A persistent concern this year has been a flattening US Treasury yield curve, caused by long-term bond yields remaining low despite rising yields on shorter tenors. Flattening can lead to inversion, often a precursor of recessions.

We enter October with a steeper yield curve taking shape. As of this writing, the 10-year Treasury yield is solidly above 3%, a level not sustained since 2011. The bond market sell-off had no single explanation but appears to have been a confluence of robust US economic data, hawkish Fed commentary and inflation concerns among investors. Traders know this combination of circumstances as a "bull steepening."

Though the volatility in bond yields is jarring after an extended low interval, the drivers of the movement are generally positive. We expect continued Fed rate hikes and strong economic growth in 2018, followed by slower growth and fewer rate movements in 2019.

Key Economic Indicators

Influences on the Forecast

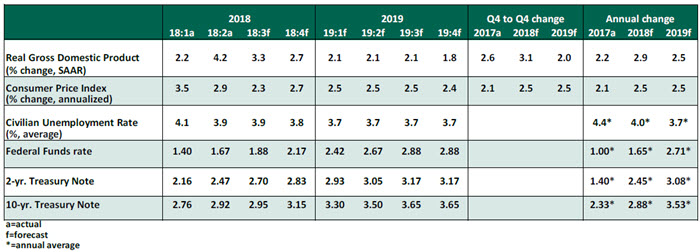

- To little surprise, the Federal Open Market Committee raised the Fed Funds target rate to 2.0%-2.25% at its meeting that concluded September 26. Fed watchers observed that the policy statement accompanying the decision no longer described U.S. monetary policy as "accommodative." But Fed Chairman Jerome Powell took care to note in a subsequent speech that interest rates were still well below their neutral level. We continue to forecast rate increases following the Fed's meetings in December, March, and June, at which time the rate will likely level off and allow the Fed time to observe the effects of higher rates.

- The September employment report showed the headline unemployment rate falling to 3.7%, a nearly 50-year low. However, the payroll gain was slower than most forecasters anticipated, with only 134,000 jobs created. At least some of this sluggishness can be attributed to slow hiring on the east coast in the aftermath of Hurricane Florence. Positive revisions to prior months' payrolls data helped to bolster the market's reaction to the report. As seasonal hiring gets underway for the holiday season, we expect continued increases to employment for the remainder of 2018.

- Wage growth continues but has yet to show the strength that a low unemployment rate would suggest. Average hourly earnings grew by 2.8% year-over-year in September, following a cycle-record high of 2.9% in August. Prominent employers have announced higher wage policies, suggesting another round of wage inflation has begun.

- Real gross domestic product (GDP) for the second quarter was affirmed at 4.2% annualized growth in its final estimate. We expect continued strength at a more tempered pace in the balance of the year as the export gains that boosted second quarter's GDP dissipate.