Summary

- The Madness of Crowding Out

- Foreign Investors Warm Up To Chinese Bonds

- Trade Deadlines Are In Sight

I will be working in Asia for most of the coming two weeks, and I am very much looking forward to it. What a great time to dig more deeply into events on the Korean peninsula, and to get a Chinese angle on trade negotiations with the United States. I am also looking forward to bulgogi, xiaolongbao, nasi lemak and other regional delicacies.

The cities I will be visiting are among the most densely populated in the world. Any of you who have been to the large cities of Asia are familiar with the crowds; the energy that they generate is exciting, and invites you to tag along. Visitors to the region must learn to navigate through the chaos.

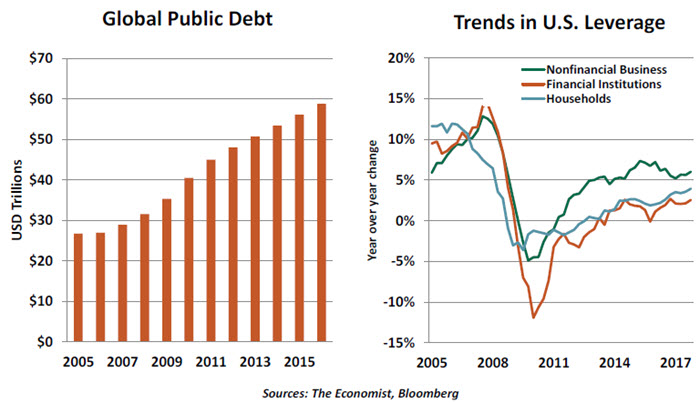

Crowding can be a problem, however, when it comes to credit. The dramatic increase in public borrowing over the last decade has absorbed copious amounts of capital that might otherwise have been used to finance spending in the private sector. If government debt grows too much, businesses and consumers seeking loans can find themselves "crowded out." Impaired access to credit is harmful to economic growth.

To date, there is little evidence that worthy borrowers are experiencing undue difficulty in accessing capital. But as the credit cycle turns and worldwide fiscal positions worsen, crowding out may become a bigger issue.

Classical economic theory holds that households apportion funds to spending and saving based on their need for income currently and in the future. This allocation can be influenced by the level of interest rates; higher yields will typically incent higher levels of investment. Banks lend the resulting pool of savings to those who want to borrow; credit taken by the public sector reduces the amount available to support business growth.

Global public debt has more than doubled over the past decade. A good portion of this increase reflects government efforts to put floors under their economies in the wake of the 2008 financial crisis. At first, debt-driven deficit spending replaced private demand; further on, governments expanded their use of leverage as households, companies and financial institutions de-leveraged. Quantitative easing programs from central banks absorbed a good fraction of the incremental sovereign debt supply, which kept interest rates low and credit available for those who wanted it.

It took time, but household and corporate balance sheets in many parts of the world returned to health. While private sector credit growth remains well below its pre-crisis pace, an expanding community of firms and individuals are feeling comfortable taking on additional debt. They have been attracted, in part, by interest rates that remain low by historical standards.

There is an enduring belief among conservative economists that government functions are less efficient than the private sector, and markets are better at allocating capital than bureaucracies. Those in this camp believe governments should step back as the private sector steps forward.

Instead, many governments continue to flood the market with new bonds, as they pursue fiscal expansion and seek to satisfy public pension obligations. Expanding debt and strong economic prospects have combined to raise sovereign interest rates in developed markets. And this, in turn, has raised borrowing costs for companies, consumers and emerging markets.

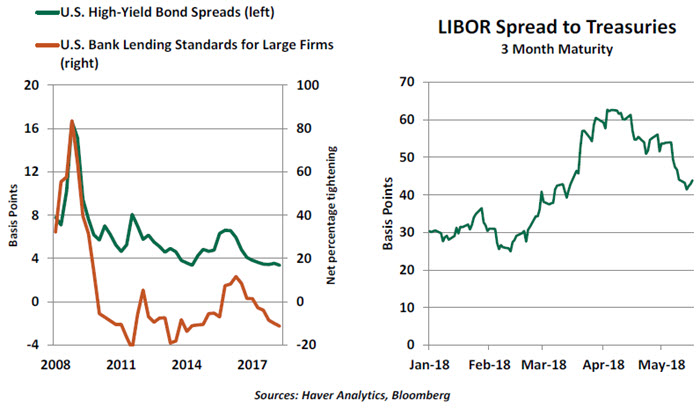

For the time being, credit conditions do not seem to reflect signs of crowding out. New debt issues have generally been well received in the markets. Spreads on high-yield debt, which one might consider a canary in the coal mine if conditions shift, remain very low. And bank lending standards remain favorable for borrowers.

But an episode from earlier this year provides a glimpse of what might lie ahead. In the wake of U.S. tax reform, the U.S. Treasury announced plans to sell a large volume of short-term securities. Yields on these instruments are nearly double what they were last fall, making them much more competitive with other short-term debt on a quality-adjusted basis.

Some investors capitalized on this development by shifting their cash holdings from prime funds (which invest in commercial paper and interbank placements) into government bond funds. This, in turn, raised the rates that companies paid for their short-term borrowing. Spreads between the London Interbank Offered Rate (LIBOR) and Treasury yields doubled, and remain elevated relative to historical norms. This is crowding out, in miniature.

The consequences of crowding out can be mitigated if higher interest rates attract new capital to credit markets. Because of its strong standing, the United States has been the beneficiary of considerable capital inflows recently, which has partially offset the impact of heavy Treasury borrowing. But the supply of global financing is not infinite, so gains for one country often come at the expense of others. In recent weeks, the "others" have been emerging markets, several of which have been struggling (as we covered here).

The situation could get more challenging. The Federal Reserve, whose holdings of government securities had swollen to more than $4.5 trillion by the beginning of last year, is in the process of cutting back. Up to $2 trillion of those holdings will be released to the markets over the next few years; new private buyers will need to be found. Long-term projections of the U.S. fiscal position are somewhat scary. And there are early signs global credit may be past peak quality.

When the business cycle starts to turn, crowds begin reversing course. And as they do, they can draw in innocent passersby. Deciding when to break from the crowd on these occasions is a terribly difficult thing to do.

China Learns to Bond

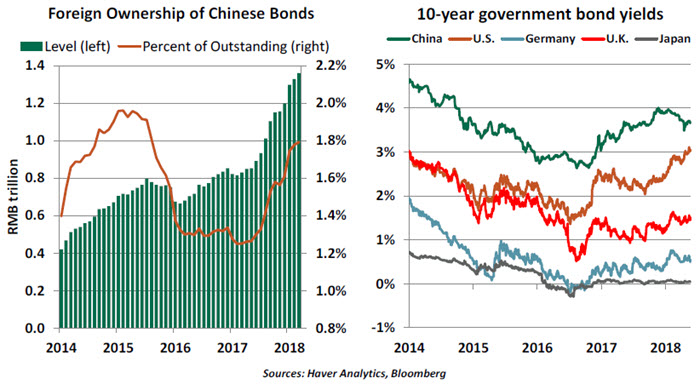

After carefully restricting foreign access to its financial markets for many years, Chinese policymakers have taken a number of steps towards financial liberalization. These include opening China's interbank bond market to foreign institutional investors in February 2016 and providing overseas investors access to the foreign exchange derivatives market to allow hedging of bond positions. The main objective has been to attract long-term inflows.

Prior to February 2016, foreign participations were subject to stringent quotas on security ownership and onerous licensing requirements. When access was relaxed, fears over capital controls, default risks and a weaker currency initially kept foreign investors at bay.

Policymakers' efforts to open up the domestic bond market (the world's third largest after the U.S. and Japan) to foreign investors are gathering steam. Foreign investment in China's domestic bond market has continued to soar this year, despite the recent sell-off in the debt of many emerging markets. Foreign ownership of Chinese fixed-income instruments has doubled in just two years, from renminbi (RMB) 0.68 trillion in March 2016 to RMB 1.36 trillion in March 2018.

Though inflows have increased, the share of foreign holdings still remains less than 2% of the RMB 75.9 trillion in outstanding domestic debt. By comparison, foreign holdings account for around 11% of Japan's debt.

The numbers of overseas institutional investors and trading volumes have both increased steadily since the launch of Bond Connect in July 2017. Bond Connect allows overseas investors to trade directly in mainland China's bond markets without having to set up onshore accounts. According to the Bond Connect first quarter 2018 flash report, commercial banks and investment vehicles such as mutual funds were the most active institutional investors.

Besides ongoing reforms, the hunt for higher yields and a relatively stable currency have also contributed positively to increased inflows. Chinese bonds became part of the International Monetary Fund's special drawing rights facility in 2016, which added depth to demand for Chinese issues and provided a seal of approval.

Bloomberg, which had initially declined to include China in its Global Aggregate Index, recently added Chinese bonds to the mix (in phases starting in April 2019). Chinese bonds may also earn inclusion in the J.P. Morgan Emerging Markets Government Bond Index. Inclusion in these global bond indices is likely to provide further impetus to the China bond market, as investors measuring themselves against these benchmarks increase their ownership of Chinese notes.

The People's Bank of China remains committed to the "two-way" expansion of financial markets and further improving the rules dealing with bond defaults, in order to prevent and reduce financial risks. Planned measures for further deepening of reforms include

- tightening of regulations on shadow banking businesses and real estate financing,

- exploring the interest rate corridor regime for effective implementation of monetary policy,

- enabling the markets to play a bigger role in determining the foreign exchange rate, and

- "steadily" promoting capital account convertibility.

Save the Date

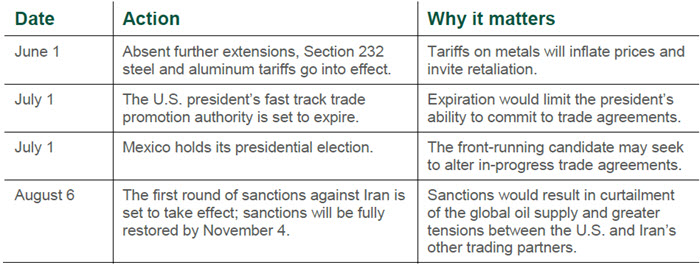

This year's trade news has been characterized by loud threats of sanctions and retaliations. While the bluster gets the most attention, there are concrete deadlines looming. A review of key upcoming dates shows that the risk of tariffs is becoming very real.

One key date already passed. On May 21, the 60-day comment period for the threatened tariffs against China closed. Tariffs of up to $150 billion could have gone into effect from that day forward. In the nick of time, the U.S. announced a truce with China. The statement from U.S. trade representatives was encouraging but light on detail. The threat of tariffs lingers. Commerce Secretary Wilbur Ross stated, "This is not a definitive agreement...If it doesn't work, the tariffs will go into effect."

© Northern Trust

northerntrust.com/disclosures

© Northern Trust

Read more commentaries by Northern Trust