Call it the news of the year, perhaps even of the decade. For the first time since the Korean Peninsula was divided in 1948, leaders of the two warring nations met late last week in what had the look and feel of a jovial reconciliation between two estranged family members. Kim Jong-un of North Korea and President Moon Kae-in of South Korea made a number of important, though tentative, breakthroughs, including an agreement to denuclearize the peninsula and a pledge to revisit several infrastructure projects that would help bring some economic unity to the two Koreas.

Which the North desperately needs, as anyone reading this knows.

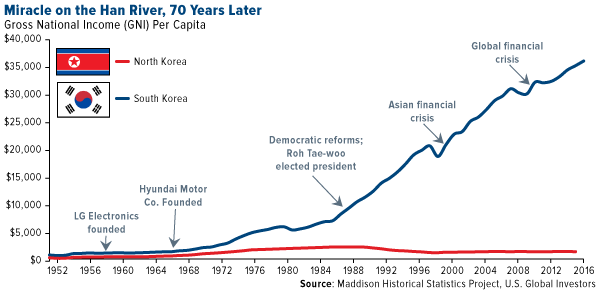

Below is economic development, as measured in gross national income (GNI) per capita, for the two nations since division. The chart looks not unlike the one I shared comparing Cuba and Singapore since their founding in 1959.

click to enlarge

Thanks to rapid growth spurred early on by business-friendly policies, South Korea is today the fourth largest economy in Asia—following China, Japan and India—and the 11th largest in the world. Most of its citizens enjoy a comfortable, middle-income lifestyle and can afford to own many of the popular consumer goods and vehicles manufactured by Samsung, LG, Hyundai and other Korean household name brands.

North Korea, on the other hand, has not advanced in any material way and today has an economy roughly 30 times smaller than its southern neighbor. Its inhabitants routinely suffer great hardship, from famines to a lack of adequate health care.

For now, many analysts are skeptical that this new development will have a huge impact on the surrounding Asian region—in the near term, at least—since North Korea’s economy is small and lacks the infrastructure necessary for rapid expansion. It’s unlikely we’ll see the sort of boom Vietnam experienced after opening its economy up to foreign direct investment (FDI) in the late 1980s. It’s just as unlikely we’ll see unification anytime soon, as that would require the presiding Kim to end the dynasty that began with his grandfather Il-sung.

Nevertheless, all good things must begin somehow, and this is as good a beginning as I can imagine.

Take our quiz and see how well you know North and South Korea!

South Korea Expected to Lead in Dividend Growth

Investors also seem to be taking in the news with a side of skepticism. The Korea Composite Stock Price Index (KOSPI) advanced a little under 3 percent in the three trading sessions following the summit, but since then it’s pared all of those gains.

South Korea is very attractive right now, with stocks trading at cheap valuation multiples relative to those in neighboring countries. Gross domestic product (GDP) growth remains robust, rising 2.8 percent in the first quarter.

The Korean market has a reputation for having a low payout ratio, despite many of its multinationals being flush with cash, but that looks set to change. Pressured by the government to do more to attract and keep foreign investors, the countries’ top 10 firms paid out a record 7 trillion won, or $6.46 billion, to offshore investors last year. Samsung Group ranked first, its payouts rising a massive 45.6 from the previous year to total 3.91 trillion won.

According to CLSA estimates, based on FactSet data, Korea tops the list for dividend growth this year and next. The investment bank is looking for a 20 percent compound annual growth rate (CAGR), which would be a huge improvement over other markets around the globe.

click to enlarge

Will Korea Become the First Cashless Society?

Recently I asked the question: “How long till bitcoin replaces cold hard cash?” The answer is: Sooner than you might think, though I’m using “bitcoin” here as a proxy for all digital currencies.

Cointelegraph reports that the Bank of Korea (BOK) announced that it’s looking into using blockchain technology and cryptocurrencies for all transactions. Such a move, according to the bank, would improve customer convenience and eliminate the cost of producing physical bills and coins.

The BOK has already set up an organization to research digital currencies and the possible ramifications of transitioning to a completely cashless society—something the Korean government has had its eye on since at least 2016.

Adoption is happening much faster than expected. Last month, the country’s leading crypto exchange, Bithumb, and Korea Pay Services, a mobile payment service provider, said they would work together to make crypto transactions available at thousands of stores and outlets.

