Global Economic Outlook - September 2018

Summary

- Cautious Optimism

After months of escalating trade tensions, there have been some constructive developments on the trade front. These include preliminary European Union (EU)-U.S. and U.S.-Mexico trade agreements. Despite these positive signals, trade frictions are far from over.

The U.S. and China, in a tit-for-tat move, imposed further 25% tariffs on $16 billion of bilateral imports amidst trade talks, bringing the current total to $50 billion. Though talks resumed between the two nations, another round of tariffs may be announced this month.

Turkey and Argentina are facing a challenging interval ahead, highlighting vulnerabilities in emerging markets (EMs). Escalating trade tensions and tightening global liquidity conditions may continue to pressure some EMs, but we do not expect them to accumulate in sufficient scale to trouble developed markets (DMs).

Overall, we are cautiously optimistic on global growth, but risks remain tilted to the downside. The following is an overview of what we are expecting in key markets.

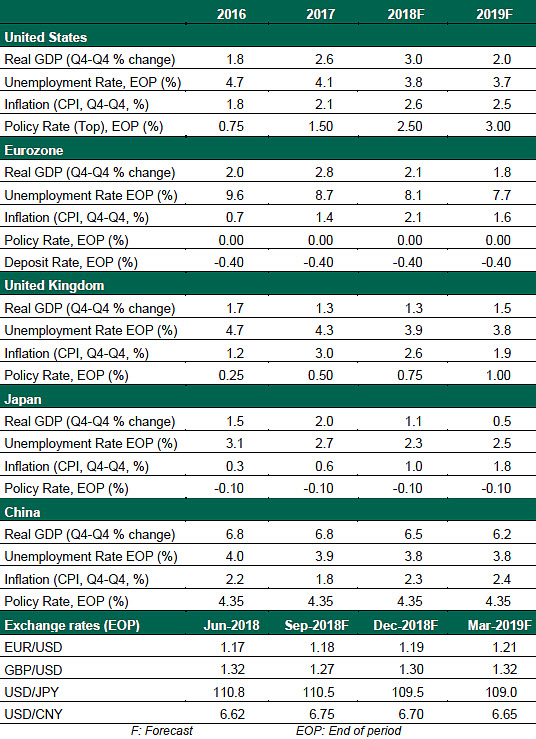

United States

- The revised estimate for real U.S. gross domestic product (GDP) growth in the second quarter was 4.2%, slightly above the already-strong initial estimate. We expect the economy to continue performing well, recording full-year growth of 3.0% this year.

- In 2019, the costs of trade actions will become more apparent and fiscal tailwinds will fade, leading to slower GDP growth and sustained inflation.

- Federal Reserve officials have a lot to consider as they contemplate further rate increases. The flattening yield curve is a growing concern, as is international debt sustainability. We expect a rate increase in each of the September and December 2018 meetings of the Federal Open Market Committee, and two additional increases in 2019 before rates reach a steady level.