Overbought or Oversold? Let These Mathematical Signals Be Your Guide

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

|

Anticipate before you participate in the market. This is a classic piece of advice I like to give investors and have written about extensively in my CEO blog, Frank Talk. Financial markets are influenced by relatively predictable cycles and trading patterns, and by better understanding these we are able to react thoughtfully to headline noise or unexpected market developments.

How many of you remember the old police procedural Dragnet? In it, Sgt. Joe Friday famously uses the line “Just the facts, ma’am.” I’ve always felt this nuts-and-bolts attitude relates perfectly to how our investments team makes its decisions on where to allocate capital. Follow the models, look at the math—and leave emotions at the door.

A Sentiment Indicator for Contrarian Investing

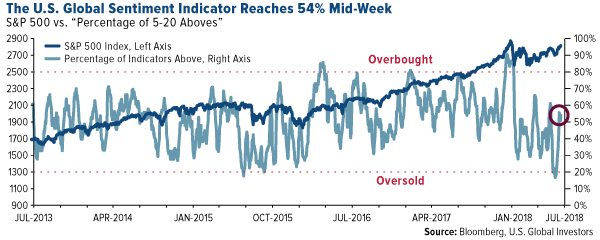

At U.S. Global Investors, one tool that we find particularly useful to track the different market cycles is our U.S. Global Sentiment Indicator. This indicator tracks 126 commodities, indices, sectors, currencies and international markets to help monitor volatility and cash flow levels.

Using this indicator, we note the percentage of positions that have five-day moving averages above or below the 20-day moving averages. Then we compare it to the S&P 500 Index. As you can see in the chart below, as of Wednesday, the sentiment indicator rebounded to 54 percent, rallying from a low of around 20 percent at the end of June.

While a drop below 20 percent means the market is extremely oversold, we do not view the market as overbought until around the 80 percent mark. Having a keen awareness of these movements allows our investments team to be more proactive rather than reactive. It helps us manage our emotions and not be swept away by negative media or overly optimistic headlines.

Explore this topic further in the Managing Expectations whitepaper!

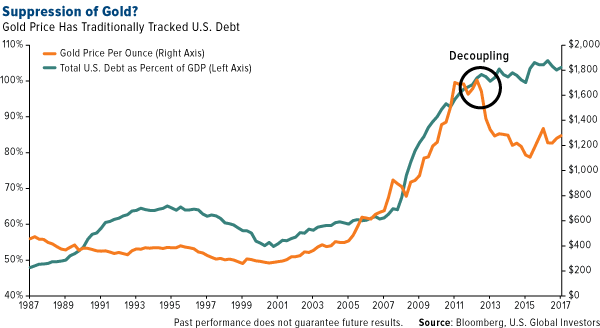

Is the Gold Market Being Suppressed?

Gold continued its trek lower this week, the price steadying around $1,220 an ounce on Tuesday following Federal Reserve Chair Jerome Powell’s congressional testimony. Powell commented that he thought the U.S. was on course for continued steady growth, supporting his expectation of a rate hike every three months. These comments sent the dollar up and gold down.

Despite this movement, I’m amazed that gold is holding up so well, particularly when you compare real interest rates in the U.S., Japan and the European Union.

In addition to these price moves, we’ve seen suppression and manipulation in the gold market in recent years. This is a topic I discussed this week in our webcast, cohosted by Randy Smallwood, CEO of Wheaton Precious Metals.

What do I mean by “gold suppression”? Historically, the price of gold has tracked U.S. debt, but as you can see in the chart below, that seems no longer to be the case.

The question, then, is not whether gold is actively being suppressed, but to what extent and by whom. Traders working at some big banks, including UBS to Deutsche Bank to HSBC, have already been charged for manipulating the price of precious metals futures contracts and fined as much as $30 million by the Commodity Futures Trading Commission (CFTC).

However, I’m skeptical that this has resolved the issue. In the past several years, gold has traded down in the week prior to China’s Golden Week, when markets are closed. As much as $2.25 billion of the yellow metal was dumped in the futures market in October 2016, as someone clearly sought to take advantage of the fact that markets were closed for the week in the world’s largest buyer of gold.

During the webcast, Randy Smallwood thoughtfully pointed out that the deliberate suppression of prices can't go on forever. I agree, and believe that precious metals such as gold and silver are significantly undervalued right now.

So what should investors be paying attention to?

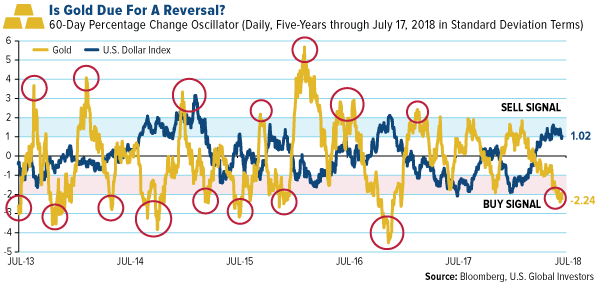

The Magic Behind the Math

Using an oscillator chart, let's compare the U.S. dollar to gold. I believe oscillators are vital to identifying the optimal time to buy or sell, and right now it appears that the greenback is overbought while gold is oversold.

Looking back over five years of data, we've discovered that, historically, when gold exceeded two standard deviations above the mean, the commodity fell 51 percent of the time in the following three months.

In contrast, when gold prices exceeded two standard deviations below the mean, it rose 77 percent of the time in the following three months. This is because gold is undervalued at this level.

Buying the laggards when the time is right could enable you to participate in a potential rally—and right now, that rally could be in gold, currently down 2.24 standard deviations.

Understanding this kind of math is almost like being adept at counting cards. In the 2008 film 21, an MIT professor helps six students become experts at card counting. The story, based on true events, shows how these students end up taking Vegas casinos for millions in winnings by following their professor’s teachings. Of course, there’s no way I can promise such an extraordinary outcome in your investments, but I do think there’s something to be said for the magic behind the math.

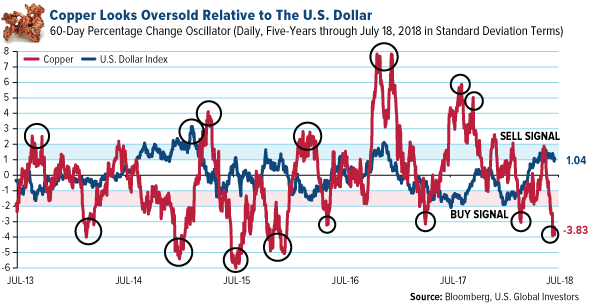

King Copper Could Also Be Due for a Reversal

Gold isn’t the only commodity that might be due for a reversal. Take a look at this chart showing copper versus the U.S. dollar. The red metal looks even more oversold than gold, down close to four standard deviations as of July 18. As I mentioned in the 2018 Commodities Halftime Report, copper looks attractive on surging demand for electric vehicles (EVs), which require between three and four times as much copper as traditional gas-powered automobiles.

In addition, based on these mathematical models, emerging markets have the potential to move higher as well. I encourage you to take a look at the chart featured in the Europe section of the Investor Alert today to see what I mean.

Always Remember the Golden Rule

|

Gold continues to be a classic example that helps illustrate seasonal rotations and price fluctuations based on a number of different factors geopolitical noise, inflation, wedding season in China and India, and much more.

The DNA of volatility, as I like to call it, shows that it is a non-event for gold to move up or down 17 percent over a rolling 12-month period. Knowing this has helped me to develop the 10 percent Golden Rule.

I have always advocated investors have around 10 percent of their portfolios in gold—5 percent in gold bullion or beautiful gold jewelry, and 5 percent in well managed gold mutual funds or ETFs. And then rebalance.

While no investment rules or statistical tools are accurate 100 percent of the time, investors can take ownership in how they use certain tools to manage emotions of the market and position themselves for greater success.

Capturing opportunities and understanding the ins and outs of the markets are what make investing so exciting.

Know a fellow investor who could benefit from this type of weekly investment analysis? Share our Investor Alert sign up page with them—subscribing is always FREE!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.15 percent. The S&P 500 Stock Index rose 0.02 percent, while the Nasdaq Composite fell 0.07 percent. The Russell 2000 small capitalization index rose 0.58 percent this week.

- The Hang Seng Composite lost 1.17 percent this week; while Taiwan was up 0.62 percent and the KOSPI lost 0.94 percent.

- The 10-year Treasury bond yield rose 6 basis points to 2.89 percent.

Domestic Equity Market

Strengths

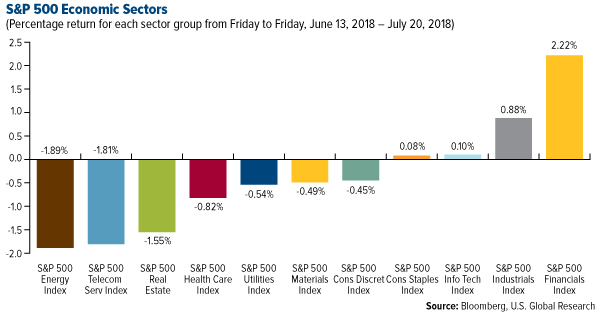

- Financials was the best performing sector of the week, increasing by 2.22 percent versus an overall increase of 0.07 percent for the S&P 500.

- United Continental was the best performing stock for the week, increasing 12.22 percent.

- Microsoft crushed its earnings, reporting $110 billion in annual revenue. The company showed strong growth in all three of its major reporting areas — especially in cloud computing, where Wall Street most wants to see growth. Its cloud unit saw revenue surge 23 percent year-over-year to $9.7 billion.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 1.89 percent versus an overall increase of 0.07 percent for the S&P 500.

- Omnicom Group was the worst performing stock for the week, falling 12.04 percent.

- Netflix's stock sank after its second quarter earnings report came in this week. The video streaming service fell short on new subscribers, as Wall Street expected. Additionally, the company's outlook for the next quarter was also disappointing.

Opportunities

- IBM posted its third straight quarter of revenue growth. The enterprise giant reported on Wednesday that second quarter revenue climbed 4 percent year-over-year to $20 billion, driven by its cloud business.

- Berkshire Hathaway loosened its buyback policy. Its chairman, Warren Buffett, and vice chairman, Charlie Munger, are now authorized to initiate share buybacks when both of them deem the repurchase price is "below Berkshire's intrinsic value." The previous policy said the share-buyback purchase price could not exceed 1.2 times book value per share.

- Samsung is reportedly planning a foldable smartphone that will be released next year, according to a report from The Wall Street Journal. The phone is rumored to have a 7-inch display and will fold in half like a wallet.

Threats

- Three men who played a pivotal role in navigating the U.S. through the 2008 financial crisis are concerned we're forgetting the lessons learned. Former Treasury Secretaries Henry Paulson and Timothy Geithner, as well as former Fed Chairman Ben Bernanke, warned at a round-table discussion marking the 10th anniversary of the financial crisis that the rising U.S. budget debt, which they called a "dysfunctional" political system, coupled with a drive to loosen rules put in place after 2008 could together endanger the economy.

- Manufacturers in every corner of America are worried about Trump's tariffs. The Beige Book, released Wednesday, showed that manufacturers across the Federal Reserve's 12 districts had seen President Donald Trump's ongoing trade spat drive up costs and disrupt supply.

- Apple is reportedly struggling to crack into India, the world’s third biggest smartphone market. The company has lost executives there in recent months and currently has a market share in the single digits as a result of cheap competition from Asian phone makers.

The Economy and Bond Market

Strengths

- The U.S. economy accelerated in June, according to an index that attempts to forecast the nation’s economic health. The leading economic index rose 0.5 percent after being flat in May, the Conference Board said Thursday. “The widespread growth in leading indicators, with the exception of housing permits which declined once again, does not suggest any considerable growth slowdown in the short-term,” said Ataman Ozyildirim, economist at the board.

- U.S. retail sales rose for a fifth month in June and figures from May were revised upward, capping a quarter that most likely will see consumer spending pick up after a tepid start to the year. The value of overall sales advanced 0.5 percent, matching economists’ projections, after the prior month was revised up to a 1.3 percent gain from 0.8 percent, Commerce Department figures showed Monday.

- U.S. industrial production increased in June, boosted by a sharp rebound in manufacturing and further gains in mining output, the latest sign of robust economic growth in the second quarter. The Federal Reserve said on Tuesday industrial production rose 0.6 percent last month after falling 0.5 percent in May. It accelerated at a 6.0 percent annualized rate in the second quarter after a 2.4 percent growth pace in the first quarter.

Weaknesses

- Housing starts decreased to a seasonally adjusted annual rate of 1.173 million in June, according to the U.S. Department of Commerce. The figure was 12.3 percent below the May rate of 1.337 million and 3.0 percent lower than the June 2017 rate. Single-family home starts fell 9.1 percent from last month. Multifamily declined 20.2 percent since May and are down 15.3 percent since June 2017.

- President Donald Trump told CNBC's Joe Kernen in an interview aired Friday morning that he was ready to place tariffs on all $505 billion worth of Chinese goods coming into the U.S. "I'm not doing this for politics — I'm doing this to do the right thing for our country," he said.

- U.S. government bond prices edged lower Wednesday as Federal Reserve Chairman Jerome Powell reiterated that the central bank would gradually raise interest rates. The yield on the benchmark 10-year U.S. Treasury note settled at 2.875 percent, compared with 2.862 percent Tuesday.

Opportunities

- Second quarter economic activity has markedly picked up pace from the first quarter. After the usual first quarter slowdown, the U.S. economy is expected to roar back in the second quarter. Next week’s advance GDP print is projected to show annualized growth jumping from the prior 2.0 percent to 4.0 percent in the three months to June, which would make it the biggest expansion since the third quarter of 2014.

- On Tuesday, the flash PMI releases from IHS Markit are expected to show manufacturing and services activity holding near June’s levels in July.

- On Wednesday, durable goods orders are forecasted to rebound by 2.5 percent month-on-month in June from a 0.4 percent dip in the prior month.

Threats

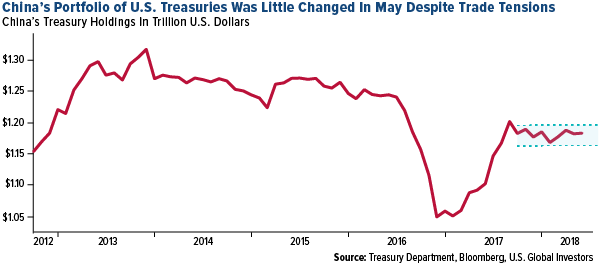

- China is still the largest foreign holder of U.S. debt, despite rising trade tensions between the world’s two biggest economies. The Asian nation’s stockpile of Treasury bonds, bills and notes held steady at $1.18 trillion in May, after dropping the previous month. Escalating trade tensions could cause China to retaliate against the U.S. by dumping its Treasury holdings, pushing U.S. interest rates higher.

- Consumer sentiment has retreated from its highs on mounting concerns over tariffs and geopolitical tensions. Next week’s release of the University of Michigan Consumer Sentiment survey is likely to reflect continued apprehension amongst consumers.

- The European Central Bank (ECB) surprised many at its June meeting by announcing the full details of the decision to end its asset purchases and when to expect the first rate increase. Traders will be looking for more clues on the central bank’s ambiguous timeline of a rate hike on Thursday.

Gold Market

This week spot gold closed at $1,232.00 down $9.45 per ounce, or 0.76 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.19 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index came in off 1.78 percent. The U.S. Trade-Weighted Dollar reversed course this week and slipped 0.23 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jul-15 | China Retail Sales YoY | 8.8% | 9.0% | 8.5% |

| Jul-18 | Eurozone CPI Core YoY | 1.0% | 0.9% | 1.0% |

| Jul-18 | Housing Starts | 1320k | 1173k | 1337k |

| Jul-19 | Initial Jobless Claims | 220k | 207k | 215k |

| Jul-25 | New Homes Sales | 670k | -- | 689k |

| Jul-26 | Hong Kong Exports YoY | 8.1% | -- | 15.9% |

| Jul-26 | ECB Main Refinancing Rate | 0.00% | -- | 0.00% |

| Jul-26 | Initial Jobless Claims | 215k | -- | 207k |

| Jul-26 | Durable Goods Orders | 2.8% | -- | -0.4% |

| Jul-27 | GDP Annualized QoQ | 4.1% | -- | 2.0% |

Strengths

- The best performing metal this week was platinum, nearly flat but down 0.07 percent after rallying 2.60 percent on Friday. Swiss exports of gold rose 2.3 percent in June, reaching 117.6 tons, according to the Swiss Federal Customs Administration. The majority of those exports – 62 percent or 61.3 tons – went to China, while 21 percent or 18.9 tons went to India. Swiss imports of gold were down 5.3 percent to 173.6 tons. Furthermore, exchange-traded funds focused on commodities saw inflows during this past week, with precious metal ETFs leading the pack at $63.2 million of gains.

- Although gold has seen a selloff in the past few days, Oversea-Chinese Banking Corp economist Barnabas Gan believes it is “likely overdone at this juncture,” reports Bloomberg. “Prices have moved lower on higher interest rate expectations following Fed Chair Powell’s comment amid a relatively positive growth outlook,” says Gan. Meanwhile, the U.S. Treasury reports that Russia is quickly liquidating U.S. dollar assets. Since the U.S. imposed heavier sanctions on Putin’s allies in April, the country has sold $81 billion worth of U.S. government debt, totally four-fifths of its cache.

- On Monday, Lundin Mining announced its $1.4 billion all-cash offer to buy Nevsun Resources, a proposition which Nevsun’s CEO believes “ignores the fundamental value of Nevsun and its assets.” As a result, Nevsun advised its shareholders to not act on Lundin’s statement. In contrast, Sibanye approved to a gold and palladium streaming agreement with Wheaton Precious Metals that will grant them a $500 million upfront cash payment.

Weaknesses

- The worst performing metal this week was palladium, down 4.74 percent likely on worries over the consideration of tariffs on automobiles which would likely hit car sales. As the bullion price slump continues to deepen, gold traders and analysts expressed a bearish outlook in Bloomberg’s weekly survey. Federal Reserve Chairman Jerome Powell announced that the central bank intends to continue raising borrowing costs, aiding the dollar and decreasing the yellow metal’s appeal. In light of this statement, the Bloomberg Dollar Spot Index rose to a two-week high, while gold-backed exchange-traded products fell to the lowest since March.

- The U.S. dollar strengthened in the days following Powell’s optimistic assessment of the domestic economy. The growth held up according to the Beige Book economic report. Unexpectedly, jobless claims dropped by 8,000 in July, down to 207,000 claims according to the Labor Department. In light of this, the bullion price fell to its lowest in a year. Rising open interest and falling prices may result in increased short positions.

- U.S. hedge fund Paulson Co. isn’t backing down in its fight against the management of Detour Gold Corp. On Thursday, Paulson Co. announced plans to call a special shareholder meeting, no later than July 28, where it will ask its shareholders to oust a majority of the company’s board of directors, reports the National Post. According to Bloomberg, Barrick Gold might be an undisclosed bidder for Detour Gold. People familiar with the matter say Barrick was asked to sign a confidentiality agreement alongside John Paulson to discuss this possibility. In other gold company news, Jake Klein, the executive chairman of Evolution Mining, says that the gold producer will consider using a strong cash position to add overseas assets to its Australian portfolio, reports the Financial Review. Evolution could have its sights Detour.

Opportunities

- President Donald Trump may be making gold great again, according to Bloomberg. Trump criticized the Federal Reserve for raising interest rates and “taking away our big competitive edge.” The president believes America “should not be penalized because we are doing so well.” After Trump’s comments, gold futures headed for the biggest increase in over two weeks.

- During Federal Reserve Chairman Jerome Powell’s testimony this week, he emphasized that the federal funds rate would rise “for now.” This careful choice of words suggests that the policy of raising rates a quarter point every quarter will not last, suggests Cornerstone Macro, as the bias is not toward faster rate hikes. “There is little reason to raise rates much further, invert the yield curve, put the brakes on the economy and risk that it does, in fact, trigger recession,” wrote the President of the Federal Reserve Back of Minneapolis.

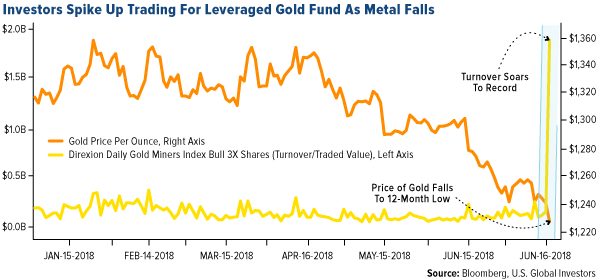

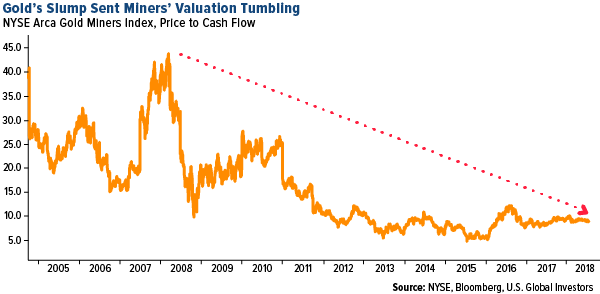

- While gold has fallen approximately $158 from its $1,369 peak in April, David Brady of Sprott Money is optimistic about the yellow metal. When comparing prior cases of gold falling over $95, Brady found that “it is reasonable to expect ‘at least’ a healthy bounce soon” according to the historical data. This outlook is supported by Direxion Daily Gold Miners Bull 3X Shares (NUGT), which had over 80 million shares valued at more than $1.8 billion trade this week. This is the largest volume the fund has ever seen. We have now seen the gold stocks outperform gold bullion for the last 6 weeks and that mights have something to do with the very bullish buyer who took on the above mentioned trade. On the chart below the price to cash flow (P/CF) ratio is charted for the NYSE Arca Gold Miners Index and we can see that this metric has based for about 6 years, as the miners have reduced debt and reigned in cost. The gold miners are trading at a P/CF of about 9.8 while the S&P 500 sports a 14.2 P/CF. And now with President Trump expressing disdain for a stronger dollar, perhaps the pendulum will swing to the other extreme.

Threats

- If the Federal Open Market Committee (FOMC) raises rates at the pace suggested by June’s forecast and the long-term yield remains at present levels, the yield curve could invert sometime in late 2018, according to Federal Reserve Bank of St. Louis President James Bullard. “The simplest way to avoid yield curve inversion in the near term,” says Bullard, “is for policy makers to be cautious in raising the policy rate.”

- Long delays in receiving environmental permits are costing mining companies millions. The U.S. relied completely on imports for 11 mineral commodities in 1984. By 2017, that number increased to 21. Domestic supplies are especially important now that the Trump administration aims to impose tariffs $34 billion worth of Chinese products, since China will likely respond in kind.

- Due to the Fed hikes and souring sentiment towards emerging markets, the dollar may remain strong for some time reports senior commodity strategist Harry Tchilinguirian. As a result, gold’s average price forecast was cut to $1,250 per ounce for 2018 and $1,100 per ounce for 2019.

July 19, 2018Based on Math Gold Is Set to Rally |

July 18, 2018Minute with the Manager: Meet Ralph Aldis |

July 16, 2018Oil Takes Center Stage: Commodities Halftime Report 2018 |

|||

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended July 20 was DigiPulse, which gained 182.56 percent.

- One of the world’s largest asset managers, BlackRock, has created a team to look into making use of cryptocurrencies, reports Financial News. According to the article, this includes taking part in the bitcoin futures market.

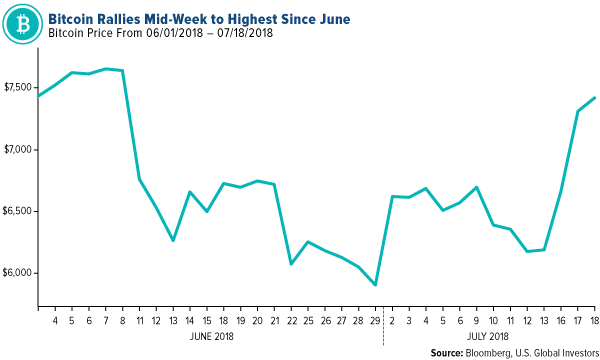

- On Monday, bitcoin headed for its largest increase in two weeks, reports Bloomberg, extending its rally into Wednesday breaking above $7,500 for the first time since June. Markets seem to be shrugging off some of the security and regulatory concerns that have plagued it for much of the year, the article continues.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended July 20 was DaTa eXchange, which lost 34.31 percent.

- Vietnam’s central bank said that it has agreed with the proposal set out by the Ministry of Industry and Trade to suspend the import of cryptocurrency mining machines, reports a local news agency. This move comes with hopes of improving the management of currency transactions in the country.

- Bitcoin was the currency of choice among the Russian intelligence officers indicted for hacking offenses related to the 2016 presidential campaign, the U.S. reported at the end of last week, writes Bloomberg. The indictment pinpoints conspirators using the digital tokens primarily when buying servers, registering domains and making other payments related to cyber breaches.

Opportunities

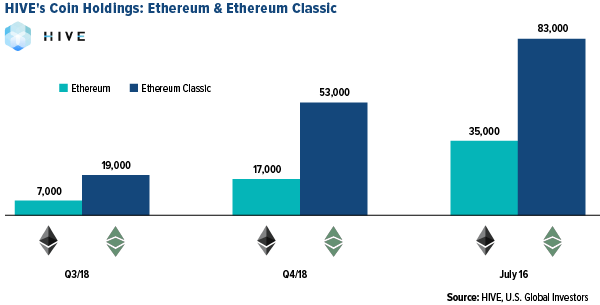

- Coinbase, the crypto exchange that currently lets users buy and sell four different digital coins, might let customers trade a longer list of tokens, reports Bloomberg. The company is looking into listing Cardano, Basic Attention Token, Stellar, Zcash and Ox, although none can be guaranteed at being added. In related industry news, HIVE Blockchain Technologies reported its financial results for fiscal year 2018 this week, noting operational highlights completed in the fourth quarter as well as its acquisition of Kolos Norway AG. The team also shared the chart below, showing that HIVE has already mined a higher number of Ethereum coins in the first quarter of 2019 than in September 2017 through the fourth quarter of 2018.

- Major League Baseball is getting into the cryptocurrency game with the launch of MLB Crypto Baseball, reports Seeking Alpha. “Gamers will pay an ether to buy a digital avatar, which are tied to specific moments in recent games,” the article continues. You can check out a short demo by going to https://mlbcryptobaseball.com/ .

- The CFA Institute announced that it will be adding topics on cryptocurrencies and blockchain to its Level I and II curriculums for the first time next year. The CFA exams are a grueling three-level program that has helped train 150,000 financial professionals, writes Bloomberg. It appears the digital currency market might be around for quite some time based on the news.

Threats

- An article from TechSpective.com this week reminds investors about some of the growing risks surrounding the cryptocurrency space. “Many people wrongly assume that digital currencies are somehow more secure than regular financial transactions, but in fact cryptocurrency can pose greater risks because no authorized oversight bodies exist to regulate these digital financial transactions,” the article explains.

- As bitcoin’s share of the entire digital currency market has reached a three-month high of 45 percent, reports MarketWatch, some think it may be one of the few coins that will survive. This trend continued on Friday, as other major altcoins other than bitcoin were all in the red in early trading. Ripple’s XRP coin, for example, is the worst performer of the smaller coins, down 3 percent this morning.

- “Malicious cartels might be lurking on your blockchain,” write researchers from Cornell University in a paper published last week. As Coindesk reports, the paper outlines a vote manipulation scheme it termed a dark decentralized autonomous organization, or “dark DAO.” This dark DAO is set up using smart contracts, would be undetectable, and would buy users votes in order to overwhelm governance systems, the article continues, issuing false signals or engaging in market manipulation.

Energy and Natural Resources Market

Strengths

- Iron ore was the best performing major commodity this week rising 0.59 percent. The commodity posted its second consecutive weekly advance after news of further environmental controls in China’s steel industry may trigger demand for higher quality iron ore inputs.

- The best performing sector this week was the Alerian MLP Index. The index rose 1.91 percent after FERC released an order that analysts called a "lifeline" for MLPs to hang on to their income tax allowance.

- The best performing stock for the week was OCI N.V. The Dutch producer of fertilizers rose 8.98 percent after analyst reports suggested the company can expect accelerating earnings and higher cash generation ability as a result of higher fertilizer prices.

Weaknesses

- Lumber was the worst performing commodity this week. The commodity dropped 14.56 percent, posting its worst weekly drop in at least three years after U.S. housing starts and building permits fell in June to the slowest rate in nine months.

- The worst performing sector this week was the S&P/TSX Oil & Gas Producers and Explorers Index. The index dropped 3.72 percent after crude oil prices declined for a third consecutive week.

- The worst performing stock for the week was Alcoa Corp. The Pittsburgh-based aluminum producer dropped 14.68 percent to fresh year-to-date lows after the company lowered its 2018 profit projection as tariffs on imported aluminum present a “significant” headwind.

Opportunities

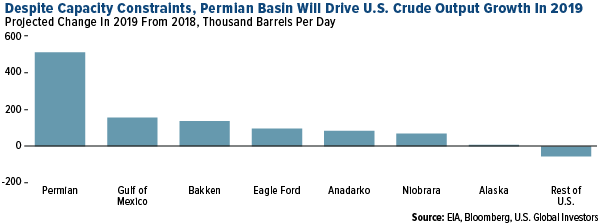

- U.S. crude oil production will continue to rise despite capacity constraints. The Permian will remain the key driver of U.S. oil production growth in 2019. The basin is forecast to average 3.9 million barrels a day (bpd) in 2019, a 514,000 bpd increase from 2018, according to an EIA report.

- Rio Tinto Ltd. and Vale SA. have reported big increases in iron ore shipments in the second quarter of 2018, reflecting rising confidence among global producers of the steel-making commodity despite concerns over the impact of trade tensions on future demand.

- Steel container cargo volumes reached record heights at the Port of Long Beach last month, surging past the previous mark, and distinguishing June 2018 as the port’s best month ever. Trade increased 14.2 percent in June, compared to the same month in 2017.

Threats

- U.S. and Western officials are considering an eventual emergency release of stockpiled oil if new supplies can’t prevent another sharp rise in prices. The Trump administration is actively assessing whether to dip into the country’s emergency oil stocks while it simultaneously pushes other countries to boost their output.

- GDP data revealed a slowing Chinese economy in the second quarter, weighed down by government initiatives to rein in risky borrowing and lending. Growth edged down, in line with expectations, to 6.7 percent from a year ago, compared with 6.8 percent in the first quarter.

- The European Union will consider introducing tariffs on coal, pharmaceuticals and chemical products from the United States if President Donald Trump imposes restrictions on European cars. “Depending on progress made during the visit of European Commission President Jean-Claude Juncker, the member states will decide on their future strategy at the end of next week.”

China Region

Strengths

- China’s second quarter gross domestic product (GDP) came in right in line with expectations at 6.7 percent year-over-year—slower than the first quarter’s 6.8 percent but still ahead of the overall 2018 target of 6.5 percent. China’s year-over-year retail sales for June came in strongly as well at 9.0 percent, better than analysts’ anticipated 8.8 percent and up from May’s 8.5 percent.

- China’s new-home prices rose 1.1 percent in June, climbing at their fastest pace in some 21 months.

- The utilities sector was the top-performing one in the Hang Seng Composite Index (HSCI) this week—and the only one in the green—rising 2.49 percent.

Weaknesses

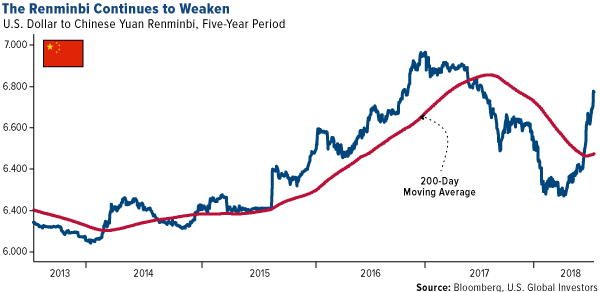

- China’s yuan continued to weaken this week, crossing the 6.8 mark on Friday and setting new 52-week lows.

- Taiwan’s export orders missed expectations this week, coming in at a year-over-year decline of 0.1 percent for June, well off from analyst’s anticipated 7.4 percent growth rate and down from last month’s 111.7 percent pace.

- Consumer goods was the worst-performing sector in the HSCI for the week, falling 2.86 percent in that time.

Opportunities

- Chinese Tencent-backed e-commerce operator Pinduoduo announced plans for an upcoming U.S. initial public offering (IPO) in which the company may seek a valuation of up to $20 billion.

- While the U.S. Federal Reserve remains—and should remain—fully independent, one potential positive of recent attention to the U.S. dollar strength and the state of the economy this week is that it serves as a reminder that if the Fed were indeed to slow at all in its pace of hikes, a weaker dollar may well ease pressure on emerging market currencies, all else being equal.

- Prime Minister Narenda Modi defeated a no-confidence vote in India’s parliament and may have garnered additional political capital and room to maneuver in so doing.

Threats

- Tariffs, tariffs, tariffs. The topics of “trade wars” and “tariffs” remain relevant for global investors in the near future, especially as U.S. President Donald Trump announced on Friday that he was “ready to go to 500”—referring to the amount of goods he’s willing to impose tariffs on.

- Central banking policies remain relevant as well. While Hong Kong’s U.S. dollar peg buffers it to some degree against broader emerging market forex issues, the region in general remains subjected to outsize effects of movement in the U.S. dollar, and therefore Fed policy. At the same time, China’s choice to permit weakening of the yuan may have broader effects as well (as may a trade war). Indonesia’s central bank stood pat at its most recent meeting, while the Philippines is talking up “strong follow-through monetary adjustment.”

- Malaysia’s finance minister Lim Guan Eng cut the outlook for his country’s economic growth back to about 5 percent for 2018, down from the central bank’s prior expectations for 5.5 to 6 percent growth, Bloomberg News reported this week.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 4.7 percent. The country lifted a state of emergency Thursday, imposed after the failed coup attempt back in 2016. Under a new presidential system of government in Turkey, established earlier this month, President Erdogan was given expanded powers to issue legislative decrees similar to the ones issued under the state of emergency.

- The Turkish lira was the best performing currency this week, gaining 90 basis points against the U.S. dollar. The lira appreciated despite the dollar rally following comments from Federal Reserve Chairman Jerome Powell on the strong U.S. economy and future rate hikes. The central bank will meet next week, and most economists predict a small rate increase.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 4.2 percent. Domestic and international politics weighed on Russian equities. Trump and Putin’s meeting that took place on Monday in Helsinki created tension among U.S. politicians. Trump has been criticized to side with Putin against American intelligence agencies. New sanctions could be announced on Russia.

- The Russian ruble was the worst performing currency this week, losing 1.4 percent against the U.S. dollar. The ruble depreciated in line with Brent crude oil, which lost 3 percent.

- Information technology was the worst performing sector among eastern European markets this week.

Opportunities

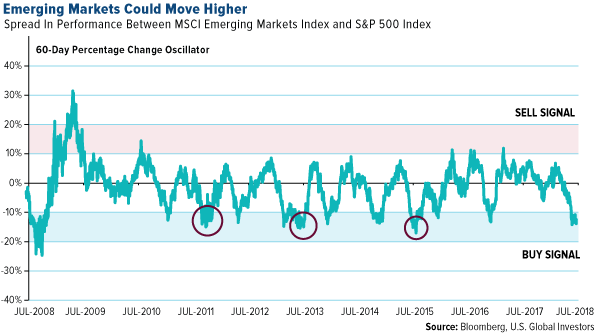

- Goldman Sachs, Franklin Templeton and Black Rock said that emerging market stocks are ready to rock and roll. As the chart below illustrates, emerging market equites have underperformed the U.S. large-caps recently and could be due for a rebound.

- The release of preliminary July PMI data takes place next week and most Bloomberg analysts are predicting no significant change, with the composite PMI at 54.8, well above the 50 level that separates growth from contraction. Moreover, next week the European Central Bank (ECB) will meet. Most likely, the policy rates will remain unchanged but investors will be looking for signs of monetary easing policy reversal.

- U.S. President Donald Trump had invited Russian President Vladimir Putin to visit the White House in the fall. Foreign leaders traveling to Washington to visit the White House are typically extended an invitation to Capitol Hill, but Congress announced that Putin is not welcome. Putin’s visit will be controversial indeed. Trump is under investigation by the FBI for colluding with Vladimir Putin to influence the 2016 U.S. elections. However, if Putin does come to the White House, it could be positive for his approval rankings in his home country.

Threats

- According to the latest polls, Putin is losing popularity. Hours before the World Cup started last month, he announced an unpopular pension reform, proposing the new retirement age for women at 63 and men at 65. Currently, women can stop working at 55 and men at 60. The percentage of Russians who trust Putin dropped to 40 percent from 80 percent after the annexation of Crimea in 2014.

- Trump threatened to impose 25 percent tariffs on imports of cars and parts that would affect our major trading partners: Canada, Mexico, Europe, Japan and South Korea. According to Cornerstone Macro research, extending major tariffs to automobiles is a big step. It would mean Trump is not limiting his trade agenda to unfair trade practices but is pursuing a nakedly protectionist agenda that would likely unleash a much more broad-based and economically consequential trade conflict, Andy Laperrier wrote in his report.

- Poland’s most outspoken proponent of tighter monetary policy believes the central bank cannot wait too much longer before delivering its first increase since 2012. Poland needs to end its longest-ever rate pause because of a “really worrisome” rebound in core inflation, according to one of 10 members of the Monetary Policy Council. The core inflation is set to triple to 2.1 percent in 2018 from this year’s average level. Last week the policy rate was left unchanged at 1.5 percent.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits