No Dog Days This Summer

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOn a personal level, summer is often a season that affords an additional measure of leisure. Some take vacations, while those still at their posts often leave on time to enjoy the long evenings.

As we move through the summer of 2018, the U.S. economy is showing no signs of slacking off. A strong second quarter was highlighted by continued job growth, manageable inflation and robust consumer spending.

This idyll may not last, however. The boost provided by tax reform will likely fade as the year proceeds, and rising inflation has attracted the Federal Reserve’s attention. The uncertainty presented by spreading trade skirmishes may impair growth while boosting prices.

We remain constructive on the outlook for this year, but foresee a return to more modest progress in 2019.

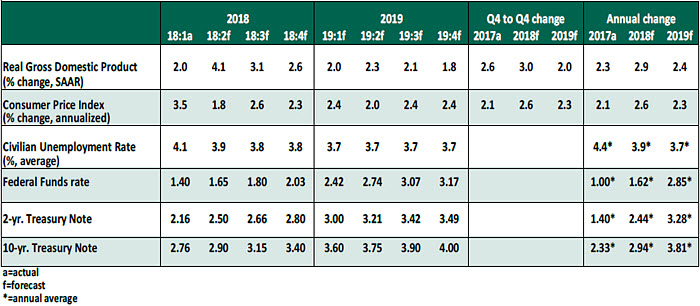

Key Economic Indicators

Influences on the Forecast

- The initial estimate of real gross domestic product (GDP) for the second quarter showed annualized growth of 4.1%, in line with consensus expectations. Consumer spending was strong, reflecting a positive employment situation and some temporary incentives from the Tax Cuts and Jobs Act of 2017.

- Export growth was another driver of the good result, but this is likely to be temporary. Foreign buyers of U.S. goods appear to have front-loaded their orders in anticipation of market disruptions from tariffs. Bear in mind that the first significant trade action, the Section 232 tariffs on steel and aluminum, went into effect June 1. The Section 301 actions against China did not occur until July. Official statistics won’t reflect trade protection until more time has passed.

- The housing sector continues to lag overall economic performance. Real residential fixed investment fell for the second straight quarter, and readings on home sales have also stepped back. Higher mortgages rates and reduced tax benefits from home ownership have been identified as root causes.

- Business investment progressed in the second quarter, but at a reduced rate. To date, the evidence suggests that a majority of corporate tax savings have been returned to shareholders and not used to upgrade internal operations.

- The unemployment rate improved slightly, to 3.9% in July from 4.0% in June. Though the number of jobs created In July was slightly below the anticipated level, revisions to prior months were robust. Hourly wage growth remained at 2.7% over the past 12 months, even though anecdotes of worker shortages are multiplying.

- Inflation is steadily increasing. The consumer price index grew 2.9% year-over-year in June, the highest level seen thus far in this economic cycle. The deflator on core personal consumption expenditures, the Fed’s preferred measure of inflation, has increased 1.9% over the past year, just shy of the Fed’s target of 2%. As unemployment remains low and trade actions increase costs, we forecast steady upward pressure on inflation.

- As widely anticipated, the Federal Open Market Committee took no action at its July meeting, affirming the current Fed Funds rate range of 1.75% to 2.0%. The theme of the Committee’s subsequent statement was strength, using the word “strong” to describe the economic activity, job gains, business investment and household spending. With such a positive signal, we expect to see quarter-point rate increases in the FOMC’s September and December meetings this year, with more hikes to follow in 2019.

- Long-term interest rates have remained low, though the 10-year U.S. Treasury yield touched 3% briefly last week. Yields have also been boosted recently by higher-than-normal volumes of issuance. We expect long-term yields to gradually increase along with short-term rates.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2018 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All