Empire of Debt

Debt in Pictures

Wargaming the Trade War

Some Thoughts on Getting Through the Great Debt Reset

San Francisco, Frankfurt, and Puerto Rico?

With all the trade war talk, we all ask the obvious question: Who will win? President Trump says the US will win. Chinese business leaders say no, we will win. Free-traders on both sides say no one will win. Few stop to ask, “What does a ‘win’ look like?”

This makes discussion difficult. People are chasing after a condition they can’t even define. Victory will remain elusive until they know what they want. Regardless, you can score me on the “no one wins” side. I believe, and I think a lot of evidence proves, that free trade between nations is the best way to maximize long-run prosperity for everyone.

However…

As Keynes famously said, we’re all dead in the long run. Trade war may end with no winners, but the parties will be better and worse off at various times as it progresses. So we have to distinguish between “winning” and “holding a temporary lead.”

On that basis, I think the US will have the upper hand initially, and could hold it for a year or two. This is because, for now, our economy is relatively strong and we can better withstand any Chinese retaliation. Beyond that point I think our current policies will begin to backfire, maybe spectacularly.

Remember, too, China has growing trade surpluses with much of the world. One Chinese insider told me that within four years China can replace lost US exports via increased trading with the rest of the world. I can’t verify that but looking at general statistics it certainly seems plausible. That doesn’t mean lost US trade won’t be felt, but China is not entirely helpless.

When watching a fight, we ask metaphorically, “Who will blink first?” In this case, that’s the wrong question. Neither side will blink but one may eventually fall to the floor, unconscious. So the better question might be, “Who will faint first?”

Next week we will deal with the tariff situation, as I get that question a lot. But let me state right here: I hope President Trump is engaged in a trade bluff and not a trade war. The market seems to think so. My Asian sources believe that it will be resolved by the end of this year. But make no mistake, an actual trade war along the lines being threatened will impact both economies negatively. Enough to throw the US into recession? Enough to cut Chinese growth in half? No one actually knows, which is a big part of the problem.

Before we proceed, let me remind you that Over My Shoulder members get to see some of the best China and trade war research I get from my worldwide sources. It’s almost like reading, well, over my shoulder.

Better yet, members get short summaries of each item by me or my co-editor Patrick Watson. This saves you time and lets you zero in on the material that’s most relevant to you… a valuable feature as we are all deluged with more and more news.

Right now you can join for just $9.95 a month, 33% off the normal cost. I’ve written a short report to show you how valuable Over My Shoulder is, with some examples from Woody Brock, Charles Gave and Ed Yardeni. Check it out here. I think you’ll see the benefit.

Now, let’s dig into China.

Empire of Debt

I described in my last two letters the many good things happening in China. Businesses are prospering while living standards rise as well. The country’s vast interior is still quite poor but life is improving (with the notable exception of the Uighurs, a Muslim minority in Western China).

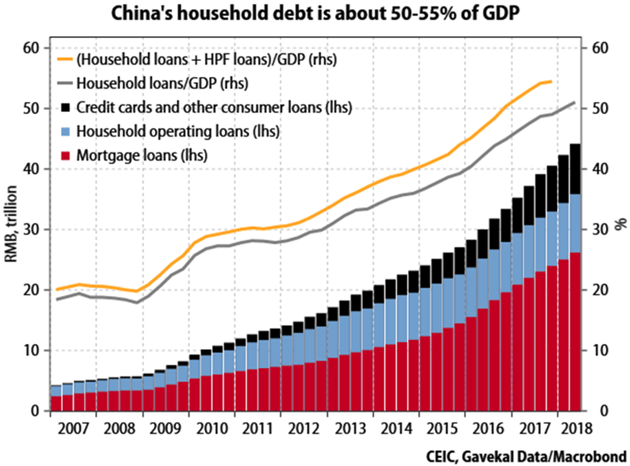

We didn’t talk about how they are financing this progress. The answer is, “with a lot of debt.” You often hear about China’s government and corporate debt, but less about households. So let’s start there.

Back in 2015, I wrote about China’s insanely leveraged farmers and others who bought stocks with borrowed money. Most regretted it, some sooner and more intensely than others. But that period seemed to convince the government to keep tighter control over consumer credit.

But note, controlling credit isn’t the same as eliminating credit, or even reducing it. Beijing wants consumers to borrow in sustainable, productive ways, as Beijing defines them. So overall household debt growth has not slowed.

Source: Gavekal

Source: Gavekal

Chinese consumer debt is growing quite a bit faster than Chinese GDP. This means that consumer debt is a growing percentage of the economy. It’s not a big problem now but at this rate will become one soon.

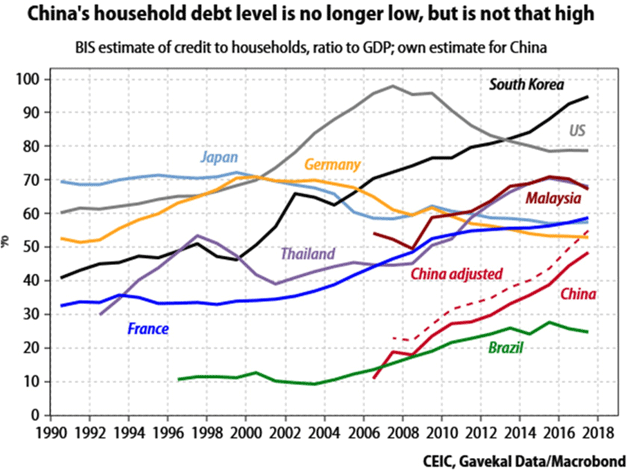

This chart shows how Chinese household debt is growing compared to other economies.

Source: Gavekal

Household debt relative to GDP is near-flat or declining in the US, Japan, Germany, and France. In China, it’s grown from 40% to 50% of GDP in just two years. Yes, those developed countries have higher absolute debt levels, but they also have higher household incomes. So this trend, if it continues, will get more worrisome.

Now, what happens when these indebted Chinese consumers find living costs rising due to a trade war with the US?

One possibility is “not much” because they don’t really need our goods. They have plenty of domestic alternatives in most categories. Nevertheless, removing or limiting US competition could raise prices in some categories.

But the bigger problem is that a trade war will mean lower exports, probably affecting the jobs of some indebted consumers. How many is unclear. China has both domestic demand and other countries it can trade with, should the US decide to raise barriers. Domestic demand might weaken if exporters have to reduce employment and the government doesn’t step in with some kind of stimulus.

The problem here is that any stimulus would probably increase government debt, a problem we haven’t even discussed yet. Not to mention corporate debt rising as companies try to keep operating with lower revenue.

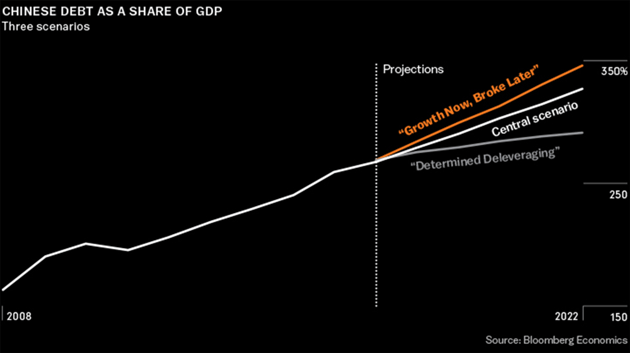

Debt in Pictures

Like everything else about China, its debt is hard to visualize. There’s a lot of it. Here is a chart from Bloomberg that projects three scenarios out to 2022.

Source: Bloomberg

Bloomberg’s base case shows Chinese debt-to-GDP reaching 330% by 2022, which would place it behind only Japan among major economies. It might be “only” 290% if GDP growth stays high.

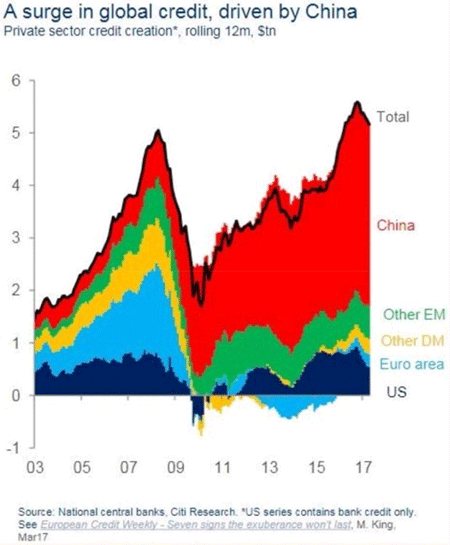

Here’s another look from Citi Research (via my friend Steve Blumenthal). This is private sector credit creation. The US series is only bank credit, by the way, so this isn’t an apples-to-apples comparison. But then much of Chinese debt is bank credit. The “shadow banks” are relatively new. Xi seems to be trying to reduce their influence. However you look at it, China has huge private debt.

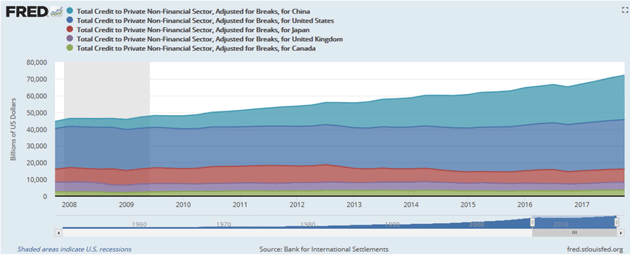

Finally, here’s a “Total Credit to Private Non-Financial Sector” graph we made on FRED using Bank for International Settlements data. That means it excludes bank debt. The US has the most such debt at $29.5T as of year-end 2017, but China is not that far behind with $26.5T. China’s debt of this type was quite a bit more than Japan, the UK, and Canada combined.

Source: St. Louis Federal Reserve Bank

Even so, Chinese growth has been largely funded by debt. Make no mistake, loans have fueled almost everything. You can argue those loans have funded a great deal of useful infrastructure and housing, with a stimulative effect. But that debt will eventually have to be repaid, and debt is future consumption brought forward. That means at some point Chinese growth is going to slow down. Maybe not for a decade or so, but they have to pay the piper.

Like the US, China also has off-the-books debt that may not show up in the totals. For instance, its social security plan is underfunded amid an aging population and shrinking prime-age workforce. The 29% payroll tax (yes, you read that right) that should be funding it often goes uncollected and the debt goes higher still. One analyst estimated strict enforcement would cut corporate profits by 2.5% and shave 0.6 percentage points off nominal GDP growth. With the Chinese government now making aggressive efforts to collect the tax, which it clearly needs, growth could falter.

Any way you look at it, China has a staggering amount of debt. Maintaining it will grow more difficult if the economy turns down. The same is true for the US, of course. Which country is better equipped to survive a trade and currency conflict?

Wargaming the Trade War

This week President Trump ordered more tariffs on an expanded list of Chinese imports. The rate will be 10% starting next week and rise to 25% at the beginning of 2019, unless China agrees to new trade policies before then. (Notably, he excluded consumer electronics products like smartphones, which shows the administration is not entirely tone deaf to the impact tariffs have on US consumers.)

Let me be very clear on one thing: I totally agree with the president that China has taken unfair advantage of global trade rules. Its requirements for foreign companies to disclose intellectual property (that then finds its way to Chinese state-owned enterprises) is outrageous. That must stop and we need to resolve assorted other differences. The question is how to accomplish it.

I had hopes Trump’s business negotiation skills would enable more productive trade negotiations. It doesn’t seem to be happening that way. To me, the best strategy would have been to assemble a united front of other top economies and demand China change its ways. We are not the only major country that has a trade problem with China. Then I would have pivoted to seeking better terms with Canada, Mexico, the EU, and others. Instead, he has aggravated allies and made working with them difficult, at best.

Part of negotiating is to have realistic demands. You will never succeed by demanding your adversary cut his own throat. Xi Jinping can be flexible on many things but he still presides over a Communist government and a command economy. That leopard is not going to change its spots. They are never going to abandon their technology goals embodied in their “Made in China 2025” program, nor would any other country.

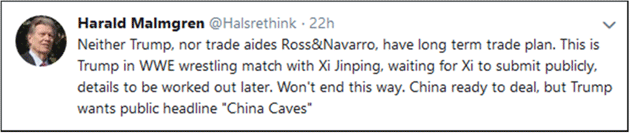

I am not the only one who thinks this. Check out this unusually blunt tweet from former trade diplomat Harald Malmgren, who literally wrote the book on US trade policy, serving under presidents starting with JFK. He’s retired now but remains “plugged in” to global finance better than almost anyone I know.

Source: Twitter

Now, it may be that the White House team is less talented than they think. Peter Navarro’s continued presence, and the president’s apparent confidence in him, is not reassuring. I said when his name was first mentioned that Navarro understands neither economics nor trade. He has done nothing to change my opinion.

But another possibility is they have an entirely different strategy than we think. Some of my contacts believe the real goal is to make US businesses pull back from operating in China at all. If that’s the goal, they are off to a good start. But that is not good for US businesses or for the US.

For the moment, the US side is negotiating from a marginally stronger position. Our economy is growing nicely and can withstand some tariff pain—though it will hurt certain sectors. This is already happening, in fact. But in the long run we are playing a very dangerous game.

International trade is like plumbing. Goods and money flow around through pipes and you can only squeeze so much through them. When the US imports goods from China, we simultaneously export dollars to China. We can do that because our currency is what everything else is settled in. Reducing imports would mean we also reduce dollar exports, leaving the rest of the world with less water in its pipes. That’s not good at all, if we want to maintain our position on top of the food chain.

In researching this letter, I ran across a nice, short explanation of the threat by currency expert Taggart Murphy. I can’t say it better myself so I’ll just quote him (emphasis mine).

Trump is doing everything he can to bring on the end of the days when the US can borrow whatever it wants in whatever amounts it wants. To be sure, there is no recipe book. The dollar is now so entrenched as the world’s money that if your assignment were to bring the curtain down on that—and thus the ability of the US to borrow whatever it wants whenever it wants—it’s not at all clear what you would do.

But you’d start by doing everything that Trump is doing—pick fights with all your allies, blow the government deficit wide open at the peak of an economic recovery, abandon any notion of fiscal responsibility, threaten sanctions on anyone and everyone who seeks to honor the deal Obama struck with Iran (thereby almost begging everyone to figure out some way to bypass the US banking system in order to do business), [Which they are openly doing –JFM] throw spanners into the works of global trade without any clear indication of what it is precisely you want for a country that structurally consumes more than it produces and thus by the laws of accounting MUST run trade and current account deficits.

That’s strong language but exactly right, especially the last part. Trade deficits are President Trump’s bugaboo, yet he might as well complain about the weather. It is what it is. The US will run a trade deficit unless we accept some combination of higher savings and lower consumption. That’s not my opinion; it’s math. Threatening China will not change it.

Trying to wean the US public off of consumption and force higher savings is just not going to work, either, which means we are going to run trade deficits.

But that is just fine. As long as we have the world’s reserve currency, we can run trade deficits with essentially no consequences. We aren’t comparable to Argentina or other countries that get into trouble because of their trade deficits. Nobody, not even their citizens, wants to hold the Argentine dollar or the Venezuelan bolivar.

This brewing trade war, if it continues, will initially favor the US but we will gradually lose the advantage as the rest of the world builds new pipes to bypass us. Something similar happened to the United Kingdom, our predecessor hegemon. We don’t know what a new world financial order would look like but the US dollar would not be on top of it.

This might be an interesting parlor game if it weren’t happening against the backdrop of populist politics, enormous debt, mass refugee migrations, and rapid technological change that could put millions out of work. Talk about “who wins” is really misleading.

Think about a boxing match. Who’s “winning” in the early rounds? Whoever threw the last punch is ahead for a moment. But then they take a punch and the lead changes. It’s only later in the match that you see which fighter has staying power.

I think the US-China trade war will be something like that. It will take a long time to see how it shakes out, and meantime we’ll see both sides alternately throwing and absorbing punches. The lead will change often and the winner could even be a third party that may not exist yet.

It is my fervent hope that China makes a genuine effort to reduce their most abusive practices, and that President Trump takes that for a “W” and calls off the tariffs. I think that is the most likely outcome. One of my most inside sources in China, whom I spoke with this week while he was in Shanghai, believes that to be the case, and most Chinese do, too. Which is why the markets are being rather sanguine about the whole process. We should learn more in the coming months.

Some Thoughts on Getting Through the Great Debt Reset

Debt is certainly one of the main challenges facing China and many nations around the globe today. The decades-long growth of debt in many countries from small, manageable levels to excessive levels is coming to an end. Bond markets will eventually rebel. We will have to restructure the debt and it will have a profound impact on how we meet future investment challenges.

As an investor, you will have to think differently to accumulate and maintain your wealth. If you’re an investment professional, you are entering one of the most disruptive periods the industry has ever seen. In either case, meeting these challenges will require thinking beyond a traditional stock-and-bond approach. Core holdings in the bull markets of our youth will no longer suffice in the future. Investors will need a better asset allocation approach. While I don’t talk about my own investment strategy in this letter very often, I think I owe it to you to tell you what I am doing for my clients. This is why I created the CMG Mauldin Smart Core Strategy.

Instead of using the traditional diversification approach, potentially resulting in a collection of across-the-board losers, the Mauldin Smart Core diversifies among trading strategies. The goal is to win by minimizing losses and having the flexibility to capitalize on market opportunities. The CMG Mauldin Smart Core Strategy is a tactical portfolio that follows a disciplined process, able to respond to the global economy on a daily basis. It utilizes four ETF strategists that trade a diversified basket of ETFs across asset classes, countries, sectors, fixed income, commodities, and cash.

The global debt super cycle is coming to an end and it will unfold in what I’m calling “The Great Reset.” I’ve just written a detailed report on how I think you should view your investments and why I believe Mauldin Smart Core can navigate the volatility coming to global financial markets. Download my free report, The Great Reset, here.

San Francisco, Dallas, Frankfurt, and Puerto Rico?

I’m making a quick trip to San Francisco tomorrow to meet with Jim Mellon, one of the smartest investors I know. Jim made his first billion in real estate and has now turned his attention to antiaging technologies. It looks like we will be working together on at least one venture, if not more.

After that meeting, I will turn around and be back in Dallas for two presentations in Dallas on October 4 at the Dallas Money Show, which happens to be on my 69th birthday. It’s at the Hyatt Regency Dallas so I hope to see you there. Then early in November I will be going to Frankfurt to do a presentation and either before or after that Shane and I will need to once again visit Puerto Rico.

I had such a great response to last week’s Art Cashin story, I’m going to close with another one. As he tells it:

In my very early days on Wall Street my income was rather small and I looked for other possible ways to seek fame and fortune. At the time, folk singers were very big—The Kingston Trio, Joan Baez, Bob Dylan, etc.

We formed a quartet and sang at bars and small clubs for a few months. Impatient, I talked our way into an audition with the Chairman of ABC-Paramount Records. We sang four songs for the Chairman and Chief A&R guy. When we finished, the Chairman said "you guys are really good! We just signed a guy from Atlantic Records. If he doesn’t work out, we'll do an album and send you on a national tour."

The guy from Atlantic Records was named Ray Charles—and that was the end of my singing career.

I also tried to sing but I was merely a good amateur. I was a high tenor and sang solos in Handel’s Messiah, high school musicals, chorales, quartets, folk rock groups. I even sang with the Fort Worth Opera chorus. I enjoyed being a tenor, then nasal surgery in my 40s turned me into a baritone and I couldn’t carry a tune.

I miss singing. Now, when I am alone, sometimes I go to YouTube, find some music and sing. Off-key or not, it just feels good. With that, I will hit the send button. You have a great week!

Your going-to-listen-to-folk-music-on-YouTube-this-weekend analyst,

John Mauldin

© Mauldin Economics

www.mauldineconomics.com

© Mauldin Economics

Read more commentaries by Mauldin Economics

Source:

Source:  Source:

Source:  Source:

Source:  Finally, here’s a “Total Credit to Private Non-Financial Sector” graph we made on FRED using Bank for International Settlements data. That means it excludes bank debt. The US has the most such debt at $29.5T as of year-end 2017, but China is not that far behind with $26.5T. China’s debt of this type was quite a bit more than Japan, the UK, and Canada combined.

Finally, here’s a “Total Credit to Private Non-Financial Sector” graph we made on FRED using Bank for International Settlements data. That means it excludes bank debt. The US has the most such debt at $29.5T as of year-end 2017, but China is not that far behind with $26.5T. China’s debt of this type was quite a bit more than Japan, the UK, and Canada combined. Source:

Source:  Source:

Source: