The U.S. inflation story made further inroads this month, with year-over-year price growth for consumers and producers alike hitting multiyear highs. U.S. consumer prices expanded at their strongest pace in more than six years, climbing to an annual change of 2.8 percent in May. Prices for final demand goods, meanwhile, grew 3.1 percent, their strongest annual surge since December 2011.

As you might expect, energy was the greatest contributor to higher prices in May, with fuel oil jumping more than 25 percent from the same month a year ago. The current average price for a gallon of regular gas nationwide was just under $3.00, compared to only $2.33 in June 2017, according to the American Automobile Association (AAA).

Inflation is set to get an even bigger jolt now that President Donald Trump has formally approved 25 percent tariffs on as much as $50 billion of Chinese goods. In response, China has vowed retaliatory action. While I agree some targeted tariffs are welcome to address intellectual property theft, tariffs at the wholesale level are essentially regulations that threaten to undermine all the work Trump has done to supercharge the U.S. economy. They act as headwinds to further growth, which in turn makes gold look attractive as a safe haven investment.

Blaming OPEC

Let’s return to energy for a moment. Hot off the success of his historic summit with North Korea leader Kim Jong-un, Trump took a stab at foreign oil producers this week, tweeting: “Oil prices are too high, OPEC is at it again. Not good!”

The president isn’t wrong, but I believe he may be overselling the Organization of Petroleum Exporting Countries’ influence here. In May, the 14-member cartel added an extra 35,000 barrels per day (bpd) in output compared to the previous month, to reach a total of 31.8 million bpd. This is down from the average 32.6 million and 32.4 million bpd OPEC collectively produced in 2016 and 2017.

Venezuela’s output deteriorated once again, falling more than 42 percent in May to 1.4 million bpd, which is less than half of what it produced 20 years ago.

The beleaguered South American country didn’t have the biggest monthly decline among OPEC members, however—that title belonged to Nigeria, which saw its April-to-May production tumble 53.5 percent to 1.7 million bpd. Analysts predict output could fall further to 1.4 million bpd by July—a level not seen since 1988—as the country’s Nembe Creek Trunk Line (NCTL) has had to be closed recently to address product theft along its route.

OPEC will meet later this month and is widely expected to loosen production curbs as global demand strengthens. In the meantime, the U.S. continues to pump even more oil on a monthly basis, and by 2019 it could be producing more than 11 million bpd for the first time ever. This would make it the world’s top oil producer, above Russia.

Want to learn more? Watch this brief video featuring Samuel Pelaez, who outlines the six factors we use to select best-in-class oil and gas exploration and production companies!

Gold Glitters on Inflation Fears and U.S. Budget Imbalance

The inflation news helped support the price of gold, which traded as high as $1,309 an ounce Thursday, its best intraday showing in four weeks.

The price jump came a day after the Federal Reserve lifted interest rates another 0.25 percent, the second time it has done so this year. Although rising rates have historically made the precious metal look less competitive, since it doesn’t offer a yield, gold markets could be forecasting slower economic growth as a result of higher borrowing costs, not to mention costlier servicing of corporate and government debt.

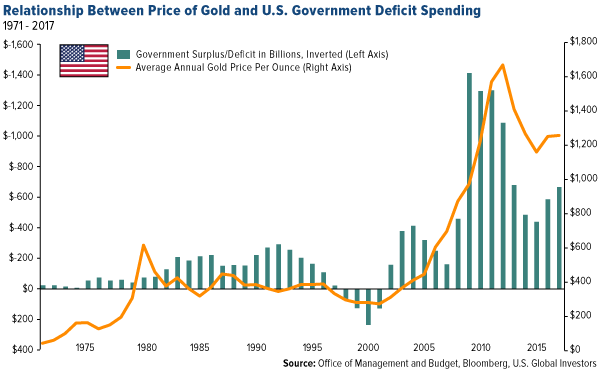

On that note, the Treasury Department announced this week that in the first eight months of the current fiscal year—October through May—the U.S. government deficit widened to a whopping $532 billion, or 23 percent more than the same eight-year period a year ago. That’s already more than the total deficits in fiscal years 2014 and 2015. Because of higher spending and lower revenues, it’s estimated that the deficit by the end of the fiscal year will balloon to $833 billion, which would be the greatest amount since 2012.

I believe this makes the investment case for gold and gold equities even more appealing as a store of value. In the chart below, notice how the price of gold has responded to government spending. I inverted the bars, representing surplus and deficit, to make the relationship more clear. In the years following the Clinton surplus of the late 90s, the difference between expenditure and revenue surged to new record amounts on the back of military spending in the Middle East and the multibillion-dollar bailouts of financial firms during the subprime mortgage crisis. Consequentially, the price of gold exploded.

Learn more about what’s driving the price of gold right now by clicking here!

How Close Are We to the End of the Business Cycle?

But back to the Fed. Besides lifting rates, the central bank has also signaled that we can expect two more hikes in 2018, suggesting it sees less and less need to accommodate a booming U.S. economy. Since the start of this particular rate hike cycle two and a half years ago, we haven’t yet seen four increases in a single calendar year.

This raises the question of how close we are to the end of the business cycle.

Rising rates, among other indicators, have often preceded the end of economic expansions and equity bull markets. Among other telltale signs: a flattening yield curve, record corporate and household debt, an overheated jobs market and increased mergers and acquisition (M&A) activity. So far this year, the value of global M&As has already reached $2 trillion, a new all-time high. The last two periods when M&As reached similar levels were in 2007 ($1.8 trillion) and in 2000 ($1.5 trillion), according to Reuters. Careful readers will note that those two years came immediately before the financial crisis and tech bubble.

Now, the world’s largest hedge fund, Bridgewater Associates, has reportedly turned bearish on “almost all financial assets,” according to one of its most recent notes to investors.

In the firm’s Daily Observations, co-CIO Greg Jensen writes that “2019 is setting up to be a dangerous year, as the fiscal stimulus rolls off while the impact of the Fed’s tightening will be peaking.”

Don’t Miss the Opportunities

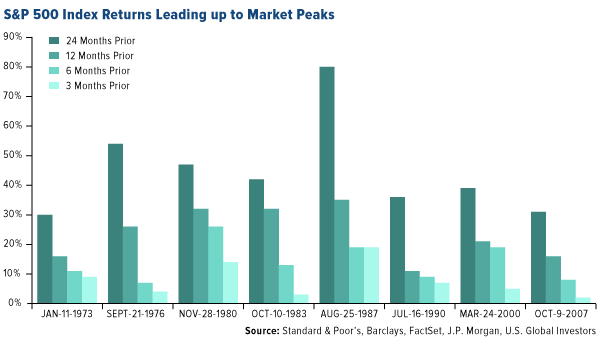

Be that as it may, calling the end of the cycle would be a fool’s errand and could result in missed opportunities, as J.P. Morgan’s Samantha Azzarello points out in a recent note to investors. Late-cycle returns can still be quite substantial, she says. Take a look at the chart below, which highlights returns 24 months, 12 months, six months and three months leading up to the past eight market peaks. Obviously returns were higher in the longer-term periods, but even the three-month periods delivered some attractive returns—returns that would be left on the table if skittish investors exited now. According to Azzarello, it’s important to “rebalance, stick to a plan and remember: get invested and stay invested.”

<

As further proof that many investors still see plenty of fuel in the tank, the June survey of fund managers conducted by Bank of America Merrill Lynch (BAML) found that equity investors are overweight U.S. stocks for the first time in 15 months. Commodity allocations are at their highest in eight years. And two-thirds of managers say the U.S. is the best region in the world right now for corporate profits, which is at a 17-year high.

That’s not to say there aren’t risks, however. Forty-two percent of survey participants said they believed corporations were overleveraged. That’s well above the peak of 32 percent from soon before the start of the financial crisis. Fund managers cited “trade war” as the biggest “tail risk” for markets at present.

This is largely why we find domestic-focused small to mid-cap stocks so attractive right now. These firms are well positioned to take advantage of Trump’s high-growth “America first” policies, yet because they don’t have as much exposure to foreign markets, they bypass many of the trade war pitfalls large multinationals must face. Since Election Day 2016, the small-cap Russell 2000 Index has outperformed the large-cap S&P 500 Index by more than 8.5 percent.

Get the scoop on small to mid-cap stocks by clicking here!

Rethinking Market Cap-Weighting

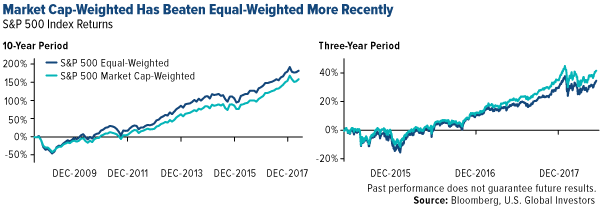

On a final note, I want to draw attention to a change we’ve observed in S&P 500 returns—specifically, the difference in performance between an equal-weighted basket of stocks and one that’s market cap-weighted. For the longer-term period, equal-weighting outperformed. But more recently, market cap-weighting has pulled ahead. This is the case for the one-year, three-year and five-year periods.

So why is this? Simply put, the phenomenally large FAANG stocks (Facebook, Apple, Amazon, Netflix and Google) have made the S&P 500 top heavy. Today, these five stocks represent a highly concentrated 12 percent of the S&P 500, nearly double from their share just five years ago. Apple alone represents 4 percent of the large-cap index.

Ten years ago, the FAANG stocks—excluding Facebook, which wasn’t public yet—had a combined market cap of $390 billion, according to FactSet data. In 2018, they’re valued at more than eight and half times that, or right around $3.32 trillion—a mind-boggling sum.

Market cap-weighted also means more money is disproportionately being reallocated to top winners such as Apple and Amazon, and so it becomes a self-fulling prophecy. This leaves you with too much exposure to companies that would be hardest hit in the event of a market downturn, and too little exposure to names and sectors that might rotate to the top in the next cycle.

Learn more about the domestic market by clicking here!

Gold Market

This week spot gold closed at $1,279.55, down $19.80 per ounce, or 1.52 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.51 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index came in off 2.69 percent. The U.S. Trade-Weighted Dollar moved higher this week with a gain of 1.35 percent.

| Date |

Event |

Survey |

Actual |

Prior |

| Jun-12 |

Germany ZEW Survey Current Situation |

85.0 |

80.6 |

87.4 |

| Jun-12 |

Germany ZEW Survey Expectations |

-14.0 |

-16.1 |

-8.2 |

| Jun-12 |

CPI YoY |

2.8% |

2.8% |

2.5% |

| Jun-13 |

PPI Final Demand YoY |

2.8% |

3.1% |

2.6% |

| Jun-13 |

FOMC Rate Decision (Upper Bound) |

2.00% |

2.00% |

1.75% |

| Jun-13 |

China Retail Sales YoY |

9.6% |

8.5% |

9.4% |

| Jun-14 |

Germany CPI YoY |

2.2% |

2.2% |

2.2% |

| Jun-14 |

ECB Main Refinancing Rate |

0.00% |

0.00% |

0.00% |

| Jun-14 |

Initial Jobless Claims |

223k |

218k |

222k |

| Jun-15 |

Eurozone CPI Core YoY |

1.1% |

1.1% |

1.1% |

| Jun-19 |

Housing Starts |

1315k |

-- |

1287k |

| Jun-21 |

Initial Jobless Claims |

221k |

-- |

218k |

Strengths

- The best performing metal this week was silver, down just 1.37 percent. Gold traders and analysts were bullish on the yellow metal due to speculation that the now confirmed interest rate hike by the Federal Reserve could ease the dollar’s rally, according to Bloomberg. It is of interest to note that over the last three weeks gold stocks, as measured by the NYSE Arca Gold Miners Index, have outperformed bullion by 121 basis points. While too early to call it a meaningful trend, that gold stocks are outperforming bullion, the seasonal summer lift in bullion buying should start to pick up in July and investors may be positioning themselves now in the equities.

- The World Gold Council is reportedly preparing a fund which would charge less than any other gold ETF, according to Bloomberg. Regulatory filings show that the SPDR Gold MiniShares Trust (GLDM) will cost 18 basis points in management fees. That is $1.80 for every $1,000 invested. For comparison, GLD charges $4 for every $1,000 invested.

- Gold priced in euros is nearing the biggest gain since September as a result of the European Central Bank’s pledge to maintain the currently record-low borrowing costs over the next year. “That means there’s going to be a large disparity between U.S. interest rates and European interest rates,” says George Gero, a managing director at RBC Wealth Management, “and that is going to probably increase the demand for gold.” Additionally, green credentials will be required from the world’s biggest gold producers in order to be traded on London’s bullion market, according to the Financial Times.

Weaknesses

- The worst performing metal this week was palladium, down 2.23 percent even with hedge funds adding more exposure to their net long position. The dollar headed for its best week since November 2016, which dropped gold prices as a result, according to Bloomberg. Kotak Commodity Services analyst Madhavi Mehta noted, “Weighing on [gold] price are sharp gains in the U.S. dollar against the euro amid diverse monetary policy outlook for the Fed and ECB.” During the past week, investors withdrew from commodity exchange-traded funds, reports Bloomberg. Precious metal funds saw $408 million in outflows, as opposed to $1.02 billion during the prior week.

- In India, gold discounts are at their widest in nine months, according to Business Standard. Dealers are providing discounts as large as $7.50 per ounce over domestic prices this week, up from $5 last week. This is the sixth straight week of discounted gold in India. The falling rupee played a significant role in denting demand for gold jewelry, which is on track to decline 18 percent this year.

- South Africa, the eighth largest gold producer globally, saw a drop in gold production for the seventh straight month in April, reports Bloomberg. Platinum-group metal production in South Africa similarly fell for the fifth straight month. In Mexico, the Penasquito mine suffered a 12-day blockade by a group of truckers who claim Goldcorp Inc. did not follow through on promises to hire locally. This mine is Goldcorp’s most significant asset. As of writing this piece, the blockade has been called off.

Opportunities

- Wheaton Precious Metals and Colbalt 27 Capital signed separate streaming agreements with Vale for an upfront consideration of $690 million. In return for finished cobalt from Voisey’s Bay mine, Wheaton agreed to pay Vale $390 million upfront for 42.4 percent of Vale’s cobalt production, along with a future payment of 18 percent of spot cobalt price. The streaming company will be entitled to production starting in 2021.

- Nighthawk Gold Corp. announced updated Inferred Mineral Resource estimate this week, of 50.305 million tonnes, with an average grade of 1.62 grams per tonne. This is for the 2.613 million ounces of gold for its 100 percent owned Colomac Gold Project, Bloomberg reports. Recent test work for the Colomac project confirms favorable recoveries for all process options including heap leaching, flotation and gravity separation. In other company news, Wesdome Mines has been raised to “strong” buy from buy, a recommendation made by Industrial Alliance Securities analyst George Topping. The company’s price target is set to C$5, implying an increase of 98 percent from its last close, reports Bloomberg.

- Inflation in the U.S. accelerated during May to the fastest pace in over six years, reports Bloomberg. The consumer price index (CPI) rose 0.2 percent from April and 2.8 percent from a year earlier. Average hourly wages, however, were unchanged from May 2017 when adjusted for inflation, which shows employees’ incomes were stagnate. The trend of no growth in real purchasing power for employees cannot go on forever. The first rounds of teacher strikes this past school year likely won’t be a onetime event or one sector of the economy shock. Labor markets are tight. Immigration labor is being choked off from participation in the future which should lead to increased Unit Labor Costs. Cornerstone Macro notes that Unit Labor Costs accelerated sharply in the 1970s driven by a jump in compensation gains which led inflation and gold during that decade.

Threats

- Consumer debt is piling up in the U.S. while borrowers keep their credit profiles healthy for now, reports Bloomberg. Dean Athanasia, co-head of Bank of America’s consumer and small-business operation, noted in a recent conference that “people and clients are definitely leveraging up and we have to watch that.” Meanwhile, senior executives and directors at Netflix, Amazon, Facebook, and Google’s parent Alphabet Inc. have disposed of $4.58 billion of their own stock so far in 2018. “If they continue selling into that weakness, then that’ll be a strong indicator of insider sentiment,” says Jonathan Moreland, director of research at InsiderInsights.com.

- Due to recent tax cuts and increased federal spending, U.S. deficit is ballooning towards 125 percent of gross domestic product after 2030, according to Congressional Budget Office predictions. “It is pretty much unprecedented that we’re seeing this level of debt expansion so late in an economic cycle,” says Jeffrey Gundlach, chief investment officer of DoubleLine Capital.

- Grievances against Randgold Resources turned violent in the town of Kéniéba, Mali, resulting in one person’s death and at least six injured. The incident was sparked when 15 employees who staged a sit-in against Randgold’s hiring practices and the dismissive local government were let go, according to Jane’s 360. On another note, mining companies in the Democratic Republic of Congo are battling new legislation that voids existing agreements and increases costs. DRC is Africa’s largest copper producer and the source of two-thirds of the world’s cobalt.

Emerging Europe

Strengths

- The Czech Republic was the best performing country this week, gaining 5 basis points. All emerging Europe markets closed lower this week, with exception of the Prague exchange, which had a slight gain. Equites traded down as trade wars between major economies are picking up. Eurozone imposed retaliatory tariffs against the U.S. on imports of jeans, motorbikes and whiskey, worth $3.3 billion.

- The Russian ruble was the best relative performing currency this week, losing 1.3 percent against the U.S. dollar. Central Bank of Russia left its main rate unchanged at 7.25 percent, while the market was expecting a 25 basis points cut.

- Information technology was the best performing sector among eastern European markets this week.

Weaknesses

- Poland was the worst performing country this week, losing 2.2 percent. Energy and commodity stocks sold off the most as fear of global trade is rising. President of Poland, Andrzej Duda, proposed a referendum on EU law primacy and domestic matters. Fifteen questions were proposed, and if approved by the Senate, the referendum will take place in the middle of November.

- The Turkish lira was the worst performing currency this week, losing 5.2 percent against the U.S. dollar. Current account deficit widened and the Fed’s decision to raise rates by 25 basis points put further pressure on an already weak lira.

- Real estate was the worst performing sector among eastern European markets this week.

Opportunities

- Russia will be in the center of news for the next few weeks. FIFA World Cup 2018 kicked off Thursday in Russia, where 12 stadiums will be hosting games over the next month. Russia has spent eight years and 700 billion rubles getting everything ready for this tournament. Moscow expects up to 1 million fans during the 2018 World Cup.

- Elections are over in Russia and as expected Prime Minister Medvedov announced an increase in the retirement age and the Value Added Tax (VAT). Renaissance Capital estimates that an increase in the retirement age to 63 for women and 65 for men might lift Russian GDP growth by 0.5 percentage points in the medium term. An increase in VAT might bring up to RUB2.5 trillion to the budget in the next five years. The VAT could go from 18 percent to 20 percent, raising government funds to cover the additional spending as outlined in the new Presidential decrees for 2018-2024.

- The European Central Bank (ECB) left all its rates unchanged as expected and outlined plans to end its stimulus program by the end of this year. The bank said Thursday that if incoming data followed its forecasts, then its monthly bond purchase program would extend by three months. However, the monthly bond-buying amount will drop from 30 billion euros, to 15 billion. The rates might stay unchanged until next summer.

Threats

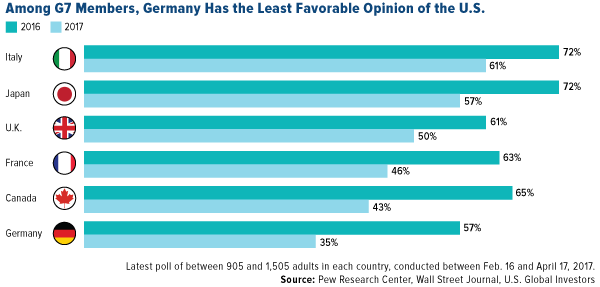

- The G7 meeting took place last weekend and this opportunity for global leaders to discuss their economic issues became a battlefield. Trump once again has said that Europe and Canada are benefiting from the trade surplus with the U.S. and has tasked Europe and Canada to stop ripping off America. The EU has a $151 billion surplus and Canada’s surplus with the U.S. stands at $100 billion. Among G7 countries, the share of people with a favorable opinion of the U.S. has dropped since 2016. Germany, Europe’s largest economy, has the least favorable opinion of the U.S.

- Eurozone industrial production fell more sharply than expected in April, resuming its 2018 decline after a March bounce. The European Union’s statistics agency said Wednesday that the output of factories, mines and utilities across the 19 countries that use the euro was 0.9 percent lower in April than in March, although 1.7 percent higher than a year earlier. Each of the eurozone’s five largest members saw a drop in output, with the Netherlands experiencing the sharpest decline at 4.4 percent. A drop in industrial output, which accounts for a quarter of the eurozone economy, might lead to weaker economic growth.

- The U.S. Treasury imposed sanctions on three Russian individuals and five companies on Monday, saying they had worked with Moscow’s military and intelligence on ways to conduct cyber-attacks against the United States and its allies. Stocks trading on the Moscow exchange were little changed at the begging of the week.

© US Global Investors

www.usfunds.com

© U.S. Global Investors

Read more commentaries by U.S. Global Investors