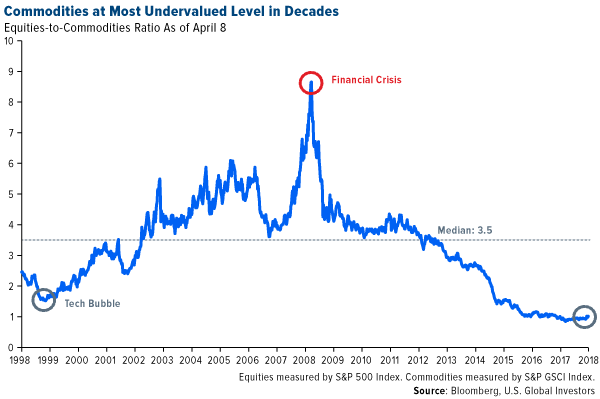

Exhibit A is the chart below, which I’ve shared before but recently updated with new data. Relative to equities, commodities are as cheap right now as they’ve been in decades. This is literally a once-in-a-generation opportunity that investors with a long-term view should seriously consider. For perspective, had you invested in a fund tracking the S&P GSCI or an equivalent commodities index in 2000, you would have seen a compound annual growth rate (CAGR) of around 10 percent for the next 10 years, according to Bloomberg data.

We all know that past performance is no guarantee of future results, but it’s doubtful you’re going to get a clearer or resounding signal that now could be an ideal time to add to your commodities exposure. If you feel as if you’ve been stuck at a traffic light these past few years, just waiting to put your foot on the accelerator, you can breathe a sigh of relief because the light may have just turned green.

Goldman: Time to Overweight Commodities

|

|

I'm not alone in my bullishness. In a note this week, analysts at Goldman Sachs write that “the strategic case for owning commodities has rarely been stronger.” The bank recommends an overweight position, estimating that commodities will yield at least 10 percent over the next 12 months, with most of the gains being made by crude oil and aluminum.

Whereas crude traders are responding primarily to concerns that output could be disrupted by intensifying conflict in the Middle East, specifically oil producer Syria, aluminum prices have skyrocketed following the imposition of fresh U.S. sanctions against a number of Russian firms. Among them is United Company RUSAL, the world’s second-largest aluminum company, responsible for producing as much as 6 percent of global supply.

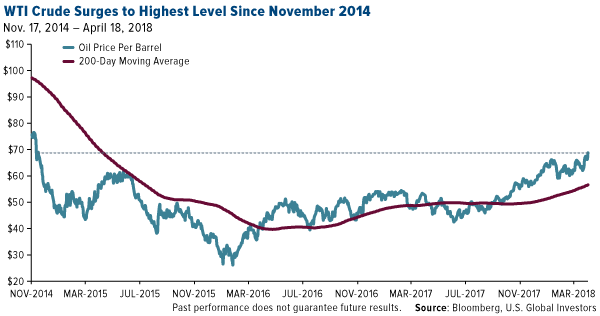

WTI Testing $70 Resistance

Since its low of $26 per barrel in February 2016, the price of West Texas Intermediate (WTI) crude has surged nearly fivefold and is currently at its highest level in more than three years. On Wednesday, oil jumped nearly 3 percent on reports that U.S. inventories had fallen more than expected, suggesting the global glut continues to recede. Yesterday, WTI tested resistance at $70, a level we haven’t seen since November 2014.

But prices retreated again today after President Donald Trump blasted OPEC on Twitter, proving once again how quants comb through social media at lightning speed and use sentiment analysis to inform their trades. “With record amounts of Oil all over the place, including the fully loaded ships at sea, Oil prices are artificially Very High! No good and will not be accepted!” the president said.

As I shared with you earlier this month, OPEC and Russia are planning to work more closely together to limit output for a number of years, possibly as many as 10 or 20. Such an agreement would help support oil prices—Saudi Arabia in particular seeks higher prices to take Saudi Aramco, the world’s largest energy company, public—but it’s likely American shale producers would ramp up production to fill the void. The U.S. is now the number two oil producer in the world, having overtaken Saudi Arabia late last year.

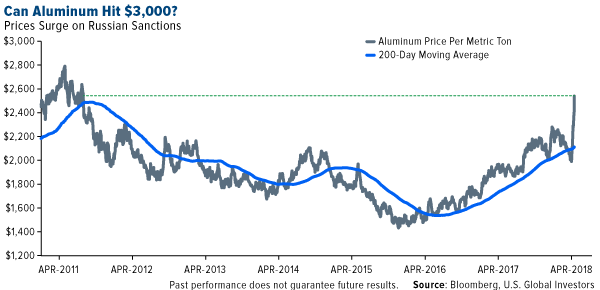

Will We See $3,000 Aluminum?

Aluminum is likewise enjoying a strong rally, jumping sharply more than 23 percent since the White House announced sanctions against select Russian firms and oligarchs in response to the Eastern European country’s alleged interference during the 2016 presidential election. In nine of the past 11 trading days through yesterday, the metal posted positive gains, surging nearly 6 percent on Wednesday alone.

