Building a Better U.S. Economy

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

This shouldn’t surprise anyone, but public trust in the federal government is eroding. Sixty years ago, 75 percent of Americans expressed faith in the government to do the right thing “most of the time” or “just about always.” Seventy-five percent! You can’t get 75 percent of people to agree on anything now, as the recent “Laurel or Yanny” video proved.

Today, only one in five Americans—a near-record low—believes our leaders make decisions in the country’s best interest. If you’re reading this, you might very well be in the camp that has some serious doubts.

|

|

The polling data, provided by the Pew Research Center, was shared by Pulitzer Prize-winning biographer Jon Meacham, who spoke this week at an Investment Company Institute (ICI) meeting in Washington, D.C. Although no fan of the president, Meacham believes, as I do, that fed up, disillusioned voters turned to Donald Trump to take on the beltway party and career bureaucrats and roll back out-of-control regulations. Similarly, Brexit in the U.K. was a populist backlash against excessive rules from unelected bureaucrats in Brussels.

Love him or hate him, Trump has so far stuck to his word, and he doesn’t seem to have any reservations about whose applecart he upsets. He’s an equal-opportunity disruptor, and for that he has opponents on all sides of the political spectrum.

It's little wonder, then, that “Trump” is likely the most spoken word in the English language right now, according to Meacham. Just don’t tell Trump that.

The presidential historian—who last month delivered the eulogy for former first lady Barbara Bush—also reminded the audience that, as bad as many people believe things are right now, they used to be much worse. Remember slavery? Remember Jim Crow?

Some people believe Trump is determined to weaken First Amendment protections, but he’s not the biggest threat to free speech this country has ever seen, Meacham said.

A little over 100 years ago, in preparation for America’s entry into World War I, Congress passed and President Woodrow Wilson signed the Espionage Act, which gave the U.S. government sweeping new authority to control and censor the press. Overnight, it became illegal to “convey information with intent to interfere with the operation or success of the armed forces of the United States or to promote the success of its enemies.” Hundreds of communist and pro-German newspapers and magazines were banned or otherwise forced to shut down.

It’s important to put things in perspective. Trump might regularly criticize what he perceives as “fake news,” but at least those outlets—the New York Times, Washington Post, CNN and others—are allowed to continue operating.

TRUST THE GOVERNMENT? TAKE OUR POLL

Trump Maintains a One-In, Five-Out Pace for Regulations

Many attendees of the ICI meeting, all representing investment and wealth management firms, weren’t so optimistic about their ability to communicate effectively with shareholders and potential clients. Some of them shared with me their observation that regulators are increasingly getting bolder about what financial firms can and cannot say, and the rules keep piling up.

Within the past year, we were asked to add disclosure under a picture of Elvis Presley in one of our gold presentations, if you can believe it. And during the conference, a fund manager said he found it ridiculous that, in a company slideshow, he was asked to add disclosure beneath a picture of Aristotle to inform clients that the ancient Greek philosopher was not, in fact, affiliated with the fund in any way.

It raises the question: What reader would assume that Elvis and Aristotle—the former having been dead 40 years, the latter 2,000 years—are affiliated with an investment firm? This is a financial blog, not the National Enquirer.

It’s common knowledge in the business that the number of investment advisors and brokers is shrinking day-by-day. You would think that the number of rules and regulations would likewise shrink, but that doesn’t appear to be the case. In such a climate, the only ones who manage to stay ahead are the Vanguards and BlackRocks of the investment world.

I believe this is among the biggest reasons why many people voted for Trump—to cut the red tape and rein in rampant bureaucracy. Here again, he’s kept his word, having so far eliminated, on average, five federal rules for every new rule created, according to the libertarian think tank Competitive Enterprise Institute (CEI).

Bye Bye, Dodd-Frank. Hello, Economic Growth?

Case in point: This week he signed legislation that severely weakened the Dodd-Frank Wall Street Reform and Consumer Protection Act. The behemoth 2010 law, intended to prevent another financial crisis, is believed to be directly responsible for the failure of a number of small and regional banks, which small businesses and rural families depend on for loans and other financial services.

That’s why I named Dodd-Frank one of the five costliest financial regulations of the past 20 years. Barney Frank himself, the former chairman of the House Financial Services Committee and one of Dodd-Frank’s chief architects, acknowledged he “sees areas where the law could be eased.”

With the most restrictive parts of Dodd-Frank gone or amended, annual economic growth in the U.S. might finally be able to break above 3 percent, a rate we haven’t seen since 2005.