According to the Korea Times, virtual currency payments will be made available at as many as 6,000 store locations across the country in the first half of 2018. By the end of the year, 2,000 more locations will come online.

Chinese Equities Have Outperformed Since 2001

Morningstar reports that, from March 2001 to March 2018, China stocks had the strongest annualized growth among global markets. Over the 17-year period, the MSCI China Index delivered an amazing 12.2 percent in annualized total returns, compared to the MSCI Emerging Markets Index with 10.7 percent and the MSCI World Index with 6 percent.

click to enlarge

What I find incredible is that, when the MSCI Emerging Markets Index was created in January 1988, China wasn’t even included. Today, the Asian giant has the heaviest weighting, representing nearly 30 percent of the index.

But the emerging markets index is changing yet again. Until now, the MSCI included only Chinese stocks that are traded on foreign exchanges—Hong Kong or New York, for instance. Starting June 1, domestic, Shanghai-listed Chinese stocks, known as A-shares, will be added for the first time ever. This will give foreign investors greater, and unprecedented, exposure to the world’s second-largest equities market.

The timing couldn’t have been better, as a huge number of Chinese unicorns—private firms with valuations exceeding $1 billion—are expected to raise capital this year through initial public offerings (IPOs), in Shanghai and elsewhere.

According to the Wall Street Journal, around a dozen Chinese companies, with a collective valuation of $500 billion, have been working with banks and investors to roll out an estimated $50 billion in new shares. Of those, the largest by far is smartphone-maker Xiaomi, which is expected to raise at least $10 billion in Hong Kong, the most ever for the exchange.

Manufacturing in China expanded again in April, posting either a 51.4 or 51.1, depending on which source you trust more—the Chinese government or financial media outlet Caixin.

click to enlarge

Click here to explore opportunities in the fast-growing China region!

The Month of May Has Been a Great Time to Buy Gold

On a final note, May is here, and that means we could see yet another excellent gold buying opportunity. In the chart below, you can see the yellow metal’s average monthly returns for the 30-year period and 10-year period. Although there are noticeable differences, in both cases, May was a great entry point ahead of the late summer rally in anticipation of Diwali and the Indian wedding season, when gifts of gold jewelry are considered auspicious.

click to enlarge

During this May in particular, the price of gold has been feeling the pressure of a stronger U.S. dollar, currently at a 2018 high, and rising Treasury yields.

But as I said in a recent Frank Talk, there are a number of reasons why you might want to consider adding gold stocks to your portfolio, including faster inflation and shrinking supply.

Learn all the reasons why gold stocks look attractive right now by clicking here!

Gold Market

This week spot gold closed at $1,315.35, down $8.00 per ounce, or 0.60 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by just 0.18 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index came in off 1.47 percent. The U.S. Trade-Weighted Dollar continued to march higher this week and gaining 1.12 percent.

| Date |

Event |

Survey |

Actual |

Prior |

| Apr-30 |

Germany CPI YoY |

1.5% |

1.6% |

1.6% |

| May-1 |

ISM Manufacturing |

58.5 |

57.3 |

59.3 |

| May-1 |

Caixin China PMI Mfg |

50.9 |

51.1 |

51.0 |

| May-2 |

ADP Employment Change |

198k |

204k |

228k |

| May-2 |

FOMC Rate Decision (Upper Bound) |

1.75% |

1.75% |

1.75% |

| May-3 |

Eurozone CPI Core YoY |

0.9% |

0.7% |

1.0% |

| May-3 |

Initial Jobless Claims |

225k |

211k |

209k |

| May-3 |

Durable Goods Orders |

-- |

2.6% |

2.6% |

| May-4 |

Change in Nonfarm Payrolls |

193k |

164k |

135k |

| May-9 |

PPI Final Demand YoY |

2.8% |

-- |

3.0% |

| May-10 |

CPI YoY |

2.5% |

-- |

2.4% |

| May-10 |

Initial Jobless Claims |

218k |

-- |

211k |

Strengths

- The best performing metal this week was silver, up 0.14 percent. Gold traders were back to bullish this week after gold bounced off its 200-day moving average after dropping to its lowest since December on Tuesday, according to the Bloomberg weekly survey of traders. The yellow metal fluctuated on Friday morning after the jobs report came out with mixed signals on low unemployment but fewer-than-expected jobs added. The United Arab Emirates rolled back a 5 percent valued-added tax on gold, diamonds and precious metals this week, intending to maintain the country’s ranking on ease of doing business as well as stimulate transactions, reports Gulf Business.