Aluminum soared to $2,715 per metric ton in intraday trading yesterday, the highest we’ve seen since April 2011. The rally may have further to run, writes Goldman Sachs, which forecasts a price range of between $2,800 and $3,000 this year.

Australian-British multinational Rio Tinto and Melbourne-based BHP, two of the world’s top aluminum producers, were both upgraded to “BUY” this week by CLSA, partly in response to rising aluminum prices but also because they maintain strong balance sheets and are expected to generate favorable free cash flow (FCF) this year.

China’s One Belt, One Road Still Needs Biblical Amounts of Materials

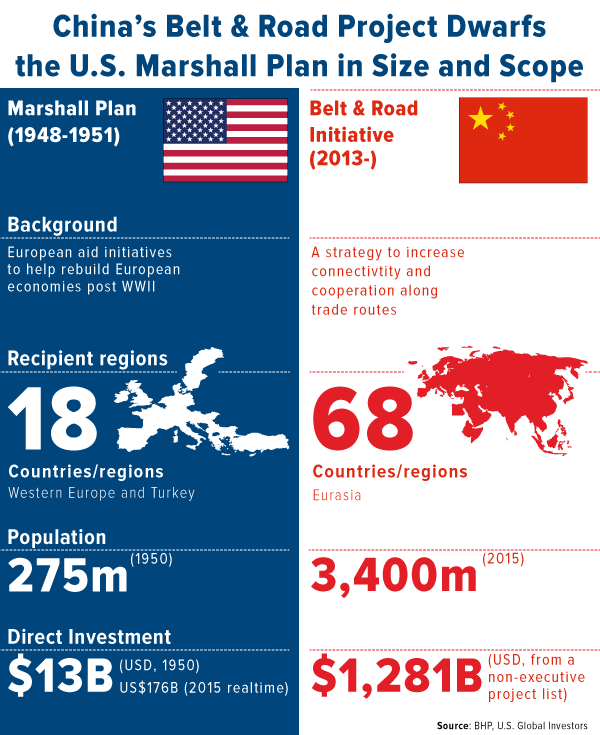

Also bolstering the commodities investment story is China’s massive ongoing “Belt and Road” megaproject, also known as the Silk Road Economic Belt. In a note this week, CLSA reminds us that the infrastructure initiative is still in its infancy, expected to be completed by 2049. It will cut through as many as 68 countries across Asia and Europe, affecting an estimated 62 percent of the world’s population. China has already spent approximately $180 billion to complete various projects, but many billions more will go toward building roads, ports, dams, high-speed rail, airports and more—all to “enhance regional connectivity,” as President Xi Jinping put it, and strengthen China’s economic clout.

To give you some scale as to how monumental and historic this undertaking truly is, the graphic below, courtesy of BHP, compares the development to the U.S. Marshall Plan, then one of the most expensive projects in human history. The Belt and Road initiative could eventually cost 12 times as much or more, with total spending estimates ranging between $4 trillion and $8 trillion.

Estimates of how much energy and natural resources will be needed during the development phase vary wildly, but I think it’s fair to assume that demand will continue to be supported for some time.

Gold Investors

Gold ended the week down slightly, the first time in three weeks it’s done so. It looks as if gold investors took some profits late in the week after the yellow metal came close to breaching $1,360 on Wednesday.

I still believe gold could hit $1,500 an ounce this year on rising consumer and producer prices, which I think are understated. This is more than apparent when you compare the official U.S. consumer price index (CPI) and alternative measures such as the New York Fed’s Underlying Inflation Gauge (UIG). And as Dr. Ed Yardeni points out in a recent blog post, the word “inflation” appeared as many as 106 times during the latest Federal Open Market Committee (FOMC) meeting, a sign that Fed members could be getting more and more concerned about mounting inflationary pressures.

Recent reports also suggest gold production is slowing, which could help support prices long-term. Exploration budgets have been declining pretty steadily since 2012, after the price of gold peaked, and fewer and fewer large-deposit mines are being discovered.

This week the China Gold Association announced that the country, the largest producer of gold, produced 98 million metric tons in the March quarter, down some 3 percent from the same period last year. This comes after total Chinese output in 2017 fell 6 percent year-over-year to 426 million tons. Granted, miners have been pressured by Beijing to curtail production as part of the government’s enforcement of tougher environmental protection policies, but the decline in output is part of a downward trend we’re seeing across the board, especially among major producers.

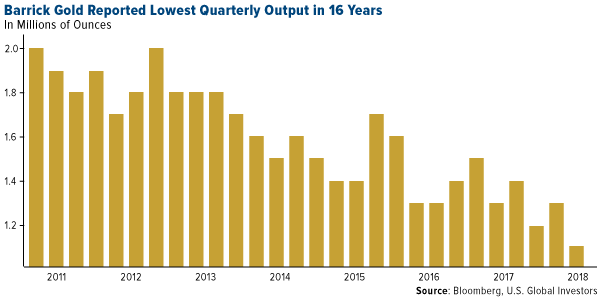

Take a look at the declining quarterly output of Barrick Gold, the world’s largest gold miner. According to its preliminary results for the first quarter, Barrick produced a total of 1.05 million ounces from its 10 projects. That’s only a 2 percent decrease from the same quarter last year, but a far cry from where it was seven years ago.

