Stop buying Iranian oil or face the music.

That’s the message the U.S. government shared with the world this week, giving importers until November 4 to cut their consumption of Iran’s crude to zero—or expect sanctions. The threat comes a month after President Donald Trump withdrew the U.S. from the Obama-era nuclear deal.

West Texas Intermediate (WTI) responded by adding more than $6 to the price of a barrel this week alone, to end above $74.

click to enlarge

Other drivers included supply disruptions in Canada and Libya, as well as a sharp, more-than-expected decline in U.S. crude inventories. Nearly 10 million barrels were drawn in the week ended June 27, the most since September 2016. Crude is now up an eye-opening 70 percent from the same time last year, contributing to the inflationary pressure that’s pushed consumer price growth to a six-year high.

And there could be more upside, should supply crunches continue along with Trump’s ongoing geopolitical efforts to isolate Tehran. Ready to see $90-a-barrel oil? That’s the forecast from Bank of America Merrill Lynch analyst Hootan Yazhari.

“We are in a very attractive oil price environment,” Yazhari told CNBC this week, “and our house view is that oil will hit $90 by the end of the second quarter of next year,” or 12 months from now.

Even if this prediction ends up overshooting the mark, I believe there could still be money to be made in the energy space on tightening supply and strong global demand. For more, I urge you to watch this brief video outlining the six factors that matter when picking energy stocks.

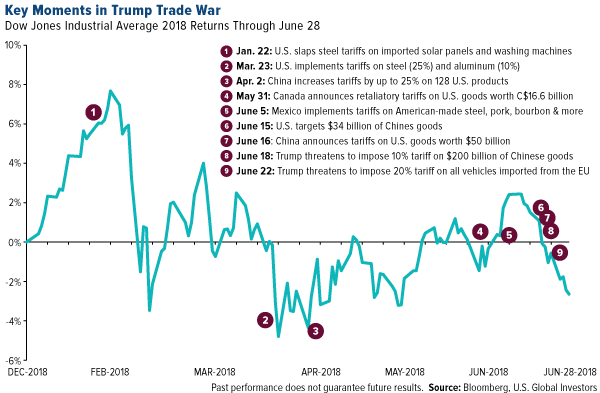

Bull Market May Have Just Hit a Trade War Wall

The U.S. market is mere days from hitting a milestone that some investors might not have anticipated in the business-friendly era of Trump. Both the S&P 500 Index and Dow Jones Industrial Average have been stuck in correction mode since early February of this year, when inflation fears and concerns of a global trade war triggered a monster selloff.

Today marks the 99th day both indices have been in correction, and according to MarketWatch, if they stay sideways another 10 trading days, it will become the longest such stretch since 1984.

Stocks managed to recover then, but as I see it, unless Trump softens his stance on trade, they will have a difficult time doing the same today. Stiff retaliatory barriers are scheduled to be raised by China, Canada and other key markets, and Canadian consumers have already started boycotting American-made goods. U.S. exports of steel, soybeans and other products are down from a year ago because of friction over the tariffs, which are essentially regulations that could jeopardize the positive work Trump has done in cutting red tape in other areas.

Below is the Dow’s performance so far this year, not including today, annotated with some key moments in the Trump trade war. I chose the Dow specifically because it includes the very largest U.S. exporters, some of which do tens of billions of dollars in sales in China alone. As the biggest U.S. exporter, Boeing delivered more than 200 aircraft to the Asian country last year, accounting for a quarter of the plane maker’s global sales. Apple generated around 20 percent of its revenue in China, or the equivalent of $44.7 billion.

click to enlarge

The question now is whether we’re headed for a recession, and how investors can prepare—though I believe the market is oversold, as I explain in the most recent edition of Frank Talk Live. The last nine years have been extraordinarily profitable, but every bull market must come to an end—not from age, remember, but from changes in monetary or fiscal policy.

This week I offered one of my favorite strategies to face the next bear market with confidence. Discover what it is by clicking here.

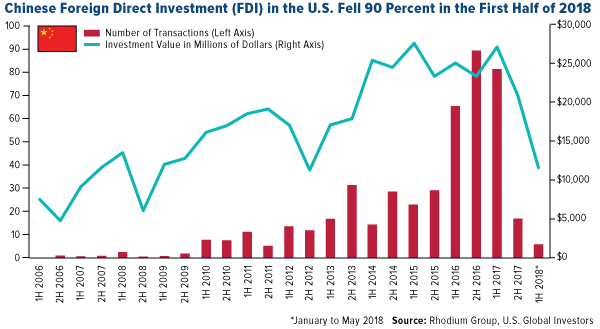

Trade war friction has strained international relations in other ways than just trade, of course. Among those is foreign direct investment (FDI), essential for global economic growth.

Chinese FDI in the U.S. Just Fell 92 Percent

China’s tech industry is exploding. Last year, gross output value of Chinese tech firms hit 20 trillion yuan, or about $3 trillion, for the first time ever. Nine of the world’s 20 biggest tech firms now call China home, beginning with Alibaba, valued at a half a trillion dollars. And for the past several years, China has filed far more patent applications than the U.S. on an annual basis. (I should mention, though, that the U.S. still has more patents overall, having just issued patent number 10 million.)

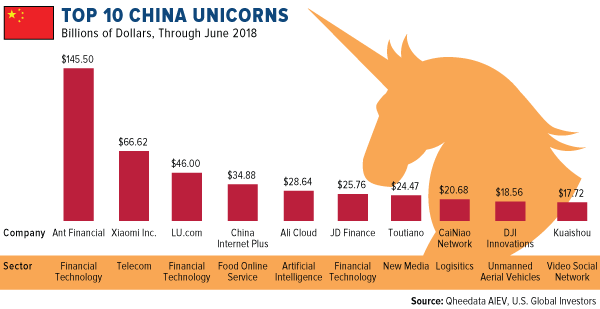

The Asian country, in fact, has more unicorns—or startups worth $1 billion or more—than any other nation on earth. Chinese unicorns account for more than half of the global total, and 66 percent in terms of valuation, according to the World Economic Forum (WEF).

Just look at the top 10 Chinese unicorns. Ant Financial, formerly known as Alipay, ranks first with a valuation of $145 billion. That’s about twice the value of the number one U.S. unicorn, Uber.

click to enlarge

It’s very likely even more capital will flow into these firms this year and next. That’s because Chinese FDI in the U.S. fell an eye-opening 92 percent in the first half of 2018, as the government cracks down on capital flight. The decline is also likely in response to the U.S. government’s increased scrutiny of Chinese acquisitions.

click to enlarge

According to economic research firm Rhodium, Chinese investors have sold $9.6 billion worth of U.S. assets, including office buildings in New York, San Francisco, Chicago and Los Angeles. That’s after making only $1.8 billion in investments. What this means is that the country’s net U.S. FDI is negative $7.8 billion so far this year.

And regarding a possible rebound in Chinese investment activity, “looming U.S. policies present substantial headwinds,” writes Rhodium’s director of research, Thilo Hanemann.

So where will all this capital go?

I don’t think anyone can say for sure, but my guess is that this will be a huge windfall for the already fast expanding Chinese tech industry.

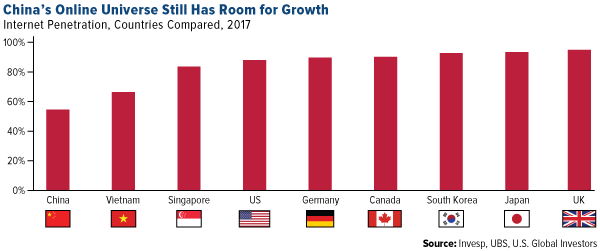

Only Half of China Is Online

There are even more reasons to be optimistic about the Chinese tech industry, including the fact that only a little over half of the country’s population is online. At 772 million people, the user base is massive—more than twice the size of the entire U.S. population—but penetration is only 54.6 percent, according to UBS. That’s well behind the U.K. (94.8 percent), Japan (93.3 percent) and the U.S. (87.9 percent).

click to enlarge

This means, of course, that the country’s tech and internet industries still have much room to grow.

China is already number one in mobile payments, having surged to a whopping $9 trillion in 2016, compared to only $112 billion for the U.S. The Asian giant is rapidly becoming cashless—so much so that a friend of mine recently had a hard time using paper money to make a purchase in a Chinese convenience store. In fact, a number of unmanned, fully-automated stores—most notably BingoBox and Alibaba’s Tao Cafe—have sprung up all over the country. Transactions are made simply by scanning your smartphone on a designated counter or plate before leaving the store.

Learn more about one of the world’s fastest-growing regions by clicking here!

Gold Market

This week spot gold closed at $1,253.17 down $16.24 per ounce, or 1.28 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.51 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index lost 2.15 percent. The U.S. Trade-Weighted Dollar ended the week essentially unchanged with Friday’s 0.83 percent fall neutralizing the gains from earlier in the week.

| Date |

Event |

Survey |

Actual |

Prior |

| Jun-25 |

New Home Sales |

667k |

689k |

646k |

| Jun-26 |

Hong Kong Exports YoY |

8.5% |

15.9% |

8.1% |

| Jun-26 |

Conf. Board consumer Confidence |

128.0 |

126.4 |

128.8 |

| Jun-27 |

Durable Goods Orders |

-1.0% |

-0.6% |

-1.0% |

| Jun-28 |

Garmany CPI YoY |

2.1% |

2.1% |

2.2% |

| Jun-28 |

GDP Annualized QoQ |

2.2% |

2.0% |

2.2% |

| Jun-28 |

Initial Jobless Claims |

220k |

227k |

218k |

| Jun-29 |

Eurozone CPI Core YoY |

1.0% |

1.0% |

1.1% |

| Jul-1 |

Caixn China PMI Mfg |

51.1 |

-- |

51.1 |

| Jul-2 |

ISM Manufacturing |

58.2 |

-- |

58.7 |

| Jul-3 |

Durable Goods Orders |

-- |

-- |

-0.6% |

| Jul-5 |

ADP Employment Change |

190k |

-- |

178k |

| Jul-5 |

Initial Jobless Claims |

225k |

-- |

227k |

| Jul-6 |

Change in Nonfarm Payrolls |

200k |

-- |

223k |

Strengths

- The best performing metal this week was palladium, down just 0.27 percent on a positive recommendation by Morgan Stanley based on deficit market supply. Gold traders and analysts became bearish this week according to the Bloomberg weekly survey as gold fell to its lowest level so far this year.

- China’s central bank revised the value of its end-of-May gold reserves to $77.32 billion, up from $73.74 billion, reports Reuters. This is notable since the central bank did not provide an explanation for the changed figure and did not change the total amount of gold held by the bank. According to Bloomberg, the Mauritius International Derivatives and Commodities Exchange expects to trade $6.5 billion of gold annually within the next five years. The move is expected to become a financial gateway from the Indian Ocean island nation to Africa and spur further gold investment.

- Nighthawk Gold announced positive drilling results of 25.50 meters of 2.68 grams per tonne (gpt) gold plus 9.95 meters of 4.90 gpt gold at its North Inca gold deposit in Canada. Yamana Gold declared commercial production had begun at its Cerro Moro gold and silver mine in Argentina.

Weaknesses

- The worst performing metal this week was platinum, down 2.78 percent. According to UBS, gold shorts increased by 3 million ounces in the prior week, the largest weekly gain since November 2015. Strategist Joni Teves writes that risks have increased and the risks to the economy are skewed to the downside. “For gold, this means that longs are more resilient and shorts hesitant. We do not expect strong safe haven flows as long as the anticipated impact on growth and inflation remains modest.” Gold has seen its worst week of the year and Jordan Eliseo, chief economist at ABC Bullion, says bullion maybe drop to $1,250, which “will likely prove an attractive entry point, with sentiment incredibly low and futures positioning continuing to unwind.”

- Investors continue to back away from commodities as commodity ETFs saw a seventh straight week of outflows. Outflows totaled $759 million this week, compared to withdrawals of $256 million in the previous period. Gold ETFs also reached their lowest holdings levels in three months as gold slumped to its lowest in 2018, reports Bloomberg.

- Gold is set for its biggest monthly drop since November 2016 on the heels of a stronger dollar, which is seeing its third straight month of gains. Gavin Wendt, senior analyst at MineLife, told Bloomberg that “the U.S. dollar has been the biggest beneficiary as investors’ first choice safe haven” and that it has “indirectly led to gold-price weakness.”

Opportunities

- RBC Capital Markets writes this week that valuations of junior gold companies have compressed this year and now sit at $38 per ounce of resources, compared to the trailing 12-month average of $54 per ounce of resources. This recent pullback could spur greater mergers and acquisitions activity given that junior miners now have more attractive valuations.

click to enlarge

- Suki Cooper, precious metals analyst at Standard Chartered, says that gold could rally after seeing a weak second quarter. “This quarter is generally a seasonally weak period for physical demand, but we’ve also seen a number of macro indicators line up to present quite a weak backdrop for the gold market.” According to Pictet Wealth Management, gold is set to stage a comeback as the dollar’s recent strength is a temporary rebound and should decline further down the road. Currency strategist Luc Luyet said on Monday that he expects bullion to climb to $1,320 an ounce by the end of the year.

- Inflation is on the rise, as seen in the costs paid by factories for materials, which climbed to a seven-year high in June in Texas. Bloomberg writes that more manufacturers are paying higher input prices and getting more for the final product, able to pass inflation onto consumers as the prices of materials used in U.S. manufacturing have been mounting for months. Larry Summers, former U.S. Treasury Secretary, told Bloomberg in a phone interview this week that Federal Reserve interest rate hikes, which slow expansion, are a greater risk to the economy than inflation. “The dangers are still much more on the side of too much slowdown than they are of too much inflation.”

click to enlarge

Threats

- General Motors (GM) issued a strong warning to the White House that it could shrink its U.S. operations and cut jobs if tariffs are broadly applied to imported vehicles and auto parts. Because GM’s Silverado pickup is the top imported model from Mexico, this is a significant issue. In addition, a lot of high-value parts are sourced from Asia. The proposed 25 percent tariff would add thousands of dollars onto their current vehicle prices.

- Bloomberg reports that gold is now the cheapest relative to crude oil in more than three years as growing concerns over a U.S.-China trade war have failed to revive demand for bullion as a safe-haven asset. High petroleum prices relative to gold can lead to a margin squeeze for large open pit mines that are more energy intensive.

- The S&P 500 Index has stumbled the last five times the Federal Reserve System Open Market Account has had Treasuries mature, writes Bloomberg. The Fed is allowing bonds to “roll off,” which means pocketing, rather than reinvesting, the proceeds as the bonds mature. This has the effect of reducing liquidities and possibly draining equities. The last five times maturity dates came and went, the S&P 500 Index fell a minimum of 68 basis points. July 1 is next maturity roll off date.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 2.1 percent. The Budapest stock exchange saw support this week from strong economic data. Business, economic and consumer confidence data improved in June, while unemployment declined to 3.7 percent. MOL, a Hungarian refinery, was the best equity this week, gaining more than 4 percent.

- The Turkish lira was the best performing currency this week, gaining 2 percent against the U.S. dollar. Erdogan won the presidential elections in the first run last Sunday, and as some uncertainty passed markets, the lira reacted positively to the election outcome.

- Real estate was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 1.8 percent. The IMF said that the recent debt relief agreement on Greece has significantly improved debt sustainability over the medium term, but longer-term prospects remain uncertain. Long-term improvements in the debt indicator can only be accomplished with strong economic growth and primary fiscal surplus.

- The Hungarian forint was the worst performing currency this week, losing 1.1 percent against the U.S. dollar. The currency continues to weaken as the country’s central bank keeps monetary policy looser than its peers do.

- Information technology was the worst performing sector among eastern European markets this week.

Opportunities

- European Union leaders have reached a deal on migration. Under the agreement, EU leaders agreed to share refugees arriving on a voluntary basis and created controlled centers inside the EU to process asylum requests. It also agreed to share responsibility for migrants rescued at sea, which should be especially positive for Italy.

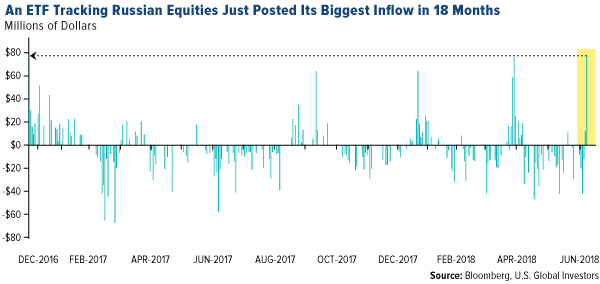

- Last week OPEC announced a smaller-than-expected production increase. OPEC’s decision and Iranian sanctions are pushing the price of oil higher and Russia generally benefits from this price movement, as most of the country’s revenue comes from the sale of oil. Last Friday, the VanEck Vectors Russia ETF had its biggest inflows in 18 months.

click to enlarge

- Two powerful world leaders, Donald Trump and Vladimir Putin, will meet on July 16, in Helsinki. Tension has increased between the U.S. and Russia after additional sanctions were imposed on Russia in April. This meeting could present an opportunity for positive dialogue surrounding global geopolitics.

Threats

- Russia’s government will lower its forecast for economic growth next year as a plan to raise a value added tax from 18 percent to 20 percent could spur inflation and hurt consumer spending. A possible increase in government spending, however, will not have an impact until the second half of next year, Bloomberg reports. Gross Domestic Product (GDP) most likely will slow down to 1.4 percent in 2019, compared with a previous projection of 2.2 percent.

- A Euro-area economic confidence index fell from 112.5 to 112.3 in June, to an eight-month low. Escalating trade tensions and rising oil prices worry European consumers. U.S. President Donald Trump threatened a 20 percent tariff on cars imported from the EU unless the bloc removes import duties and other barriers to U.S. goods. Brent crude oil gained 19 percent year-to-date and is trading at almost $80 per barrel, a level last seen back in 2014.

- Elections in Turkey are over. The stock market and the lira rebounded this week, but the long-term outlook for Turkey is not certain. Erdogan won the first round of elections, gaining 52.5 percent of votes, while his AKP party and alliance with MHP (a nationalist, non-religious, right-wing party) has the majority in parliament. An announcement of new cabinet members should take place next week and investors will be looking after new economic plans. If Erdogan uses his executive powers to push for looser fiscal and monetary policy, the lira could depreciate further.

© US Global Investors

www.usfunds.com

© U.S. Global Investors

Read more commentaries by U.S. Global Investors