Is This Just the Calm Before the Storm?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsHurricane Florence made landfall in North Carolina today, bringing with it destruction and calamity, the cost of which could top $170 billion, according to analytics firm CoreLogic. If so, that would make it the costliest storm ever to hit the U.S. To date, 2005’s Hurricane Katrina holds the top spot, costing an estimated $160 billion, followed by last year’s Harvey ($125 billion) and Maria ($90 billion).

Not to minimize the impact Florence will have on millions of Americans’ lives, but storms, even of this size, have rarely triggered major equity selloffs. According to research firm CFRA, in the last 15 years, the S&P 500 Index declined an average 0.2 percent in the month after a hurricane, but was up an average 3.9 percent in the subsequent three months. Home improvement companies such as Home Depot and Lowe’s could be beneficiaries, while insurance companies might take a hit.

Markets are subdued right now, with the S&P 500 having gone more than 55 days without a 1 percent move in either direction. Trading volumes are also lower-than-average, suggesting Wall Street is in wait-and-see mode before making major adjustments.

Could this just be the calm before the storm?

Consumers and Small Business Owners Are Feeling Good

Appropriately enough, Florence comes to us on the 10-year anniversary of Lehman Brothers’ collapse— the spark that set off the financial crisis—reminding us it’s never the wrong time to prepare for such a catastrophe. (I’ll have more to say on Lehman later.) That includes now, even as a raft of positive economic data was released this week. The University of Michigan consumer sentiment index climbed to 100.8 in September, against expectations of only 96.6. This was its second-highest reading since 2004.

What’s more, the NFIB Small Business Optimism Index soared to 108.8 in August, its highest level ever in the series’ 45-year history.

“As the tax and regulatory landscape changed, so did small business expectations and plans,” commented National Federation of Independent Business (NFIB) president and CEO Juanita Duggan.

Against this background, Nobel laureate Robert Shiller told Bloomberg on Thursday that the market “could get a lot higher before it comes down… It’s highly priced, but it could get much more highly priced. It’s a risky market now.”

Time to Get Defensive?

Ray Dalio has a slightly different perspective. The billionaire founder of Bridgewater Associates, the world’s largest hedge fund, reminded investors this week that we’re in the “seventh inning” right now, and as such, investors should probably get “more defensive.” Last week, I shared with you that the global purchasing manager’s index (PMI) is steadily slowing down, falling to a 21-month low of 52.5 in August.

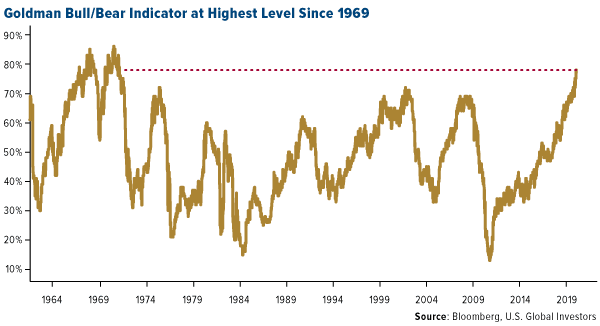

Again, markets have been relatively tranquil for a while now, but just as people on the East Coast were urged to prepare in anticipation of Hurricane Florence, now might be the time to adjust your portfolio in advance of a possible market downturn. This week, Goldman Sachs reported that its bull/bear indicator, which gauges the likelihood of a bear market, climbed to its highest point since 1969.

Goldman analysts point out, however, that the indicator could be read to mean not that a bear market is right around the corner, but that a period of lower returns could be expected.

One of the ways investors could batten down the hatches, so to speak, is with gold, which historically has performed very well in September as we approach Diwali and the Indian wedding season. This week I had the privilege to join Liz Claman on FOX Business’ Countdown to the Closing Bell, and I told her that, under the circumstances, gold is doing exceptionally well. The precious metal may be under pressure from a strong U.S. dollar and higher Treasury yields, but in Japan, Germany and elsewhere, government bond yields are negative, which has boosted gold demand.

While I’m here, I’d like to congratulate Liz and her show—Countdown placed in the top four business news programs this past quarter, reaching nearly 230,000 viewers, according to Nielsen Media Research. Liz continues her reign as the highest-rated female business news anchor on television. I’m very honored to be able to share my views with her and her audience, and to have appeared in her 2007 book, The Best Investment Advice I Ever Received.

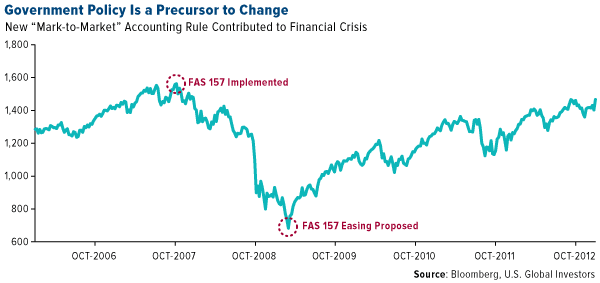

What Caused the Lehman Brothers Bankruptcy: A New Accounting Rule

Among the most eye-opening comments Valukas made during his interview is that “the federal government knew everything Lehman was doing—its risk exceedances [and] the fact that they did not have a liquidity pool.” According to Lehman’s 10-K from November 2007, the bank was leveraged an incredible 30.7 times its net worth, up dramatically from 23.7 times only four years earlier.Before my interview, Liz spoke with the very man who was called in to conduct forensic accounting on Lehman Brothers’ bankruptcy, Anton Valukas. The fourth-largest U.S. bank at the time of its demise, with $85 billion worth of mortgage-backed securities, Lehman resulted in global market-cap erosion of $10 trillion in October 2008 alone.