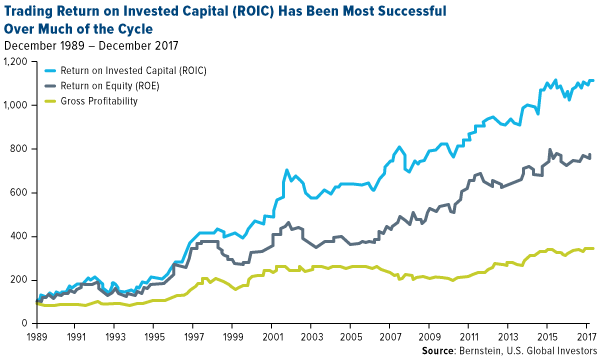

In the meantime, asset management firm AllianceBernstein shows that, over the past 30 years, the best performing factor has been return on invested capital (ROIC). According to the firm, ROIC outperformed return on equity (ROE) by one and a half times, and gross profitability by nearly three times.

Seeing this chart was particularly vindicating for us, as ROIC is among the most important factors we pay attention to when making our investment decisions.

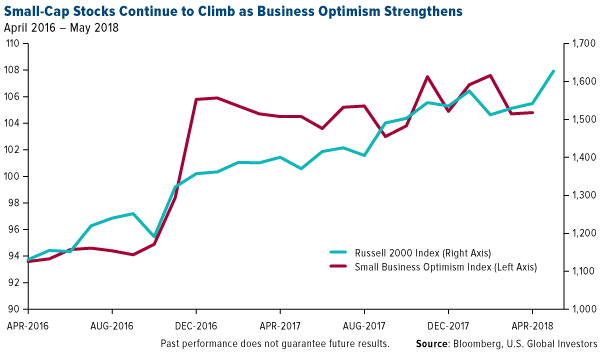

Government Policy Right Now Favors Small-Cap Stocks

The Dodd-Frank rollback is just the latest move by the Trump administration that should benefit smaller businesses. Quarter-to-date, the small-cap Russell 2000 Index is up more than 6 percent, compared to the S&P 500 Index, which is up 2.8 percent. Meanwhile, small business optimism , as measured by the National Federation of Independent Business (NFIB), remains near a historic high, posting 104.8 in April, up a hair from the previous month.

I often say it’s not about which party is in power but rather the policies that matter. Whether the Republicans or the Democrats control Washington isn’t the point. There are ways for investors to make money in either case, and right now, government policy favors domestic small-cap stocks that have limited exposure to overseas markets. The trend is your friend, as they say, and with respect to small-caps, that certainly seems to be the case.

Learn more about small and mid-cap stocks by clicking here!

Happy Memorial Day!

Memorial Day weekend is traditionally the beginning of the busy summer travel season, and this year is forecast to set a new record for flight demand. Airlines for America (A4A) predicts that 246.4 million people will fly on U.S. airlines this summer, or 2.68 million per day, which is up 3.7 percent from last summer.

What this means, number one, is that now might be a good time to consider airline stocks, and two, you should definitely book your summer flights now if you haven’t already done so.

Whatever you decide, though, make sure to take time out this weekend to remember those who helped preserve your right to own property and travel freely, among other liberties. In the words of President Franklin Roosevelt, spoken on the eve of the D-Day invasion, American troops fought “not for the lust of conquest” but to liberate and “let justice arise.” Indeed, the brave servicemen and women “yearn for the end of battle, for their return to the haven of home.”

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.15 percent. The S&P 500 Stock Index rose 0.31 percent, while the Nasdaq Composite climbed 1.08 percent. The Russell 2000 small capitalization index gained 0.02 percent this week.

- The Hang Seng Composite lost 1.01 percent this week; while Taiwan was up 1.03 percent and the KOSPI rose 0.01 percent.

- The 10-year Treasury bond yield fell 12.5 basis points to 2.932 percent.

Domestic Equity Market

Strengths

- Utilities was the best performing sector of the week, increasing by 3.09 percent versus an overall increase of 0.23 percent for the S&P 500.

- Foot Locker was the best performing stock for the week, increasing 28.31 percent.

- Shares of shoe retailer Foot Locker surged Friday after the company reported earnings well ahead of Wall Street expectations. The stock rallied after the company reported adjusted earnings per share at $1.45 for the first quarter, above consensus estimates of $1.25 from FactSet. The company posted revenue of $2.03 billion, which also beat forecasts. "The flow of premium product continues to improve, with increasing breadth and depth in the most sought-after styles from our key vendors," CEO Richard Johnson said in a statement.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 4.54 percent versus an overall increase of 0.23 percent for the S&P 500.

- Best Buy was the worst performing stock for the week, falling 12.52 percent.

- The owner of MoviePass hit a new low. Shares of Helios & Matheson, the technology company that bought MoviePass last year, plunged 11 percent to a new low of $0.50 Tuesday morning.

Opportunities

- S&P 500 earnings strength appears likely to continue for at least the next several quarters, boosted by improving forecasts for top-line growth, writes Bloomberg Intelligence strategists Gina Martin Adams and Peter Chung. If there's a challenge to earnings trends on the horizon, it's likely a combination of margin pressures due to rising input costs and tough comparisons in 2019. Higher rates and commodity prices are increasingly defining winners and losers in S&P 500 earnings.

- Blackstone's valuation could jump more than 50 percent if it converts into a C-corp., according to a Credit Suisse analyst. The firm could make the switch as early as 2019 if KKR's planned conversion results in a significant increase in valuation over the next year, the analyst wrote in a note. KKR and Ares, which are the first major PE managers to move to change structures, have since seen their stock prices outpace Blackstone.

- Leon Cooperman said the stock market is "fairly valued" and valuations of technology firms are reasonable. Cooperman told CNBC May 22 that FAANG stocks could gain further and that he is positive on traditional banks, saying it was a "mistake" to sell JPMorgan. He said he also exited his Wells Fargo position in favor of Citigroup.

Threats

- Victoria's Secret parent, L Brands, tumbled after lowering guidance. Shares fell more than 6 percent in after-hours trading Wednesday after the retailer beat on both the top and bottom lines but lowered its full-year 2018 earnings guidance to a range of $2.70 to $3.00 a share from $2.95 to $3.25.

- Moody’s said it may cut Campbell Soup’s credit rating after the company posted a steep drop in profitability and its chief executive suddenly stepped down. All of the company’s ratings are under review, including its Baa2 senior unsecured rating, Moody’s said in a report on May 21. That’s only two steps above speculative-grade. Moody’s did not say how many levels the downgrade could amount to.

- Sears continues to shut down stores. The company is closing at least 40 stores, including 31 Sears stores and nine Kmart stores.

The Economy and Bond Market

Strengths

- The flash IHS Markit U.S. manufacturing purchasing managers index inched up to 56.6 this month, up from 56.5 in April, and touched the highest level since September 2014. A similar survey of service-oriented businesses also rose, climbing from to 55.7 from 54.6 in April.

- National home values have increased 8.7 percent since last April to a median value of $215,600, according to Zillow. Newly released data from the Federal Housing Finance Agency (FHFA) confirm the gains seen by Zillow, as home prices rose in all 50 states and the District of Columbia in the first quarter of 2018 compared to a year earlier. The FHFA report shows first quarter home prices rose 6.9 percent from a year earlier. Annual appreciation surpassed 10 percent in several states including Nevada at 13.7 percent, Washington at 13.1 percent, Idaho at 11.1 percent and Colorado at 10.6 percent.

- Durable-goods orders fell 1.7 percent in April, mostly due to a decline in contracts for Boeing. Most businesses took in more orders and increased investments last month. Economists surveyed by MarketWatch forecast a 1 percent decline in orders for durable goods. A better way to judge orders is to strip out the outsized effect of planes and cars. Orders minus transportation rose 0.9 percent, the government said, to mark the third straight gain.

Weaknesses

- Japan’s manufacturing sector lost steam in May, signaling that the world’s third-largest economy may not be rebounding as well as expected after contracting in the first quarter of this year. The Nikkei Japan PMI for manufacturers showed a preliminary reading of 52.5 for May, down from 53.8 in April.

- Economic momentum in the eurozone cooled yet again in May as more temporary factors weighed on output in manufacturing and services. The composite PMI fell to an 18-month low of 54.1, down from 55.1 in April, IHS Markit said. New order growth weakened, hiring and backlogs of work showed slower rates of increase and companies became less optimistic about the outlook. The euro hit the lowest level since November after the report.

- German exports fell the most in more than five years at the start of 2018, holding back growth in Europe’s largest economy. A breakdown of first quarter GDP data showed foreign sales fell 1 percent, the most since 2012. Imports also declined, and net trade knocked 0.1 percent off GDP. The German GDP report showed government spending also slipped in quarter one. Overall economic growth — confirmed at 0.3 percent — was supported by consumer spending and capital investment.

Opportunities

- An alternative price gauge was noted by members of the Federal Open Market Committee at its May meeting, minutes released on Wednesday showed. The 12-month Trimmed Mean PCE rate — which strips out the most extreme movements in the components of the PCE index — suggests “relatively stable” underlying inflation at levels below 2 percent, officials thereby signaled.

- Municipal-bond investors always have an eye on the population of any city or state they buy, given that a declining tax base often precipitates credit-rating downgrades or financial problems. If they bought bonds issued by the Texas cities of Frisco, New Braunfels and Pflugerville, the latest report by the U.S. Census Bureau is akin to an earnings beat: the three cities were named the fastest growing in the year ended July 1. In fact, seven of the 15 cities with the fastest-growing populations were in Texas, the census reported on Thursday. San Antonio saw the largest numeric increase, adding 24,208 new arrivals, or about 60 people a day on average. And there may be more opportunities for municipal investors and to take advantage of the influx of people into the Lone Star state. S&P Global Ratings estimates that 40 percent of the land in Frisco is undeveloped. The ratings company says that Fort Worth, which bumped Indianapolis to become the 15th largest city in the U.S., also has a "significant" amount of undeveloped land.

