Emerging market stocks and bonds are having a rough year, but Russ argues against abandoning the asset class.

For the first time since late 2016, emerging markets (EM) are under-performing their developed market counterparts. While few asset classes—outside of oil—are having a stellar year, EM is having a particularly bad time. An index of developed equity markets is roughly flat year-to-date; EM stocks are down approximately 2%. Emerging market bonds are having an even worse year, down more than 5%.

What’s going on? Is it time to lighten up on the asset class? The answer to the latter question is no.

A number of catalysts are to blame. Emerging markets are struggling with a sharp and abrupt reversal in the dollar, concerns about global growth and idiosyncratic issues surrounding particular markets such as Turkey and Brazil. That said, there are three good reasons to stick with the asset class.

1. The return of relative value.

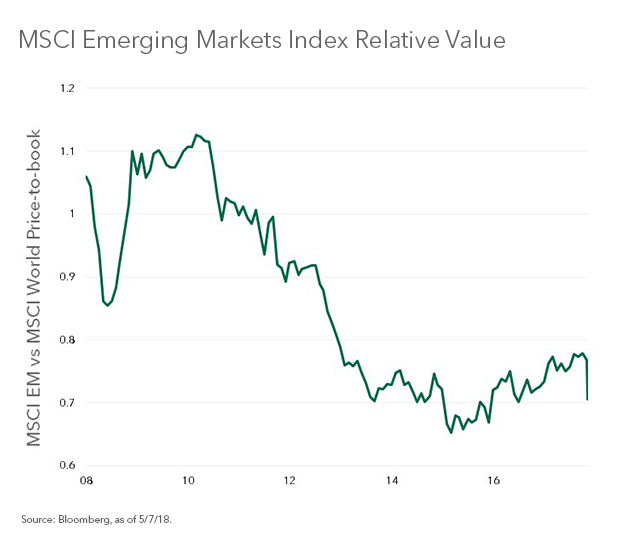

Like every other asset class, EM stocks and bonds have been cheaper. However, recent weakness has restored relative value, particularly for stocks. Based on price-to-book (P/B), the MSCI Emerging Index is trading at a 30% discount to MSCI World Index of developed markets (see accompanying chart). This represents the largest discount since December 2016 and compares favorably with the 10-year average of 14%.

2. Despite the typical first quarter slowdown, the global economy is in solid shape.

As I discussed back in late January, global economic growth is key for EM and I referenced industrial metals as a good real-time proxy for global growth. While softer in recent days, the JOC-ERCRI Metals Index has risen 20% during the past year and is still up 4% year-to-date. Other indicators of global growth, such as the global purchasing managers index (PMI), also confirm the ongoing expansion.

3. A stronger dollar is a headwind, not a death sentence.

There is no doubt that the rapid and surprising appreciation of the dollar has hurt EM assets. That said, the dollar is not the sole, or even primary determinant of emerging market performance. For equities in particular, changes in the dollar have historically had a modest impact on relative returns.

Expecting a better second half

While the past several weeks have been extremely unpleasant for EMs, there is reason to expect a better second half. The dollar’s sharp rebound is arguably the result of a rapid and violent unwind of a very crowded short trade. Recent changes in positioning suggest much of this adjustment has already occurred.

Beyond the dollar, the global economy should rebound this summer as the lagged impact of U.S. tax cuts and fiscal stimulus are fully realized. In particular, a likely acceleration in capital spending should be supportive of global trade, and by extension emerging markets. For investors who have already lived through the volatility, this is probably the wrong time to sell.

Russ Koesterich, CFA, is Portfolio Manager for BlackRock’s Global Allocation team and is a regular contributor to The Blog.

Investing involves risks, including possible loss of principal.

International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks may be heightened for investments in emerging markets.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of May 2018 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts.

There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

©2018 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

494858

© BlackRock

Read more commentaries by BlackRock