“Why were there no prosecutions or civil suits?” Valukas asked. Simply put: “The government knew.”

Some of the blame is also owed to an accounting rule, FAS 157—also known as “mark-to-market,” or “fair value accounting”—that was enacted in November 2007. A year later, after Lehman had sent global markets in a tailspin, FAS 157 was already being fingered by some as the culprit. William Isaac, the former chairman of the Federal Deposit Insurance Corporation (FDIC), said before the Securities and Exchange Commission (SEC) that the bankruptcy was “due to the accounting system, and I can’t come up with any other explanation.” Steve Forbes, chairman of Forbes Media, called mark-to-market accounting the “primary reason” for the meltdown.

I’m in agreement, writing back in March 2009 that “a case could be made that the convergence of FAS 157, highly leveraged balance sheets and the loss of the uptick rule were the trigger that set off the financial meltdown.”

The Financial Accounting Standards Board (FASB) proposed more lenient accounting guidelines in March 2009—the same month the market bottomed and began to recover. Coincidence?

So not only did the government allegedly allow the meltdown to happen, it then used taxpayer money to bail out the banks, which I believe exacerbated economic anxiety and sewed further distrust in the beltway party.

In my view, this contributed to two things: bitcoin, and the election of Donald Trump. Many people’s faith in traditional banking was obliterated, opening up the opportunity for a new type of currency, a cryptocurrency, to fill.

As for Trump, I wrote last year that the “bully,” as some call him, was elected to take on even larger bullies in the beltway party—career bureaucrats, regulators and other entrenched officials who make it their mission to oppose any Washington outsider who threatens to shake up the status quo. They were hostile to President Jimmy Carter, a fellow

The Short End Is Your Friend

On a final note, with interest rates on the rise, it’s important to stay on the short end of the yield curve when investing in fixed-income, as shorter-maturity yields are less sensitive to rate increases than longer-term bonds. This is one of five reasons why I think it makes sense to invest in municipal bonds right now.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.92 percent. The S&P 500 Stock Index rose 1.16 percent, while the Nasdaq Composite climbed 1.36 percent. The Russell 2000 small capitalization index gained 0.50 percent this week.

- The Hang Seng Composite gained 0.72 percent this week; while Taiwan was up 0.19 percent and the KOSPI rose 1.61 percent.

- The 10-year Treasury bond yield rose 5 basis points to 2.99 percent.

Domestic Equity Market

Strengths

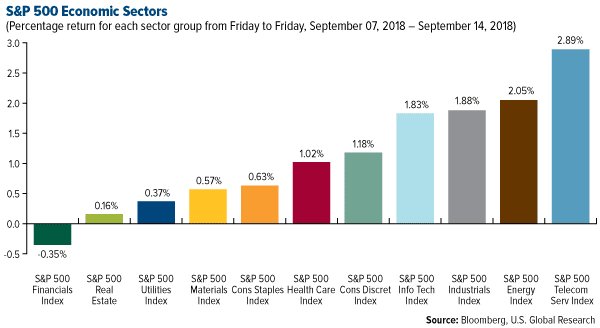

- Telecommunications was the best performing sector of the week, increasing by 2.89 percent versus an overall increase of 1.18 percent for the S&P 500.

- Advanced Micro Devices was the best performing stock for the week, increasing 19.50 percent.

- Advanced Micro Devices shares have experienced remarkable growth recently. Jim Kelleher, an analyst at Argus, just increased his price target on AMD shares from $23 to $40. FBN Securities came to a similar conclusion on Thursday when it also set a price target of $40 and initiated an outperform rating.

Weaknesses

- Financials was the worst performing sector for the week, decreasing by 0.35 percent versus an overall increase of 1.18 percent for the S&P 500.

- Kroger was the worst performing stock for the week, falling 14.12 percent.

- Insurance and construction stocks have taken a beating ahead of Hurricane Florence. Companies like Travelers and Summit Materials have fallen as traders anticipate damage from Florence.

Opportunities

- On Wednesday, Apple unveiled three new iPhones — the XS, the XS Max, and the XR — and a next-generation Apple Watch Series 4. Reportedly, the Series 4 contains new features intended to aid older wearers, such as an EKG sensor and fall detection.

- Tobacco stocks surged after the Food and Drug Administration (FDA) threatened to pull flavored e-cigarettes if the industry did not take steps to combat the “epidemic of e-cigarette use among teenagers.” Altria and British American Tobacco gained more than 6 percent each.

- Citigroup has created a Digital Asset Receipt for customers who want to invest in cryptocurrencies without owning them. This system would move cryptocurrencies into an existing regulatory structure, allowing big Wall Street investors to get exposure to the new asset class without accepting all the risks of investing directly.

Threats

- Electric-car maker Nio went public on Wednesday and, within 24, their shares soared 75 percent. This remarkable rise occurred despite Robin Zhu of Bernstein giving the shares an “underperform” rating and stating he believed a capital raise was coming within 12 and 18 months.

- The internet may radically change now that European politicians have backed controversial, new copyright legislation. If this comes into effect, tech giants will have to pay to link to journalistic articles and scan uploaded content for any copyright breaches.

- Attorney General Jeff Sessions is reportedly open to investigating social media companies for anti-competitive behavior and issues regarding free speech, according to Bloomberg. Later this month, he will meet with state attorney generals, who have already begun their own investigations.

The Economy and Bond Market

Strengths

- American confidence in the U.S. economy rose at the end of the summer and reached a near 14-year high, according to a survey of consumer sentiment. The University of Michigan’s consumer sentiment index rose to 100.8 in September from 96.2, based on a preliminary reading. This is the second highest level since 2004, trailing only the results in March.

- U.S. industrial production rose 0.4 percent in August, boosted by gains in the production of automobiles, oil and natural gas. The median forecast of economists surveyed by Bloomberg was a 0.3 percent gain.

- Business inventories in the U.S. increased in line with economist estimates in the month of July, the Commerce Department revealed in a report released on Friday. The Commerce Department said business inventories climbed by 0.6 percent in July.

Weaknesses

- U.S. retail sales rose by less than forecast in August as purchases of automobiles and clothing fell. The value of overall sales climbed 0.1 percent from the prior month, Commerce Department figures showed Friday. The median forecast of economists surveyed by Bloomberg called for a 0.4 percent gain.

- The U.S. government had a $214 billion budget deficit in August, representing almost double the amount for the same period last year as outlays swelled, according to Treasury Department data released on Thursday. Economists polled by Reuters had forecast the Treasury posting a $156.5 billion deficit for the month.

- U.S. consumer prices rose less than expected in August as underlying inflation pressures appear to be slowing. The Labor Department said on Thursday that the Consumer Price Index (CPI) increased 0.2 percent last month after a similar gain in July. In the 12 months through August, CPI increased 2.7 percent, slowing from July's 2.9 percent rise. Persistently low inflation has been a concern throughout the economic recovery.

Opportunities

- September flash PMI surveys from IHS Markit will provide important signals for economic trends in the US and eurozone at the end of the third quarter. Prior data has indicated robust growth for both economies, indicative of third quarter annualized growth of just below 3 percent and 2 percent respectively.

- New York sits at number one on the list of the world's most attractive financial centers, according to the Z/Yen global financial centers index. It is followed by London and Hong Kong, in second and third place, respectively.

- Jeff Bezos is launching a $2 billion fund to support homeless families and education using Amazon's methods. In a statement, Bezos said that "the child will be the customer" when describing plans for early education schools.

Threats

-

The Goldman Sachs Bear/Bear Index, which is based on measures of equity valuation, growth momentum, unemployment, inflation and the slope of the yield curve, is now at a level last seen nearly 50 years ago. Although the economic indicator is at a level that has historically preceded bear markets, Goldman strategists have said that a long period of relatively low returns from stocks is more likely than a recession at this point.

- Next Wednesday, investors will be awaiting the release of August building permits and housing starts. The following day existing home sales data will be released. Weakness in the housing market is expected to continue.

- Hurricane Florence made landfall near Wilmington, North Carolina on Friday with sustained winds of 90 mph and will likely continue through the weekend. Significant economic damage could be sustained.

Gold Market

This week spot gold closed at $1,193.50 down $2.74 per ounce, or 0.23 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.33 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index closed up 0.44 percent. The U.S. Trade-Weighted Dollar reversed course this week and fell 0.41 percent, erasing the prior week’s gain.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-11 | Geremany ZEW Survey Current Situation | 72.0 | 76.0 | 72.6 |

| Sep-11 | Germany ZEW Survey Expectations | -13.0 | -10.6 | -13.7 |

| Sep-12 | PPI Final Demand YoY | 3.2% | 2.8% | 3.3% |

| Sep-13 | Germany CPI YoY | 2.0% | 2.0% | 2.0% |

| Sep-13 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Sep-13 | CPI YoY | 2.8% | 2.7% | 2.9% |

| Sep-13 | Initial Jobless Claims | 210k | 204k | 205k |

| Sep-13 | China Retail Sales YoY | 8.8% | -- | 8.8% |

| Sep-17 | Eurozone CPI Core YoY | 1.0% | -- | 1.0% |

| Sep-19 | Housing Starts | 1231k | -- | 1168k |

| Sep-20 | Initial Jobless Claims | 210k | -- | 204k |

Strengths

- The best performing metal this week was platinum, up 1.40 percent as hedge funds cut their bearish outlook in the futures market. Gold traders and analysts were bullish for a fourth week in a row, as measured by a Bloomberg survey. Gold futures had their biggest gain in two weeks after almost 22,000 December contracts changed hands on the Comex in New York in only 10 minutes as inflation data came in weaker than expected. Bloomberg writes that this is more than 11 times the 100-day average for that time of day. Spot gold nearly finished the week with a gain but prices drifted lower on Friday afternoon.

- U.S. job openings rose in July to a new record and the largest share of workers since 2001 quit their jobs. Job postings exceeded the number of unemployed people in July, which helps explain why wages rose subsequently in August at the fastest space in almost ten years. This labor market strength could push wages even higher, which typically leads to rising inflation – something that can be positive for the price of gold.

- According to the Perth Mint, demand for Australian bullion products rose in August for a second month in a row. Sales of gold coins and bars totaled 38,904 ounces last month, representing a 30 percent gain from the prior month and an increase of 68.2 percent from the same time last year. The Perth Mint also sold 520,245 ounces of silver in August, posting an increase of 6.9 percent from July and a 32.7 percent increase from August 2017.

Weaknesses

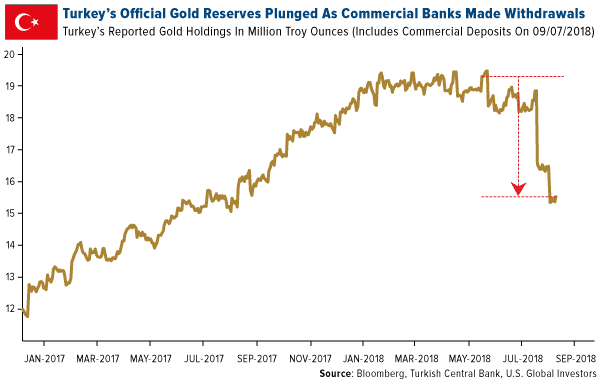

- The worst performing metal this week was silver, down 0.85 percent despite hedge funds cutting their bearish wagers on both silver and gold. As the lira continues to fall, commercial lenders in Turkey have withdrawn as much as $4.5 billion in gold reserves in an effort to avert a liquidity crisis. Bloomberg writes that weekly holdings, as reported by the Central Bank of Turkey, have fallen by almost one fifth since June 15 to 15.5 million ounces. Perhaps the selling from Turkey has dampened the seasonal fall rally in gold.

- Reuters reports that dealers in India have been offering gold at a discount for the first time in over a month, as an uptick in local rates moderated demand. India, the world’s second largest consumer of gold, saw the yellow metal being sold at up to a $2 per ounce discount over official domestic prices this week, compared with a premium of $1 last week. There is a 10 percent import tax on the yellow metal in India.

- U.S. core inflation, CPI, unexpectedly slowed in August as apparel prices fell by the most in seven decades and medical care costs declined. Inflation slowed to a 2.7 percent annual gain, down from 2.9 percent in July. Kevin Cummins, senior U.S. economist at NatWest Markets, said that “the broader trend in inflation is that it’s moved higher from where it had been, but any worry of an outbreak or idea that inflation will break out – this data casts some doubt on that.” U.S. producer prices also fell unexpectedly last month, for the first drop in 18 months, according to a Labor Department report this week. Bloomberg’s Katia Dmitrieva writes that the data suggests inflationary pressures may be taking a breather even as most signs of economic growth remain strong.

Opportunities

- The timing could be right for several Australian gold companies to look into acquisitions. Bloomberg notes that Australian gold stocks have outperformed their Toronto-listed peers by 23 percent over the last 12 months due to their wide operating margins and strong cash positions, among other factors. Analysts at Ord Minnett wrote in a note this week that Newcrest Mining, Evolution Mining and Northern Star Resources are the most likely to be looking at potential acquisitions in North America in the next year. Northern Star recently acquired the Pogo Mine in Alaska. Ramelius Resources made an all-share takeover offer for a smaller rival and is on the lookout for more asset acquisitions, according to its CEO and Managing Director Mark Zeptner.

- Shandong Gold Mining, a Shanghai-listed producer and China’s second-largest gold miner by market value, is offering 327.7 million new shares for a first-time share sale in Hong Kong that could raise as much as $767, reports Bloomberg’s Crystal Tse. Rival gold producer Zhaojin Mining Industry is one of five companies who have agreed to buy stock in the offering. This comes as the Hang Seng Index has entered a bear market and Shandong’s shares having fallen 24 percent year to date. Proceeds from the offering my allow Shandong to purse an acquisition. Canadian miner New Gold is working with BMO Capital Markets to find a buyer as they’re exploring selling and other options, reports Reuters.

- The ratio of Comex paper claims to physical gold continues to rise, currently at 325 to 1 versus the average of 152 to 1 year-to-date. The percentage of gold available for delivery as a percentage of total COMEX gold inventory is down to 1.73, versus 12 percent at the beginning of the year and the five-year average of 9.82 percent. With such a limited supply of physical gold to potentially settle trades, a short squeeze could materialize.

Threats

- South Africa’s gold mining industry continues to hit speed bumps. More than 50 people have died in the country’s mines so far this year, similar to the levels seen in 2017. Although far below the 615 deaths recorded in 1993, 2017 marked the first rise in deaths in a decade. Most gold mining fatalities are due to workers being crushed under falling rocks, which can be caused by more frequent tremors as companies dig deeper to find more gold. The government is investigating Sibanye Gold operations, as over half the gold mining deaths have occurred at their mines this year. Production of the yellow metal has contracted 15 percent from a year earlier, according to Statistics South Africa. This represents a tenth consecutive monthly drop in production in South Africa. Platinum-group metals production has also fallen 6.2 percent from a year earlier and total mining output is 5.2 percent lower, reports Bloomberg’s Renee Bonorchis.

- Well-known hedge fund manager Ray Dalio said in an interview on Bloomberg TV this week that the U.S. is probably two years away from its next downturn. Dalio said that the current tax cut-driven stimulus will begin to fade in 18 months around the same time when the U.S. will increase borrowing to help pay off pensions, healthcare and other unfunded obligations. “Two years out is when I’m worried about. It’ll be more of a dollar crisis than a debt crisis, and I think it’ll be more of a political and social crisis,” said Dalio.

- The S&P 500 has gained 41 percent since the first post-economic crisis Federal Reserve rate hike in December 2015. This marks the longest rally ever during a tightening cycle, writes Bloomberg’s Sarah Ponczek. The downfall that often follows these rallies historically could be of concern as the second strongest rally came before the crash of 1987.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended September 14 was FUTURAX, which gained328.71 percent. Morgan Stanley will join other Wall Street firms in creating a way for clients to play the digital currency market, reports Bloomberg. The bank is planning to offer trading in “complex derivatives tied to the largest cryptocurrency,” according to a person familiar with the matter.

- The New York Department of Financial Services (NYDFS) approved the Gemini dollar on Monday, a stablecoin proposed by Tyler and Cameron Winklevoss, reports MarketWatch. The Gemini dollar will be backed by U.S. dollars held at State Street Bank, the article continues. In a press release on the matter, New York DFS Superintendent Maria T. Vullo reiterated New York’s commitment to fostering innovation while ensuring responsible growth.

- Those who are wary of the cryptocurrency space, particularly in regard to initial coin offerings (ICOs), may find solace in the latest ruling by a U.S. federal judge. According to the judge, the U.S. securities laws may now cover an ICO, a move that hands the government a legal victory to regulate “billions of dollars in cybercurrency offerings much like stocks,” Bloomberg reports. This ruling will help promote responsibility and anti-fraud action in the space.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended September 14 was HarmonyCoin, which lost 84.64 percent.

- Cryptocurrencies as a whole are going through a slump due to negative sentiment. Popular coin Ethereum fell more than 30 percent in the last seven days and fell over 8 percent on Wednesday to below $170, reports Business Insider. This is a level not seen since May 2017 when the coin began to surge for the year. CEO and founder of CryptoCompare.com, Charles Hayter, told Business Insider that “it’s a continuation of the story that ICOs are selling their raised funds which are adding to downward pressure. This has spooked the market and turned the dial up on negative sentiment.”

- Two securities linked to cryptocurrencies were temporarily suspended on Sunday by the U.S. Securities and Exchange Commission (SEC). As Bloomberg reports, the suspension cited investor confusion regarding assets. The suspension will last through September 20 for halted securities Bitcoin Tracker One and Ether Tracker One, the article continues.

Opportunities

- In order to accelerate use, blockchain startup Chain is being acquired by the for-profit arm of the Stellar Foundation, “merging an enterprise that’s signed up big financial firms as customers with a group that publicly advocates the technology’s adoption,” Bloomberg writes. Stellar’s Lightyear will merge with Chain under a new name, Interstellar, and now Chain clients like Visa and Nasdaq will be able to use Stellar’s network.

- In an interview over the weekend at the Ethereum Industry Summit in Hong Kong, co-founder of Ethereum Vitalik Buterin said that “1,000-times growth” in the cryptocurrency space is over. While some may call this prediction of a “ceiling in sight” as negative, Buterin explained that the next step will simply be to get people interested in the real applications of the blockchain industry, Bloomberg reports.

- Citigroup is said to be developing a new mechanism for trading cryptocurrencies, reports Bloomberg and according to a person with knowledge of the plans. This would put the bank at the forefront of Wall Street’s efforts to let clients bet on the largely unregulated market, the article continues. Citibank would act as an agent that issues digital asset receipts (DARs) which “enables trading by proxy without direct ownership of the underlying coins,” said the person with knowledge of the matter.

Threats

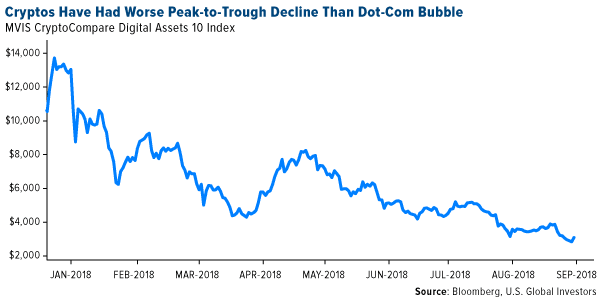

- Due to huge drop in cryptocurrency prices this week, many media outlets are now comparing the move to the dot-com bubble. The selloff in cryptocurrencies deepened into Thursday trading, with digital currencies dropping around 80 percent, reports Bloomberg. “The tumble has now surpassed the Nasdaq Composite’s 78-percent peak-to-trough decline after the dot-com bubble burst in 2000,” the article reads. The chart below shows how an index of the top 10 cryptocurrencies verifies such a comparison.

- The number of short orders placed on Ethereum reached a new record high on Wednesday, reports Coindesk.com. These “bearish bets” have risen by more than 200 percent in the past four weeks with prices hitting a 13-month low on Thursday of $167, the article continues.

- According to bitcoin analyst Jani Ziedins of CrackedMarket, the limited magnitude of bounces seen in the most popular digital currency is suggesting that a breach of critical support prices for cryptos could be imminent. “The trend is most definitely lower, but each bounce is still a selling opportunity,” Ziedins wrote in a recent blog article. “The worst is still ahead of us.”

Energy and Natural Resources Market

Strengths

- Iron ore was the best performing major commodity this week rising 0.6 percent. The commodity rallied after China announced it would not curb the capacity of steelmakers that meet low emission standards during this winter, suggesting demand for steelmaking iron ore may be stronger than expected.

- The best performing sector this week was the S&P/TSX Diversified Metals and Miners Index. The index rose 5.4 percent as miners were set for their best week since the end of July, after a weaker U.S. dollar and a softening of the trade war rhetoric lifted commodities.

- The best performing stock for the week was Ecopetrol SA. The Colombian integrated oil major rose 12.7 percent tracking higher oil prices, and following rumors that negotiations with its unions are progressing well and is likely the company will avoid a previously proposed labor strike.

Weaknesses

- Lumber was the worst performing commodity this week. The commodity dropped 4.2 percent after homebuilding stocks sank following a bearish call on Wall Street.

- The worst performing sector this week was the S&P 1500 Construction and Materials Index. The index dropped 0.4 percent as Hurricane Florence lumbers toward the East Coast. Analysts argue that the lack of customers due to evacuation orders and the stormy weather may weigh on construction order growth in the September quarter.

- The worst performing stock for the week was Siemens Gamesa Renewable Energy SA. The Spanish wind power manufacturer dropped 9.5 percent after Goldman said the company may be affected by a slowdown in new orders out of India.

Opportunities

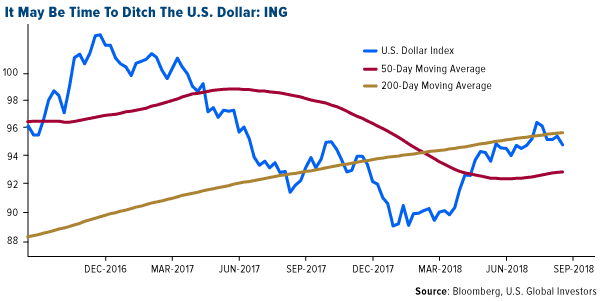

- Time to ditch the U.S. dollar as Trump's wars and the economy weigh, says ING Groep NV. Pro-cyclical factors that supported the U.S. dollar lately will likely go into reverse and the U.S. economy and stock markets “won’t be immune to any escalation in trade wars,” argue the bank’s strategists. On technical terms, the U.S. dollar also failed to reclaim the critical 96 level, and dropped back to 92.8 to find moving average support.

- Demand for physical delivery of metals in the U.S. is rising rapidly. This week, U.S. copper premiums rose to the highest since 2014 as users scramble to secure supply. Premiums to secure the metal rose to 7.5 cents per pound, the highest since at least 2014, on transport shortages and concerns over import duties.

- U.S. crude is trading at a big discount to global crude, handing domestic producers a golden opportunity to cash in on exports. The price gap is also expected to keep the U.S. energy industry firing on all pistons during the typically quiet fall season.

Threats

- Commodity ETFs saw their eighth consecutive week of outflows. Investors withdrew $156 million from ETFs that focus on commodities this week. Over the past eight weeks, outflows totaled $3.15 billion.

- China hit record low investment growth. The sluggishness of fixed asset investment for August disappointed economists, who had hoped for a stronger print resulting from Beijing’s fiscal impulse. The print was the slowest rate of growth in more than a quarter century.

- OPEC oil production surged last month, more than making up for the expected drop in Iranian crude exports. In its monthly report, the International Energy Agency said OPEC crude output climbed in August by 420,000 barrels a day, to average 32.63 million barrels a day. This marks the cartel’s biggest month-on-month increase in more than two years.

China Region

Strengths

- Thailand’s SET Index jumped 2.03 percent this week, and Vietnam’s Ho Chi Minh Stock Index climbed even further, rising 2.32 percent over the last five trading days.

- India’s exports reading clocked in up 19.2 percent year-over-year for the month of August, up from July’s reading of 14.3 percent.

- Energy was the top-performing sector this week in the Hang Seng Composite Index, rising 3.19 percent, just barely nudging out Information Technology, which rebounded and rose 3.15 percent for the week.

Weaknesses

- The Philippines Stock Exchange Index dropped 2.43 percent for the week.

- Philippine exports missed expectations this week, coming in at a year-over-year rise of only 0.3 percent for the most recent (July) measurement period, short of an anticipated 1.8 percent rise.

- Singapore’s year-over-year retail sales fell 2.6 percent for the July period, well short of analysts’ expectations for a 0.7 percent gain and down from the prior revised growth rate of 2.2 percent.

Opportunities

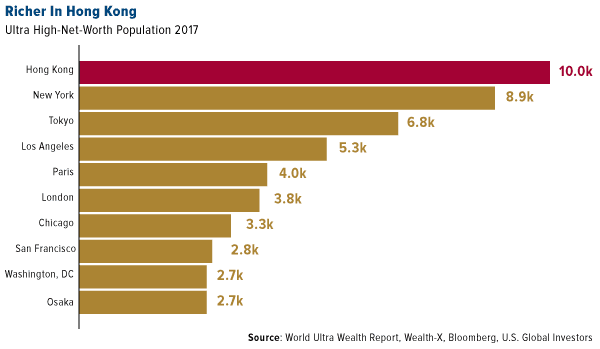

- Move over, New York. Hong Kong has now surpassed NYC as home to the ultra-rich people (defined as individuals worth at least $30 million), according to a recent Bloomberg News story. Nowhere in mainland China made the top 10 list, which was rounded out by third place Tokyo and then on down to Los Angeles, Paris, London, Chicago, San Francisco, Washington D.C. and Osaka.

- There is more speculation that a follow-up U.S.-North Korea/Trump-Kim summit—perhaps with South Korea as well—could occur, possibly as soon as October, according to media reports this week following the receipt at the White House of a letter from Kim Jong Un.

- On the bright side of things, a new round of U.S.-China trade talks is welcome and may well avoid further escalation and retaliation between the two economic juggernauts.

Threats

- However, to some degree trade war concerns must remain an ongoing threat. U.S. President Donald Trump reportedly instructed aides to proceed with tariffs on roughly $200 billion of Chinese goods, despite the new round of trade talks with China. The U.S. imported $505 billion in goods from China in 2017, and has already imposed 25 percent tariffs on $50 billion worth of goods.

- At least two large brokerage houses this week cut their expectations for Macau on concerns over a possible slowdown in revenue growth and VIP gaming expenditures.

- Investor concern over any broad slowdowns or emerging markets risks could continue to have outsized effects upon countries deemed to be at risk.

Emerging Europe

Strengths

- Czech Republic was the best performing country this week, gaining 2.4 percent. The central bank indicated that there is no reason to delay another rate hike since the economy is strong. The next policy meeting will take place on September 26 with a 25 basis point rate hike to 1.5 percent likely.

- The Turkish lira was the best relative performing currency this week, gaining 4.1 percent against the dollar. The Central Bank of Turkey hiked rates by 6.25 percent, from 17.75 percent to 24.0 percent, far above the expected increase of 3.25 percent.

- Telecom Service was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 2.5 percent. The European Union Parliament voted in favor to initiate the sanctions process that could potentially strip Hungary of its voting rights for not adhering to European Union values.

- The Hungarian forint was the worst relative performing currency this week, gaining 60 basis points against the dollar. The EU has added pressure on local equities and the nation’s currency due to the initiation of sanctions procedures.

- Health care was the worst performing sector among eastern European markets this week.

Opportunities

- The Central Bank of Europe (ECB) left rates unchanged and reiterated its policy plan to halve asset purchases in the fourth quarter then end it at the close of the year. ECB President Draghi sounded more optimistic, saying that the risks to growth are broadly balanced. He also emphasized the continued improvement in the labor market and rising wages. The euro moved higher against the dollar after the central bank announcement.

- Chinese e-commerce giant Alibaba and Russian technology group Mail.ru announced a joint venture along with the Russian sovereign wealth fund and MegaFon. The new company will be named AliExpress. Alibaba will own 48 percent of the company with MegaFon owning 24 percent, Mail.ru owning 15 percent and the sovereign wealth fund owning 13 percent. This is a step forward to digitalize Russia and develop an e-commerce platform. Regional trade group Ecommerce Europe estimated in 2016 that only 20 percent of Russians shop online.

- Reuters, citing German Interior Minister Horst Seehofer, said that Germany has reached a deal with Italy to return migrants who have already applied for asylum that is expected to be signed soon. The deal is part of a compromise between German Chancellor Merkel’s Christian Democrats and Seehofer’s Bavarian Christian Social Union and appears to resolve their dispute over returning migrants that nearly brought down the government.

Threats

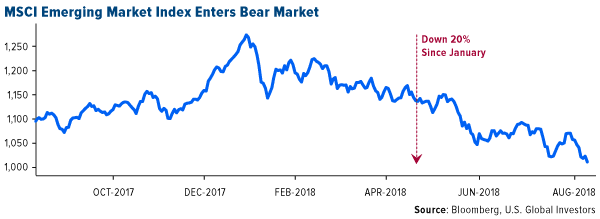

- The MSCI Emerging Market Index has lost 20 percent of its value from its peak in January, entering bear market territory. The weakness may continue as fear of more trade tensions and further Fed tightening may push emerging market equities lower.

- Eurozone industrial production dipped in July by 0.1 percent on the year compared with expectations for a 1 percent gain, signaling weakness in the third quarter. The seasonally adjusted output was more sluggish than anticipated, falling by 0.8 percent compared to the prior month, versus forecasts of a 0.5 percent drop.

- Russia’s foreign reserves rose to a multi-year high of $460.4 billion in August. Reserves cover nearly 16 months of imports and are around four times the stock of short-term external debt, according to Win Thin from the BBH Global Currency Strategy Team. In the short term, Russia may be covered for its financing needs. However, in the longer term, if the U.S. imposes more sanctions that cuts off Russia’s access to global capital markets, it may have a significant impact on corporate Russia. If state-owned companies could no longer service their debt, the government would have to step in, draining foreign reserves.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 3.00 | +0.06 | +1.90% |

| DJIA | 26,154.67 | +238.13 | +0.92% |

| Gold Futures | 1,199.10 | -1.30 | -0.11% |

| Hang Seng Composite Index | 3,680.19 | +26.23 | +0.72% |

| Korean KOSPI Index | 2,318.25 | +36.67 | +1.61% |

| Nasdaq | 8,010.04 | +107.50 | +1.36% |

| Natural Gas Futures | 2.77 | -0.01 | -0.36% |

| Oil Futures | 68.95 | +1.20 | +1.77% |

| Russell 2000 | 1,721.72 | +8.54 | +0.50% |

| S&P 500 | 2,904.98 | +33.30 | +1.16% |

| S&P Basic Materials | 371.61 | +2.10 | +0.57% |

| S&P Energy | 545.87 | +10.94 | +2.05% |

| S&P/TSX Global Gold Index | 151.95 | -0.71 | -0.47% |

| S&P/TSX VENTURE COMP IDX | 715.16 | +3.10 | +0.44% |

| XAU | 63.36 | +0.32 | +0.51% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 3.00 | +0.13 | +4.68% |

| DJIA | 26,154.67 | +992.26 | +3.94% |

| Gold Futures | 1,199.10 | +14.10 | +1.19% |

| Hang Seng Composite Index | 3,680.19 | -17.77 | -0.48% |

| Korean KOSPI Index | 2,318.25 | +59.34 | +2.63% |

| Nasdaq | 8,010.04 | +235.92 | +3.03% |

| Natural Gas Futures | 2.77 | -0.17 | -5.92% |

| Oil Futures | 68.95 | +3.94 | +6.06% |

| Russell 2000 | 1,721.72 | +51.05 | +3.06% |

| S&P 500 | 2,904.98 | +130.96 | +4.72% |

| S&P Basic Materials | 371.61 | +10.39 | +2.88% |

| S&P Energy | 545.87 | +16.28 | +3.07% |

| S&P/TSX Global Gold Index | 151.95 | -6.53 | -4.12% |

| S&P/TSX VENTURE COMP IDX | 715.16 | +47.28 | +7.08% |

| XAU | 63.36 | -2.70 | -4.09% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 3.00 | +0.06 | +2.08% |

| DJIA | 26,154.67 | +979.36 | +3.89% |

| Gold Futures | 1,199.10 | -121.70 | -9.21% |

| Hang Seng Composite Index | 3,680.19 | -548.00 | -12.96% |

| Korean KOSPI Index | 2,318.25 | -105.23 | -4.34% |

| Nasdaq | 8,010.04 | +249.00 | +3.21% |

| Natural Gas Futures | 2.77 | -0.20 | -6.71% |

| Oil Futures | 68.95 | +2.06 | +3.08% |

| Russell 2000 | 1,721.72 | +36.99 | +2.20% |

| S&P 500 | 2,904.98 | +122.49 | +4.40% |

| S&P Basic Materials | 371.61 | -5.19 | -1.38% |

| S&P Energy | 545.87 | -13.43 | -2.40% |

| S&P/TSX Global Gold Index | 151.95 | -42.00 | -21.66% |

| S&P/TSX VENTURE COMP IDX | 715.16 | -46.10 | -6.06% |

| XAU | 63.36 | -21.31 | -25.17% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2018):

MegaFon PJSC

Siemens Gamesa Renewable Energy SA

Evolution Mining

Northern Star Resources

Ramelius Resources

The Homes Depot Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The MVIS CryptoCompare Digital Assets 10 Index is a modified market cap-weighted index which tracks the performance of the 10 largest and most liquid digital assets.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

A basis point, or bp, is a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01% (0.0001).

The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money.

The Goldman Sachs bull/bear indicator takes into account five factors: growth momentum (measured by the average percentile for U.S. ISM indexes), the slop of the yield curve, core inflation, unemployment and stock valuations as measured by the Shiller price-earnings multiple.

The Global Financial Centers Index (GFCI) is a ranking of the competitiveness of financial centers based on over 29,000 financial center assessments from an online questionnaire along with over 100 indices from various organizations. It is published by Z/Yen and the China Development Institute.

The S&P/TSX Global Mining Index provides investors with a benchmark for global mining portfolios and a basis for innovative, index-linked investment vehicles. Eligible securities are classified under five GICS sub-industries: Aluminum, Diversified Metals & Mining, Gold, Precious Metals & Minerals, and Coal & Consumable Fuels.

The S&P Composite 1500 Materials Index comprises those companies included in the S&P Composite 1500 that are classified as members of the GICS materials sector.

The Bangkok SET Index is a capitalization-weighted index of all the stocks traded on the Stock Exchange of Thailand.

The Philippine Stock Exchange PSEi Index is a capitalization-weighted index composed of stocks representative of the Industrial, Properties, Services, Holding Firms, Financial and Mining & Oil Sectors of the PSE.

The COMEX is a commodity exchange in New York City formed by the merger of four past exchanges. The exchange trades futures in sugar, coffee, petroleum, metals and financial instruments.

The Michigan Consumer Sentiment Index (MCSI) is a monthly survey of U.S. consumer confidence levels conducted by the University of Michigan. It is based on telephone surveys that gather information on consumer expectations regarding the overall economy.

The NFIC Small Business Optimism Index is compiled from a survey that is conducted each month by the National Federation of Independent Business (NFIB) of its members.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All