Since the news hit April 11, Barrick is up about 3 percent, even after a Friday selloff.

While some investors might view the lower output as disappointing, others no doubt see it as a reminder that gold is a finite resource, one of the many reasons why it’s remained so highly valued for centuries. As I’ve written before, the low-hanging fruit has likely already been picked, making the task of mining the yellow metal more difficult as well as expensive. Supply isn’t growing nearly as fast as it once did.

And yet demand continues to climb. Not only do the peoples of India, China, Turkey and other countries have a strong cultural affinity to gold—an obsession that will only intensify as incomes rise—but the metal still plays a vital role as a portfolio diversifier in times of economic and political uncertainty.

Franco-Nevada IPO at 10

|

|

On a final note, Franco-Nevada, one of our favorite players in the gold space, recently celebrated its 10- year anniversary as a publically-traded company. As if to commemorate the occasion, the company reported record sales and profit in 2017, not to mention a record $167.9 million in dividends paid—all while staying debt-free.

“I am pleased that Franco-Nevada’s 10th full year since its IPO was its best year ever,” commented CEO David Harquail.

I’d like to congratulate my good friends Seymour Schulich and Pierre Lassonde, who conceived of the gold royalty model and cofounded the company back in 1983. (As I’ve explained before, Franco-Nevada was the first IPO I worked on as a young analyst in Toronto.) Seymour and Pierre are true rock stars in the world of gold mining, and what they’ve managed to achieve is nothing short of legendary.

Read more about Franco-Nevada’s record year by clicking here!

April 20, 2018These Two Funds Offer an Attractive Risk/Reward Profile |

April 18, 2018The Texas Economy Trumps That of Russia |

April 16, 2018Which Has the Bigger Economy: Texas or Russia? |

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.42 percent. The S&P 500 Stock Index rose 0.52 percent, while the Nasdaq Composite climbed 0.56 percent. The Russell 2000 small capitalization index gained 0.94 percent this week.

- The Hang Seng Composite lost 1.82 percent this week; while Taiwan was down 1.70 percent and the KOSPI rose 0.87 percent.

- The 10-year Treasury bond yield rose 12 basis points to 2.96 percent.

Domestic Equity Market

Strengths

- Energy was the best performing sector of the week, increasing by 2.60 percent versus an overall increase of 0.34 percent for the S&P 500.

- Textron was the best performing stock for the week, increasing 12.08 percent.

- Netflix matched Wall Street estimates on both the top and bottom lines and crushed subscriber growth targets, announcing it added 7.41 million subscribers — a first-quarter record.

Weaknesses

- Consumer staples was the worst performing sector for the week, decreasing by 4.36 percent versus an overall increase of 0.34 percent for the S&P 500.

- Philip Morris International was the worst performing stock for the week, falling 17.26 percent

- As part of its effort to reduce spending by $1 billion, Qualcomm announced it will lay off 1,500 employees across its San Diego and Bay Area locations, according to WARN filings with the state of California.

Opportunities

- Stock bulls seem to have the upper hand as the month of April unfolds. The S&P 500 has turned positive for the year and historically stands a good chance of posting gains this month. Since 2007, the only time the benchmark gauge has closed out April with a loss was in 2012.

- Facebook announced it is working on its own chips, according to Bloomberg. The move would reduce its reliance on companies like Intel, and the company could use chips for hardware devices, artificial intelligence, or the servers in its data centers.

- Goldman Sachs bought a personal finance app called Clarity Money to bolster its Marcus online lending business, Reuter’s reports citing a Goldman release. Terms were not disclosed.

Threats

- Investors should be prepared for more volatility as overstretched markets adapt to the end of easy central-bank money, according to the head of the IMF’s capital-markets department. The sharp selloff earlier this year in the stock market was a "fairly isolated" event that involved the unwinding of bets that low volatility would continue, the IMF’s Tobias Adrian said in an interview. Nonetheless, markets will likely face more choppy waters ahead, Adrian said.

- Tesla temporarily shut down its Model 3 assembly line for the second time since February as part of efforts to "improve automation and systematically address bottlenecks" in the production of its vehicle for the masses. Traders are paying close to the highest premium on record to protect against a 10 percent decline in Tesla's stock over the next month, relative to bets on a 10 percent gain.

- The U.S. Consumer Financial Protection Bureau and the Office of the Comptroller of the Currency proposed that Wells Fargo pay a $1 billion penalty to resolve investigations into auto-insurance and mortgage-lending abuses, Reuters said.

April 19, 2018Will Inflation Boost Gold to $1,500? |

April 17, 2018How to Play Gold in an Uptrend |

March 27, 2018The Gold Price Will Continue to Rise, Says Frank Holmes |

The Economy and Bond Market

Strengths

- Retail sales in the U.S. rose a better-than-expected 0.6 percent in March for the first advance in four months, suggesting tax cuts and refunds may be having a positive impact on spending, according to a Commerce Department report on Monday. The improvement in demand went beyond a bump in automobile sales, as consumers went shopping at furniture and home stores along with electronics and appliance sellers.

