Summary

Despite rising uncertainties, the global economy has been resilient. Escalating trade tensions, coupled with tightening liquidity conditions, have not yet had a notable impact on global growth. However, protectionism, a stronger U.S. dollar and increasing risks of a hard Brexit are casting doubt over an otherwise thriving global economy.

Developing risks have put the focus back on emerging markets (EMs) and their domestic weaknesses. The majority, if not all, of the EM currencies have suffered over the last couple of months. For them, the focus is likely to be on getting their houses in order to limit further damage from an uncertain external environment.

Our baseline expectation is that strains on both the trade and political fronts will be defused, but the risks continue to remain tilted to the downside.

The following is an overview of our expectations for key markets.

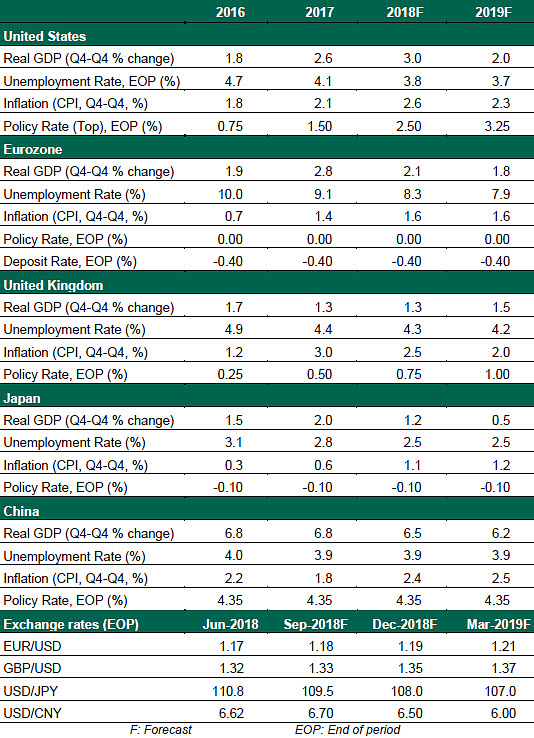

United States

- The initial estimate of real U.S. gross domestic product (GDP) in the second quarter was a strong 4.1% (annualized), led by net exports. The prospect of imminent trade actions may have led to front-loading of purchases before any tariffs were enforced.

- In the second half of the year, the persistent impacts of tax reform position the U.S. for continued growth. However, we expect the expansion to downshift to a more sustainable rate in 2019, as temporary incentives from tax reform expire and the costs of trade actions become more apparent.

Eurozone

- Amid the gloomy trade environment, some silver linings are emerging. The European Union (EU) and Japan signed a trade agreement, one of the largest in the world to date.

- Another more positive development includes an agreement between the EU and the U.S. to suspend threatened tariffs and to “resolve” the steel and aluminum tariffs as well. The progress is encouraging, but the agreement lacks specifics. If recent patterns in these kinds of agreements serve as an example, it is too early to rejoice.

- Key risks for the eurozone include Italy’s high public debt and renewed discontent over refugees, which nearly broke up Angela Merkel’s coalition government last month in Germany.

United Kingdom

- Brexit talks have stalled, with U.K. Prime Minster Theresa May’s plan facing opposition from all sides. Even the parliamentary calculation around Brexit after recent resignations of hard-Brexiters is looking more challenging now.

- The probability of a “hard” Brexit, defaulting to World Trade Organization (WTO) rules, with tariffs and hard borders, has risen notably on the back of recent events. Though we continue to expect a “softer” Brexit that preserves access to the common market, the path to that conclusion is looking less clear.

- Incoming economic data isn’t entirely in line with the Bank of England’s narrative, yet we do not expect it will be enough to derail the August rate hike.

Japan: Speculations over Monetary Policy

- Recent speculation that the Bank of Japan might tweak its stimulus led to a spike in Japanese Government Bond yields. Contrary to speculations, the central bank in its July meeting vowed to maintain “extremely low” interest rates “for an extended period of time”. We see no change in the monetary policy stance.

China: Currency Back in Focus

- Besides the increasing likelihood of a trade war, the weaker Chinese yuan is emerging as another problem area for Chinese policymakers.

- China is pushing to get some nations on their side with regards to the trade tariffs, but hasn’t been successful. China tried to convince the EU to launch joint action against the U.S. at the WTO. Perhaps due to interests shared by both the U.S. and the EU, the latter refused to side with the Chinese.

- On the growth front, policymakers are continuing with their easing. Following the recent reduction in bank reserve requirements, the People’s Bank of China injected $74 billion into the financial system. Stimulus measures including business tax cuts and increased spending on infrastructure were also announced recently.

- Overall, we expect China to remain in an easing position without moving benchmark interest rates.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2018 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Global Economic Forecast – August 2018

© Northern Trust

Read more commentaries by Northern Trust