Assumptions Everywhere

Negative Cash Flow

The Threats Go On

The Venus Flytrap: Entitlements

LA, Maine, Beaver Creek and Boston

In describing the global debt train wreck these last few weeks, I’ve discovered a common problem. Many of us define “debt” way too narrowly.

A debt occurs when you receive something now in exchange for a promise to give something back later. It doesn’t have to be cash. If you borrow your neighbor’s lawn mower and promise to return it next Tuesday, that’s a kind of debt. You receive something (use of the lawn mower) and agree to repayment terms – in this case, your promise to return it on time and in working order.

One reason you try to get that lawnmower back on time and in the proper condition is that you might want to borrow it again in the future. In the same way that not paying your bank debt will make it difficult to get a bank loan in the future, not returning that lawnmower may make your neighbor a tad bit reluctant to lend it again.

Debt can be less specific, too. Maybe, while taking your family on a beach vacation, you notice a wedding taking place. Your 12-year-old daughter goes crazy about how romantic it is. In a moment of whimsy, you tell her you will pay for her tropical island beach wedding when she finds the right guy. That “debt,” made as a loving father to delight your daughter, gets seared into her brain. A decade later, she does find Mr. Right, and reminds you of your offer. Is it a legally enforceable debt? Probably not, but it’s at least a (now) moral obligation. You’ll either pay up or face unpleasant consequences. What is that, if not a debt?

These are small examples of “unfunded liabilities.” They’re non-specific and the other party may never demand payment… but they might. And if you haven’t prepared for that possibility, you may be in the same kind of trouble the US government will face in a few years.

Uncle Sam has made too many promises to too many people, with little regard for its future ability to fulfill them. These are debt. Worse, some of them are additional debt on top of the obligations we already see on the national balance sheet.

Even worse, entire generations have planned their retirement lives around the government fulfilling those promises. If those promises aren’t met, their lifestyles will indeed become a potential train wreck.

That will be our topic today as we continue my Train Wreck series. This will be chapter 8. If you’re just joining us, here are links to prior installments.

In the coming weeks we’ll summarize the train wreck series and then shift the discussion to how you can prepare. But first, I want to leave no doubt about how big this problem is.

Assumptions Everywhere

Let’s start with what we know. The official, on-the-books federal debt is currently about $21.2 trillion, according to the US National Debt Clock. I say “about” cautiously because decimal points really matter when the numbers are this large. The difference between $21.1T and $21.2T is $100 billion. That used to be a lot. Now it’s a rounding error.

Anyway, $21.2T is the face amount of all outstanding Treasury paper, including so-called “internal” debt. This is about 105% of GDP and it’s only the federal government. If you add in state and local debt, that adds another $3.1 trillion to bring total government debt in the US to $24.3 trillion or more than 120% of GDP. Then there’s corporate debt, home mortgages, credit cards, student loans, and more. Add it all together and total debt is about 330% of GDP, according to the IIF data I cited in Debt Clock Ticking. We are in hock up to our ears.

But it’s actually worse than that, due to the kind of promises I mentioned above. Prime among them are Social Security and Medicare. Strictly speaking, these aren’t “unfunded” because they have dedicated revenue streams: payroll taxes. Most Medicare recipients also pay premiums. To date, these revenue sources have covered current expenditures and more, allowing the programs to build up reserves. But that’s about to change.

As of this year, both programs are in negative cash flow, meaning Congress must provide additional cash to pay the promised benefits. It will get worse, too. The so-called “trust funds” are going to run dry sooner or later, and it may be sooner. This month’s annual trustee report estimated Social Security will run out of reserves in 2034, and the hospitalization part of Medicare will go dry in 2026.

Just for the record, those “trust funds” don’t exist except as an accounting fiction. It is like you saving $100,000 for your child’s education and then borrowing all the money from your children’s education fund. You can pretend in your mind that you have set aside $100,000 for your child’s future education, but when it comes time to make those payments, you’ll have to pull it out of current income or liquidate other assets.

The US government has borrowed (or used or whatever euphemism you want to apply) all the money in those trust funds. So, talking about running out of reserves in 2034 or 2026 is rather meaningless. We’ve already run out of reserves. I was talking with Scott Burns about this and other facts over the unfunded liability (he wrote a book on it with Professor Larry Kotlikoff) and he gave me the great line, “The only truly bipartisan cooperation in Congress is that both sides lie.” Any time a politician talks about putting a “lock box” around Social Security or Medicare trust funds, he or she is either staggeringly ignorant or lying.

But, going with their terminology, these estimates of when the trust funds run out depend on a slew of assumptions. To estimate revenue, they must know how many workers the US has, their wages, and at what rates those wages will be taxed. To estimate expenses, they must know how many retirees will be drawing benefits, the amount of those benefits, and how long the retirees will live to receive them. They also have to assume an inflation rate on which the cost-of-living adjustment is based. A small deviation in any of those can have huge long-term consequences.

For what it’s worth, then, Social Security says it has a $13.2 trillion unfunded liability over the next 75 years. That’s the benefits they expect to pay minus the revenue they expect to receive.

Medicare projections require even more assumptions: what kind of treatments the program will cover, how much treatment senior citizens will need, and what those treatments will cost. All these could vary wildly but the “official” assumptions put Medicare’s 75-year unfunded liability at $37 trillion. It could be vastly more or, if we all get healthier and healthcare costs drop, could be less.

This being the government, I think the safe course is to assume their numbers are the best case, resembling reality only if everything goes exactly right. And of course, it won’t.

My friend Professor Larry Kotlikoff estimates the unfunded liabilities to be closer to $210 trillion. (Click on that sentence for a link to his Forbes column.) That’s a far cry from the $50 trillion official estimate.

So, at a minimum, we can probably assume Social Security and Medicare are at least another $50 trillion in debt on top of the $21.2 trillion (and growing) on-budget federal debt. And then you come to the scary part. This doesn’t include civil service or military retirement obligations, or federal backing for some private pensions via the Pension Benefit Guaranty Corporation, or open-ended guarantees like FDIC, Fannie Mae, and on and on.

Negative Cash Flow

Think back to my example of promising your daughter the beach wedding. That is sort of what is happening with Social Security, if you had accompanied the promise by asking your daughter to save a nickel a week toward paying for it. The resulting $28 after ten years would not begin to cover the cost, but your daughter will rightly argue she did her part. You will be on the hook for the rest, just as Congress will be on the hook with angry retirees who think they “paid” for their benefits.

That means benefits will continue once the trust funds run dry. Maybe they’ll make some minor cuts here and there, but voters won’t allow much, at least until enough Boomers leave the scene to let younger generations outnumber them. But as I continue to argue, Boomers are going to live a lot longer than the younger generations think. The deal each generation makes with previous generations is to die on schedule. The Boomer generation is going to break that deal. We will not go willingly into that good night.

But in reality, arguing over whether it’s $50 trillion or $200 trillion is pretty pointless. Long before we get to testing that hypothesis, we will have to cut spending or raise taxes or some combination of both.

This week, the Congressional Budget Office released its 2018 Long-Term Budget Outlook. Like the Social Security and Medicare trustees, the CBO makes assumptions, so it’s fair to be skeptical of its estimates. In fact, we had all better hope they are too pessimistic because we’re in deep trouble otherwise.

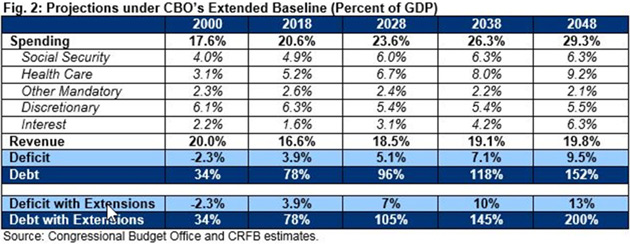

Because the CBO thinks federal spending will grow significantly faster than federal revenue, CBO foresees debt as a percentage of GDP will likely be 200% of GDP by 2048. But we will hit the wall long before then. Consider this table from the Committee for a Responsible Federal Budget.

CBO numbers show that by 2041, Social Security, health care, and interest expenditures will consume all federal tax revenue. All of it. Everything else the government does (including defense) will require going into more debt.

Yes, making that projection requires an assumption about tax revenue, which requires another assumption about GDP. It could be wrong. But if so, I think it will be wrong in the non-helpful direction because CBO projections don’t include recessions. (You think we’ll get to 2048 without some years of negative GDP growth? I’ll take that bet.)

Note also that the amounts CBO projects for Social Security and healthcare spending may well be low. I think they are very low. They assume some payment cuts to doctors and hospitals that Congress routinely overrules each year, as well as a different inflation benchmark to govern cost-of-living adjustments. And I have little hope Congress and presidents, now or future, will ever gain control over “discretionary” spending.

Of course, the interest expense depends on interest rates. CBO assumes the 10-year Treasury will go from today’s below-2% yield to 3.7% in 2028 and 4.8% by 2048. That might be too high, too low, or just right. Your guess is as good as mine (or CBO’s).

The CBO also assumes a fairly robust employment picture throughout that time. However, we are entering a period in which automation will replace mass numbers of human jobs. It might also result in new industries and new jobs, but history shows the transition to create new jobs will take time. Bain & Company’s Karen Harris estimates automation could eliminate 40 million US jobs by 2030 and depress wages for the jobs that remain. That will reduce payroll tax revenue and drive safety-net spending higher, neither of which will help reduce the debt.

It’s not just Bain, either. McKinsey, Boston Consulting, and other think tanks all expect similar job losses, which CBO does not consider. Yet, it will mean more people not paying Social Security and taxes, hence large revenue losses and even bigger deficits, and more unemployed people looking for the social safety net to help them.

Note: The bulk of those job losses will come in the latter half of the 2020s as new technologies kick in. And new technologies always bring about new jobs, but unfortunately not in the places where the old jobs were lost nor in the industries for which people are trained. To paraphrase Jerry Lee Lewis, there is going to be a whole lot of retraining going on.

So, take whatever estimates are made about future deficits and debt, and realize they are going to be worse. There will be fewer people working and paying taxes and more people living longer and using benefits. Kiss your assumptions goodbye.

The Threats Go On

So, the on-budget picture looks terrible, and even more so when you add the unfunded liabilities on top of it. What else could go wrong? Plenty. I’ll mention just four more possibilities.

First, at least some of the state and local pension debt I described two weeks ago could easily wind up on the federal government’s plate. Enough states are in a pickle to probably get some kind of bailout through Congress. Maybe not this Congress, but when it’s a Democratic Congress? It may be a whole other ballgame. This would add trillions to federal spending.

Second, CBO and pretty much everyone else assumes the world will avoid major wars. Aside from the death, destruction, and resource diversion, wars are expensive. Our relatively minor (in the historical scheme of things) Iraq and Afghanistan involvements added trillions in debt. Will we get through the next two decades without more such actions, whether large or small? I fervently hope so, obviously, but I would not bet on it.

Third, the life extension technologies I think are coming soon will raise Social Security spending because people will live longer. They may also raise payroll tax revenue if people keep working longer, but it’s not clear which way the scale will tip. It will likely be a net drain on the budget, at least initially. And by the mid-2030s when true rejuvenation is widely available, kiss your actuarial assumptions goodbye.

Fourth, all this presumes that those with capital to lend will stay interested in lending it to the US government. They may not, as the government’s financial condition becomes increasingly precarious. Yes, we’ve heard this before and it proved groundless. Things change. The fact that people cried wolf doesn’t mean no wolves are out there.

The Venus Flytrap of Western Civilization: Entitlements

My friend Dr. Woody Brock, one of the best economists and social commentators that I know, wrote a marvelous essay this last week about part of the entitlement issues. I’m going to close with a few lines from his letter. You can see some of his other work at www.SEDinc.com. His more exclusive quarterly Profiles are a treasure trove of economic insight. (Occasionally he lets me share them in Over My Shoulder, by the way.) Now to the beginning of his latest Profile:

The death of the extended family throughout the G-7 nations during 1850-1950 will go down as one of the most momentous developments of past centuries. For it is this development that gave rise to the modern welfare state with its crippling retirement and medical promises made to all citizens. How did today’s entitlements crisis begin, why does it get ever larger, and what can be done about it?

President Trump’s tax reform bill has rightly been criticized for inflating the US fiscal deficit. To many, this was unconscionable at a point when US federal debt is already 100% of GDP. Yet like everyone else, these critics have been mum on the far greater growth of debt that will accrue from ever-exploding entitlements expenditures. This latter prospect was identified a decade ago by the bi-partisan Simpson-Bowles committee as by far the gravest threat to the future of the US.

CBO projections show that within 18 years, entitlements spending will absorb all US federal tax revenues—leaving no revenues even for interest expense on the debt and for the military. In Germany, which proudly pays annually for its expenditures without incurring debt, Deutche Bank has estimated that by 2045, income tax rates of 80% (total, not marginal rates) would be needed for its PAYGO system. The entire workforce of the nation would be in bondage to the elderly. Other nations face even worse prospects.

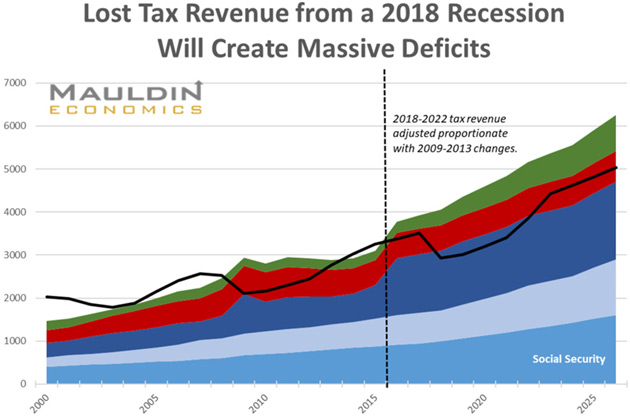

Those spending projections and massive deficits are going to happen in the 2020s. Here is a graph that we used last year showing what is likely to happen during the next recession (which I now think we will likely avoid this year, but it is coming), if tax revenue falls to the same degree it did in the last one.

We will have at least a $2 trillion deficit in the next recession, plus a bear market that leaves pensions even more underfunded, and a slower recovery because high debt crowds out future growth. Numerous academic studies back up that statement.

I think a future Democratic Congress and president, or maybe a split Congress that is desperate for funding, will enact a Value-Added Tax (VAT) in response to this. At least that is what I hope. Woody is a little more pessimistic than I am and thinks, quoting at the end of his analysis, that politics and not demographics is the problem:

Furthermore, why need benefits be trimmed much less slashed when the staggering new wealth of the top 10% can be taxed to pay for all promised benefits? Today’s obsession with the growth of inequality will significantly impact how the US will resolve the entitlements issue. The nation will not cut benefits because doing so will prove politically impossible, as President Clinton has long stressed.

Rather, the nation will fund its promised Social Security and Medicare benefits via the only kind of tax that can raise the staggering sums needed to fund them: a net-worth tax on, say, the top 15% of the population. Raising income tax rates on the rich will not raise anywhere near the amount needed for the next 40 years. Only a net-worth tax can do so.

Here are the relevant mathematics. As already stated, the net worth of US households has now reached $100 trillion. The top 15% wealthiest families own 90% of this wealth, or about $90 trillion. When push comes to shove, resistance by the rich against a wealth tax will be swamped by the political reality that a good 60% of Americans will be obsessed with funding their old age. Thus, rich as they are, the very wealthy will have little political leverage with which to fend off an annual net-worth tax.

The political logic will be: “Look, you rich people have had a return on your wealth of over 6% during the past hundred years. Why should this change very much? But if this is so, then it is time for you to pay your fair share, that is, to part with 2.5% of your total net worth annually. Your wealth will still continue to grow. With increased annual tax revenue of some $2.5 trillion, it will be possible for Americans to receive their promised benefits.”

We would expect the same logic to translate into additional net-worth taxes at the state and municipal level.

The fallout from such a policy will of course be disastrous.

Oh, dear gods, I hope he is wrong. It would be beyond disastrous.

Next week, I will try to close this series by summing up all the debt we have to deal with globally, recognizing that we are all in it together. And we will begin looking at strategies we can take to protect ourselves. The good news is none of this is going to happen within the next few years, so we have time to make plans. I’m in the same situation as you and already implementing some changes.

LA, Maine, Beaver Creek and Boston

I am flying to Los Angeles in mid- July to talk about the future of social organization with Bob Lefsetz, whom I have long wanted to meet. Then I have the annual Camp Kotok economics/fishing trip to Maine, then a board meeting with Ashford Inc. at the Beaver Creek Park Hyatt, where Shane and I will take an extended vacation, and then a trip to Boston to visit with friends in the area, among them the above-quoted Woody Brock at his family’s Gloucester compound.

My twins and their husbands are coming down this weekend to be with dad on their birthday, and they are getting the entire family together for sushi one night. I’m really looking forward to that.

This week I had a meeting with someone quite inspirational to me and was going to tell you about it here. However, I want to tell the story carefully and we couldn’t get it edited by our deadline. I’ll work on it and share next time.

Meanwhile, I hope your summer is going well (or winter if you’re Down Under). Happy Fourth of July to all my US friends. Amid the celebration, take a moment to cherish the freedoms we have and remember that not everyone has them.

Your working on our plans for prospering during The Great Reset analyst,

John Mauldin

[email protected]

© Mauldin Economics

www.mauldineconomics.com

© Mauldin Economics

Read more commentaries by Mauldin Economics