- U.S. homebuilding increased more than expected in March amid a rebound in the construction of multi-family housing units. Housing starts rose 1.9 percent to a seasonally adjusted annual rate of 1.32 million units, the Commerce Department said on Tuesday. Economists polled by Reuters had forecast housing starts rising to a pace of 1.26 million units last month.

- While U.S. factory production may have cooled in March from the previous month, a look at year-over-year gains tells a different story. Output increased 3 percent from March 2017, the biggest annual gain since June 2012. The boost in manufacturing comes as fiscal stimulus provides support for increased business investment, while improving global economies and a weaker dollar help underpin U.S. exports.

Weaknesses

- Confidence gauges spanning small businesses, factories and the public at large are coming off the boil as U.S. tariffs on imported metals, along with threats and counter threats over Chinese goods, roil the stock market and cast a cloud over what was otherwise a bright economic outlook. The latest indications of concern came on Thursday in the Federal Reserve Bank of Philadelphia’s regional manufacturing survey, whose index of business activity six months from now dropped to the lowest level since July. Earlier in the week, a similar gauge for New York State registered the steepest one-month drop since the September 11 terrorist attacks.

- High rates of debt in the U.S. have made the economy much more sensitive to interest-rate increases, Dallas President Robert Kaplan wrote in an essay. The Dallas Fed expects U.S. GDP growth of 2.5 percent to 2.75 percent in 2018, but less than 2 percent in 2020 as short-term stimulus fades. Kaplan wrote that due to a high level of government debt "as well as historically high levels of corporate debt as a percentage of GDP, the economy is becoming much more interest rate sensitive."

- Connecticut’s debt keeps rising, and so does the penalty it pays in the bond market. The state was downgraded last Friday by S&P Global Ratings for the third time in as many years, pushing its bonds down one step to A, the fifth-lowest investment grade rank. The company cited Connecticut’s mounting obligations, which will only increase as a result of its decision to cover $540 million of debts for its distressed capital city, Hartford, to keep it from collapsing into bankruptcy. The extra yield that investors demand on 10-year Connecticut General Obligation bonds rose to about 91 basis points, up from around 60 basis points last May, before it widened in the wake of the state’s last downgrade, according to Bloomberg indices. Connecticut spreads are the second-highest among the states tracked by Bloomberg, with only Illinois paying more. S&P said it cut the rating because of an increase in Connecticut’s debt, which it said is “not likely" to shrink anytime soon.

Opportunities

- The Conference Board Leading Economic Index rose 0.3 percent to 109, following increases in the index in January and February. “The LEI points to robust economic growth throughout 2018,” said Ataman Ozyildirim, director of business cycles and growth research at the Conference Board. “While the Federal Reserve is on track to continue raising its benchmark rate for the rest of the year, the recent weakness in residential construction and stock prices—important leading indicators—should be monitored closely.” While the index’s rise in March was slower than in previous months, “its six-month growth rate increased further and points to continued solid growth in the U.S. economy for the rest of the year,” Mr. Ozyildirim said.

- Volatility in the Treasuries market is subdued, according to Bank of America Merrill Lynch’s MOVE Index. The measure of anticipated price swings in U.S. bonds dropped below 50 on Monday for the first time in three months, putting it closer now to its record low of about 44, than to its high for the year of about 72 in early February. The decline may suggest traders increasingly doubt the Federal Reserve will follow through on its plan to raise interest rates at least two more time this year, writes The Daily Prophet’s Robert Burgess. A lower pace of rate hikes could help lift bond returns.

- Investors should consider adding to their municipal bond holdings during "modest pockets of underperformance” in the coming months before the summer doldrums, Matthew Gastall, executive director of Morgan Stanley Wealth Management said in an e-mailed note on Wednesday. The outlook is "bright” in the short-term for munis, he continued.

Threats

- Only two months ago, the prospect of 10-year Treasury yields reaching 3 percent was an almost certainty after a relentless climb from 2.4 percent at the start of the year. But a retreat ensued, sending them as low as 2.72 percent in early April, only to reverse course again this week. The 10-year yield breached 2.9 percent on Thursday, the highest in eight weeks.

- Fed Governor Lael Brainard warned against dismantling banking regulations designed after the financial crisis, as she identified growing threats to financial stability in the U.S. economy. While calling recent economic gains "heartening," she said tax cuts and new spending represented a rare case of pro-cyclical fiscal stimulus that could heighten risks of inflation or financial imbalances. In that environment, she cautioned against rolling back regulatory safeguards.

- In five years, the U.S. government is forecast to have a worse debt profile than Italy, the perennial poor man of the G-7 industrial nations. The U.S. debt-to-GDP ratio is projected to widen to 116.9 percent by 2023 while Italy is seen narrowing to 116.6 percent, according to the latest data from the IMF. The U.S. will also place ahead of both Mozambique and Burundi in terms of the weight of its fiscal burden.

