The Federal Open Market Committee (FOMC) met on May 1-2, 2018. Its closely watched statement included the passage: “Inflation on a 12-month basis is expected to run near the Committee’s symmetric 2 percent objective over the medium term.”

The term “symmetric” was a new addition to the communication. For those who have forgotten their high school geometry lessons—or for artists unsure how a visual descriptor applies to inflation rates—the idea is that the target inflation rate is not a hard ceiling. This seemingly subtle change of phrasing is an attempt by the FOMC to set market expectations as inflation readings exceed 2%.

Few expect the price level to accelerate uncomfortably; there are too many secular governors to overcome. Nonetheless, as the demand side of the American economy continues to grow faster than the supply side, some additional inflation is to be expected. And that should prompt the FOMC to continue the recent trend of moderate interest rate increases.

Key Economic Indicators

Influences on the Forecast

-

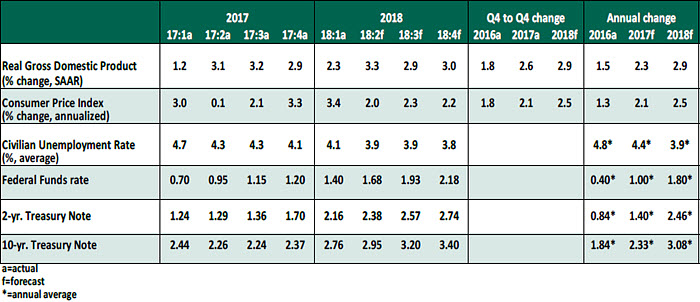

- Gross domestic product (GDP) for the first quarter was an upside surprise, showing 2.3% growth after adjusting for inflation. A combination of a heavy winter, slower consumer spending and expected seasonality were all at play.

-

The pause in consumer spending (1.1% growth) was partly attributable to the absence of outlays related to disaster recovery from last year’s storms. The report showed strong growth in business investment (6.1%). We anticipate that the first quarter will be the slowest of 2018, with loose fiscal policy promoting additional consumer activity, business investment and government spending in the remainder of the year.

-

- The U.S. trade deficit narrowed slightly in the first quarter, thanks to solid export growth. But most forecasters are expecting the U.S. trade imbalance to grow substantially in coming quarters, which will drag on measured economic growth. Our projections do not yet incorporate the threat of new tariffs by both Washington and our trading partners.

-

- The U.S. unemployment rate is now 3.9%, a level last seen in the year 2000. Total employment increased by 164,000 in April, and job creation in prior months was revised upward. Wage growth was subdued at 2.6%. Overall, the employment report continued a years-long trend of steady jobs growth. The unemployment rate has little room left to fall.

-

- The employment cost index (ECI) for the first quarter rose by 2.71% year-over-year, a rate of increase not seen since 2008. The ECI is a combined metric of the costs of salaries and benefits. Employers are facing higher labor costs, yet another factor that could lead to higher prices.

-

- Measures of inflation are higher. The deflator on personal consumption expenditures is 2.0% higher than it was a year ago (1.9% excluding food and energy). The consumer price index rose by 2.4% for the year ending in March, while the producer price index rose by a strong 3.0%.

-

Softer signals of inflation abound. Manufacturing surveys of import prices are very high, and anecdotes of price pressures are multiplying in the Federal Reserve’s Beige Book report of regional conditions.

-

- Import tariffs remain small, but even if only a fraction of currently threatened tariffs are put in place, the outcome can only be inflationary. Trade negotiations continue on multiple fronts: within the North American Free Trade Agreement, with China, and with producers of steel and aluminum. A one-month reprieve to keep most countries exempt from the Section 232 tariff on metals is an encouraging sign of negotiation, but ongoing extensions appear to be unlikely.

-

- At its May meeting, as expected, the FOMC held the Fed Funds rate range at 1.50-1.75%. FOMC commentary acknowledged recent growth in business investment and a greater likelihood of inflation. We expect to see overnight rates increase by 25 basis points each in June, September and December.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2018 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust