Boston - As short-term rates move higher and the Treasury yield curve flattens, many investors are thinking about how to earn income while also protecting themselves against rising rates.

In this post, we'll discuss why municipal floating-rate notes -- an often-overlooked part of the market -- may be an attractive option for these investors.

Fed hikes in focus

Rising expectations of Federal Reserve rate hikes following the strong August employment report have put even more focus on the front end of the curve recently.

For example, markets have been expecting a hike at the upcoming Sept. 26 Fed meeting and according to the latest reading from the CME's FedWatch Tool, the market is now pricing in about an 80% chance of another rate hike, at the December Fed meeting.1

And with the Treasury curve flattening, some investors are favoring bonds at the front end of the curve that have seen their yields rise recently, but still have less rate risk than long-duration bonds.

What are muni floating-rate notes?

In municipal bonds, the front end of the curve has been particularly popular with investors seeking tax-free income. However, this popularity has caused short-duration muni bonds to become rich relative to Treasury bonds of similar duration.

One alternative that investors may not be aware of are municipal floating-rate notes, which can offer attractive income and a way to potentially hedge against short-term interest-rate risk. In addition, as short term rates continue to rise, investors may potentially realize additional tax-advantaged income. Short-term rates have been rising but are still relatively low by historical standards. While fixed-rate bonds could lose value if short rates continue to rise, floating-rate instruments may help protect against rising rates because their duration is effectively zero.

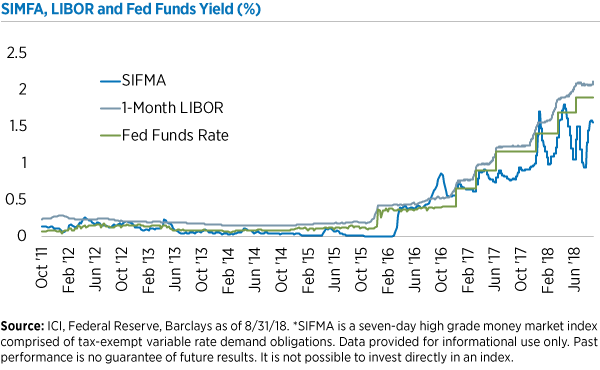

Like bank loans (also called leveraged loans), muni floating-rate notes have coupons that float, or reset, at periodic intervals. The coupons of muni floating-rate notes are tethered to short-term rates such as the weekly Securities Industry and Financial Markets Association (SIFMA) Municipal Swap Index2 or London Interbank Offered Rate (LIBOR). Both SIFMA and 1-month LIBOR have been moving higher lately (see the figure below), and could continue to rise if the Federal Reserve continues to hike its key short-term rate.

Rates may continue to rise

Muni floating-rate notes typically pay yields that are based on SIFMA or a percentage of LIBOR plus a credit spread. Each coupon floats, or resets, at periodic intervals based on the movement of SIFMA or LIBOR. In that way, they are similar to bank loans.

However, muni floating-rate notes are generally investment-grade securities, while leveraged loans are typically rated below investment grade. It's also important to remember that income from muni floating-rate notes is exempt from federal taxes; income from corporate bank loans or Treasury bonds is federally taxable.

If the Fed continues to hike rates as expected, floating-rate munis could see their yields rise too. In fact, their yields have already moved considerably higher from a few years ago when the Fed first started signaling a move away from the zero interest rates after the financial crisis. With the Fed apparently in the mid-to-late stage of its hiking cycle, we believe now is the time to look at floating-rate munis.

Bottom line: Muni floating-rate notes may be a way to earn attractive after-tax income with some protection from rising rates.

1The CME FedWatch Tool analyzes the probability of FOMC rate moves for upcoming meetings. Using 30-Day Fed Fund futures pricing data, which have long been relied upon to express the market's views on the likelihood of changes in U.S. monetary policy, the tool visualizes both current and historical probabilities of various FOMC rate change outcomes for a given meeting date. (Source: CME Group)

2The SIFMA Municipal Swap Index, produced by Municipal Market Data (MMD), is a seven-day high-grade market index comprised of tax-exempt variable rate demand obligations (VRDOs) from MMD's extensive database. It is not possible to invest directly in an index.

Eaton Vance does not provide legal or tax advice. The discussion herein is general in nature and is provided for informational purposes only.There is no guarantee as to its accuracy or completeness. Individuals should consult their own legal and tax counsel as to matters discussed.

An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Longer-term bonds typically are more sensitive to interest-rate changes than shorter-term bonds. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer's ability to make principal and interest payments. Investments rated below investment grade (typically referred to as "junk") are generally subject to greater price volatility and illiquidity than higher-rated investments. Derivative instruments can be used to take both long and short positions, be highly volatile, result in economic leverage (which can magnify losses), and involve risks in addition to the risks of the underlying instrument on which the derivative is based, such as counterparty, correlation and liquidity risk.

Before investing in any Eaton Vance fund or unit investment trust (UIT), prospective

investors should consider carefully the investment objective(s), risks, and charges and

expenses. For open-end mutual funds and UITs, the current prospectus contains this and

other information. To obtain a mutual fund prospectus or summary prospectus and the most

recent annual and semiannual shareholder reports, contact your financial advisor or

download a copy here. Read the prospectus carefully before you invest or send money. For

closed-end funds, you should contact your financial advisor. To obtain the most recent

annual and semi-annual shareholder report for a closed-end fund contact your financial

advisor or download a copy here. To obtain a UIT prospectus, contact your financial advisor

or download a copy here. Before purchasing any variable product, consider the objectives,

risks, charges, and expenses associated with the underlying investment option(s) and those

of the product itself. For a prospectus containing this and other information, contact your

investment or insurance professional. Read the prospectus carefully before investing.

Not FDIC Insured. No Bank Guarantee. May Lose Value.

Eaton Vance does not provide tax or legal advice. Prospective investors should consult with

a tax or legal advisor before making any investment decision.

The information on this Web page is for U.S. residents only and does not constitute an offer

to sell, or a solicitation of an offer to purchase, securities in any jurisdiction to any person to

whom it is not lawful to make such an offer.

©2018 Eaton Vance Distributors, Inc. | Member FINRA / SIPC | Two International Place,

Boston, MA 02110 | 800.836.2414 | eatonvance.com

© Eaton Vance

Read more commentaries by Eaton Vance