Really Ready for Retirement?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSUMMARY

- Really Ready for Retirement?

- The Next NAFTA

In the span of human history, retirement is a fairly new idea. Only a few generations ago, most of our ancestors could expect to work until the end of their lives. We are happy to report this is no longer the case. Improving longevity brings the opportunity for retirement, but also the responsibility for preparing. Unfortunately, many Americans have not handled this responsibility very well at all.

As recently as 1980, 46% of all private-sector workers were covered by a defined-benefit retirement plan (such as a pension). Today, that figure is 15%. As pension programs disappeared, many workers failed to compensate with their own savings. Younger workers know they are responsible for funding their own retirements—but all too often, they are not saving enough.

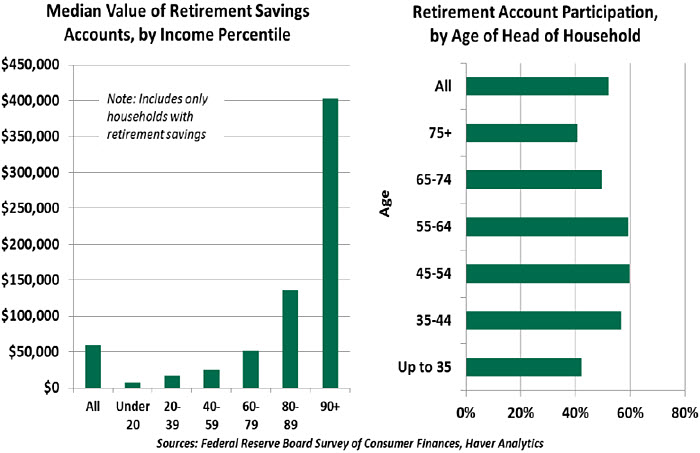

The U.S. Social Security Administration estimates that 36% of workers have not saved any money for retirement. For the bottom half of those who have saved, the median value of retirement savings is approximately $14,000. Retirement planners suggest that a worker earning the median annual income of $45,000 would need $31,500 per year in retirement, more than the entire value typically saved. Social Security will help, but not as much as many retirees may hope.

Segmenting consumers by age cohort reveals further concerns. While older workers have less time to save and should therefore have the most savings, their actual savings still leave much to be desired. And many workers currently in retirement live with the risks that they will outlive their savings or that increased medical costs will deplete their savings faster than planned. Medicare is vital, but it does not cover the full cost of insurance.

Younger workers face more obstacles to saving. They are likely earning smaller amounts and have less disposable income to set aside for the future. Student loans have left them carrying more debt as they start their careers, leading to the consumption of income that might otherwise be saved. Others may not yet have taken a job with an employer-sponsored retirement fund.

For the young and the old, the statistics reveal a bifurcation between those who are on track to save enough to retire, and those who are not. The resulting inequality is a broad concern, one that will persist past our working years.

Some of the saving shortfall is a lingering effect of the Great Recession. As the unemployment rate climbed to 10% and durations of unemployment stretched longer, workers stopped making retirement contributions. Many of the unemployed dipped into their retirement savings or relied on credit to maintain their lifestyles. Upon regaining a source of income, paying down accumulated debt has hampered saving, and rebuilding their retirement accounts has been a lower priority.

The inadequacy of private saving will put increased pressure on Social Security. Social Security provides a monthly payout proportional to worker’s contributions. But for median earners, the payments are not at all generous. Today, a worker retiring at age 65 with a salary of $45,000 would expect to receive about $1,250 monthly. This annual income

of $15,000 is below the poverty guideline for a household of two people.

Social Security payouts were originally intended to be a lifeline for the small portion of older workers with no other savings. But reliance on the program has become widespread. The Social Security Administration estimates that 21% of elderly married couples and 44% of unmarried elderly persons rely on Social Security for 90% or more of their income. This level of dependence will make any meaningful reform to payouts a painful prospect.

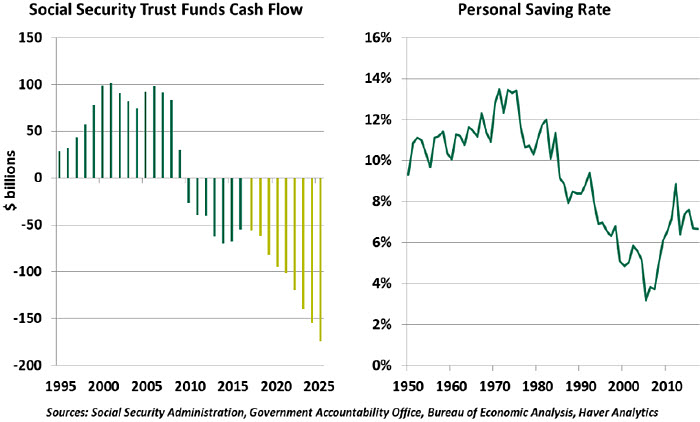

The sustainability of the Social Security system has been questioned. The program began consuming its reserves to pay benefits in 2010. At current funding levels, the system will be unable to pay full benefits to retirees starting in the year 2035. But it’s too pessimistic to write off Social Security as defunct by the time today’s young workers retire. Minor changes to eligibility and tax rates can restore the system to solvency. At worst, the trust fund will be depleted, and payments funded by the current contributions of workers would continue, but at reduced levels. Any income in old age is better than none, but relying solely on Social Security is a fate all younger workers should strive to avoid.

The burden on all workers will grow as the population ages. Social Security, Medicare and housing subsidies for the elderly will increase future government liabilities. Today’s adults increasingly find themselves helping to care for their aging parents by combining households or funding their parents’ stays in nursing homes. Broader economic costs will accrue as both retirees and their burdened children find themselves with less disposable income. In a consumer-led economy like the U.S., a reduction in consumption is an acute pain. And a class of voters who find themselves left in poverty may choose to take unpredictable political actions.

The warnings of tomorrow’s ills are clear, and the solution is obvious: Save more today. Roughly two-thirds of U.S. workers have access to a saving program through their employer. However, of those who have access a plan, only 41% actually contribute to it.

To encouraging saving, retirement plan administrators are turning to behavioral economics. First, workers must overcome their present bias. Retirement sounds distant, and workers see more pressing needs for their money now. Workers who do not save forfeit not just payroll contributions, but also years of employer matches, market gains and dividend reinvestment in retirement accounts. It’s never too early to start saving; yet while an early start is preferred, it is also never too late to begin a saving program.

Once convinced of the need to save, workers must find room in their budgets. They may hesitate to reallocate funds to make a retirement contribution. To address this, retirement plans now offer “save more tomorrow” systems, a pledge to put a portion of future pay raises into savings. The worker feels no pain from losing current income, and the future contributions will not feel like a loss.

Workers may also be intimidated by the myriad choices involved in retirement. The menu of mutual funds will scare workers with no financial education. Faced with overwhelming choices, it’s easiest to make no decision at all. However, workers can be steered toward a preferable outcome through the plan’s default option. Workers who do not make a

retirement selection can be placed in a plan that makes small contributions into a safe fund.

The worker is free to opt out or make other elections. But in such an approach, more workers

save more money, a better outcome for most.

The recent comprehensive update of the Bureau of Economic Analysis’ National Income and Product Accounts contained a morsel of encouraging news. The BEA’s definition of saving was revised to better account for income to small business owners. This provided a boost to the national saving rate, but only in aggregate. The upside was limited to business owners, a minority of Americans. This did nothing to ameliorate the low levels of savings outlined above.

We see one more reason for optimism. Just as the concept of retirement was foreign to our predecessors, we see an evolving understanding of what retirement means today. More people are working in their older years: some by necessity, but many by choice. As services represent an increasing share of economic output, workers who stay mentally sharp can continue working longer, at jobs they enjoy and on terms of their choosing. Others may choose to “semi-retire:” work seasonally, work on a project basis or support their children by taking care of their grandchildren.

Older homeowners have an additional resource: The equity in their homes. Reverse mortgages, in which a financier buys a home by paying installments to an owner-occupant, have a reputation for offering unfavorable terms. However, with proper oversight, they can be a helpful resource to let homeowners remain in place, maintain their lifestyles, and handle unplanned expenses.

An entire industry is devoted to retirement planning, and we do not deign to offer guidance in this space. Retirement savings should be aligned with each individual’s time horizon, risk appetite and other factors. What matters more than anything is that we all plan for retirement, set goals and save. Save more today, and save more tomorrow. But please, save something.

Neighborly Negotiations

After months of gridlock, a breakthrough was finally made in the North American Free Trade Agreement (NAFTA) process last week. The U.S. and Mexico reached a bilateral agreement to revise key terms of their trade with one another.

Under the accord, Mexico will continue to sell manufactured goods to the U.S., but there will be new provisions for the auto sector, which is a critical component of continental trade. The new “rules of origin” for auto components require 75% of a vehicle’s content (compared to the current 62.5% and the initial U.S. demand of 85%) to be of North American vintage. A new labor rule has been proposed, which would require that 40% to 45% of auto content be produced by workers earning at least $16/hour.

The Mexican government estimates that around 32% of its current auto exports would not comply with the revised rules. These vehicles (models like Honda HR-V, the Volkswagen Jetta and Golf) and parts would be subject to a 2.5% Most Favored Nation tariff, the maximum the U.S. can collect in accordance with its World Trade Organization commitments.

Carmakers will need to raise prices or reduce their margins on these vehicles to absorb the tariff. Longer term, they’ll be faced with the question of whether to take on the expense of reworking their supply chains. If the tariffs increase the cost of North American manufacturing, producers may find it more efficient to source even less

content from North America.

The agreement between the U.S. and Mexico includes a softer version of the “sunset clause” for the trade agreement (allowing ten years to wind down before expiration), the removal of dispute settlement panels and the preservation of steel and aluminum tariffs. The new NAFTA deal would also maintain zero tariffs on agricultural products, preserve an open energy sector and thwart currency manipulation.

Bearing in mind the benefits NAFTA has delivered to the Mexican economy, a renewed deal is better for Mexico than no deal. It won’t materially move the dial for either country as concessions have been made from both sides (significant by Mexico and more minor by the U.S.).

Following this bilateral agreement, Canada was pressured to join the party. Talks have thus far been inconclusive. The White House tried to enforce a short deadline to submit the deal to Congress, but September 30 is a more realistic target.

Though the odds of a trilateral agreement have increased, both nations are still far apart on some of contentious issues, which are politically sensitive for Canada:

- NAFTA's dispute settlement chapter must be consistent and comfortable for all three partners. The U.S. wants the Chapter 19 system (for complaints about illegal subsidies and dumping) to be removed and the investor-state dispute settlement system to be made voluntary. Canada is fighting for stronger enforcement mechanisms.

- Canada’s dairy market uses quotas supported by tariffs. The U.S. wants Canada to remove entry barriers to its agriculture sector.

- Canada seeks to protect its cultural industries.

Other issues include intellectual property, duty-free treatment of small amounts of goods purchased in the U.S. and the fate of U.S. tariffs on Canadian steel and aluminum.

It is in best interest of all three nations to work out a deal. Canada is among the most important U.S. trade partners and has key allies in the U.S. It is also the second largest source of foreign direct investment ($523.8 billion, equivalent to 13% of the total) to the U.S. The Bureau of Labor Statistics estimates around 9 million U.S. jobs are dependent on Canadian trade. And Canada is the top export market for 35 U.S. states, many of which are

politically important with midterm elections approaching.

Even with a deal in place, NAFTA ratification will be a complex process (see here for details on adoption and implementation in the U.S.). Though President Trump sees “no political reason to keep Canada in the new NAFTA deal,” it is worth mentioning that the NAFTA cannot be abandoned unilaterally. Yet risk of a termination cannot be ruled out entirely as even the Canadian Prime Minister Justin Trudeau believes that “no NAFTA is better than a bad NAFTA deal.”

A deal other than a trilateral agreement, like a U.S-Mexico bilateral deal as suggested by President Trump, is unlikely to win the Congressional approval, as the Trade Promotion Authority was granted only for a trilateral deal.

Tensions will remain high, and negotiators will play hardball. But we remain encouraged that negotiations are underway, and are optimistic that acceptable terms can be reached.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2018 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All