Gold Market

This week spot gold closed at $1,336.37, down $9.05 per ounce, or 0.67 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.34 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index came in up 1.13 percent. The U.S. Trade-Weighted Dollar reversed course this week and rose 0.58 percent following last week’s loss.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Apr-16 | China Retail Sales YoY | 9.7% | 10.1% | 9.4% |

| Apr-17 | Germany ZEW Survey Current Situation | 88.0 | 87.9 | 90.7 |

| Apr-17 | Germany ZEW Survey Expectations | -1.0 | -8.2 | 5.1 |

| Apr-17 | Housing Starts | 1267k | 1319k | 1295k |

| Apr-18 | Eurozone CPI Core YoY | 1.0% | 1.0% | 1.0% |

| Apr-19 | Initial Jobless Claims | 230k | 232k | 233k |

| Apr-24 | New Home Sales | 63k | -- | 618k |

| Apr-24 | Conf. Board Consumer Confidence | 126.0 | -- | 127.7 |

| Apr-26 | Hong Kong Exports YoY | 3.1% | -- | 1.7% |

| Apr-26 | ECB Main Refinancing Rate | 0.00% | -- | 0.00% |

| Apr-26 | Initial Jobless Claims | 230k | -- | 232k |

| Apr-26 | Durable Goods Orders | 1.1% | -- | 3.0% |

| Apr-27 | GDP Annualized QoQ | 2.0% | -- | 2.9% |

Strengths

- The best performing metal this week was palladium, up 4.23 percent on worries over supply issues due to sanctions on Russia. Gold traders are bullish this week on gold prices as ETF holdings backed by gold saw inflows for 12 days straight, according to Bloomberg.

- Jewelers in India, the second largest gold consuming nation in the world, expect a 10 percent rise in gold sales on key Hindu celebration day Akshaya Tritya, despite higher gold prices this year. Last year, sales of gold jewelry on the holiday were between 22 and 24 metric tons. Although bullion demand was down 5.4 percent in China in the first quarter as compared to the same time last year, demand for gold jewelry was up 5.6 percent to 180.50 tons.

- Turkey collected 1.34 tons of gold this week in a gold-based bond issuance, according to state-run Anadolu Agency. The Turkish Central Bank also transferred approximately 220 tons of its gold reserves stored in the U.S. Federal Reserve System back to Turkey yesterday. Two other banks are in the process of transferring 95 tons of gold reserves from the U.S. over to Turkey.

Weaknesses

- The worst performing metal this week was gold, down 0.70 percent on a slightly stronger dollar this week. Although bullion saw big inflows this week, the VanEck Vector Gold Miners ETF saw investors withdraw $132.8 million from the fund, reducing assets by 1.6 percent, reports Bloomberg. This was the fifth-straight day of outflows totaling $373.5 million. The Empire Fed survey was weaker than expected with the “future” component of the survey dropping from 44.1 to 18.3 on bearish trade sentiment.

- This week China’s holdings of U.S. Treasuries grew to the most in six months by $8.5 billion to $1.18 trillion in February, reports Bloomberg. China remains the largest creditor of the U.S., followed by Japan. Speculation is growing that China is increasing its holdings in order to use it as a bargaining chip in trade negotiations with the U.S.

- Just two weeks after launching, the Secured Overnight Financing Rate (SOFR), which was meant to replace Libor, has hit some bumps. The Federal Reserve Bank of New York said that it mistakenly included certain transactions in the settings for 10 days and will not be revising the incorrect data. Bloomberg writes that SOFR is a rate based on overnight loans collateralized by U.S. Treasuries.

Opportunities

- Several fund managers and prominent investors recommended this week to invest in gold. Kotak Mutual Fund said that investors should allocate to gold as a “risk cover” amid expected higher volatility. Fritz Folts, chief investment strategist and managing partner at 3EDGE Asset Management, said that “We will definitely have more volatility this year. And gold can help us there.” Bloomberg writes that hedge fund manager Said Haidar predicts that the U.S. economy growth will not benefit the U.S. dollar, which is potentially good for gold. The S&P Global Ratings recently took three positive rating actions in the gold sector, upgrading a few big gold companies to stable from negative. This is a very positive sign to investors that gold companies are becoming more investable.

- The U.S. dollar will potentially continue to weaken, due to a tweet from President Trump saying that Russia and China are “playing the currency devaluation game.” In Bloomberg View, Robert Burgess writes that the U.S. relies on foreign debt to finance the deficit and if investors believe that the dollar will weaken, they might be less likely to buy debt. Some argue that the current administration wants a weaker dollar, as Viraj Patel, a currency strategist at ING Groep NV, said on Monday that the president’s comments are “another implicit signal of the administration’s desire for a weaker U.S. dollar – especially against major trading partners.”

- According to Bloomberg, Trump administration officials are looking into using a Cold War era defense act to help keep struggling coal and nuclear power plants open. The Defense Production Act, allows the president to effectively nationalize a private industry to ensure the nation has resources that could be needed during a war or after a disaster. This Act was last used in 2001 to keep natural gas flowing to California to avoid blackouts.

Threats

- Morgan Stanley said this week that investors might need to prepare for a downside as the end of the current economic cycle is near and U.S. markets are overpriced. Hedge funds saw two consecutive months of sinking returns, the first back-to-back loss since early 2016. Investors are claiming that the VIX, or the CBOE Volatility Index, is rigged, reports Bloomberg. On Wednesday the index spiked as much as 11 percent in an hour. More speculation arose when a trade of 13,923 puts on the S&P 500 took place just before opening, when the previous daily trading volume never exceeded 75 contracts.

- In a bleak outlook, the U.S. debt-to-GDP ratio is projected to grow higher than that of Italy by 2023 to 116.9 percent, according to data from the International Monetary Fund. These figures are renewing the focus on a deteriorating budget after the passage of $1.5 trillion in tax cuts. World debt has also grown to a record amount of $164 trillion, which could make it more difficult for countries to respond to recessions or refinance debts.

- The Treasury yield curve from five to 30 years flattened on Wednesday to just 29 basis points, the narrowest spread since 2007, writes Bloomberg. According to St. Louis Fed President James Bullard, the central bankers should debate the yield curve now and he believes that it could invert within six months, which would be an ominous sign for growth.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended April 20 was GPU Coin, which gained 711.73 percent. Seeking Alpha notes that after putting in a loud rally late last week, bitcoin this week has “quietly continued to creep upward.” On a percentage basis, other coins like Ether and Litecoin are making even larger moves.

- According to BitcoinMagazine.com, Coinbase is acquiring Earn.com, a “social network that allows users to earn digital currency by replying to emails and completing small tasks online.” Coinbase also announced that Earn.com’s co-founder and CEO Balaji Srinivasan will be its first chief technology officer. Earn.com is Coinbase’s fifth acquisition.

- Although it is the risk and volatility of cryptocurrencies that attract speculators, one group of Silicon Valley venture capitalists and Wall St. fixtures are investing in a digital currency that is “boring” by design, reports Bloomberg. The concept is called Basis and co-founder Nader Al-Naji says it is designed to be a cryptocurrency, but “without the volatility that we believe has prevented popular adoption to date.” Billionaire hedge fund manager Stanley Druckenmiller and Kevin Warsh, former governor of the U.S. Federal Reserve, have already bought in.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended April 20 was WCOIN, which lost 27.69 percent.

- Kraken, a U.S.-based cryptocurrency exchange, is ending its trading services for Japanese residents, writes the Wall Street Journal. The move comes as regulators step up oversight in the country, which is one of the world’s biggest bitcoin-trading hubs. According to the company, it is looking to focus in other countries, but could resume services in Japan at a later time, the article continues.

- Absent of any identified catalysts, bitcoin fell suddenly on Tuesday, putting the price on pace to finish lower for the first time in seven days, reports Bloomberg. The drop was around 1.6 percent, the biggest intraday decline since April 12. Perhaps bitcoin bulls are getting nervous, reasons the article.

Opportunities

- Samsung, the world’s biggest maker of smartphones and semiconductors, is looking at blockchain technology to manage its vast global supply network, reports Bloomberg. According to Song Kwang-woo, the blockchain chief at the group’s logistical and information and technology arm (Samsung SDS Co.), using a blockchain ledger system could cut shipping costs by 20 percent and would help keep track of global shipments worth tens of billions of dollars a year.

- Barclays Plc might be “banking on bitcoin” pretty soon, reports Bloomberg. The British bank has been gauging clients’ interest in the possibility of starting a cryptocurrency trading desk. This move would put Barclays in the same position as Goldman Sachs Group, in “pioneering a new business on Wall Street,” the article continues.

- According to a Bloomberg headline this week, “Blockchain Is About to Revolutionize the Shipping Industry.” Although robot-operated ports and vast computer databases track cargoes currently, the shipping industry still relies on millions and millions of paper documents. Container and shipping lines have teamed up with technology companies to upgrade the world’s most complex logistics network, using the adoption of blockchain. “Should they succeed, documentation that takes days will eventually be done in minutes, much of it without the need for human input,” the article continues.

Threats

- New York Attorney General Eric Schneiderman said in a press statement on Tuesday, that 13 cryptocurrency trading platforms, including Coinbase, will be questioned about their operations, reports BNN. Information about fee structures and safety measures to protect customer accounts will be sought. According to the article, trading platforms have to respond to these inquiries before the first of May. While the news could be seen as a threat to these platforms, it is ultimately aimed at protecting consumers and investors, which is always positive.

- Wild swings in the price of bitcoin this week are leaving advocates of the cryptocurrency anxious after what’s already been a choppy week of trading, writes Bloomberg. Some investors are blaming the moves on actions by large bitcoin holders, otherwise known as “whales.” Founder and CEO of IronChain Capital, Jonathan Benassaya, believes the best explanation is coming from those whales in the market who want to have some sort of control over what’s going on. “It’s some sort of manipulation from actors,” Benassaya said.

- Wall Street analyst Richard Bernstein believes that cryptocurrencies are “no different from the coins in your favorite online game,” reports Bloomberg. In addition, the fact that these coins are tradable is what makes them a classic asset bubble, according to Bernstein. As the article continues, the presence of a bubble doesn’t mean that the economics and businesses related to cryptocurrencies aren’t viable, but “suggests that the return-on-investment could be considerably lower than investors currently expect,” Bernstein wrote.

Energy and Natural Resources Market

Strengths

- Nickel was the best performing major commodity this week rising 8.5 percent. The commodity rallied to a near three-year high as metals investors drove up the price on speculation that global supply would be damaged if Norilsk – one of the world’s biggest producers of the commodity – were to be included in the Russian sanctioned company list.

- The best performing sector this week was the S&P1500 Oil & Gas Refiners and Marketing Index. The index rose 6.6 percent after U.S. gasoline demand rose to all-time highs.

- The best performing stock for the week was Alcoa Corp. The largest U.S. alumina and aluminum products producer rose 9.2 percent after beating analyst expectations for the first quarter and raising its annual EBITDA guidance to $3.5 billion from $2.5 billion previously.

Weaknesses

- Gold was the worst performing commodity this week. The commodity dropped 0.7 percent, posting its first weekly decline in three, as easing political tensions between the U.S and Russia coupled with a strengthening dollar sapped demand for the metal as a haven.

- The worst performing sector this week was the NYSE Arca Gold Miners Index. The index dropped 0.5 percent tracking the weekly decline in gold prices.

- The worst performing stock for the week was Grupa Lotos SA. The Polish petrochemical refiner dropped 6.7 percent after the Polish government announced Lotos’ Gdansk refinery, may be carved out in a planned merger with bigger rival Orlen to allow the city of Gdansk to maintain the benefits its receives from the refinery. The Gdansk refinery is the most profitable asset within the Lotos portfolio.

Opportunities

- Gasoline demand surges to record high as spring beckons. While summer weather still seems to be light-years away for much of the U.S., drivers are showing little restraint on the road despite gas prices hitting a three-year high. Gasoline demand reached 9.9 million barrels per day, an all-time high for American consumers.

- Similarly, China’s crude processing facilities’ output rose to a record in March. Major refiners in the Asian nation increased activity after the Lunar New Year holidays, demanding greater crude oil inputs to satisfy rising demand for refined products.

- China GDP for the first quarter advanced 6.8 percent, avoiding a sequential decline. The Asian nation carried most of its strong economic momentum from last year into the first quarter of 2018, with government crackdowns on financial risks and industrial pollution dragging less on activity than earlier expected.

Threats

- Oil is starting to back up in West Texas and has recently sold at a $6 to $9 discount to crude prices elsewhere in the U.S. While production is expected to continue rising, Permian producers are starting to encounter congested pipelines and shortages of materials and workers – bottlenecks that have caused some investors to sour on producing companies operating in the region.

- U.S. President Donald Trump slammed OPEC for inflating oil prices after the cartel showed a willingness to further tighten crude markets. The crude glut that’s weighed on prices for three years has almost been wiped out by OPEC’s production cuts, but the group is looking to keep supply contained and drive inventories even lower.

- The German ZEW survey headline numbers for April showed that the headline economic sentiment numbers deteriorated more than expected, coming in at -8.2 versus -1.0 expectations and 5.1 seen last. The survey, which correlates highly with raw commodity performance, cited trade war risks as the main reason for decline.

China Region

Strengths

- The first quarter reading for year-over-year China GDP clocked in at a solid 6.8 percent, in line with analysts’ estimates and the prior print.

- China’s retail sales numbers beat estimates. Year-over-year sales for the March period came in up 10.1 percent, ahead of an anticipated 9.7 percent print.

- China’s home price gains last month were led by price advances in smaller cities, Bloomberg News reported this week, as the average increase across the 70 cities tracked each month came in at 0.42 percent. Third-tier cities saw gains of 0.94 percent. Overall, home prices climbed in 55 cities during March, up from only 44 in February.

Weaknesses

- Non-oil exports from Singapore came up short this month. Analysts expected 1.2 percent year-over-year growth for the March period; instead, exports actually declined by 2.7 percent.

- Overseas remittances to the Philippines rose only 4.5 percent for the February (most recent) period, down from the prior month’s 9.7 percent reading and below analysts’ estimates for a growth rate of 10.6 percent.

- China’s aggregate financing and new yuan loans both came in short of expectations, although both were also up from their respective February prints. New yuan loans came in at 1.120 trillion, shy of 1.175 expected, while aggregate financing came in at only 1.330 trillion, well below expectations for a 1.800 trillion showing.

Opportunities

- China’s Tencent is heading for another initial public offering (IPO), reports The Straits Times. Meilishuo, an online fashion retailer that is backed by Tencent, is in talks about a U.S. IPO to develop its e-commerce stance, the article continues.

- As Japan’s Prime Minister Shinzo Abe visited the United States this week, he apparently continued to push for expansion of the Trans-Pacific Partnership, although U.S. President Trump seems to prefer bilateral trade agreements. The fact that the TPP’s latest iteration was indeed signed into being, and endures, means it remains an opportunity—perhaps for the United States, perhaps for China or others—but definitely for the Partnership’s signatories.

- While China’s overall FAI came in at only 7.5 percent this month, it ought to be noted that China continues to see sturdy investment in “New Economy” industries and service sectors. The chart below, as reported by CLSA, helps to show this trend.