- Six Fed rate hikes, the launch of a new potential reference rate (along with related futures), a climb in the Libor/OIS spread that spooked investors and even the federal funds effective rate rising toward the upper bound of officials' target range have combined to make the front end of the yield curve interesting again, write Bloomberg Intelligence strategists Ira Jersey and Aleksandr Nozhnitskiy.

Threats

- Many U.S. households remain in a precarious financial position despite unemployment falling to the lowest level in years, a new Fed survey shows. The 2017 report on the economic well-being of U.S. households found that conditions have generally improved but many groups continue to struggle. The report showed two in five Americans don’t have enough savings to cover a $400 emergency expense, and one in four don’t feel they are “at least doing OK” financially.

- New Jersey Treasurer Elizabeth Muoio said structural budget troubles are accelerating and the state is on track for a $2.4 billion deficit if tax increases aren’t in place for the fiscal year starting July 1. The shortfall endangers Governor Phil Murphy’s $37.4 billion budget, which relies on taxes on high earners, yet-to-be-legalized recreational marijuana and services such as Airbnb and Uber.

- Kentucky's issuer credit rating has been cut to A from A+ by S&P as the state faces increased budgetary strain from rising costs due to pension obligations and a constrained revenue-raising environment. The ratings company said the state's income levels are well below the national average and economic growth that has consistently lagged the country is further complicating Kentucky’s long-term fiscal health.

Gold Market

This week spot gold closed at $1,301.70 up $9.70 per ounce, or 0.70 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.62 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index lost 1.40 percent. The U.S. Trade-Weighted Dollar continued its movement higher this week with a gain of 0.66 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-23 | New Home Sales | 680k | 662k | 672k |

| May-24 | Initial Jobless Claims | 220k | 234k | 223k |

| May-25 | Durable Goods Orders | -1.3% | -1.7% | 2.6% |

| May-28 | Hong Kong Exports YoY | 9.1% | -- | 8.0% |

| May-29 | Conf. Board Consumer Confidence | 128.0 | -- | 128.7 |

| May-30 | Germany CPI YoY | 1.9 | -- | 1.6% |

| May-30 | ADP Employment Change | 185k | -- | 204k |

| May-30 | GDP Annualized | 2.3% | -- | 2.3% |

| May-31 | Eurozone CPI Core YoY | 1.0% | -- | 0.7% |

| May-31 | Initial Jobless Claims | 230k | -- | 234k |

| May-31 | Caixin China PMI Mfg. | 51.2 | -- | 51.1 |

| Jun-1 | Change in Nonfarm Payrolls | 190k | -- | 164k |

| Jun-1 | ISM Manufacturing | 58.0 | -- | 57.3 |

Strengths

- The best performing metal this week was platinum, up 1.50 percent on expected Chinese demand for the metal, where demand for heavy-duty emission legislation will come into play by 2020. Bloomberg’s weekly survey showed that gold traders and analysts are divided on their outlook for bullion prices for next week. The yellow metal rose higher this week amid mounting geopolitical tensions and talks of tariffs on automobile imports.

- Gold prices rose higher on Wednesday after the Federal Reserve minutes pushed the Treasury yield down, which is a bullish signal for gold. Bullion was also up 1 percent Thursday morning after President Trump announced that the summit with North Korea would no longer be happening. Gold has historically performed well during periods of geopolitical instability, as investors often view it as a “safe haven” asset.

- National home values increased 8.7 percent since last April to a median value of $215,600 and the pace of appreciation is the fastest since June 2006, reports Bloomberg. This is a sign of rising inflation. Gold demand in Turkey remains strong and the nation has imported 118 metric tons in the first four months of this year. Suki Cooper, precious metal analyst at Standard Chartered Bank in New York, said in a report this week that in Turkey “local consumers have turned to gold as a store of value amid rising inflation, heightened political and economic tensions, and currency weakness.”

Weaknesses

- The worst performing metal this week silver, up 0.43 percent, but slightly trailing gold. Due to disappointing results at its flagship gold mine in Egypt, Centamin Plc cut its production forecast, reports Bloomberg. The move sent the stock down as much as 18 percent, the biggest fall in five years. “Underground gold output at Sukari has declined 10 percent so far this year, and production is likely to total 505,000 ounces to 515,000 ounces,” the company wrote in a statement.

- Commerce Secretary Wilbur Ross praised tariffs on steel and aluminum imports, reports Bloomberg, as his agency considers whether similar measures would boost the nation’s auto manufacturers. Should such a tariff be implemented the U.S. auto industry could raise car prices to consumers. Across the sea, China warned this week of a Canadian investment chill following the rejection of the Aecon Group takeover. “Prime Minister Justin Trudeau’s government on Wednesday killed a proposed Chinese takeover of the Toronto-based construction firm,” the article continues. Finally, back in the U.S., a nonprofit research center that analyzes government data found that the number of white-collar prosecutions is on track to hit a 20-year low under President Donald Trump.

- According to Bloomberg, the strong U.S. dollar is too much of a headwind for gold. As the yellow metal fell below $1,300 an ounce for the first time this year, hedge funds and other large speculators pared bullish bets on bullion to the lowest in more than two years, the article reads. This spurred the biggest weekly decline since December.

Opportunities

- The U.S. central bank released minutes of its policy meeting at the start of the month that could signal rising inflation. Bloomberg writes that by inserting the word “symmetric” a second time in the minutes “policy makers seemed to signal a relaxed view over the prospects of inflation moving above target in the coming months.” Joseph Song, senior U.S. economist at Bank of America Corp. said that “we’ve heard a lot of Fed officials say they were comfortable with an overshoot of inflation” above the central bank’s 2 percent target. Capital Economics writes that a rise in business inflation expectations has been more pronounced recently and that market-based measures of breakeven inflation compensation have also been rising significantly.

- Bloomberg reports that the temporary calm between the United States and China ended this week after President Trump announced a push for tariffs on imported cars and trucks, which would shake up the global auto industry. Japanese Trade Minister Hiroshige Seko said on Thursday that “imposing broad, comprehensive restrictions on such a large industry could cause confusion in world markets, and could lead to the breakdown of the multilateral trade system based on WTO rules.”

- Due to heightened geopolitical tensions and the renewal of U.S. sanctions on Iran, OPEC’s third-largest producer, the price of Brent crude has diverged from gold and copper, reports Bloomberg. Oil and gold generally move in the same direction due to their inflationary link. An ounce of gold currently buys the fewest barrels of oil since November 2014, perhaps indicating that some investors don’t expect inflation to rise and the noise in oil prices are only temporary. However, with such a divergence between the N.Y. Fed’s Underlying Inflation Gauge Full Data Set Measure, compounding at 13.21 percent trailing five years, and its Underlying Inflation Gauge Prices Only Measure only compounding at 1.94 percent over the same period, it might be better to bet on the full data set measure of future inflation.

Threats

- Emerging market companies and governments are struggling to deal with the rising cost of borrowing in dollars as a record slew of bonds become due, with some $249 billion needing to be repaid or refinanced through next year, reports Bloomberg. Mark Mobius, who is usually bullish on emerging markets, said that there is danger of contagion from the deteriorating situation in Turkey, plus Argentina and Brazil are not going well and may signal higher rates to come.

- Collateralized loan obligations (CLOs), or repackaged corporate loans are growing hugely in demand, with the biggest bond grader for CLOs, Moody’s Investors Service, unable keep up with demand for rating securities. Strong demand allows managers to sell CLOs with weaker protections and it makes the leveraged loans that get bundled into the securities riskier too, writes Bloomberg. Michael Temple, Amundi Pioneer’s direction of U.S. credit research, says that this “means a lot of CLOs have been stuffed with weaker credits” and that in a downturn “if and when that happens, will uncover these weaknesses.” Lu Wang of Bloomberg reports that signs are showing many U.S. stock investors are ill-prepared to deal with a margin call. The deficit of net cash in equity brokerage accounts just reached the widest ever of $317 billion, according to New York Stock Exchange data.

- European insurers’ standpoint is that U.S. Treasuries are cheap, but not cheap enough even with yields near multi-year highs. Bloomberg writes that AXA SA, the eurozone’s second biggest insurer, is spurning Treasuries in favor of bonds cheaper to hedge, such as those from Switzerland and Japan. Nicole Montoya, head of fixed income in Asia and the U.K. at AXA, said that “remaining exposed to FX volatility is more costly under Solvency II.” Solvency II is a European directive that came into effect in January 2016 stipulating that European insurers must have a capital requirement that protects foreign assets from a 25 percent price swing in the exchange rate. Investors have been piling into CCC rated bonds, some of weakest junk-rated companies, just two notches above default rating, and they have been returning 330 basis points in total this year, according to Bloomberg data. Premiums have fallen to their smallest since July 2014 on CCC bonds as investors are starving for income.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended May 25 was LatiumX, which gained 140.91 percent. This week, on May 22, crypto-enthusiasts remembered “Bitcoin Pizza Day,” reports Bloomberg. This date celebrates the first ever bitcoin transaction in 2008 of two pizzas for 10,000 coins. “At today’s price near $8,200 per bitcoin, you could get about 6.5 million $12.50 pizzas,” the article continues.

- Despite bitcoin’s sluggish start to the week, Rodrigo Marques, chief executive of Atlas Quantum (one of Brazil’s largest crypto trading platforms), is calling for a rally to $20,000, reports MarketWatch. Marques believes that the currency’s move under $8,000 was an interim low for bitcoin, saying that he expects the rise to $20k to hit within six months.

- Deutsche Boerse, owner of the Frankfurt Stock Exchange, is considering offering cryptocurrency products, writes Coindesk. Jeffrey Tessler, head of clients, products and core markets, spoke at an industry event on Wednesday and said that any move into the crypto space by the German company may not be immediately forthcoming, reports Bloomberg, but did claim, “We are deep at work with it.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended May 25 was Nexty, which lost 45.46 percent. According to Bloomberg, the Department of Justice is in the early stages of a criminal probe into whether traders are manipulating the price of bitcoin and other cryptocurrencies. Seeking Alpha reports that the investigation comes amid skepticism that exchanges are actively pursuing cheaters, wild price swings and a lack of regulations.

- Tom Lee, head of research at Fundstrat Global Advisors, predicted on May 7 that the price of bitcoin would rally during last week’s Consensus conference in New York. Unfortunately for Lee, bitcoin didn’t rally. In fact, Bloomberg reports that cryptocurrencies slumped about 10 percent during the past week and Lee admitted this in a report to clients last Friday.

- Bitcoin fell below $8,000 this week, reports Bloomberg, the lowest level in a month. According to the article, the digital currency is now down almost 20 percent since a May 4 peak, as of Wednesday morning.

Opportunities

- Argentina’s Banco Masventas reported that starting Monday, it has enabled customers to send cross-border payments using bitcoin, reports CoinDesk. The payment system is made possible through the bank’s partnership with Latin America-focused exchange startup Bitex. Manuel Beaudroit, Bitex chief marketing officer, told CoinDesk that the startup believes this marks the first time that a domestic bank has adopted bitcoin for cross-border payments, the article continues.

- Cryptocurrency investor Brian Kelly, who is also the founder and CEO of BKCM (investment firm focused on digital currencies), said Monday that bitcoin cash is the “must-own” digital currency at the moment, reports CNBC. Bitcoin cash miners met recently to discuss funding for a bitcoin cash development fund, Kelly told CNBC, in which miners are “going to take some of the rewards they get from mining and put it in a fund to build stuff on top of bitcoin cash.” Kelly added, “that’s how blockchains gain value.”

- The Commodities Futures Trading Commission (CFTC) has issued guidelines for listing virtual currency derivative products for exchanges and clearinghouses registered with the CTFC, reports Seeking Alpha. According to the article, the advisory addresses areas such as enhanced market surveillance, large trader reporting and outreach to member and market participants.

Threats

- The Pentagon is struggling with whether or not to flag cryptocurrencies as risky, reports Bloomberg News. As it works to recruit a more “tech-savvy workforce,” it’s facing the confusion of what to make of people who invest or trade bitcoin. “The question is whether owning bitcoins or lesser-known cryptocurrencies such as Ripple and Ethereum is an indicator of risky personal behavior – one that should flag extra scrutiny in security clearances – or just another investment choice,” the article reads.

- As the economic crisis deepens in Venezuela, bitcoin mining has exploded, reports Bloomberg. However, according to one businessman on this week’s “Decrypted” podcast, once he started to mine bitcoin after seeking other ways of making money, authorities raided his office. In fact, he said the police tried to extort him – forcing him to flee the country altogether.

- Joe Davis, a senior economist at the Vanguard Group, wrote in an op-ed this week that bitcoin is not a currency, makes for a poor investment choice, and its biggest threats are the very institutions it was meant to overthrow. According to MarketWatch, Davis argues that bitcoin does not meet the criteria of a currency, arguing that it’s dubious medium of exchange and its excessive volatility does not make it a suitable store of value. “As for bitcoin the currency? I see a decent probability that its price goes to zero,” he wrote.

Energy and Natural Resources Market

Strengths

- Natural gas was the best performing major commodity this week rising 2.95 percent. The commodity rallied after hotter-than-normal weather patterns are expected across most of U.S. until June 3.

- The best performing sector this week was the S&P/TSX Composite Gold Index. The index rose 1.91 percent after gold posted its biggest weekly increase in two months.

- The best performing stock for the week was Novatek PJSC. The Russian gas producer rose 7.31 percent after Total SA announced it would take a 10 percent stake in Novatek’s multibillion dollar liquefied natural gas project in Russia.

Weaknesses

- Crude oil was the worst performing commodity this week. The commodity fell 5.11 percent, the worst weekly drop in at least two months after Saudi oil minister Al-Falih stated that OPEC and its allies were "likely" to boost crude output in the second half of the year.

- The worst performing sector this week was the S&P/TSX Oil & Gas Exploration and Production Index. The index dropped 6.86 percent after crude prices posted a large weekly drop.

- The worst performing stock for the week was Petrobras SA. The Brazilian integrated oil major dropped 21.93 after a nationwide truckers strike in Brazil led to a presidential order that will force Petrobras to freeze diesel prices and backtrack on plans to move to a market-based fuel pricing policy.

Opportunities

- The recent U.S. dollar rally that may have hurt commodities is likely to be over, according to Bloomberg’s Mark Cudmore. According to the recently published analysis, the greater-than-4-percent rally in the currency has run its course suggesting the U.S. dollar may resume its longer-term downtrend. A weaker U.S. dollar may result in a tailwind for commodity prices.

- There are plenty of reasons to be bullish on copper, according to a lengthy analysis published by Bank of Montreal. According to the report, growth rates will be driven by electric vehicles and renewable energy, somewhat decoupling the narrative from the overall China growth story. Additionally, the report highlights the copper project pipeline is at the lowest level we have seen this century.

- Gold posted its biggest weekly increase in two months as traders reacted to new global political developments, beginning with the cooling of expectations from the U.S. and North Korea summit, while seeing increasing physical coin demand as emerging markets from Argentina to Turkey see their currency values drop drastically.

Threats

- OPEC and Russia are discussing gradually boosting oil production in the second half. There are a couple of options up for debate before the group`s meeting at the end of June. Producers are debating an increase ranging from 300,000 barrels per day, a larger increase of about 800,000 barrels per day favored by Russia. The increase in production may stifle the recent spike in crude prices.

- President Trump ordered an investigation into whether auto imports weaken the U.S. economy and threaten national security. The move may trigger new tariffs on foreign cars and inflame trade tensions with allies such as Japan, Germany, Canada and Mexico. The headlines could negatively impact aluminum and other key raw materials that feed the automakers’ supply chain.

- Industrial metals used for property construction tumbled this week after market participants claimed China may unveil further property control measures. Regulators in China are said to be preparing statements that will seek to guide property prices lower in the coming weeks, a move that may impair the growth rate in the property construction sector.

China Region

Strengths

- Thailand’s GDP came in at a 4.8 percent growth rate for the first quarter, ahead of expectations for a 4.0 percent pace and better than the prior quarter’s 4.0 percent pace.

- Singapore’s GDP growth game in slightly better than expected for the first quarter. Actual numbers for year-over-year first quarter growth were in line at 4.4 percent, but quarter-over-quarter growth clocked in at 1.7 percent, ahead of estimates for 1.6 and up from the prior quarter’s pace of 1.4 percent. Additionally, Singapore’s year-over-year industrial production beat as well, notching up a 9.1 percent showing for the April measurement period, better than analysts’ anticipated 8.0 percent print.

- Taiwan’s export orders for the April measurement period came in up 9.8 percent, beating expectations for a 7.9 percent and higher than March’s pace of 3.1 percent.

Weaknesses

- Energy was the worst-performing sector in the Hang Seng Composite Index, tumbling by 8.41 percent this week as OPEC discussions revealed possible production boosts amid declining energy prices.

- Hardware producer Ju Teng International Holdings (3336 HK) fell 12.77 percent since the close of last Friday’s trading, making new 52-week lows.

- Indonesia has continued to see outflows this month, Bloomberg News reports in an assessment of the iShares MSCI Indonesia ETF. The article observes outflows of more than $79 million, and notes that Indonesia’s Jakarta Composite is Asia’s second-worst-performing index year to date. While the central bank did step in this week to try to calm fears, upcoming local elections, U.S. dollar strength and higher energy prices have all served to weigh upon the index.

Opportunities

- Following high level trade talks in the United States last weekend, the U.S. and China announced a trade “truce” of sorts, with “both parties hav[ing] agreed to suspend the tariffs,” as Secretary of the Treasury Steven Mnuchin said on Monday. China announced plans to continue to ramp up purchases of American goods, is following through on cutting tariffs on imported vehicles to China, and announced plans to reduce import duties on a wide range of other various consumer goods. Secretary of Commerce Wilbur Ross is set to head to China for more talks in early June. To be sure, there remains a lot of work to be done—the fate of ZTE, in particular, hangs in the balance (representative, in a way, of U.S. concerns on intellectual property and Chinese concerns about sudden, dramatic and disruptive U.S. actions)—but the fact remains that the U.S. and China have, for the moment, established something of a framework and a (relatively) more positive tone on the subject of trade.

- Hon Hai’s Foxconn Industrial arm, which is aiming for a $4.3 billion IPO in China, is reportedly already heavily oversubscribed. The IPO is on track to be China’s largest since the 2015 stock market crash.

- China is reportedly planning to do away with birth limits, press reports suggested this week, which would end a long-standing policy only recently (2015) relaxed to two children.

China has an increasingly older demographic and last year €”even with a two-child policy in place €”births actually declined.

Threats

- Trade talks with China remain in the forefront of investors’ minds. And while we did get some mildly encouraging progress this week (see the trade “truce” bullet above), it also remains possible that, as one WSJ article title put it this week, “U.S.-China Trade Tensions Represent the New Normal.” This could create real or perceived uncertainty, which could weigh on markets or exacerbate headline risk.

- The issue of U.S. dollar strength—and the question over whether said strength will persist—continues to loom large for emerging markets.

- North Korea is still North Korea, and so remains something of a wildcard. Despite a visit to the U.S. by South Korean President Moon this week, at the start of the week the Trump administration walked back expectations for the scheduled June 12 summit, later going so far as questioning whether the summit would still take place, and indeed, by Thursday morning—following a hike in negative rhetoric from North Korea—President Trump cancelled the summit altogether even as he left the door open to talks in the future. There remain promising hints of what could be—more dialogue, a recent release of American prisoners, and the voluntary destruction of some nuclear facilities by North Korea, to name a few of the most prominent recent events—and indeed, the President affirmed his desire to meet Kim Jong Un in the publicly-released letter sent to the North Korean. But there is no longer any imminent summit. (Or is there? By late Friday afternoon, President Trump suggested the summit could indeed still be on, perhaps even on June 12. Only time will tell.)

Emerging Europe

Strengths

- The Czech Republic was the best performing country this week, gaining 1.2 percent. Moneta Bank was the best performing equity trading on the Prague exchange, gaining more than 2 percent. Moneta announced an extraordinary gain of CZK 110M from the sale of non-performing loans in the month of April and May. Management expects profits for the whole year from the sale of non-performing loans for CZK 750M, reaching CZK 475M in the first quarter.

- The Russian ruble was the best performing currency this week, gaining 5 basis points against the U.S. dollar. The Russian currency continues its rebound in May after a sharp decline in April. This month, the currency has been supported by higher oil prices.

- Information technology was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 3.5 percent. The banking index lost more than 4 percent in the past five years. The Greek economy remains among the world’s least competitive, despite reforms and fiscal policy changes, according to the 2018 International Institute for Management Development (IMD) World Competitiveness Ranking published on Thursday. Greece ranked 57 among 63 countries, taking the same position as last year.

- The Turkish lira was the worst performing currency this week, losing 4.8 percent against the U.S. dollar. Turkey’s central bank raised its late liquidity window rate by 300 basis points to 16.5 percent on Wednesday, but the decision to boost interest rates at Wednesday’s emergency meeting did not support the lira for long. The currency continues to weaken before the scheduled snap election in June.

- Real estate was the worst performing sector among eastern European markets this week.

Opportunities

- Greece and its international creditors have reached an initial agreement on the reforms Athens must adopt in order to complete the fourth bailout review. After the fourth review is complete, discussions on the debt relief will start, paving way for Greece to exit its eight-year bailout program later in the summer.

- In Russia, disposable incomes and real wages jumped more than expected in April, helping fuel a 2.4 percent increase in retail sales. Real disposable income increased 5.7 percent in April, compared with upwardly revised expansion by 4.5 percent in the previous month, the Federal Statistics Service reported on Tuesday. Inflation-adjusted wages jumped 7.8 percent.

- Next week, final May inflation for the eurozone will be released. Most Bloomberg economists predict a pickup in inflation. May CPI is expected to rise to 1.6 percent, above the prior reading of 1.2 percent. The core inflation should spike to 1 percent from 0.70 basis points.

Threats

- Business activity in the eurozone slowed in May more sharply than expected. The Flash Markit Eurozone Composite Purchasing Managers Index fell to 54.1 in May from 55.1 in April, an 18-month low, but still above the 50 level that separates contraction from expansion. Manufacturing PMI fell to 55.5 from 56.2, and the Service PMI dropped to 53.9 from 54.7.

- U.S. officials are discussing a 25 percent tax on imported cars and trucks. According to an article from The Economic Times, roughly 12 million cars and trucks were produced in the United States last year, while the country imported 8.3 million vehicles worth $192 billion. The United States is the second-biggest export destination for German auto manufacturers after China, while vehicles and car parts are Germany's biggest source of export income. More tariffs will further strain relations between the U.S. and Europe. Steel and aluminum tariffs are set to hit the European Union on June 1.

- The 300 basis point hike in Turkey announced this week was not enough to support the falling currency. President of Turkey, Recep Tayyip Erdogan, announced he will lower rates after he wins the snap election next month. Dovish rate policy will further put pressure on the already weak currency.

May 23, 2018Yields Look Overextended and Ready for Mean Reversion |

May 21, 2018Blockchain Will Revolutionize How We Mine Precious Metals |

May 18, 2018Consensus 2018 Conference Recap |

|||

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All