In the Blink of an Eye, Gold Spikes Higher

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits |

In my interview earlier this week with Kitco News' Daniela Cambone , I told investors that when gold is ready to reverse course, we could see it happen in the blink of an eye!

That’s exactly what took place on Friday morning.

Gold prices moved up close to 2 percent today, and gold stocks climbed even higher following comments from Federal Reserve Chair Jerome Powell. During his speech at the Jackson Hole Economic Symposium, Powell reiterated the central bank’s commitment to raise interest rates gradually while the U.S. economy continues its strong performance.

Despite the positive moves for the yellow metal today, I remain bullish that gold has much higher to climb.

Really, No Inflation? What About “Fake” CPI?

At the start of the week, CNBC reported that the average price of a Toll Brothers home rose to $851,900 in the third quarter. That’s up from $791,000 a year earlier! Not only that, the cost of a 30-year mortgage continues to rise over the last 12 months, according to the latest data from Freddie Mac. Add in gas at the pump and food, and inflation is up more than 2.9 percent. Yup, no inflation!

Pay Attention to PMI and Trade Wars

I want to remind investors to remain cautious while sifting through the latest economic releases and headlines dominating their news feeds. Trade wars continue to escalate at a faster pace than previously expected and manufacturing activity around the world seems to be slowing down, as evidenced in PMI releases. Consequently, a bulk of commodities are still feeling the pressure.

As I’ve written about many times, the purchasing managers’ index (PMI) is an important forward-looking economic indicator that we closely monitor to make sense of the world economy. Manufacturing PMI gathers data such as global output, new orders, exports and prices. GDP, on the other hand, is important, but more like looking through your rearview mirror.

On that note, I want to leave all of our loyal shareholders and readers with this special commentary as we head into the weekend. I hope you enjoy it.

The 5 Dimensions of a Rich Life

Studies show that mindfulness and having an attitude for gratitude is important in all aspects of life. One way to increase gratitude is to regularly take stock of not only your finances, but the other dimensions of your life as well. This includes relationships with family and friends, personal and professional achievements, and ways in which you give back.

During my recent trip to the Oxford Club’s Private Wealth Seminar in Whistler, I was reminded of this very topic. I had the privilege of hearing from numerous inspiring and intelligent investment professionals during the event, including my good friends and chief strategists at the Oxford Club, Alex Green and Marc Lichtenfeld.

One of the presentations, however, really stood out to me. The topic included the five dimensions to living a rich and fulfilling life, a theme also covered in Alex Green’s book Beyond Wealth.

The key? Being “rich” isn’t all about money.

1. Monetary Gain and Financial Freedom

When you think of richness, you likely go straight to monetary wealth. Granted, this dimension of life is incredibly important, but what’s more important are the steps taken to achieve a sense of financial stability. Having the knowledge and skills to responsibly build wealth can bring a sense of strength, comfort and safety that is unmatched.

This is particularly true for those approaching retirement age, a time when families don’t want to rely on the government for assistance, but instead want a nest egg, and then some.

As demonstrated in one of my favorite books, The Millionaire Next Door, the average millionaire doesn’t make ostentatious displays of wealth, rather they under consume and live in average-to-middle class neighborhoods and focus on investing. Simple strategies like these can make a world of difference.

2. Extraordinary Experiences

|

Are you challenging yourself to stray from your everyday activities? Extraordinary experiences, such as traveling the world, bring a new perspective to life. Pushing yourself out of your comfort zone is the key to growth.

I often write about the importance of explicit and tacit knowledge, with tacit knowledge referring to real world experiences, or boots-on-the-ground research. I have always believed this type of knowledge is just as important as textbook knowledge. Having your driver’s license, for example, is simply a piece of paper. It means nothing until you put it to use, get out on the open road and explore.

I travel often for both business and leisure and it’s true that you have to see the sights, taste the food, meet the people and hear the music to experience the limitless delights that the world has to offer.

3. Personal Achievement

Everyone has different goals they set out to accomplish in their lifetime. Taking time to list out all of your personal achievements thus far, as well as the goals you’re still working toward, is one way to truly put things in perspective.

Continuing the pursuit of personal achievement keeps you active physically and mentally, and encourages you to keep learning. One personal achievement I am very proud of is my completion of numerous marathons all over the world. Running these races was challenging no doubt, but equally as rewarding.

4. Ways of Giving Back

One of the many rewarding aspects of life is having the ability to make a lasting impact on your community and those around you. Giving back typically comes in the form of volunteering, whether it’s with your time or money, to help support causes close to your heart. At U.S. Global Investors we make it a point to support our local community and I’ve always encouraged employees to volunteer for and share causes important to them.

5. Strong Relationships– Intellectual and Emotional

Love and friendship are easily two of the most meaningful components of a rich and fulfilling life, and both are achieved through strong relationships. Whether at home or at the office, surrounding yourself with like-minded, passionate, successful and caring individuals can truly be the driving force behind how you choose to live your life.

Social wealth and a sense of connection are just as powerful as financial wealth. Self-confidence and self-worth are important feelings, and often times, high self-worth is correlated with high net worth. To me, relationships are one of the most rewarding aspects of life and in this video I discuss the crucial role that mentors played in mine. The wisdom and experience of someone who has walked a different path than you, or who is further down the road than you are, can help steer you away from setbacks or roadblocks to maintain a balanced life.

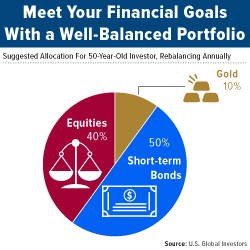

Maintaining a Well-Balanced Portfolio

|

| click to enlarge |

Interpersonal relationships aren’t the only thing that a fulfilled person should balance. It’s never too late to start learning the basics of a well-managed portfolio.

One rule of thumb is to have an ever-shifting balance between equities and bonds, with some exposure to gold for diversification. Traditionally, equities are more growth-oriented than bonds, but also hold greater risk. As you age, your portfolio should evolve to contain a higher allocation to bonds, which favor safety and liquidity over growth.

Learn more about investment opportunities in the bond market by clicking here!

I believe it’s prudent that your allocation to bonds be equal to your age, as seen in this chart. Follow the 10% Golden Rule, and put the remainder of your portfolio in equities.

As a refresher, here’s what I mean by the “10% Golden Rule”. The rule suggests a 10 percent portfolio allocation to gold, with 5 percent in bullion or gold jewelry and 5 percent in well-managed gold mutual funds or ETFs.

Remember to rebalance annually, adjusting allocations and weightings as investment goals change.

While we have an eye for gold at U.S. Global, we also provide investors with a wide array of opportunities to invest with us, ranging from emerging markets and natural resources to infrastructure and domestic funds.

Explore potential opportunities for diversifying your portfolio by clicking here!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.47 percent. The S&P 500 Stock Index rose 0.86 percent, while the Nasdaq Composite climbed 1.66 percent. The Russell 2000 small capitalization index gained 1.93 percent this week.

- The Hang Seng Composite gained 2.25 percent this week; while Taiwan was up 1.11 percent and the KOSPI rose 2.05 percent.

- The 10-year Treasury bond yield fell 4 basis points to 2.81 percent.

Domestic Equity Market

Strengths

- Energy was the best performing sector of the week, increasing by 2.64 percent versus an overall increase of 0.86 percent for the S&P 500.

- Advanced Micro Devices was the best performing stock for the week, increasing 21.29 percent.

- The equity bull market is now the longest ever on record. Measured from its rise from the trough hit in March 2009, it has lasted an incredible 3,454 days.

Weaknesses

- Consumer Staples was the worst performing sector for the week, decreasing by 1.79 percent versus an overall increase of 0.86 percent for the S&P 500.

- L Brands was the worst performing stock for the week, falling 15.13 percent.

- Gap stumbled as same-store sales saw a bigger-than-expected drop. Shares fell nearly 7 percent in after-hours trading on Thursday after the retailer said same-store sales in the second quarter fell 5 percent. This was worse than the 2.55 percent drop that was expected, reported Reuters.

Opportunities

- Eventbrite is going public. The ticketing website hasn’t announced how much money it hopes to raise. However, it did say it would use the proceeds from an initial public offering to increase its capitalization and financial flexibility, as well as pay off its debt, which stands at $66.36 million according to an S-1 filing out Thursday.

- Xiaomi released its first results as a publicly traded company. Revenue soared 68 percent in the second quarter amid strong sales of smartphones and connected devices, reports Reuters.

- The world's largest publicly traded marijuana company hit a record high. Shares soared more than 11 percent on Monday, hitting a record high of $37.65 days after Constellation Brands upped its stake to 38 percent.

Threats

- Microsoft is reportedly being investigated by U.S. authorities for potential bribery and corruption over software sales in Hungary. The Washington Post reports than the Department of Justice and SEC are examining how the company sold software, such as Word and Excel, to firms that solid the programs in turn to Hungarian government agencies.

- BHP Billiton announced that statutory profit fell 37 percent as a result of its fatal Brazil mine disaster. However, it also declared a record dividend of $0.63 a share. The massive drop in profitability put into question the sustainability of the growth in dividends.

- Facebook, YouTube and Twitter could face fines if they fail to take down terrorist content within minutes. The EU Commissioner for Security Julian King is drawing up legislation which would force tech companies to take down terrorist content or face fines.

The Economy and Bond Market

Strengths

- Provided that the U.S. economy remains healthy, central bankers are prepared to raise interest rates again, according to a report from the Federal Reserve’s recent meeting. Minutes from the July 31 and August 1 Federal Open Market Committee Meeting stated that “[m]any participants suggested that if incoming data continued to support their current economic outlook, it would likely soon be appropriate to take another step in removing policy accommodation.”

- Strong U.S. macro and credit fundamentals should continue to support municipal bonds, wrote Mark Paris, head of state and local debt investments at Invesco. Paris stated that new tax revenues from internet sales and legalized gambling should "support the finances of state and local governments."

- The latest initial jobless claims edged lower, hovering near levels not seen since the Nixon administration. The release for the period ended August 18 coincided with the survey week for the August employment report and suggests that labor-market conditions are tightening further at the end of summer, reports Bloomberg Economics’ Tim Mahedy and Carl Riccadonna.

Weaknesses

- For the first time in four months, orders for U.S. durable goods fell in July due to a marked decrease in new contracts for passenger jets. A government report last Friday reported orders for long-lasting goods fell 1.7 percent in July. In a MarketWatch survey, economists forecast a 1.1 percent decline in durable goods.

- The IHS Markit Flash U.S. Manufacturing Purchasing Managers’ Index registered 54.5 in August, down from 55.3 in July. This is the lowest reading since November 2017. Rates of output and new business growth in manufacturing are slowing according to the latest data, which mirrors trends seen across the service sector.

- July marked the fourth straight month that U.S. home sales fell. This is the longest streak of monthly declines since 2013. A shortage of properties on the market pushed up house prices, likely putting off some potential buyers. Existing home sales fell 0.7 percent to a seasonally adjusted rate of 5.34 million units last month, according to the National Association of Realtors on Wednesday. In a Reuters poll, economists had forecast existing home sales would gain 0.6 percent to a rate of 5.40 million units in July.

Opportunities

- While the Treasury curve has been heading toward inversion, investors in U.S. municipal bond market have pushed its curve the other way. In fact, the difference in the slope of the two markets’ yield curves is almost at record levels. A reversal in that slope could create opportunities for savvy fixed-income traders.

- Next Wednesday, the second release of second quarter gross domestic product should confirm the robust economic growth seen during the quarter. Economists’ forecasts anticipate growth of 4.0 percent.

- Given its large weight in the economy, next Thursday’s release of personal consumption expenditures will be watched closely as an indicator of economic strength for the third quarter. Overall, personal spending has remained robust despite the ongoing trade conflicts.

Threats

- Consumer sentiment has shown signs of deterioration due to the ongoing trade conflict. The University of Michigan’s sentiment survey will be released next Friday. This is anticipated to show a further weakening in confidence.

- While unemployment is at all-time lows, personal income growth continues to grow at a tepid pace. Next Thursday’s personal income release is unlikely to see a change in that trend.

- The housing market has hit a slump in the last couple of months with sales of new and existing homes falling off a cliff. The release of pending home sales next Wednesday is likely to reinforce that weakness.

Gold Market

This week spot gold closed at $1,205.90 up $20.85 per ounce, or 1.76 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.73 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index surged 4.92 percent. The U.S. Trade-Weighted Dollar Index slid 0.97 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-23 | Initial Jobless Claims | 215k | 210k | 212k |

| Aug-23 | New Homes Sales | 645k | 627k | 638k |

| Aug-24 | Durable Goods Orders | -1.0% | -1.7% | 0.7% |

| Aug-27 | Hong Kong Exports YoY | 6.0% | -- | 3.3% |

| Aug-28 | Conf. Board Consumer Confidence | 126.5 | -- | 127.4 |

| Aug-29 | GDP Annualized QoQ | 4.0% | -- | 4.1% |

| Aug-30 | Germany CPI YoY | 2.0% | -- | 2.0% |

| Aug-30 | Initial Jobless Claims | 215k | -- | 210k |

| Aug-31 | Eurozone CPI Core YoY | 1.1% | -- | 1.1% |

Strengths

- The best performing metal this week was palladium, up 2.50 percent despite money managers flipping to net bearish positions in the futures market with Friday’s update. Gold traders have switched back to a mostly bullish outlook, as of Thursday’s afternoon survey, for the yellow metal this week, as it appears the price is nearing its floor, according to the weekly Bloomberg survey. Gold finally posted a weekly gain for the first time in seven weeks for the biggest weekly gain since March amid a protracted U.S.-China trade war and after the speech by Federal Reserve Chairman Jerome Powell. Gold miners, as measured by the Philadelphia Gold & Silver Index of mining companies, set its lowest 14-day RSI reading in 31 years, writes Bloomberg. This demonstrates that gold mining stocks are as oversold as they’ve been since the crash of October 1987.

- Chris Howard, director of precious metals at the United Kingdom’s Royal Mint, said this week that they’ve seen “a substantial pick-up in business which was further triggered when gold went below $1,200 last week.” Howard also shared that physical gold demand has increased more than 25 percent so far in the third quarter compared to the second quarter of this year. In the face of greater U.S. sanctions, Russia bought more gold in July than in any other month this year. The Russian central bank purchased 26.1 tons of the yellow metal last month, bringing its total holdings to 2,170 tons valued at $77.4 billion, according to the International Monetary Fund. Although much attention has been drawn to outflows of gold-backed ETFs in the U.S., the Chinese-listed Bosera Gold Open-End ETF has seen over $1 billion in inflows so far this year. Bloomberg writes that this is the second-most popular ETF backed by a precious metal, demonstrating that gold investments are flowing out in the West and flowing into gold funds in the East.

- Government think tank Niti Aayog has suggested that the Indian government slow the import duty on gold from the existing level of 10 percent in order to reduce gold smuggling into the country. Aayog also recommends that the GST rate be slashed from the current 3 percent level. Principal advisor Ratan P. Watal wrote in a recent report that “a reduction in the customs duty in the past in India has been argued to support tax compliance coupled with a significant reduction in the quantum of gold smuggled into India.”

Weaknesses

- The worst performing metal this week was silver, largely unchanged by the end of the week as hedge funds boosted their bearish silver view to a 19-week high. At the start of this week the naysayers were pushing their negative views on gold with a vengeance. Investors and analysts have questioned why gold prices aren’t higher due to rising geopolitical risks and why gold has been replaced by the U.S. dollar as the safe-haven investment. SkyBridge Capital told Bloomberg this week that the next big buying opportunity for gold might come when the Federal Reserve transitions to a looser monetary policy from the current tightening cycle now. However, senior portfolio manager at the firm Tony Gayeski said that “we’re a long way from that”, referring to another round of quantitative easing. Bloomberg reports that ETFs tracking gold have seen outflows for 13 consecutive weeks to mark the longest run in five years.

- Several assets are now hitting record net short positions: gold, 10-year Treasuries and now the euro went net short last week. A buildup of speculative short positions in the U.S. Treasuries market could set up traders for pain ahead, according to Jeffery Gundlach of DoubleLine Capital. According to the latest data from the Commodity Futures Trading Commission, net short positions on 10-year Treasuries from hedge funds have hit the highest level on record. In the currency futures, speculators are now net short euros for the first time since May 2017, writes Brown Brothers Harriman. Lastly, the bears have the upper hand in the gold futures market as speculators have the first net short position since late 2001.

- Mining companies in the Democratic Republic of Congo have established a Mining Promotion Initiative to discuss concerns about new mining code in the country that negatively impacts miners who account for 80 percent of cobalt and 90 percent of gold production. These companies are working together to addresses issues in the new Congo mining code which they believe could discourage further investment in larger and small sustainable projects.

Opportunities

- The dollar saw its biggest selloff in a month today when the People’s Bank of China (PBOC) and the Federal Reserve “delivered a one-two punch”, reports Bloomberg. Katherine Greifeld writes that “the PBOC announced that banks would resume a ‘counter-cyclical’ factor when calculating the yuan’s daily reference rate, restraining the influence of market forces that have been driving the currency lower versus the greenback.” Federal Reserve Chairman Jerome Powell said in a speech at the annual Kansas City Fed policy symposium today that “there does not seem to be an elevated risk of overheating” and that he sees little sign of inflation surging past the central bank’s current 2 percent target. The speech was seen as dovish by many and could indicate that interest rate hikes are less likely to happen.

- ANZ strategists Daniel Hynes and Soni Kumari wrote in a report that they “see gold prices stabilizing at current levels, with the probability of a short-covering rally increasing substantially.” Gold prices could be back on their way up and so could silver due to a heightened gold/silver ratio. The gold price is currently 81 times higher than silver right now, which is a level that’s only been reached on four occasions since the mid-1990’s, reports Bloomberg. When the gold/silver ratio previously exceeded 80, silver rallied three of the four times.

- A new platinum-gold alloy created by U.S. scientists is now the world’s most wear-resistant metal. This new alloy is so wear-resistant that if you made tires out of it, they would have to skid around the Earth’s equator 500 times before wearing out the tread, writes India Today. The new alloy is 100 times more durable than high-strength steel and could have many new potential uses.

Threats

- According to JPMorgan Chase & Co.’s August survey of credit fund managers, the percent of those with bullish outlooks is just 20 percent, down from 63 percent in July, writes Bloomberg. Another signal of credit downturn is that credit card issuers have lowered the limits for subprime consumers by 10 percent as their losses mount. This amounts to a 3 percent decrease in the average borrowing cap on new credit card accounts to $5,649. TransUnion found that the share of credit card loans that are at least 90 days past due rose to 1.53 percent in the second quarter, which is still below the 2.71 percent delinquency rate for the same time 10 years ago. The Citi economic data index showed this week that the average correlation between the U.S. and other economies hit an all-time low and the sharp decline is not sustainable. This could suggest that either global data will improve or that the U.S. economy will slow down.

- New developments this week in Special Counsel Robert Mueller’s probe involving Russian interference in the 2016 election could have negative impacts on the market. Allen Weisselberg, first an accountant for President Donald Trump’s father and then chief financial officer of the Trump Organization, has received immunity from federal prosecutors in their case against President Trump’s former lawyer Michael Cohen. Cohen pleaded guilty to several charges this week and told prosecutors that President Trump directed him to pay women for their silence regarding alleged affairs ahead of the 2016 election. Frank Agostino, an attorney who formerly prosecuted U.S. tax cases, told Bloomberg that “because there are tax implications to all these transactions, it even opens up Trump’s tax returns to state and federal prosecutors.”

- South African gold producers remain deadlocked with labor unions over wage demands. Sibanye Gold, the top producer in the country, said that if wage demands went into effect, the sector would be forced to close more mine shafts since they cannot afford the union’s proposed wage increases, as they struggle to control overall operating costs.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended August 24 was Happycoin, which gained 299.48 percent.

- As part of reforms to enhance the integrity of voting in Kenya, the country’s electoral agency intends to use blockchain technology to help offer real-time results, reports Bloomberg. East Africa’s biggest economy is turning to blockchain to boost transparency and reduce perceptions of opacity, in an area that has been marred by rigging claims and violence, the article continues.

- CoinDesk reports that LumenLab, an affiliate to insurance giant MetLife Asia, has successfully trialed an insurance product powered by blockchain that offers financial protection to pregnant women with a risk of gestational diabetes. The product is called “Vitana” and connects customers’ digital medical records to their mobile phones so that they can be issued a policy in a few minutes and make automatic payouts without requiring customers to file a claim for benefits. Zia Zaman, CEO of LumenLab and chief innovation officer in Asia of MetLife, said in a new release on Monday that the company “saw an opportunity to test how blockchain can make insurance more seamless and we’ve partnered with some of the best companies in their fields to create a blueprint to launch new parametric insurance products in the future.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended August 24 was DigiFinexToken, which lost 42.74 percent.

- Roger Ver, the digital currency advocate often referred to as “Bitcoin Jesus,” is having a hard time convincing investors to convert to the “supposed second coming of the world’s biggest cryptocurrency,” – Bitcoin Cash, reports Bloomberg. New blockchain analytics from Chainalysis show that Bitcoin Cash is barely being used in commerce. Not only that, a review of payments received by some of the largest crypto merchant processing services show that Bitcoin Cash payments fell to $3.7 million in May from $10.5 million in March, the article continues.

- The Securities Exchange Commission (SEC) has dismissed more bitcoin exchange-traded funds, writes Seeking Alpha. It rejected applications for nine separate bitcoin-based funds, which would have been listed on the CBOE or NYSE Arca. The reason behind the rejection remains the same, the article continues, that there are not enough protections against fraud and market manipulations.

Opportunities

- A handful of cryptocurrency exchanges have signed on to what looks to be the industry’s first self-regulatory organization, writes Seeking Alpha. The organization, called the Virtual Commodity Association, is a “step toward transparency in the opaque and volatile market.” In September, representatives from various exchanges will meet to set goals for the group, founded by the Winklevoss twins.

- The National Science Foundation (NSF), a U.S. government organization, granted $800,000 to researchers working on a distributed ledger platform being developed at the University of California – San Diego, reports Coindesk.com. The proposed blockchain-centric platform called Open Science Chain (OSC) would help researchers efficiently access and verify data collected through scientific experiments, according to the NSF website.

- The GTI VERA Convergence Divergence Indicator, which detects trend reversals, looks poised to benefit bitcoin bulls, reports Bloomberg. The last time this signal pointed to a reversal, bitcoin surged 39 percent the following month, the article continues, which may enable many cryptocurrency believers to breathe a sigh of relief. Germany is aiming to withdraw from the U.S.-led financial system, reports CCN.com, which could give the price of bitcoin a boost. Europe’s biggest economy has witnessed both Iran and Turkey get hit hard by U.S. sanctions throughout the past several months, leading to Heiko Maas, German foreign minister, to react with the latest announcement. According to one German-Finnish entrepreneur, the withdrawal of European economies from the global banking system is optimistic for bitcoin and crypto, as “it will lead to the devaluation of the U.S. dollar and other reserve currencies.”

Threats

- Regulators in China are looking to block over 100 cryptocurrency exchanges overseas that offer trading services to domestic investors, reports CoinDesk.com. The China National Fintech Risk Rectification Office has identified 124 trading platforms with overseas IP addresses, but that are still available in the country, the article continues. According to a report by the Shanghai Securities Times, the office now plans to ramp up efforts to monitor the space and to block Internet access to these platforms.

- Kryptovault, a Norway-based crypto miner which operates several farms in the region, might have to shut down one of its locations temporarily due to noise complaints and failure to have the correct permits. CoinDesk reports that local officials said the facility was operating illegally and that many complaints have been coming in about noise levels from local residents over the last few months. The facility runs 9,500 computers and the fans used to cool the facility are what creates the noise pollution. The Kryptovault CEO has said that the firm will look into investing in noise reduction equipment and has applied for the missing permits.

- The U.S. Federal Trade Commission (FTC) is again warning consumers about bitcoin scams. CoinDesk writes that the scammers are sending threatening letters, mostly to men, about exposing an alleged secret and that they must pay a confidentiality fee through bitcoin to remain silent. This is not the first time the FTC has provided guidance and education to consumers about potential crypto scams. The agency’s education division hosted

Energy and Natural Resources Market

Strengths

- Zinc was the best performing major commodity this week rising 6.7 percent. The commodity posted its best week in more than six months as the Chinese spot market tightens and stockpiles fall.

- The best performing sector this week was the S&P 1500 Oil & Gas Refining and Marketing Index. The index rose 7.1 percent after Credit Suisse boosted its outlook on the sector, suggesting a widening of Brent-WTI spreads in the third quarter will lead to expanded profitability for the entire sector.

- The best performing stock for the week was CNOOC Ltd. The Chinese crude producer rose 11.0 percent after it earned analysts praise for its cost controls and solid first half of the year earnings.

Weaknesses

- Lumber was the worst performing commodity this week. The commodity dropped 5.8 percent after U.S. purchases of new homes unexpectedly dipped to the weakest pace in nine months. Higher prices and mortgage rates continue to sideline demand, adding to signs of a cooling in the housing market.

- The worst performing sector this week was the Bloomberg Auto Parts & Equipment Index. The index dropped 2.6 percent after Continental AG slashed its guidance for the second time this year, citing disappointing sales in China and Europe, as well as continued uncertainty around NAFTA negotiations.

- The worst performing stock for the week was Fortescue Metals Group Ltd. The Australian iron ore producer dropped 4.7 percent to a 52-week low after the company posted a 58 percent decline in net profit in the 2017/2018 financial year as a result of lower realized iron ore prices.

Opportunities

- Everything adds up to a sizeable gold rally, according to Bloomberg. After five months of losses, everything is falling into place for gold to get a reprieve. After touching a 19-month low, gold bears reached peak excitement by taking short positions to multi-year highs. Now, Bloomberg argues, a positive shift in the yuan is all that’s needed for a catalyst to send gold and gold equities rallying.

- Trade war-related headlines had led to a slide in base metals prices, but evidence of spot demand suggest sizeable destocking is taking place. Base metal stocks at Shanghai Futures Exchange warehouses all declined on Friday August 24, with zinc stocks dropping to 11-year lows. Deliverable zinc stocks shed 4,130 tonnes, or 11.8 percent, over the week to reach 30,800 tonnes. Copper stocks fell 8,486 tonnes, or 5.5 percent, over the past week to 146,590 tonnes.

- The outperformance in U.S. stocks relative to the rest of the world won’t continue, JPMorgan said. Emerging markets and value assets will rally and the dollar’s strength will abate. Such a set up would be greatly beneficial for natural resources equities and commodities.

Threats

- Durable goods orders dropped the most in six months as U.S. economic data continues to slow down. After a modest June rebound, durable goods orders show a greater than expected contraction, dropping 1.7 percent against expectations for a 1.0 percent drop.

- U.S.-China trade talks made no progress in Washington D.C. this week, setting the stage for further escalation of the trade war. In addition, Mexico and the U.S. also failed to work out their NAFTA issues, with Mexico requesting Canada to back the negotiations before any deal can be agreed.

- There is a 70 percent chance of a global recession within five years, Pimco’s CIO of non-traditional strategies said. Marc Seidner advised investors to find shelter as loose monetary policy ends.

China Region

Strengths

- In a green week across the region, the Philippines, Shanghai, Hong Kong’s Hang Seng Composite and South Korea all returned more than 2 percent for the week.

- Taiwan’s export orders rose 8.0 percent for the July period, well above expectations for a 2.9 percent reading and up from last month’s drop of 0.1 percent.

- Thailand’s second quarter, year-over-year GDP reading came in better than expected at a 4.6 percent growth rate, beating analysts’ anticipated 4.4 percent print. Quarter-over-quarter growth beat expectations as well for the second quarter, coming in at a 1.0 percent rate, better than expectations of a 0.9 percent print.

Weaknesses

- In a rising market this week, utilities was the worst-performing sector in the Hang Seng Composite Index, falling 82 basis points.

- Industrial production in Singapore did clock in in line, but at a year-over-year growth rate of 6.0 percent, the July measurement came in lower than June’s 8.0 percent revised reading and dropped 1.7 percent month-over-month, below expectations for only a 1.0 percent decline.

- Landing International Development Ltd. (582 HK) shares in Hong Kong dropped more than 42 percent this week in “their biggest weekly plunge ever after the casino operator said Chairman Yang Zhihui was unreachable,” Bloomberg News reported. Caixin had reported earlier that Yang is a target of investigation into ties to possible corruption. The unreachability of Yang this week comes about two weeks after the company’s $1.5 billion Philippine project was thrown into doubt.

Opportunities

- Three Chinese provinces now possess gross domestic product readings of greater than $1 trillion, matching the number of U.S. states that have reached that milestone. Look out, California, Texas and New York because the GDPs of Guangdong, Jiangsu and Shandong provinces are right behind you! Next week, we’ll feature a similar chart that demonstrates a remarkably different ordering of GDP sizes—but this one will be based on purchasing power of parity, and, you will notice, with a consequentially different ordering ... so stay tuned for next week’s chart!

- “China Keeps Promises to Wall Street Even as Trade War Drags On,” one Bloomberg headline read late this week in a succinct summary of the Chinese follow-through on a commitment to continue to open up its financial system and remove limits on foreign ownership of its banks and bad-debt managers.

- Geely Automobile Holdings Ltd (175 HK) reported a 54 percent jump in net income for the first half of 2018, and is now the third-largest carmaker in China, surpassing its top three Japanese rivals even as the company moves to begin selling its new Lynk & Co. line of vehicles in Europe soon.

Threats

- Trade wars real, perceived and/or both remain a concern for both global and China-region investors. The low-level, low-expectations U.S.-China trade talks this week did not result in any notable progress. Tariffs and counter-tariffs proceed at present.

- Currency issues and inflation remain relevant as investors continue to watch EM FX carefully and in particular with regard to the status of the U.S. dollar, the PBOC’s handling of the renminbi and local EM inflationary concerns. This week, though in thin trading, the Indonesian rupiah rose (fell) to new 52-week highs (lows), as an example.

- It came out Friday that U.S. President Donald Trump has requested that Secretary of State Mike Pompeo refrain from traveling to North Korea in the absence of “sufficient progress” toward denuclearization. President Trump also noted that Mr. Pompeo may head to North Korea after the U.S.-China trade issues resolve. Mr. Trump opined that China has not been of particular help of late with respect to North Korea, presumably “because of our much tougher Trading stance,” the president wrote on Twitter.

Emerging Europe

Strengths

- Poland was the best performing country this week, gaining 3.04 percent. Equites trading on the Warsaw exchange moved higher on the news that STOXX upgraded Poland to Developed Market from Emerging Market status.

- The Polish zloty was the best performing currency this week, gaining 2.11 percent against the U.S. dollar. Poland expects public debt to shrink to 48.9 percent of gross domestic product (GDP) in 2019 from 49.2 percent in 2018. The rate of unemployment is projected to drop further to 5.6 percent from 6.2 percent this year.

- Information technology was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 67 basis points. OTP Bank declined the most among stocks trading on the Budapest exchange, losing 1.4 percent. The country’s competition authority lowered the fine on Hungarian banks, related to alleged collusion during the 2011-2012 conversion of foreign exchange (FX) loans, to a total 5 billion forint from the initial 9.5 billion forint. OTP Bank’s penalty was cut from 3.92 billion forint to 1.44 billion forint.

- The Russian ruble was the worst performing currency this week, losing 51 basis points against the U.S. dollar. Prospects on new sanctions from the U.S. put pressure on the currency. Russia’s central bank suspended its FX purchases through the end of September.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

- According to Bloomberg’s article by Srinivasan Sivabalan, emerging market stock valuations may be flashing a rebound signal. For the past five years, the price- to-earnings ratio of the MSCI Emerging Markets Index has fluctuated between 75 percent of that of the S&P 500 (in good times) to 66 percent (in bad times). With the EM Index trading last Friday at the lower end of the range, a bounce back may be in the works.

- On Tuesday, after an eight-year bailout period, the Greek Prime Minister Alexis Tsipras declared the end of the bailout program. Greece turned a 15.1 percent budget deficit in 2008 into a 0.8 percent surplus last year. However, the country still owes billions to creditors who will continue to regularly review progress on the planned reforms.

- A while ago FTSE upgraded Poland to developed markets and this week STOXX followed in its footsteps. For the time being, the list of Polish companies that will be added to the STOXX Europe 600 Index is unknown. The exact list of companies will be published on September 3. The effect will be positive for ETFs and actively managed funds buying equities included in the index.

Threats

- Preliminary eurozone Manufacturing PMI for August was reported at 54.6 versus the prior reading of 55.1. The reading remained well above the 50 level that separates growth from contraction; however, a lower reading indicates slowdown in manufacturing activity. We also noticed that the one-month reading is below the three-moth moving average, which could suggest a downtrend.

- The United States has placed new sanctions on two Russian shipping companies for violating sanctions against North Korea, as well as two individuals over cyber-related activities. Additional sanctions were announced on Friday in relation to the poisoning of former spy Sergei Skripal. The latest measures appear far less stringent than those considered by Congress.

- Eurozone consumer confidence weakened sharply in August to its lowest level in more than a year, preliminary data from the European Commission showed Thursday. The flash consumer confidence indicator dropped to -1.9 from -0.5 in July, which was revised from -0.6. Economists had forecast a score of -0.7.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All