Too Many Trillions

Rapid Maturity

Leverage Plus Leverage

Circling Vultures

NYC, St. Louis, Maine, Beaver Creek, Cleveland, Gloucester, and Newport

Rather go to bed without dinner than to rise in debt.

—Benjamin Franklin

What can be added to the happiness of a man who is in health, out of debt, and has a clear conscience?

—Adam Smith

There are no shortcuts when it comes to getting out of debt.

—Dave Ramsey

Modern slaves are not in chains, they are in debt.

—Anonymous

Debt isn’t always a form of slavery, but those old sayings didn’t come from nowhere. You can find hundreds of quotes on the Internet discussing the problems of debt. Debt traps borrowers, lenders, and innocent bystanders, too. If debt were a drug, we would demand it be outlawed.

The advantage of debt is it lets you bring the future into the present, buying things you couldn’t afford if you had to pay full price now. This can be good or bad, depending on what you buy. Going into debt for education that will raise your income, or for factory equipment that will increase your output, can be positive. Debt for a tropical vacation, probably not.

And that’s our core economic problem. The entire world went into debt for the equivalent of tropical vacations and, having now enjoyed them, realizes it must pay the bill. The resources to do so do not yet exist. So, in the time-honored tradition of lenders everywhere, we extend and pretend. But with our ability to pretend almost gone, we’re heading to the Great Reset.

I’ve been analogizing our fate to a train wreck you know is coming but are powerless to stop. You look away because watching the disaster hurts, but it happens anyway. That’s where we are, like it or not.

And we don’t even really like to talk about it in polite circles. In a private email conversation this week, which must remain anonymous, this pithy line jumped out at me:

The total of Federal (remember they do not use GAAP) debt, state debt, and city debt [unfunded liabilities included] exceeds $200 trillion dollars. There is no set of math that works to pay this off. Let me be sure it’s heard by repeating it: There is no set of math that works to pay this off. Therefore, there has to be some form of remediation. This conversation is uncomfortable, so it is avoided.

Today’s letter is chapter 5 in my Train Crash series. If you’re just joining us, here are links to help you catch up.

Last week, we discussed the Italian political crisis and potential eurozone breakdown. That is a dangerous possibility, but far from the only one. As we’ll see today, the world has so much debt that the cracks could happen anywhere.

I said above that if debt were a drug, we would outlaw it. But we also know that people get hooked on illegal drugs all the time. The law doesn’t stop them. Likewise, common sense and regulations don’t stop us from overusing debt. And as we will see, the withdrawal can be painful indeed.

First, a quick announcement. If you have any interest in the mining and energy resource sectors, be on the lookout for an email from my partner, Ed D’Agostino. He is going to interview one of the top speakers from my Strategic Investment Conference—Marin Katusa. Marin is an expert in the resource sector and he impressed the crowd at the SIC with his sector knowledge. You’ll want to hear what Marin has to say.

I’ve followed Marin’s career for the last fifteen years, and I greatly respect his opinion of the mining and energy resource sector. I encourage you to listen in on Ed’s interview.

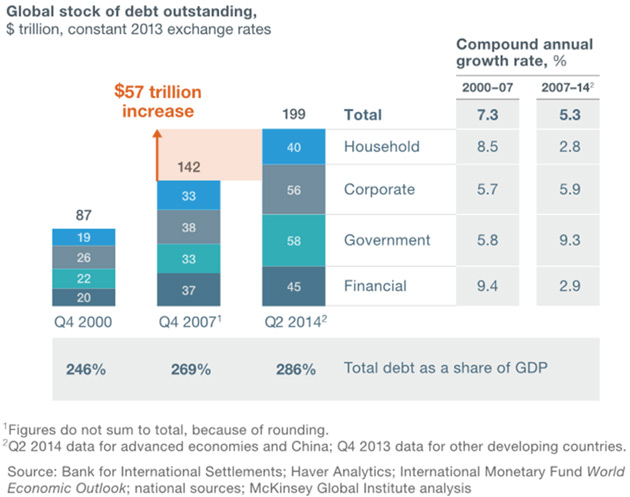

Too Many Trillions

Three years ago, the McKinsey Global Institute released a massive research report called Debt and (not much) Deleveraging. It reviewed the global debt situation and where it might be taking us. The answers were not pleasant. I wrote about it at the time in Living in a Free-Lunch World.

The McKinsey team created this fascinating graphic summing up the world debt situation as of mid-2014.

Source: McKinsey Global Institute

From the Great Recession’s beginning through Q2 2014, global debt grew $57 trillion to $199T. (From here on, I will use capital T to denote trillions, since we must use the word distressingly often). That includes household, corporate, government, and financial debt. It does not include unfunded liabilities.

Dr. Woody Brock wrote this week:

CBO projections show that within 18 years, entitlements spending will absorb all US federal tax revenues—leaving no revenues even for interest expense on the debt and for the military. In Germany, which proudly pays annually for its expenditures without incurring debt, Deutsche Bank has estimated that by 2045, income tax rates of 80% (total, not marginal rates) would be needed for its PAYGO system. The entire workforce of the nation would be in bondage to the elderly. Other nations face even worse prospects.

I should note that the CBO projections assume no recessions and an optimistic compound 3% growth rate. I think most of my readers would assume that neither will end up being the case.

But even $199T back in 2014 was a lot of money. We should also note that, through the magic of double-entry accounting, each dollar of debt liability appears on someone else’s balance sheet as a $1 asset. Debt is wealth, if you are the lender. Most of you reading this probably are, in some fashion.

(If we could somehow make this debt magically disappear, we would also make wealth disappear, but we may have to do exactly that. This is a serious problem we will address later in this series. For now, just note that I am aware of it.)

McKinsey calculated that from 2007–2014, world debt levels grew at a 5.3% compound annual growth rate. That was slower than the previous seven years but still considerably faster than the world economy grew. Hence, debt as a share of world GDP rose to 286%.

Not all the debt categories grew equally. Government debt grew far faster than household, corporate, or financial debt. Household debt growth fell to a relative crawl, from 8.5% annual growth in 2000–2007 to only 2.8% in 2007–2014. Which makes sense because families had little choice but to deleverage, often via bankruptcy.

Government and corporate borrowers faced no such pressure. Their debt kept growing at a slightly higher pace after the recession. Yes, some corporations hunkered down and rebuilt their balance sheets. Most did not. They kept borrowing and lenders kept lending, encouraged by central bank-generated liquidity.

This is an important point I’ll return to in future letters. We talk a lot about profligate governments running up debt, and rightly so, but they are not alone. Businesses are equally and sometimes more addicted to debt. That would be fine and even positive if it were funding innovation and new production. But much of this new corporate debt paid instead for share buybacks that reduce equity, leaving the corporation more leveraged. That seems to be what shareholders want. They should beware what they wish for.

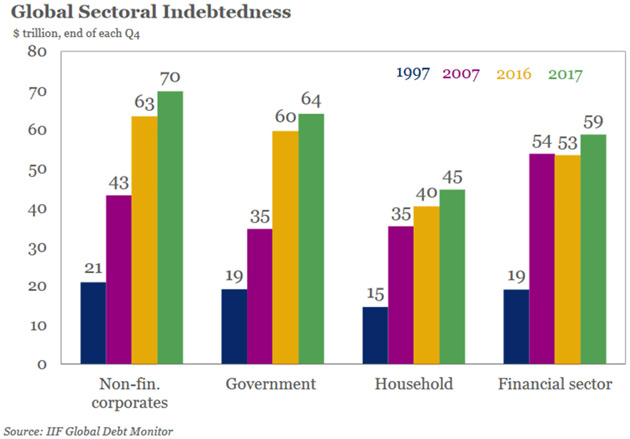

Rapid Maturity

As far as I know, McKinsey has not updated that 2015 report, but we can get similar data from the Institute for International Finance’s Global Debt Monitor.

The totals aren’t the same as McKinsey showed for those years, so I suspect they have different data sources. They’re close enough for our purposes, though.

Adding together the same-colored bars, we get these global debt totals:

If those are accurate and my math is right, global debt grew at an 8.5% compound rate from 1997 to 2007. Then it slowed to 3.6% from 2007 through 2017. That’s good. We went on a worldwide debt diet.

But last year, we appear to have binged because debt grew 10.2% from 2016 to 2017. Breaking it down by sector, non-financial corporate debt grew 11.1%, government debt grew 6.7%, household debt grew 12.5%, and financial sector debt grew 11.3%, all in calendar 2017.

Looking only at 2017, government debt seems to be the least of our problems. The biggest debt growth was everywhere else. But why did it suddenly accelerate last year? In part, because the world economy grew enough to let global debt-to-GDP ratios fall slightly.

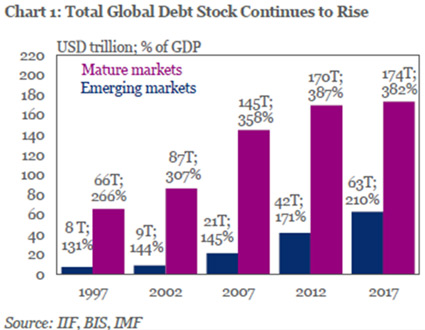

Here’s another IIF chart showing global debt as a percentage of GDP for both “mature” (what they call developed countries) and emerging markets:

The developed world is far more leveraged than the EM world, but EM countries are no pikers at 210%. They often lack the stabilizing resources developed countries possess, too. IIF points to Argentina, Nigeria, Turkey, and China for the largest debt ratio increases last year. But many emerging market businesses and financial companies borrowed money in dollars, as the dollar was relatively weak and US interest rates ridiculously low. Further, our yield-hungry investors, both as individuals and its institutions, were more than willing to lend to them to get something more than 1–2% that they could from sovereign bonds.

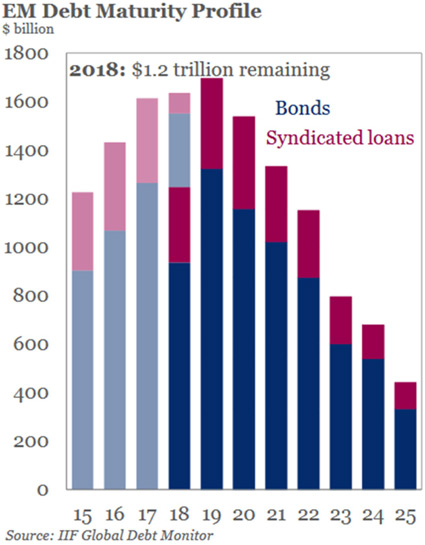

This level of emerging market debt is unsustainable because, among other reasons, debt matures and must be either repaid or refinanced. Here’s emerging market debt by maturity:

Some $4.8T in emerging market debt matures from this year through 2020, much of which will need to be rolled over at generally higher rates and, if USD strength continues, in a disadvantageous currency environment. Will that be possible? I don’t know, but we’re going to find out—possibly the hard way.

But that’s a relatively minor concern. We have a much bigger one back home.

Leverage Plus Leverage

The IIF report includes this note about US corporate debt:

US non-financial corporate debt hit a post-crisis high of 72% of GDP: At around $14.5 trillion in 2017, non-financial corporate sector debt was $810 billion higher than it was a year ago, with 60% of the rise stemming from new bank loan creation. At present, bond financing accounts for 43% of outstanding debt with an average maturity of 15 years vs. the average maturity of 2.1 years for US business loans. This implies roughly around $3.8 trillion of loan repayment per year. Against this backdrop, rising interest rates will add pressure on corporates with large refinancing needs.

I see at least three alarming points in this paragraph.

First, corporate debt is now 72% of GDP. That’s in addition to the government debt that is approaching (or has passed depending on how you count debt) 100% of GDP and household debt at 77% of GDP. Add in 81% financial sector debt, and the US combined debt-to-GDP ratio is near 330%.

Second, 60% of new corporate debt is coming not from bond sales but new bank loans—and those bank loans have much shorter maturity, averaging 2.1 years. That means refinancing time is coming for much of it, and rates are not going lower.

Third, IIF infers about $3.8T in corporate loan repayments each year—just in the US. That’s a lot of cash companies need to find and I’m not sure all can do it. Aside from higher interest rates, the companies that need credit (as opposed to high-rated ones that borrow only because they can do it cheaply) tend to be riskier.

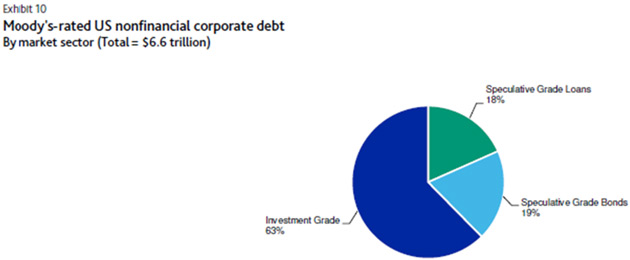

From a recent Moody’s report, we see that 37% of US nonfinancial corporate debt is below investment grade. That’s about $2.4T.

Source: Moody's Investors Services

The proportion is similar globally. Furthermore, all corporations, both investment grade and speculative, added significantly more leverage since the Great Recession.

Again, not all leverage is the same. Some companies borrowed to fund share buybacks but have vast cash flow and reserves. They can easily deleverage if necessary. Smaller, riskier companies have no such choice. I think they present the greatest systemic risk.

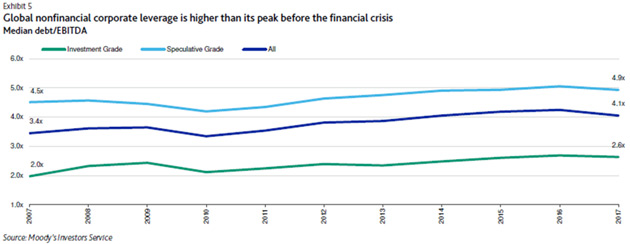

That said, it’s still a bit mind-boggling that, even after the Great Recession, just a decade later the average non-financial business went from 3.4x leverage to 4.1x. They are now roughly 20% more leveraged than they were the last time all hell broke loose. CEOs and boards seem to have learned little from the experience—or maybe learned too much. If you believe the Fed has your back, then leveraging to the moon makes sense.

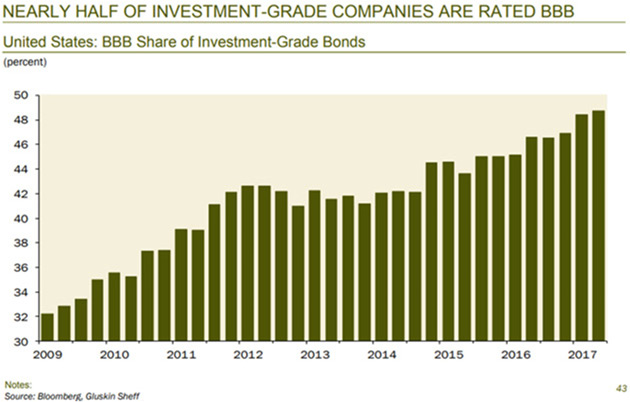

Now, I know some readers will take comfort in the fact that 63% of the corporate debt is rated investment grade. But as they say in Texas, hold on, cowboy, don’t ride away so fast. A lot of that debt is rated BBB, the lowest investment grade rating. For the glass half-empty crowd, that means they are just one step above junk. The chart below from my friend Rosie (David Rosenberg) shows that the number of BBB-rated companies is up 50% since 2009.

Source: David Rosenberg

The problem, as I described in High Yield Train Wreck, is that bondholders and lenders won’t wait for the rescuers. When funds and ETFs, which hold BBB debt, start getting redemptions, investors won’t hang around to see which domino falls next. Institutions have rules that will make them start selling troubled bonds early. Liquidity probably won’t be there. Clearing the market will require sharply lower prices, which will create more selling pressure and eventually recession.

To further exacerbate the problem, the rating agencies that didn’t react quick enough in 2008 may be a little bit more trigger-happy this time. This will cause heartburn for CEOs with BBB paper outstanding.

To be sure, regulators and Congress took measures to avoid a similar crisis repeating. The banks aren’t the problem. The “shadow banking system” is the source for much of the shaky debt. The same investors stretching for yield in emerging markets have loaded up on private debt, too.

Steve Wasserman’s last weekly commentary is a good capstone here:

Moody’s has issued a statement that CMBS loans are now almost as risky as in 2007 because 75% of them are interest only, and the interest only period is now 6 years, up from 2.2 years just a few years ago. In addition, they are becoming much more covenant light, and are at higher leverage. All of this is a red flag since these things create much more risk of serious problems when the recession hits. There is also a bigger concentration of single tenant properties, which, as we have seen in retail, can be deadly in a recession. Asset and sponsor quality is also deteriorating. There is now so much competition to put out loans by so many non-bank sources, that borrowers can get lenders to compete, which always means lower quality underwriting. Far too much capital chasing too few good deals.

Underwriting is not nearly as bad as in 2006–2007 yet, but it appears the trend is what it always has been, when the economy is strong and there is too much capital, underwriting standards fall down, and then the stage is set for a bad outcome when the economy goes bad. It is typically 10–12 years between collapse of the last crash and then credit quality deterioration and the next credit collapse. We are at 10 years. Dodd Frank had rules to try to avoid a replay of 2008 in CMBS, but a lot of loans now are made by private equity funds that are not subject to these regulations.

One thing that is immutable is that as each generation comes into Wall Street, they think they know better how to do it, and they eventually do the same dumb loans in pursuit of profits and bonuses. It has never been different. We are not about to have a major crash again, but CMBS loan quality is deteriorating now, and one day in the next 2–3 years, it will be a bad problem. When they start doing a lot of CDOs and virtual CMBS pools with derivatives, then that is a sure sign the end is near.

I think Steve pretty much has it right. We’re ok for now, but we will have a problem when recession strikes. The next crisis, which I think will be yet another debt crisis, won’t look like the last one, but it will rhyme.

Circling Vultures

As in nature, carnage for some is opportunity for others. Investment bankers who specialize in corporate liquidations and restructuring see good times coming. Here’s a haunting quote from last month:

"I do think we're all feeling like we were back in 2007," Bill Derrough, the co-head of recapitalization and restructuring at Moelis & Co., told Business Insider. "There was sort of a smell in the air; there were some crazy deals getting done. You just knew it was a matter of time."

A matter of time, indeed. Moelis and others are confident enough to start staffing up before the business appears, despite the tight labor market. Think about how unusual this is. Most companies are in a just-in-time, fully-optimized production mode. You succeed by precisely matching production capacity with current sales… unless you are a restructuring specialist. In that case, you hire the best people you can find and let them twiddle their thumbs until opportunities appear. And you think they will, soon.

Others will have opportunity as well—even you, if you are holding cash and in position to buy some of the valuable assets that will get “restructured” in the next few years. Doing it successfully will take extensive research and iron discipline. Many will try, few will do it well. Start preparing now and you may be one of the few.

Remember, in 2009, it was easy to find great companies paying 4% to 6% dividends with single digit P/E ratios. You didn’t have to be an accredited investor to pick up juicy returns. You will get another chance not too many years from now. Patience, grasshopper.

NYC, St. Louis, Maine, Beaver Creek, Cleveland, Gloucester, and Newport

I know, I know. I said I wasn’t traveling in June and July. Except for when things came up, and they have.

After I finished my last letter, I found out I had to be in Boston on Tuesday morning very early, flying in the night before and then back home the next night. Now I have to be in New York Monday evening and back in Dallas Tuesday afternoon. Then I must go to St. Louis for a day, too.

In August, I go to Grand Lake Stream, Maine for the Camp Kotok economists gathering/fishing trip. Then I have an Ashford, Inc. board meeting in Beaver Creek where Shane and I will spend an extra couple of days at the Ashford-owned Grand Park Hyatt. At some point, Shane and I go to Cleveland for an executive checkup with Dr. Mike Roizen. Mike West of BioTime and Patrick Cox will be there, too. Besides getting rather aggressive all-day physicals, you can imagine we will have some fascinating health and aging conversations.

Speaking of Mike R., we are pulling for a miracle comeback by the Cavaliers. A game six in Cleveland will make everything in my world stop so I can be there to be on the floor with Mike. Sometimes a man just has priorities.

Then after Maine, we will spend a couple days in Gloucester with Woody Brock followed by a leisurely trip down to Newport, Rhode Island to see my great friend Steve Cucchiaro, now of 3Edge and Windhaven fame, and his fiancé.

Recently, my daughter Tiffani had a different type of celebration with her daughter (my granddaughter), Lively. They celebrate Lively’s “half birthday” exactly halfway through the year from her last birthday. It turns out the Ritz has a young girl package that makes for a very special day. Tiffani sent me a video as Lively opened her “half birthday” present: the new Taylor Swift album, which made her very happy. But tucked inside it were tickets to the upcoming Taylor Swift concert and Lively practically exploded with excitement. Who knew? Thankfully, there weren’t tickets for Papa John (as she calls me). I’m not sure I could handle 20,000 screaming young girls while listening to Taylor Swift’s music at the same time.

But you know what? Seeing the excitement in her eyes, I would’ve steeled myself and gone into that breach just to see that look again! Tomorrow, I will accompany that excited young girl to the Nasher Sculpture Museum with her mother. It would be a dream if she can be just as excited with Rodin.

And with a smile on my face, I will hit the send button. You have a great week! Hopefully there is a young one that can light up your life as well, or an old friend.

Your much rather deal with a Taylor Swift concert than The Great Reset analyst,

John Mauldin

[email protected]

© Mauldin Economics

www.mauldineconomics.com

© Mauldin Economics

Read more commentaries by Mauldin Economics