- The Federal Reserve signaled this week that it is willing to allow inflation to exceed the 2 percent goal by adding a reference to the “symmetric” nature of the inflation target. Analysts consider that this is significant in that it underscores the fact that deviations from the target to the upside will be treated equally as deviations to the downside and that the FOMC has tolerated inflation below target for a long time.

- As seen in the chart below, gold climbed significantly after the Federal Reserve announced it would stick to a steady path of interest rate increases this year. Gold also rebounded this week as investors weighed the uncertainty of whether or not the U.S. will withdraw from the Iranian nuclear accord. WTI crude oil prices are up nearly 13 percent year-to-date, and a higher oil price is generally a signal of rising inflation, which is historically positive for the gold price. Gold demand in Iran soared to a three-year high of 9.3 tons in the first quarter, reports Bloomberg.

click to enlarge

Weaknesses

- The worst performing metal this week was gold, down 0.60 percent. Gold fell earlier this week due to a strong dollar and got close to erasing the gains experienced this year so far. Stephen Innes, head of trading for Asia Pacific at Oanda Corp., wrote in a report this week that “rising interest rates and a firming dollar remain bearish risks for gold and silver.” The world’s largest ETF backed by gold saw its biggest daily outflow in three months with close to $186 million taken out on Tuesday before the start of the Fed meeting.

- BullionVault’s Gold Investor Index fell to its lowest level since August early this week to 52.5, down from 53.7 in March. Bloomberg reports that a reading above 50 indicates more buyers than sellers among clients. Perth Mint released April sales figures showing that gold coin and minted bar sales were down compared to the prior month, from 29,883 ounces in March to 15,161 ounces in April. Sales of U.S. Mint American Eagle gold coins have also fallen and dropped to their weakest levels since 2007, while silver coin purchases for April rose 10 percent higher than last year.

- The World Gold Council released its first quarter report on Thursday showing that global gold demand was down 6 percent quarter-over-quarter and down 7 percent year-over-year to 973 metric tons. China, the world’s largest gold consumer, saw demand increase 7 percent, while India, the second largest consumer, saw demand fall 12 percent. The drop in gold demand in India can be attributed to a steady rise in prices in the last three months and tighter credit to jewelers after a bank fraud, reports Bloomberg First World.

Opportunities

- Although the U.S. dollar has been on a hot streak as of late, which is usually negative for gold, some think that the uptrend won’t continue for long. Automated trend-followers have moved to neutral from a big short position on the dollar in recent weeks and now they’ve blown through all their stop-losses. Bloomberg writes that dollar bears are no longer fighting a headwind posted by automated buying from a group with combined assets of around $277 billion.

- Mike McGlone, commodity strategist at Bloomberg Intelligence, writes that gold should be on the rise due to continued mean reversion and gold awakening from its narrowest 52-week trading range in 13 years. Egyptian billionaire and Orascom Telecom Chairmain Naguib Sawiris said that he expects gold price to rise to $1,800 per ounce. Sawiris recently transferred half of his $5.7 billion net worth into bullion.

- Detour Gold reported a tough quarter Friday and advised the market of another mine plan revision that resulted in the stock falling about 35 percent over the next two trading sessions. Dan Rollins of RBC published a note calling for someone to take over the company. Detour has typically traded with a premium due to the large production base and long life, but lack of flexibility with regard to grade, risk they can turn a consistent profit, has not been fully appreciated. Generally, buyers of assets the size of Detour have been puck shy to get back into the acquisition game. However, Detour could be in the crosshairs of a Canadian based company(s) that does not already have operations in Canada, where they might also be able to harvest some tax losses to offset the takeover premium, much like Eldorado Gold’s purchase of Integra Gold last year.

Threats

- Deutsche Bank research, using its database of 45 countries, found that the deteriorating fiscal and external situation for the U.S. has increased the probably of a U.S. debt crisis by 7 percentage points, to a level around 16 percent. Demand for U.S. debt abroad has been trending lower in recent years and the bid-to-cover ratio has been declining, including for T-bills and 2-year and 10-year Treasury auctions. The U.S. set a first-quarter record by borrowing $488 billion, $47 billion more than estimated. However, Treasury Secretary Steven Mnuchin said in an interview on Monday that “I think the market can easily handle it.”

- Although there has been an increase in gold exploration budgets, there has not been a subsequent increase in gold discoveries. Mining Weekly writes that $54.3 billion has been allocated to gold exploration over the past decade, which is 60 percent higher than the preceding 18-year period. However, only 215.5 million ounces of gold has been discovered in the most recent 10 years, compared with 1.73 billion ounces in the preceding 18 years.

- RBC Capital Markets writes that since 2017 the average daily trading value of gold has declined to an average of around $1.6 billion, which it believes is indicative of a reduced level in interest in precious metal equities. Previously the combined daily trading value of the gold miners and junior gold miners ETFs rose from around $790 million in 2007 to a peak of $2.4 billion in 2016.

Emerging Europe

Strengths

- The Czech Republic was the best relative performing country this week, losing 60 basis points. CEZ AS, a utility company, gained the most among stocks trading on the Prague exchange. The company will announce its first quarter results next week.

- The Russian ruble was the best relative performing currency this week, losing 50 basis points against the U.S. dollar. Emerging European currencies recorded sharp losses against the dollar this week. However, the ruble was supported by a slight uptick in the price of oil. The manufacturing PMI for April was reported at 51.3, above the expected reading of 505.5. Inflation remained unchanged at 2.4 percent, below the Central Bank’s target.

- Information technology was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 4.4 percent. April’s inflation came in at 10.85 percent, above expectations of 10.45 percent. S&P rating agency unexpectedly lowered the country’s credit rating, citing a deteriorating inflation outlook, long-term depreciation and volatility of the exchange rate.

- The Turkish lira was the worst performing currency this week, losing 4.5 percent against the U.S. dollar. Strength in the dollar and political noise around the upcoming early elections in June are pushing the currency to new record-low levels. President Erdogan’s focus before the early elections is on lower rates, not so much on a falling lira.

- Industrials was the worst performing sector among eastern European markets this week.

Opportunities

- During the Eurogroup meeting last week, Greece’s creditors stated that the country is on track to reach a final deal on June 21 and exit its bailout program in August. Bank stress test results should be announced next week, and most analysts expect a positive outcome.

- Nomura International Plc is betting on a rebound in both the Czech koruna and the Polish zloty after the currencies fell to the weakest level in months against the euro this week. The Hungarian forint fell to the weakest level in almost two years on Tuesday. It could be a buying opportunity, as these economies are doing relatively well, with good external financing positions and strong export prospects given the growing strength of European demand, said Nigel Rendell, a senior analyst for EMEA at Medley Global Advisors.

- The Czech centrist, populist ruling ANO party could be days away from forming a new coalition, ending a month of political instability. The Czech Republic has been without a new government for half a year as most parties have backed away from joining with ANO, while its leader Andrej Babis fights off fraud allegations. A new minority cabinet will most likely include the Social Democrats and be backed in parliament by the Communists. The lack of new government had no effect on the stock market.

Threats

- According to Bloomberg, Turkish stocks are the cheapest in nine years. The price-to-estimated earnings ratio of the benchmark Borsa Istanbul 100 Index is approaching a low multiple of seven, the level last seen in 2009. Further weakness may come, as the lira is on a downtrend, current account deficit is widening, inflation is high, and the government may be running out of options to stimulate its economy.

click to enlarge

- Euro-area economic growth slowed in the first quarter, posing a challenge for the European Central Bank (ECB) to cut down on stimulus measures. The 0.4 percent expansion in the first quarter was the weakest in six quarters and followed 0.7 percent at the end of 2017. Inflation unexpectedly slowed in April to 1.2 percent year-over-year from 1.3 percent the prior month. The core rate, which excludes highly volatile items like food, dropped to 0.7 percent, which is the weakest reading in more than a year.

- Trump’s administration on Monday granted Europe, Mexico and Canada tariff exemption on imports of aluminum and steel until June 1. This prolongs the uncertainty period. The eurozone Manufacturing PMI declined from a record high of 60.6 in December to 56.2 in April. If tax are announced next month on imports of aluminum and steel from Europe into the United States, the Manufacturing PMI may continue its slide downward.

|

|

May 4, 2018

|

|

May 3, 2018

|

|

May 3, 2018

|

|

© US Global Investors

www.usfunds.com

© U.S. Global Investors

Read more commentaries by U.S. Global Investors