Threats

- Since 2015, China’s quarterly growth figures haven’t varied by more than 0.1 percentage point on a year-over-year basis, writes Bloomberg Businessweek. The U.S., by contrast, sees notable swings on a quarter-over-quarter basis. This begs the question: Do China’s economic numbers have a credibility problem? According to the article, the world has “long suspected that China fudges its numbers, which is why the investment community has assembled an array of alternative measures.” These include rail cargo volume, electricity use and even satellite imagery of factory sites.

- As President Trump confirmed this week that the United States has “started talking to North Korea directly” at “very high levels,” press reports later confirmed that nominee for Secretary of State Mike Pompeo had actually traveled to North Korea to meet with Kim Jong Un in late March. While everything seems to be on track and progressing for an upcoming U.S.-North Korea summit, President Trump also suggested midweek that he will walk out from any talks deemed unproductive. The upside of all this is that North Korea will almost certainly refrain from missile tests as talks (more than likely) drag on; the downside is that North Korea remains something of a wildcard, with clear potential to subject the market to headline risk.

- China announced this week that it will seek to open its automobile market, allowing foreign companies to own more than 50 percent of local ventures. The move comes as the Trump administration continues its pressure on Chinese trade issues, and, while this announcement was fairly well-telegraphed, the timeline for the changes is sooner than some analysts expected.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 4.2 percent. Greek banks continue to outperform on expectations of positive stress test results, which should be announced on May 5. Head of the IMF Christine Lagarde said that Greece’s bailout program "is expected to come to an end in August.”

- The Russian ruble was the best performing currency this week, gaining 1.5 percent against the U.S. dollar. In the absence of further sanctions along with higher oil prices, the ruble rebounded after last week’s selloff following the U.S. administration’s announcement of the toughest sanctions on Russia. Brent crude oil closed at $73.7 per barrel, gaining 1.6 percent in the past five days.

- Materials was the best performing sector among eastern European markets this week.

Weaknesses

- The Czech Republic was the worst performing country this week, losing 1.2 percent. Central European Media Enterprise Ltd., a commercial television broadcaster, and Philip Morris, a tobacco producer, recorded the two biggest losses among stocks trading on the Prague exchange. Shares of Central European Media Enterprise declined by 1.75 percent and Philip Morris lost 80 basis points.

- The Czech koruna was the worst performing currency this week, losing 60 basis points. The koruna recorded its biggest daily decline in the past five days on Friday, losing 60 basis points against the U.S. dollar; while in contrast, the dollar had its biggest daily gains.

- Information technology was the worst performing sector among eastern European markets this week.

Opportunities

- In its latest economist survey, Bloomberg results show that the European Central Bank (ECB) will take longer to lay out its plans to exit quantitative easing program (QE) as protectionist measures threaten the eurozone outlook. The ECB will meet next week, and no change is expected in policy settings.

- According to IMF data, Spain’s per capita GDP exceeded that of Italy’s in 2017. The IMF also forecast that Spain would become 7 percent richer than Italy over the next five years. By 2023, some former Soviet bloc countries, including Slovakia and the Czech Republic, are also expected to become richer than Italy on a per capita basis.

- Germany is asking the U.S. administration to exempt its country’s companies from the new, tough U.S. sanctions on Russia. Trade between Germany and Russia rose to EUR 54.4 billion last year from EUR 45 billion in 2016.German industrial giants including Siemens AG, Daimler AG and Volkswagen AG do business with entities tied to people subject to the sanctions. Europe is more closely tied to Russia than the United States is, and may be able to work with Russia under some sanction exemptions, if granted.

Threats

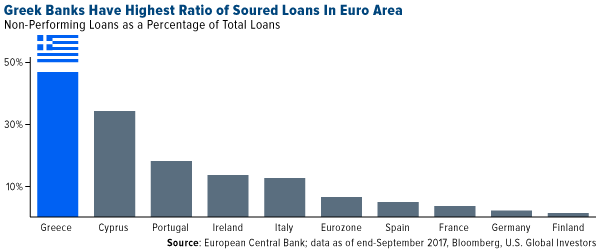

- Greek banks are recovering from recession and the biggest sovereign debt restructuring ever. After three rounds of capital injections in the past five years, banks’ balance sheets are improving, but Greek banks still have the highest ratio of bad loans in the euro area. On a positive note, incoming stress test results in May will most likely show that the four banks have sufficient capital, even under exam’s adverse scenario.

- Russian equites and the Russian ruble are recovering from last week’s selloff after the U.S. imposed a new set of sanctions against Russian companies, individuals and government officials. In the latest round of sanctions, the U.S. administration asked U.S. investors to dispose of shares and debt of publically traded aluminum producer Rusal, EN+ Group (the parent company of United Rusal) and GAZ Group (non-listed commercial vehicle producer) by May 7. According to Wood & Company, the latest set of sanctions increases the risk associated with holding Russian stocks.

- Turkey’s National Security Council advised to extend the state of emergency for another three months. President Erdogan called for a snap election on June 24. Turkey is moving from a parliamentary system to an executive presidency. Erdogan is expected to win the majority in the first round of elections, and under the new system, he will prepare the budget, dissolve parliament and appoint high- level officials, including ministers as well as some top judges. Investors may see more volatility in the next few months.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits