Why Emerging Market Stocks Are Looking Cheap

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAs Russ explains, dismal performance of emerging markets this year has make them look like a bargain again.

Following a stellar 2017, emerging market (EM) equities are once again on the back foot. The MSCI Emerging Market Index is trailing developed markets stocks by roughly 8% this year, despite rallying in recent weeks. Unlike the U.S., EM equities never enjoyed a real bounce since the late winter sell-off.

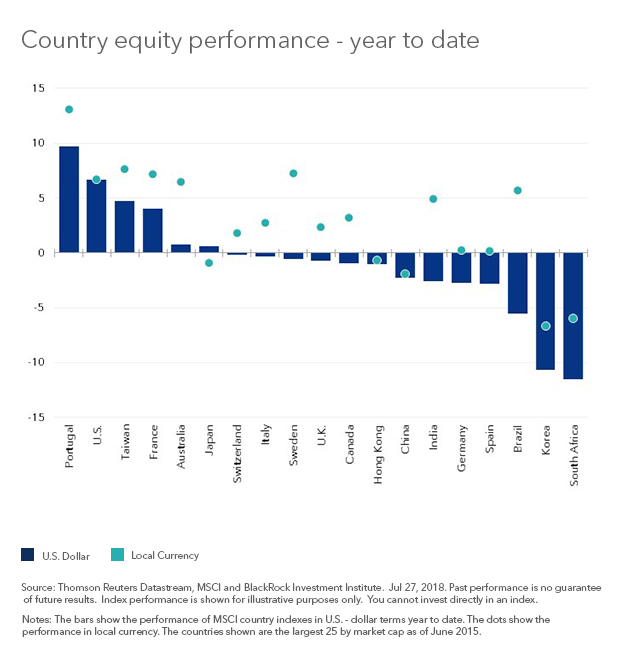

With the exception of a few outliers, notably Russia and Mexico, most of this year’s worst performing equity markets are EMs (see Chart 1). Developed market stocks, led by the United States, have recouped most of their winter swoon. In contrast, EM stocks are still down 14% from their January high in dollar terms.

The consequence of the selloff? EM stocks are once again looking like a bargain. Here’s why:

Valuations once again look cheap.

The MSCI Emerging Market Index is trading at 13.5 times trailing earnings and 11.3 times forward earnings. The former represents a 26% discount to developed markets. Based on price-to-book (P/B) EM stocks look even cheaper, with a 30% discount to DMs the largest since the summer of 2016 and significantly below the post-crisis norm of around 17%.

Economic data is improving.

After a dismal spring, EM economic data is starting to improve, at least relative to expectations. This year’s underperformance coincided with a rapid deterioration in EM economic prospects. From late March through mid-June the Citi EM Index of Economic Surprises plunged from +40 to -25. In other words, economic data went from reliably beating expectations to chronically missing estimates. Since mid-June things have started to look better; economic data is strengthening relative to expectations.

The dollar rally has stalled.

The dollar remains a real threat to EM assets. That said, the Dollar Index (DXY) has been mostly contained the past two months. Unlike earlier this spring, European and Chinese growth prospects are stabilizing. At the same time, the dollar is no longer a crowded short, as it was earlier in the year. While a relatively strong U.S. economy still suggests an upward trajectory for the dollar, the ascent no longer looks so steep.

Risks remain.

A more constructive view on EM equities comes with three big caveats: financial conditions, trade and precision. As painfully demonstrated, despite secular improvements in current account positons and financial stability, EM assets are still vulnerable to tightening U.S. financial conditions. This is particularly true when Federal Reserve tightening is accompanied by a stronger dollar. With the U.S. economy experiencing good momentum, the Fed is likely to continue to tighten into 2019.

And while trade issues have faded in recent weeks, fundamental tensions with China have not been resolved. If trade concerns escalate, EM assets are vulnerable.

Finally, it is important to remember that EM equities are not a homogenous asset class. In reality EM is a heterogeneous collection of countries, with wildly varying fundamentals and valuations. Turkey is not Taiwan and Brazil is not Poland.

I see the best opportunities and value in EM Asia. While not without its risks, this segment of the world looks to once again offer some value.

Russ Koesterich, CFA, is Portfolio Manager for BlackRock’s Global Allocation team and is a regular contributor to The Blog.

Investing involves risks, including possible loss of principal.

International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks may be heightened for investments in emerging markets.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of August 2018 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

©2018 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

USR0818U-564833-1780650

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All