At PIMCO, we think it’s only a matter of time before global fixed income investors own more Chinese assets, particularly given the prospect of benchmark inclusion into several major global indexes and greater accessibility for the onshore Chinese bond market. In the following interview, Kimberley Stafford, Tomoya Masanao, Robert Mead and Stephen Chang discuss why we see Chinese bonds as an increasingly important element in global investment portfolios and how we are assisting our clients globally to access this opportunity.

Q: Why are investors showing increasing interest in China’s onshore bond markets?

Kimberley Stafford: Valued at roughly $12 trillion (U.S.), China’s bond market is the world’s third-largest after the U.S. and Japan, representing over 10% of the global bond market. While offshore Chinese markets and onshore equity markets have long been accessible to global investors, lack of access has limited foreign investor ownership of the onshore bond market to a relatively low 3%-4%. But this is changing.

The onshore China bond markets, particularly the China interbank bond market (CIBM), are becoming increasingly accessible to global investors. We believe that the inclusion of onshore China bonds into emerging market (EM) and global bond indexes will increase strategic allocations.

Last year, Bloomberg Barclays and Citigroup added China into a few bespoke indexes and new subindexes, acknowledging the progress that China has made toward making its bond market more accessible. However, most investors have been focusing on inclusion into three flagship indexes: JPMorgan Government Bond Index-Emerging Markets (GBI-EM) Global Diversified; Citi World Government Bond Index (WGBI); and Bloomberg Barclays Global Aggregate Index. We expect the inclusion of China in these major indexes over the next one to four years, driving around $250-$300 billion in passive flows alone into the onshore markets.

China has long been an important element in PIMCO’s global macro analysis and long-term opportunity set. As momentum has grown around index inclusion, we have been carefully assessing the risks and implications as we look to facilitate a broader range of our EM and global client portfolios to access this opportunity set.

Q: What avenues are available to global investors seeking access to China’s markets?

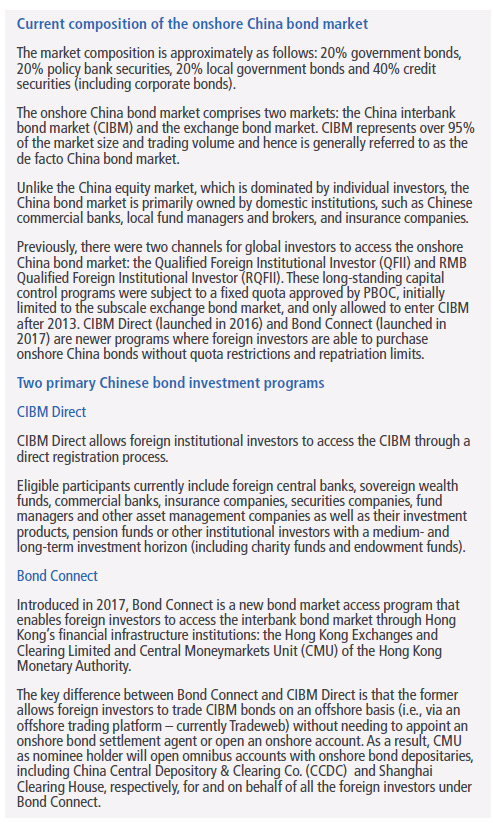

Stafford: CIBM Direct (launched in 2016) and Bond Connect (launched in 2017) are relatively new programs where foreign investors can purchase onshore China bonds without quota restrictions and repatriation limits. We continue to assess their relative efficiencies and risks (see table below), and anticipate that further refinements will be made by Bond Connect.

As one of the earliest entrants among global asset managers, PIMCO has been investing in the onshore China bond market via the Qualified Foreign Institutional Investor (QFII) program since 2014 and CIBM Direct since 2017. From our experience, setting up a local account and appointing an onshore bond settlement agent can be an onerous process for many global investors. As a result, PIMCO is proactively working with clients and custodians to prepare as early as possible, before index inclusion.

Q: What is PIMCO’s assessment of the macroeconomic climate in China?

Robert Mead: Having the most powerful leadership in decades creates the potential for many positive developments in China. Overall, strong leadership could further reinvigorate structural reforms in a decisive, top-down fashion. Coherent macro policies are already strengthening control of the financial system and helping to revitalize state-owned enterprises. The rapid rebalancing toward a consumer- and services-oriented economy over the past five years could accelerate further. Despite opposition from the U.S., concentrated investment in research and development (R&D) and mass deployment of technology in the industrial, services and household sectors could also raise productivity. In this optimistic scenario, a strong revival in productivity and animal spirits could support real GDP growth of 6.5%−7.0%.

As the surprising events surrounding North Korea this year illustrate, a grand strategic bargain between China and the U.S. is possible on trade and geopolitics. With its long-term orientation, China’s leadership can make tactical accommodations, while the transaction-oriented Trump administration is focused on short-term election cycles.

In this bullish scenario, surging foreign portfolio investment and an increase in central bank allocations could strengthen the yuan and boost its role as a reserve currency.

Q: What key risks should investors be aware of?

Mead: The bullish scenario notwithstanding, China faces several risks over the next few years.

The first is elevated debt levels. President Xi promoted “controlling debt risks” to the number-one priority this year. Since the global financial crisis in 2008, China’s non-financial debt has jumped 120 percentage points to 250% of GDP. Corporate debt increased to 130% of GDP, while various direct and contingent local government liabilities amounted to more than 50% of GDP. Shadow-banking excesses further compound China’s systemic vulnerability. We are encouraged by the appointment of credible technocrats such as Vice Premier Liu He and the new People’s Bank of China (PBOC) Governor Yi Gang. However, the moral hazard of assuming no defaults in opaque and legally ambiguous local government financing vehicle (LGFV) bonds and the likely rise of corporate defaults into the next cyclical slowdown raise concerns.

Another risk is the potential for a downturn in property. Household debt at 53% of GDP in 2017 is not high in absolute terms, but its rise in combination with property reflation raises some red flags. In the past 10 years, household debt has jumped 700% from US$830 billion to $6.3 trillion as property prices increased by 300% in major cities. Measured against urban disposable income, household debt rose to 1.4x from 0.6x. If this pace is sustained over the secular horizon, property reflation and household debt may reach alarming levels. We note, though, that current housing inventory is low and tight government policy has plenty of room for relaxation.

The third risk we identify is the intensifying China-U.S. rivalry. The potential for a major trade conflict between China and the U.S. has been a rude awakening for the market in 2018. China and the U.S. represent competing economic models, conflicting geopolitical interests, and contrasting ideologies and political systems. The deepening of China-U.S. interdependence seen over the past 20 years may no longer be viable, but a stable strategic equilibrium has not yet emerged, and the risk of a strategic miscalculation is significant considering the volatile policies of the Trump administration.

Q: How does PIMCO view valuations in the onshore Chinese bond market compared to developed markets?

Tomoya Masanao: The neutral policy rate – the rate needed to ensure trend growth and at-target inflation – is often used as a valuation anchor for global bonds. In 2014, PIMCO developed the concept of The New Neutral as a secular framework for interest rates. It foresees that post-crisis neutral policy rates will be much lower than their historical levels. In the case of the U.S., we estimated 0%-1% for real neutral rates, equivalent to 2%-3% nominal bond rates.

We continue to expect that low equilibrium policy rates will anchor global fixed income markets. Our forecast is for fairly range-bound global fixed income markets and what we see as generally balanced upside and downside risks to the forward yield curves.

This New Neutral framework can be relevant for China as a starting point for fundamental analysis. However, when we look at China’s bond markets, neutral rates may not be as applicable as they are to the U.S. and other developed markets. In general, neutral rates can be a powerful valuation anchor for bonds where a central bank is operating as an independent agent in a conventional policy regime with a policy rate as a key control variable. This may not be the case in China, given the PBOC’s institutional set-up and policy regime, an economic model based on financial repression and the secular unwinding of that model.

Investors, therefore, need to establish an alternative valuation framework for the Chinese markets, one which should be a hybrid approach with quantitative and qualitative assessment of China’s policy set.

Q: Where do the best opportunities for our investors lie?

Stephen Chang: As coherent reforms progress under new policymakers in China, one of the most interesting developments for global investors is the accelerated financial integration of the onshore yuan-denominated bond market.

Issuance in both the onshore yuan and offshore dollar credit markets has been brisk. The investment universe has continued to expand, with new sectors, debut issuers and instruments across the capital structure. We expect debt issuance by Chinese entities both onshore and abroad to remain robust over the next few years.

We remain constructive on China’s consumer, technology, and services sectors in the new economy and plan to spend more time on the ground in China looking for credit investment opportunities over the next several years.

However, we expect credit performance to diverge markedly among sectors due to varying industry dynamics and the policy mix. Liquidity may ebb and flow as China aims to deleverage the financial system while maintaining broad stability. Corporate fundamentals will likely degrade, defaults will likely increase, and implicit guarantees for local government financing vehicles and state-owned enterprises are likely to fade gradually. For these reasons, careful security selection is vital.

As a result, we believe it is essential to pair China macro analysis with rigorous bottom-up credit research. We continue to grow our Asia-Pacific investment team and are committed to investing further resources into this growing market with the aim of extracting more value for our clients around the world.